Aramco Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

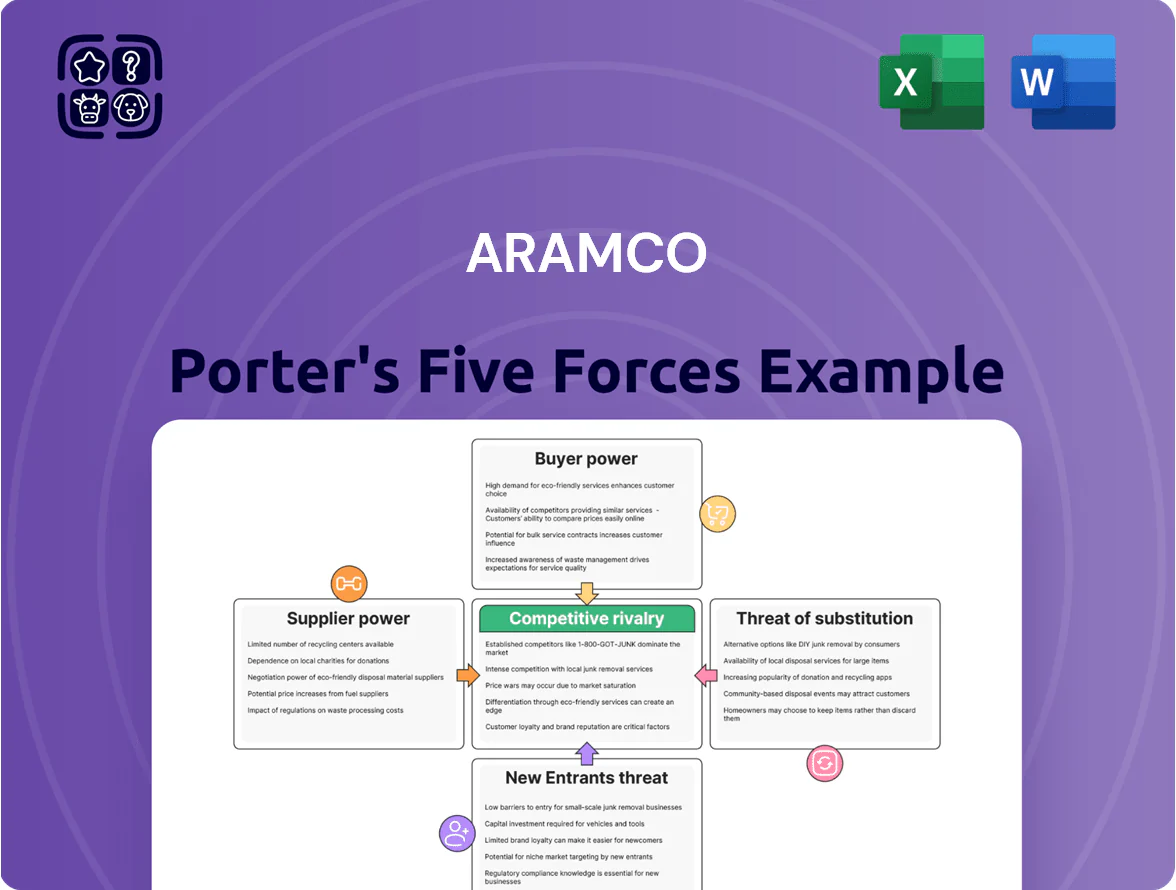

Suppliers Bargaining Power

Specialized Oilfield Service Providers

Aramco depends on high-tech services from SLB (Schlumberger) and Halliburton for complex drilling and reservoir management, firms that command higher margins—SLB reported $29.1B revenue in 2024.

However, Aramco’s mega contracts (often >$1B) and 2024 procurement spend of ~$50B give it strong bargaining power to push prices and terms.

Aramco’s iktva localization program aims 70% in-country value by 2025, cutting foreign supplier dependence and raising local supplier share, which weakens supplier power.

Technological and Digital Infrastructure Partners

The shift to AI-driven Smart Fields ties Aramco to cloud and analytics leaders like AWS, Microsoft Azure, and Google Cloud, who in 2024 held ~62% of global cloud market and thus wield moderate supplier power due to niche energy software and high ecosystem switching costs.

Aramco’s internal VC and R&D — including a $500m+ digital investment earmark in 2023 and in-house projects reducing third-party licenses by ~14% in 2024 — are lowering dependence and bargaining leverage.

Raw Materials for Chemical Expansion

Labor and Specialized Engineering Talent

The global shortage of petroleum engineers and sustainability experts raised average oilfield engineer salaries ~18% globally from 2020–2024; Aramco competes with oil majors and green-tech firms for talent, increasing human-capital costs and retention spend.

Aramco offsets pressure with prestige, higher pay, and multi-year training—its 2024 graduate program intake rose ~12%, keeping the skilled pipeline steady despite market competition.

- Global petroleum engineer shortage; pay up ~18% (2020–2024)

- Aramco 2024 graduate intake +12%

- Competes vs oil majors + green tech for specialists

- High wages, prestige, training reduce supplier (labor) power

Geopolitical and Logistics Infrastructure

Suppliers of maritime shipping and pipeline infrastructure are critical to Aramco’s export capacity; Saudi Arabia exported 9.6 million barrels per day in 2024, so logistic access matters for revenue and market share.

Aramco’s subsidiary Bahri owns ~70 tankers (2025), but third-party charters fill global gaps; long-term charters and alliances reduced spot-rate exposure after 2022–23 freight volatility.

Strategic contracts and pipeline stakes cut supplier power, yet concentrated global shipping routes and chokepoints keep supplier leverage moderate.

- 2024 exports: 9.6 mbd

- Bahri fleet: ~70 vessels (2025)

- Long-term charters lower spot risk

- Chokepoints sustain supplier leverage

Limited supplier clout vs concentrated pockets: Aramco $50B buys, SLB, cloud, catalysts

Suppliers hold limited overall power: Aramco’s ~$50B 2024 procurement, mega contracts (> $1B), iktva push to 70% local value by 2025, and in‑house digital/R&D cuts dependency. Moderate pockets of power exist with SLB/Halliburton (SLB $29.1B 2024), hyperscale cloud (~62% market 2024), specialty catalysts ($18.5B global 2024) and skilled labor (+18% pay 2020–24).

| Metric | Value |

|---|---|

| Procurement 2024 | $50B |

| SLB revenue 2024 | $29.1B |

| Cloud market 2024 | ~62% |

| Specialty catalysts 2024 | $18.5B |

| Engineer pay rise 2020–24 | +18% |

What is included in the product

Tailored exclusively for Aramco, this Porter's Five Forces overview uncovers competitive dynamics, supplier and buyer bargaining power, substitution threats, and entry barriers, highlighting disruptive risks and strategic levers that influence Aramco’s pricing power and long-term profitability.

A concise Porter's Five Forces snapshot for Aramco—quickly assess supplier, buyer, rivalry, entrant, and substitute pressures to guide strategic and investment decisions.

Customers Bargaining Power

Global Refineries and Industrial Buyers

National Governments and Strategic Reserves

National governments and state utilities buy oil for strategic reserves and energy security; in 2024 global strategic petroleum reserves held ~1.5 billion barrels, so sovereign purchases form a steady demand base for Aramco.

These buyers negotiate on geopolitical ties and long-term contracts—Saudi crude supplied under long-term deals can undercut spot volatility, with state contracts often spanning 3–10 years.

The customer base is stable but politically sensitive, requiring Aramco to balance diplomacy and commercial terms; delivery disputes or sanctions risks can shift volumes quickly.

Chemical and Manufacturing End-Users

As Aramco expands into chemicals, its customer base in plastics and manufacturing is more fragmented and price-sensitive, with global polymer resin buyers facing >200 global suppliers and spot resin prices swinging 20–30% year-on-year (2024).

Buyers can source alternatives from PDH/steam crackers in US, China, and Gulf, so bargaining power is moderate; Aramco offsets this by using low-cost gas liquids and integrated refining-chemicals scale to offer margins 3–5 percentage points above peers in 2024.

Retail Fuel Consumers

Retail fuel consumers face high bargaining power: motorists are price-sensitive and can switch stations over small price gaps or convenience; Aramco served ~3,500 service stations globally by end-2024, so local competition is intense.

Aramco counters with brand strength and integrated loyalty programs—reported retail margin capture rose ~12% in 2024 in markets using loyalty schemes—reducing churn and extracting downstream value.

- High price sensitivity — easy switching

- ~3,500 global stations (end-2024)

- Loyalty programs raised retail margin ~12% (2024)

- Location and convenience still key

Wholesale Energy Traders

Commodity traders and banks provide over $200 billion in global oil-market liquidity and drive short-term price discovery for Aramco’s grades, especially in spot and paper markets.

They rarely control Aramco’s long-term contracts, which covered about 70% of 2024 export volumes, so traders affect near-term spreads but not core revenue terms.

Aramco’s 2024 crude output ~10.1 mb/d and market share in Asia lets it set regional benchmark discounts rather than passively accept prices.

- Traders: key for liquidity, short-term prices

- Long-term contracts: ~70% of exports in 2024

- Aramco output: ~10.1 mb/d in 2024 → price setter in Asia

Aramco: Stable exports via long‑term contracts, retail margins up, traders set short spreads

| Metric | 2024 |

|---|---|

| Output | 10.1 mb/d |

| Exports via LT contracts | ~70% |

| Export volumes | ~6.5 mb/d |

| Global stations | ~3,500 |

| Strategic reserves | ~1.5 bn barrels |

What You See Is What You Get

Aramco Porter's Five Forces Analysis

This preview shows the exact Aramco Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples; it's fully formatted and ready for use.

You're looking at the final, professionally written document; once you complete your purchase, you'll get instant access to this identical file for download and application.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Suppliers Bargaining Power

Specialized Oilfield Service Providers

Aramco depends on high-tech services from SLB (Schlumberger) and Halliburton for complex drilling and reservoir management, firms that command higher margins—SLB reported $29.1B revenue in 2024.

However, Aramco’s mega contracts (often >$1B) and 2024 procurement spend of ~$50B give it strong bargaining power to push prices and terms.

Aramco’s iktva localization program aims 70% in-country value by 2025, cutting foreign supplier dependence and raising local supplier share, which weakens supplier power.

Technological and Digital Infrastructure Partners

The shift to AI-driven Smart Fields ties Aramco to cloud and analytics leaders like AWS, Microsoft Azure, and Google Cloud, who in 2024 held ~62% of global cloud market and thus wield moderate supplier power due to niche energy software and high ecosystem switching costs.

Aramco’s internal VC and R&D — including a $500m+ digital investment earmark in 2023 and in-house projects reducing third-party licenses by ~14% in 2024 — are lowering dependence and bargaining leverage.

Raw Materials for Chemical Expansion

Labor and Specialized Engineering Talent

The global shortage of petroleum engineers and sustainability experts raised average oilfield engineer salaries ~18% globally from 2020–2024; Aramco competes with oil majors and green-tech firms for talent, increasing human-capital costs and retention spend.

Aramco offsets pressure with prestige, higher pay, and multi-year training—its 2024 graduate program intake rose ~12%, keeping the skilled pipeline steady despite market competition.

- Global petroleum engineer shortage; pay up ~18% (2020–2024)

- Aramco 2024 graduate intake +12%

- Competes vs oil majors + green tech for specialists

- High wages, prestige, training reduce supplier (labor) power

Geopolitical and Logistics Infrastructure

Suppliers of maritime shipping and pipeline infrastructure are critical to Aramco’s export capacity; Saudi Arabia exported 9.6 million barrels per day in 2024, so logistic access matters for revenue and market share.

Aramco’s subsidiary Bahri owns ~70 tankers (2025), but third-party charters fill global gaps; long-term charters and alliances reduced spot-rate exposure after 2022–23 freight volatility.

Strategic contracts and pipeline stakes cut supplier power, yet concentrated global shipping routes and chokepoints keep supplier leverage moderate.

- 2024 exports: 9.6 mbd

- Bahri fleet: ~70 vessels (2025)

- Long-term charters lower spot risk

- Chokepoints sustain supplier leverage

Limited supplier clout vs concentrated pockets: Aramco $50B buys, SLB, cloud, catalysts

Suppliers hold limited overall power: Aramco’s ~$50B 2024 procurement, mega contracts (> $1B), iktva push to 70% local value by 2025, and in‑house digital/R&D cuts dependency. Moderate pockets of power exist with SLB/Halliburton (SLB $29.1B 2024), hyperscale cloud (~62% market 2024), specialty catalysts ($18.5B global 2024) and skilled labor (+18% pay 2020–24).

| Metric | Value |

|---|---|

| Procurement 2024 | $50B |

| SLB revenue 2024 | $29.1B |

| Cloud market 2024 | ~62% |

| Specialty catalysts 2024 | $18.5B |

| Engineer pay rise 2020–24 | +18% |

What is included in the product

Tailored exclusively for Aramco, this Porter's Five Forces overview uncovers competitive dynamics, supplier and buyer bargaining power, substitution threats, and entry barriers, highlighting disruptive risks and strategic levers that influence Aramco’s pricing power and long-term profitability.

A concise Porter's Five Forces snapshot for Aramco—quickly assess supplier, buyer, rivalry, entrant, and substitute pressures to guide strategic and investment decisions.

Customers Bargaining Power

Global Refineries and Industrial Buyers

National Governments and Strategic Reserves

National governments and state utilities buy oil for strategic reserves and energy security; in 2024 global strategic petroleum reserves held ~1.5 billion barrels, so sovereign purchases form a steady demand base for Aramco.

These buyers negotiate on geopolitical ties and long-term contracts—Saudi crude supplied under long-term deals can undercut spot volatility, with state contracts often spanning 3–10 years.

The customer base is stable but politically sensitive, requiring Aramco to balance diplomacy and commercial terms; delivery disputes or sanctions risks can shift volumes quickly.

Chemical and Manufacturing End-Users

As Aramco expands into chemicals, its customer base in plastics and manufacturing is more fragmented and price-sensitive, with global polymer resin buyers facing >200 global suppliers and spot resin prices swinging 20–30% year-on-year (2024).

Buyers can source alternatives from PDH/steam crackers in US, China, and Gulf, so bargaining power is moderate; Aramco offsets this by using low-cost gas liquids and integrated refining-chemicals scale to offer margins 3–5 percentage points above peers in 2024.

Retail Fuel Consumers

Retail fuel consumers face high bargaining power: motorists are price-sensitive and can switch stations over small price gaps or convenience; Aramco served ~3,500 service stations globally by end-2024, so local competition is intense.

Aramco counters with brand strength and integrated loyalty programs—reported retail margin capture rose ~12% in 2024 in markets using loyalty schemes—reducing churn and extracting downstream value.

- High price sensitivity — easy switching

- ~3,500 global stations (end-2024)

- Loyalty programs raised retail margin ~12% (2024)

- Location and convenience still key

Wholesale Energy Traders

Commodity traders and banks provide over $200 billion in global oil-market liquidity and drive short-term price discovery for Aramco’s grades, especially in spot and paper markets.

They rarely control Aramco’s long-term contracts, which covered about 70% of 2024 export volumes, so traders affect near-term spreads but not core revenue terms.

Aramco’s 2024 crude output ~10.1 mb/d and market share in Asia lets it set regional benchmark discounts rather than passively accept prices.

- Traders: key for liquidity, short-term prices

- Long-term contracts: ~70% of exports in 2024

- Aramco output: ~10.1 mb/d in 2024 → price setter in Asia

Aramco: Stable exports via long‑term contracts, retail margins up, traders set short spreads

| Metric | 2024 |

|---|---|

| Output | 10.1 mb/d |

| Exports via LT contracts | ~70% |

| Export volumes | ~6.5 mb/d |

| Global stations | ~3,500 |

| Strategic reserves | ~1.5 bn barrels |

What You See Is What You Get

Aramco Porter's Five Forces Analysis

This preview shows the exact Aramco Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples; it's fully formatted and ready for use.

You're looking at the final, professionally written document; once you complete your purchase, you'll get instant access to this identical file for download and application.