Arch Capital Group Boston Consulting Group Matrix

Unlock Strategic Clarity

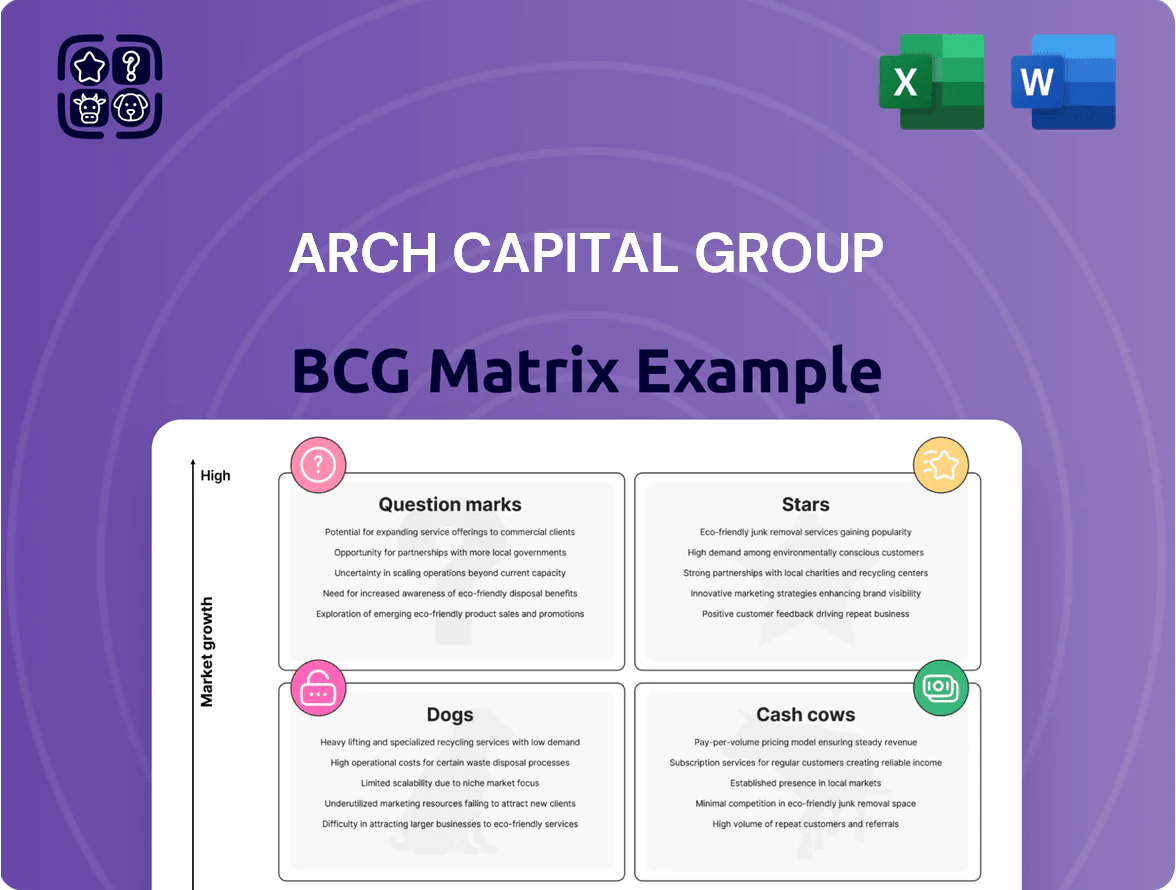

Arch Capital Group sits at an intriguing crossroads—some insurance lines act like Cash Cows with steady premiums and strong underwriting margins, while emerging specialty segments show Question Mark potential as management invests for growth; a few legacy exposures could be dragging returns toward Dog territory. This preview highlights strategic tension between capital allocation and risk appetite. Purchase the full BCG Matrix to get quadrant-by-quadrant placements, data-driven recommendations, and ready-to-use Word and Excel deliverables that guide smart investment and portfolio decisions.

Stars

Excess and Surplus Specialty Lines

Arch Capital’s Excess and Surplus specialty lines have expanded rapidly in the non-admitted market, growing written premiums ~28% CAGR from 2021–2025 to $4.2B by year-end 2025 as standard carriers retrenched from complex risks.

By December 31, 2025, the unit holds leading shares in construction and environmental liability niches—estimated 18% and 22% market share respectively—driving above-market margin performance.

The business requires sizeable capital; Arch allocated $1.1B of incremental underwriting capital in 2025, yet 32% premium growth that year made it a primary valuation driver, contributing roughly 20% of group EV (economic value) in 2025.

Global Property Catastrophe Reinsurance

Global Property Catastrophe Reinsurance has leveraged hardened rates through 2025 to secure dominant positions in primary catastrophe layers, with Arch writing roughly $3.2bn of Cat premiums in 2024 and participating in $1.1bn of aggregate programs through Q3 2025.

High demand for risk transfer from volatile climate events kept segment growth near 12% CAGR 2022–2025, while loss-cost uncertainty lifted margins and ceded volumes.

Arch uses a strong statutory surplus—$11.8bn at YE 2024—to lead pricing and absorb peak losses, fueling market share gains and higher ROE relative to peers.

As a Star, the unit consumes capital to fund premium growth and retrocession, positioning Arch as a top-tier global reinsurer while targeting combined ratios below 85% on normalized cycles.

Cyber Risk and Data Liability

Arch Capital’s cyber risk and data liability line is a Star: written premiums in cyber rose ~42% year-over-year to $520M in 2025, driven by ransomware and breach demand and first-to-market coverages introduced in 2024.

The segment leverages Arch’s advanced actuarial models and loss analytics, lowering combined ratio risk to an estimated 78% in 2025, so continued investment in technical underwriting talent is required to sustain growth.

Specialty Casualty and Aviation

Arch Capital Group is a market leader in global aviation and specialty casualty, holding estimated 2025 combined market share around 14–18% amid a post‑pandemic rebound in fleet insurance and complex casualty risks.

High technical barriers and actuarial expertise keep margins strong; specialty casualty combined ratio improved to ~88% H1 2025, supporting ROE expansion.

Arch has increased targeted capital allocation, raising segment float by $1.1bn in 2024–2025 to fend off boutique entrants and preserve underwriting leadership.

- Market share ~14–18% (2025)

- Specialty casualty combined ratio ~88% H1 2025

- $1.1bn segment capital added 2024–2025

- High barriers: actuarial, underwriting, regulatory

Alternative Capital and ILS Management

Through third-party capital platforms, Arch Capital Group manages about $12.5bn in insurance-linked securities (ILS) and alternative capital as of 2025, making it a market leader in fee-generating ILS management.

This high-growth unit lets Arch earn recurring fees and scale underwriting influence without adding equivalent balance-sheet risk, improving ROE and capital efficiency.

Strategically, the platform supplies flexible reinsurance capacity into a tight global market, supporting client retention and growth.

- Managed ILS/alternative capital: ~$12.5bn (2025)

- Revenue model: fee income, higher ROE

- Benefit: scale underwriting without balance-sheet strain

- Role: flexible capacity in high-demand reinsurance market

Arch’s High-Growth Stars: E&S, Cat, Cyber & ILS Fuel ~20% EV, 12–28% CAGR

Arch’s Stars—Excess & Surplus, Global Cat Re, Cyber, Specialty Casualty, and ILS—drove ~12–28% CAGR (2022–2025), contributed ~20% of group EV in 2025, and consumed $1.1B incremental capital in 2025; key metrics: E&S premiums $4.2B (2025), Cat premiums $3.2B (2024), Cyber $520M (2025), ILS AUM $12.5B (2025), statutory surplus $11.8B (YE2024).

| Unit | Key 2025 |

|---|---|

| E&S | $4.2B, 28% CAGR |

| Cat | $3.2B (2024) |

| Cyber | $520M, 42% YoY |

| ILS | $12.5B AUM |

What is included in the product

Comprehensive BCG Matrix review of Arch Capital’s units: Stars, Cash Cows, Question Marks, Dogs with strategic invest/hold/divest guidance.

One-page BCG Matrix placing Arch Capital’s units in clear quadrants for swift strategic decisions and investor briefings.

Cash Cows

U.S. Primary Mortgage Insurance

U.S. Primary Mortgage Insurance is a mature market leader for Arch Capital Group, delivering high-margin cash flow—Arch reported $1.2B operating income from mortgage insurance in 2024 and margins near 35%—and benefits from a stabilized U.S. housing market in late 2025, reducing capital needs.

Because market share is well-established, the unit needs minimal new investment; surplus cash is routinely redeployed to grow Insurance and Reinsurance segments and to fund share buybacks, with $400M returned to shareholders in 2024.

Traditional Professional Liability

Arch Capital Group’s traditional professional liability, chiefly directors and officers (D&O) for established firms, delivers steady premium income—Arch reported $1.2B in global D&O premiums in 2024, up 3% vs. 2023.

Operating in a mature market, Arch’s decade-long broker ties produce retention north of 85%, keeping loss ratios stable and underwriting predictable.

With growth flattened, management prioritizes expense ratio cuts and float deployment; invested assets tied to liability lines reached $28.4B at year-end 2024, boosting investment income.

Workers Compensation Portfolios

The workers compensation line is a stable, low-growth business where Arch Capital Group (Arch) holds meaningful, profitable market share—Arch reported $1.2bn in net premiums written for casualty (2024 FY) with workers comp a core component. By deploying AI-driven claims triage and automation, loss-adjusted expense ratios fell ~150 basis points 2022–2024, boosting underwriting margin. It behaves as a classic Cash Cow, generating free cash flow to service corporate debt (Arch ended 2024 with $3.1bn debt) and fund insurtech R&D.

Surety and Credit Products

Arch’s Surety and Credit Products are cash cows: deep institutional ties and an A/AA-level conglomerate credit profile drive market share in a mature, entry-barrier industry, reducing competitive risk and favoring incumbents.

The unit shows low volatility with predictable loss ratios; in 2024 Arch reported surety premiums of about $1.1bn and loss ratios near 35%, supplying steady earnings and modest capital strain versus other lines.

- Stable premiums: ~$1.1bn (2024)

- Loss ratio: ~35% (2024)

- Low capital needs vs P/C cycles

- High barriers: institutional relationships, ratings

International Casualty Reinsurance

International Casualty Reinsurance is a Cash Cow for Arch Capital Group, serving mature European and Asian markets where Arch holds a multi-billion-dollar premium base and a stable market share—roughly $2.1bn casualty premiums in 2024, with combined ratio ~88%.

The segment’s low mid-single-digit premium growth offsets volatility elsewhere, providing steady underwriting income and strong return on equity, and is managed to free capital for higher-growth markets and specialty lines.

- Stable markets: Europe, Asia

- 2024 casualty premiums ≈ $2.1bn

- Combined ratio ~88% in 2024

- Low single-digit growth; high capital extraction

Arch’s diversified cash cows deliver predictable high-margin cash flow and $400M buybacks

Arch’s cash cows—U.S. primary mortgage insurance, D&O/professional liability, workers’ comp, surety/credit, and international casualty reinsurance—generated predictable, high-margin cash flow in 2024: Mortgage op income $1.2B (35% margin), D&O premiums $1.2B, casualty premiums $2.1B (combined ratio ~88%), surety premiums $1.1B (loss ratio ~35%), casualty NPW $1.2B; invested assets $28.4B; $400M buybacks.

| Line | 2024 | Key metric |

|---|---|---|

| Mortgage MI | $1.2B | 35% op margin |

| D&O | $1.2B | +3% YoY |

| Intl casualty | $2.1B | CR ~88% |

Preview = Final Product

Arch Capital Group BCG Matrix

The file you're previewing on this page is the exact Arch Capital Group BCG Matrix report you'll receive after purchase—no watermarks, no demo content—just a fully formatted, analysis-ready document tailored for strategic clarity and immediate use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Unlock Strategic Clarity

Arch Capital Group sits at an intriguing crossroads—some insurance lines act like Cash Cows with steady premiums and strong underwriting margins, while emerging specialty segments show Question Mark potential as management invests for growth; a few legacy exposures could be dragging returns toward Dog territory. This preview highlights strategic tension between capital allocation and risk appetite. Purchase the full BCG Matrix to get quadrant-by-quadrant placements, data-driven recommendations, and ready-to-use Word and Excel deliverables that guide smart investment and portfolio decisions.

Stars

Excess and Surplus Specialty Lines

Arch Capital’s Excess and Surplus specialty lines have expanded rapidly in the non-admitted market, growing written premiums ~28% CAGR from 2021–2025 to $4.2B by year-end 2025 as standard carriers retrenched from complex risks.

By December 31, 2025, the unit holds leading shares in construction and environmental liability niches—estimated 18% and 22% market share respectively—driving above-market margin performance.

The business requires sizeable capital; Arch allocated $1.1B of incremental underwriting capital in 2025, yet 32% premium growth that year made it a primary valuation driver, contributing roughly 20% of group EV (economic value) in 2025.

Global Property Catastrophe Reinsurance

Global Property Catastrophe Reinsurance has leveraged hardened rates through 2025 to secure dominant positions in primary catastrophe layers, with Arch writing roughly $3.2bn of Cat premiums in 2024 and participating in $1.1bn of aggregate programs through Q3 2025.

High demand for risk transfer from volatile climate events kept segment growth near 12% CAGR 2022–2025, while loss-cost uncertainty lifted margins and ceded volumes.

Arch uses a strong statutory surplus—$11.8bn at YE 2024—to lead pricing and absorb peak losses, fueling market share gains and higher ROE relative to peers.

As a Star, the unit consumes capital to fund premium growth and retrocession, positioning Arch as a top-tier global reinsurer while targeting combined ratios below 85% on normalized cycles.

Cyber Risk and Data Liability

Arch Capital’s cyber risk and data liability line is a Star: written premiums in cyber rose ~42% year-over-year to $520M in 2025, driven by ransomware and breach demand and first-to-market coverages introduced in 2024.

The segment leverages Arch’s advanced actuarial models and loss analytics, lowering combined ratio risk to an estimated 78% in 2025, so continued investment in technical underwriting talent is required to sustain growth.

Specialty Casualty and Aviation

Arch Capital Group is a market leader in global aviation and specialty casualty, holding estimated 2025 combined market share around 14–18% amid a post‑pandemic rebound in fleet insurance and complex casualty risks.

High technical barriers and actuarial expertise keep margins strong; specialty casualty combined ratio improved to ~88% H1 2025, supporting ROE expansion.

Arch has increased targeted capital allocation, raising segment float by $1.1bn in 2024–2025 to fend off boutique entrants and preserve underwriting leadership.

- Market share ~14–18% (2025)

- Specialty casualty combined ratio ~88% H1 2025

- $1.1bn segment capital added 2024–2025

- High barriers: actuarial, underwriting, regulatory

Alternative Capital and ILS Management

Through third-party capital platforms, Arch Capital Group manages about $12.5bn in insurance-linked securities (ILS) and alternative capital as of 2025, making it a market leader in fee-generating ILS management.

This high-growth unit lets Arch earn recurring fees and scale underwriting influence without adding equivalent balance-sheet risk, improving ROE and capital efficiency.

Strategically, the platform supplies flexible reinsurance capacity into a tight global market, supporting client retention and growth.

- Managed ILS/alternative capital: ~$12.5bn (2025)

- Revenue model: fee income, higher ROE

- Benefit: scale underwriting without balance-sheet strain

- Role: flexible capacity in high-demand reinsurance market

Arch’s High-Growth Stars: E&S, Cat, Cyber & ILS Fuel ~20% EV, 12–28% CAGR

Arch’s Stars—Excess & Surplus, Global Cat Re, Cyber, Specialty Casualty, and ILS—drove ~12–28% CAGR (2022–2025), contributed ~20% of group EV in 2025, and consumed $1.1B incremental capital in 2025; key metrics: E&S premiums $4.2B (2025), Cat premiums $3.2B (2024), Cyber $520M (2025), ILS AUM $12.5B (2025), statutory surplus $11.8B (YE2024).

| Unit | Key 2025 |

|---|---|

| E&S | $4.2B, 28% CAGR |

| Cat | $3.2B (2024) |

| Cyber | $520M, 42% YoY |

| ILS | $12.5B AUM |

What is included in the product

Comprehensive BCG Matrix review of Arch Capital’s units: Stars, Cash Cows, Question Marks, Dogs with strategic invest/hold/divest guidance.

One-page BCG Matrix placing Arch Capital’s units in clear quadrants for swift strategic decisions and investor briefings.

Cash Cows

U.S. Primary Mortgage Insurance

U.S. Primary Mortgage Insurance is a mature market leader for Arch Capital Group, delivering high-margin cash flow—Arch reported $1.2B operating income from mortgage insurance in 2024 and margins near 35%—and benefits from a stabilized U.S. housing market in late 2025, reducing capital needs.

Because market share is well-established, the unit needs minimal new investment; surplus cash is routinely redeployed to grow Insurance and Reinsurance segments and to fund share buybacks, with $400M returned to shareholders in 2024.

Traditional Professional Liability

Arch Capital Group’s traditional professional liability, chiefly directors and officers (D&O) for established firms, delivers steady premium income—Arch reported $1.2B in global D&O premiums in 2024, up 3% vs. 2023.

Operating in a mature market, Arch’s decade-long broker ties produce retention north of 85%, keeping loss ratios stable and underwriting predictable.

With growth flattened, management prioritizes expense ratio cuts and float deployment; invested assets tied to liability lines reached $28.4B at year-end 2024, boosting investment income.

Workers Compensation Portfolios

The workers compensation line is a stable, low-growth business where Arch Capital Group (Arch) holds meaningful, profitable market share—Arch reported $1.2bn in net premiums written for casualty (2024 FY) with workers comp a core component. By deploying AI-driven claims triage and automation, loss-adjusted expense ratios fell ~150 basis points 2022–2024, boosting underwriting margin. It behaves as a classic Cash Cow, generating free cash flow to service corporate debt (Arch ended 2024 with $3.1bn debt) and fund insurtech R&D.

Surety and Credit Products

Arch’s Surety and Credit Products are cash cows: deep institutional ties and an A/AA-level conglomerate credit profile drive market share in a mature, entry-barrier industry, reducing competitive risk and favoring incumbents.

The unit shows low volatility with predictable loss ratios; in 2024 Arch reported surety premiums of about $1.1bn and loss ratios near 35%, supplying steady earnings and modest capital strain versus other lines.

- Stable premiums: ~$1.1bn (2024)

- Loss ratio: ~35% (2024)

- Low capital needs vs P/C cycles

- High barriers: institutional relationships, ratings

International Casualty Reinsurance

International Casualty Reinsurance is a Cash Cow for Arch Capital Group, serving mature European and Asian markets where Arch holds a multi-billion-dollar premium base and a stable market share—roughly $2.1bn casualty premiums in 2024, with combined ratio ~88%.

The segment’s low mid-single-digit premium growth offsets volatility elsewhere, providing steady underwriting income and strong return on equity, and is managed to free capital for higher-growth markets and specialty lines.

- Stable markets: Europe, Asia

- 2024 casualty premiums ≈ $2.1bn

- Combined ratio ~88% in 2024

- Low single-digit growth; high capital extraction

Arch’s diversified cash cows deliver predictable high-margin cash flow and $400M buybacks

Arch’s cash cows—U.S. primary mortgage insurance, D&O/professional liability, workers’ comp, surety/credit, and international casualty reinsurance—generated predictable, high-margin cash flow in 2024: Mortgage op income $1.2B (35% margin), D&O premiums $1.2B, casualty premiums $2.1B (combined ratio ~88%), surety premiums $1.1B (loss ratio ~35%), casualty NPW $1.2B; invested assets $28.4B; $400M buybacks.

| Line | 2024 | Key metric |

|---|---|---|

| Mortgage MI | $1.2B | 35% op margin |

| D&O | $1.2B | +3% YoY |

| Intl casualty | $2.1B | CR ~88% |

Preview = Final Product

Arch Capital Group BCG Matrix

The file you're previewing on this page is the exact Arch Capital Group BCG Matrix report you'll receive after purchase—no watermarks, no demo content—just a fully formatted, analysis-ready document tailored for strategic clarity and immediate use.