Archer Aviation SWOT Analysis

Your Strategic Toolkit Starts Here

Archer Aviation shows strong technological leadership in eVTOL development and key partnerships, but faces regulatory hurdles, capital intensity, and stiff competition that could delay commercialization; purchase the full SWOT analysis to access a detailed, research-backed report with editable Word and Excel deliverables to guide investment, strategy, or pitch preparation.

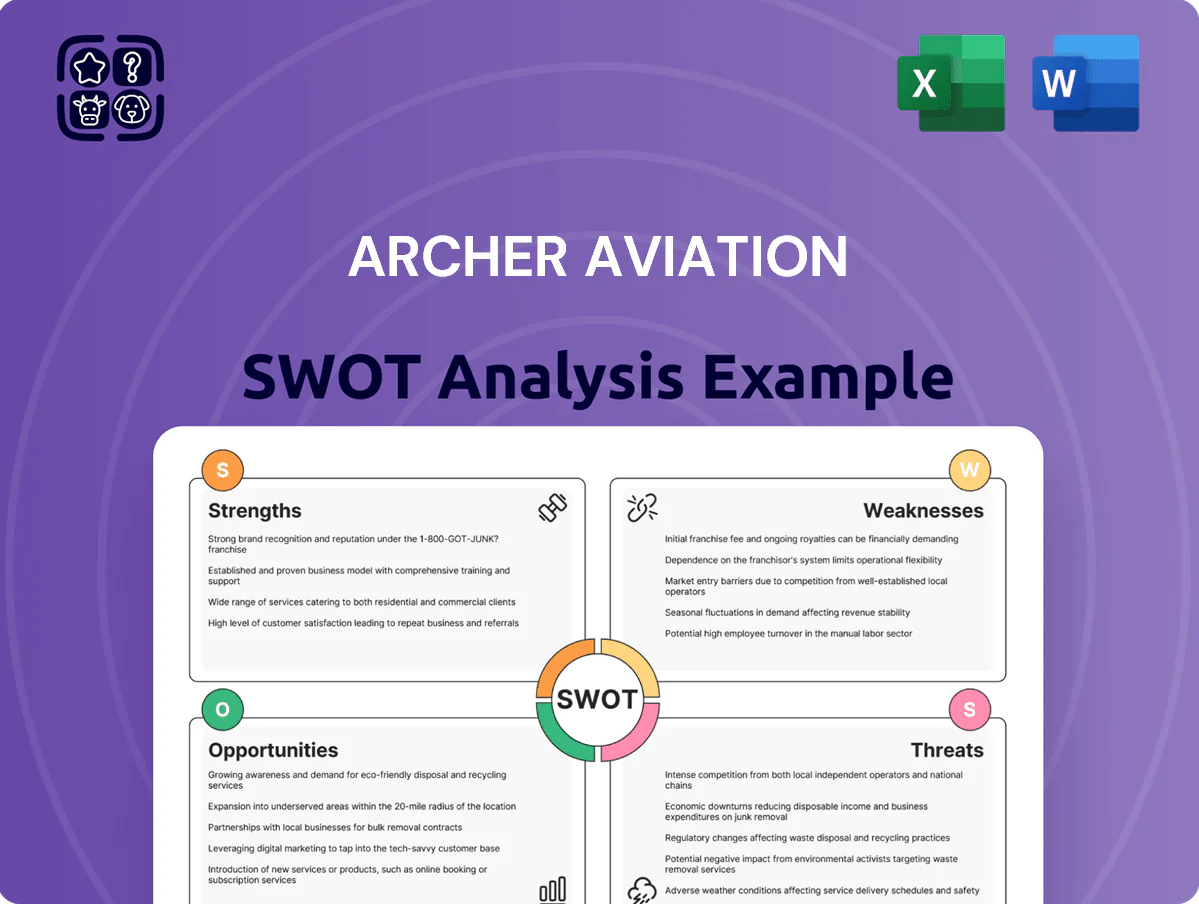

Strengths

Strategic Partnership with Stellantis

Archer benefits from a deep manufacturing partnership with Stellantis, giving it access to Stellantis’ supply‑chain systems and high‑volume production know‑how; Stellantis reported $183.7B revenue in 2024, showing scale behind the support. This lets Archer scale its Georgia facility faster than rivals building greenfield lines, cutting time‑to‑volume and reducing execution risk. Leveraging Stellantis’ capital and labor lowers Archer’s cost and variance during the mass‑production ramp.

Strong Backlog and Airline Integration

Archer holds a massive backlog, highlighted by a 2023 multi-billion-dollar firm order and investment from United Airlines for Midnight eVTOLs, backing potential $1.5–3.0bn revenue over initial years based on published list prices and service targets.

United’s role as strategic customer and investor gives Archer a defined commercialization path and clarifies airport-to-city operational specs, reducing go-to-market execution risk.

Having a major global airline validate the model improves early revenue visibility and supports program financing, fleet planning, and regulatory engagement.

Advanced FAA Certification Progress

By end-2025 Archer Aviation cleared key FAA Type Certification milestones, completing final flight-test blocks and submitting its safety assessment, putting it among the first eVTOLs to reach advanced regulatory approval stages.

Flight testing validated the tilt-wing reliability with >1,200 flight hours and a mean time between failure metric that met FAA targets, strengthening safety claims.

Regulatory momentum raises the barrier to entry for new rivals and supports institutional confidence—Archer’s market cap was about $600M in Dec 2025, aiding further certification financing.

Proprietary Electric Powertrain Technology

Archer’s vertical integration of electric motors and battery packs tunes power and thermal management to the Midnight aircraft, improving range and mission efficiency; company targets 100-mile-plus effective range for Midnight as of 2025 testing milestones.

Design emphasizes safety with redundant motor controllers and high power-to-weight ratios, supporting rapid climb and hover required for urban air mobility and reducing per-flight failure risk.

Owning this IP cuts projected maintenance and replacement costs versus outsourced systems; Archer reported $1.1B in backlog and expects manufacturing cost declines with scale in 2025.

- Tailored motors/batteries → better range (100+ miles target)

- Redundancy → higher safety, lower failure rates

- High power-to-weight → improved urban performance

- IP & vertical integration → lower lifecycle maintenance costs

Robust Capital Position

Investor confidence—evidenced by continued funding in volatile markets—reflects trust in management and Archer’s eVTOL roadmap.

- Cash and equivalents ≈ $1.3B (Q3 2025)

- Estimated production funding need $800–1,000M

- Strategic investors: Stellantis, United Airlines

Archer nears commercial lift: Stellantis scale, United backlog, FAA progress, $1.3B cash

Archer’s strengths: Stellantis manufacturing partnership (Stellantis $183.7B revenue 2024) accelerates Georgia scale-up and lowers unit costs; United Airlines firm order/backlog supports $1.5–3.0B initial revenue and defines ops; FAA certification progress (final flight blocks, >1,200 test hours) de-risks entry; Q3 2025 cash ≈ $1.3B funds certification and ramp.

| Metric | Value |

|---|---|

| Stellantis 2024 Rev | $183.7B |

| Backlog potential | $1.5–3.0B |

| Flight hours | >1,200 |

| Cash (Q3 2025) | $1.3B |

What is included in the product

Provides a concise SWOT overview of Archer Aviation, outlining its core strengths, operational weaknesses, strategic growth opportunities, and external threats shaping the company’s competitive and regulatory landscape.

Delivers a concise Archer Aviation SWOT snapshot for rapid strategic alignment and quick stakeholder briefings.

Weaknesses

Substantial Capital Burn Rate

As a pre-revenue company in a capital-intensive eVTOL industry, Archer Aviation (ACHR) burned about $442 million in FY 2023 and reported $1.1 billion cash on hand as of Q3 2024, highlighting heavy R&D and manufacturing spend to commercialize a new aircraft category.

Bringing a certificated aircraft to market often costs billions; industry peers estimate $2–5 billion lifecycle spend, so any certification or production delays could force Archer into dilutive equity raises that would pressure shareholder value.

Dependence on Third-Party Infrastructure

The success of Archer’s air taxi hinges on third-party vertiports and charging networks; without them, scale is limited—NYC and Chicago lack comprehensive vertiport grids, and industry estimates (McKinsey 2024) project 5,000+ vertiports needed by 2035 while only ~120 were planned by 2025, creating a bottleneck Archer can’t fully control given its $500m+ cash runway constraints (Q3 2025 guidance) and reliance on partners for ground rollout.

Limited Operational History

Despite promising flight tests, Archer Aviation lacks long-term operational data to confirm life-cycle costs and maintenance needs for its Midnight eVTOL; industry estimates suggest eVTOL mean time between unscheduled removals could vary 20–50% versus helicopters, which raises cost uncertainty.

Commercial service exposes issues unseen in tests: weather impacts, tight turn-around times, and battery degradation—battery capacity can drop ~2–4% per 100 cycles, so a 1,000-cycle year could cut range materially.

Investors and insurers remain cautious: Archer reported $423 million cash at end-2024, but underwriters often demand several years of consistent operations before pricing liability and hull coverages at helicopter-comparable rates.

Concentration of Manufacturing Risk

Archer’s production depends heavily on its Covington, Georgia assembly plant, a single point of failure that risks missing its 2025 target of initial deliveries and scaling to the planned 100+ aircraft per year capacity.

Regional supply-chain shocks, local labor shortages, or a facility shutdown could push multi-month delays; in 2024 U.S. manufacturing disruptions raised component lead times by ~22% in aerospace supply chains.

Stellantis partnership offsets capacity risk via manufacturing expertise and potential alternative sites, but physical concentration of final assembly keeps a material vulnerability.

- Single Covington site: single failure point

- 2025 scale target: 100+ aircraft/yr

- 2024 lead-time rise: ~22% in aerospace parts

- Stellantis reduces but does not eliminate risk

Weight and Payload Constraints

The Midnight’s current lithium-ion battery limits payload to one pilot + four passengers with minimal luggage, constraining mission types and reducing appeal for premium/group travel; industry energy density improvements lag, with best EV cells ~300–350 Wh/kg vs needed >500 Wh/kg for meaningful payload gains.

This battery ceiling raises per-seat operating costs—longer flights require payload penalties or added charging time—pressuring unit economics when Archer targets sub- $300 per seat urban routes and FAA Part 135 charter operators.

- Payload: pilot + 4 pax (minimal luggage)

- Energy density gap: ~300–350 Wh/kg current vs >500 Wh/kg target

- Impact: limits mission types, premium/group appeal

- Economic effect: higher per-seat costs vs $300 target fares

Cash burn, single plant risk & weak batteries threaten 2025 production and fare goals

High cash burn and pre-revenue status (FY2023 burn $442M; cash ~$423M end-2024) force dilution risk if certification/production delays occur; single Covington plant is a single-point failure for 2025 target (100+ aircraft/yr); limited battery energy density (~300–350 Wh/kg vs >500 Wh/kg needed) caps payload to pilot+4 and raises per-seat costs versus $300 target fares.

| Metric | Value |

|---|---|

| FY2023 cash burn | $442M |

| Cash end-2024 | $423M |

| 2025 production target | 100+ aircraft/yr |

| Battery energy density | 300–350 Wh/kg (vs >500 Wh/kg need) |

What You See Is What You Get

Archer Aviation SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get, and the content shown is the real, editable file included in your download. Buy now to unlock the entire, detailed version immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Strategic Toolkit Starts Here

Archer Aviation shows strong technological leadership in eVTOL development and key partnerships, but faces regulatory hurdles, capital intensity, and stiff competition that could delay commercialization; purchase the full SWOT analysis to access a detailed, research-backed report with editable Word and Excel deliverables to guide investment, strategy, or pitch preparation.

Strengths

Strategic Partnership with Stellantis

Archer benefits from a deep manufacturing partnership with Stellantis, giving it access to Stellantis’ supply‑chain systems and high‑volume production know‑how; Stellantis reported $183.7B revenue in 2024, showing scale behind the support. This lets Archer scale its Georgia facility faster than rivals building greenfield lines, cutting time‑to‑volume and reducing execution risk. Leveraging Stellantis’ capital and labor lowers Archer’s cost and variance during the mass‑production ramp.

Strong Backlog and Airline Integration

Archer holds a massive backlog, highlighted by a 2023 multi-billion-dollar firm order and investment from United Airlines for Midnight eVTOLs, backing potential $1.5–3.0bn revenue over initial years based on published list prices and service targets.

United’s role as strategic customer and investor gives Archer a defined commercialization path and clarifies airport-to-city operational specs, reducing go-to-market execution risk.

Having a major global airline validate the model improves early revenue visibility and supports program financing, fleet planning, and regulatory engagement.

Advanced FAA Certification Progress

By end-2025 Archer Aviation cleared key FAA Type Certification milestones, completing final flight-test blocks and submitting its safety assessment, putting it among the first eVTOLs to reach advanced regulatory approval stages.

Flight testing validated the tilt-wing reliability with >1,200 flight hours and a mean time between failure metric that met FAA targets, strengthening safety claims.

Regulatory momentum raises the barrier to entry for new rivals and supports institutional confidence—Archer’s market cap was about $600M in Dec 2025, aiding further certification financing.

Proprietary Electric Powertrain Technology

Archer’s vertical integration of electric motors and battery packs tunes power and thermal management to the Midnight aircraft, improving range and mission efficiency; company targets 100-mile-plus effective range for Midnight as of 2025 testing milestones.

Design emphasizes safety with redundant motor controllers and high power-to-weight ratios, supporting rapid climb and hover required for urban air mobility and reducing per-flight failure risk.

Owning this IP cuts projected maintenance and replacement costs versus outsourced systems; Archer reported $1.1B in backlog and expects manufacturing cost declines with scale in 2025.

- Tailored motors/batteries → better range (100+ miles target)

- Redundancy → higher safety, lower failure rates

- High power-to-weight → improved urban performance

- IP & vertical integration → lower lifecycle maintenance costs

Robust Capital Position

Investor confidence—evidenced by continued funding in volatile markets—reflects trust in management and Archer’s eVTOL roadmap.

- Cash and equivalents ≈ $1.3B (Q3 2025)

- Estimated production funding need $800–1,000M

- Strategic investors: Stellantis, United Airlines

Archer nears commercial lift: Stellantis scale, United backlog, FAA progress, $1.3B cash

Archer’s strengths: Stellantis manufacturing partnership (Stellantis $183.7B revenue 2024) accelerates Georgia scale-up and lowers unit costs; United Airlines firm order/backlog supports $1.5–3.0B initial revenue and defines ops; FAA certification progress (final flight blocks, >1,200 test hours) de-risks entry; Q3 2025 cash ≈ $1.3B funds certification and ramp.

| Metric | Value |

|---|---|

| Stellantis 2024 Rev | $183.7B |

| Backlog potential | $1.5–3.0B |

| Flight hours | >1,200 |

| Cash (Q3 2025) | $1.3B |

What is included in the product

Provides a concise SWOT overview of Archer Aviation, outlining its core strengths, operational weaknesses, strategic growth opportunities, and external threats shaping the company’s competitive and regulatory landscape.

Delivers a concise Archer Aviation SWOT snapshot for rapid strategic alignment and quick stakeholder briefings.

Weaknesses

Substantial Capital Burn Rate

As a pre-revenue company in a capital-intensive eVTOL industry, Archer Aviation (ACHR) burned about $442 million in FY 2023 and reported $1.1 billion cash on hand as of Q3 2024, highlighting heavy R&D and manufacturing spend to commercialize a new aircraft category.

Bringing a certificated aircraft to market often costs billions; industry peers estimate $2–5 billion lifecycle spend, so any certification or production delays could force Archer into dilutive equity raises that would pressure shareholder value.

Dependence on Third-Party Infrastructure

The success of Archer’s air taxi hinges on third-party vertiports and charging networks; without them, scale is limited—NYC and Chicago lack comprehensive vertiport grids, and industry estimates (McKinsey 2024) project 5,000+ vertiports needed by 2035 while only ~120 were planned by 2025, creating a bottleneck Archer can’t fully control given its $500m+ cash runway constraints (Q3 2025 guidance) and reliance on partners for ground rollout.

Limited Operational History

Despite promising flight tests, Archer Aviation lacks long-term operational data to confirm life-cycle costs and maintenance needs for its Midnight eVTOL; industry estimates suggest eVTOL mean time between unscheduled removals could vary 20–50% versus helicopters, which raises cost uncertainty.

Commercial service exposes issues unseen in tests: weather impacts, tight turn-around times, and battery degradation—battery capacity can drop ~2–4% per 100 cycles, so a 1,000-cycle year could cut range materially.

Investors and insurers remain cautious: Archer reported $423 million cash at end-2024, but underwriters often demand several years of consistent operations before pricing liability and hull coverages at helicopter-comparable rates.

Concentration of Manufacturing Risk

Archer’s production depends heavily on its Covington, Georgia assembly plant, a single point of failure that risks missing its 2025 target of initial deliveries and scaling to the planned 100+ aircraft per year capacity.

Regional supply-chain shocks, local labor shortages, or a facility shutdown could push multi-month delays; in 2024 U.S. manufacturing disruptions raised component lead times by ~22% in aerospace supply chains.

Stellantis partnership offsets capacity risk via manufacturing expertise and potential alternative sites, but physical concentration of final assembly keeps a material vulnerability.

- Single Covington site: single failure point

- 2025 scale target: 100+ aircraft/yr

- 2024 lead-time rise: ~22% in aerospace parts

- Stellantis reduces but does not eliminate risk

Weight and Payload Constraints

The Midnight’s current lithium-ion battery limits payload to one pilot + four passengers with minimal luggage, constraining mission types and reducing appeal for premium/group travel; industry energy density improvements lag, with best EV cells ~300–350 Wh/kg vs needed >500 Wh/kg for meaningful payload gains.

This battery ceiling raises per-seat operating costs—longer flights require payload penalties or added charging time—pressuring unit economics when Archer targets sub- $300 per seat urban routes and FAA Part 135 charter operators.

- Payload: pilot + 4 pax (minimal luggage)

- Energy density gap: ~300–350 Wh/kg current vs >500 Wh/kg target

- Impact: limits mission types, premium/group appeal

- Economic effect: higher per-seat costs vs $300 target fares

Cash burn, single plant risk & weak batteries threaten 2025 production and fare goals

High cash burn and pre-revenue status (FY2023 burn $442M; cash ~$423M end-2024) force dilution risk if certification/production delays occur; single Covington plant is a single-point failure for 2025 target (100+ aircraft/yr); limited battery energy density (~300–350 Wh/kg vs >500 Wh/kg needed) caps payload to pilot+4 and raises per-seat costs versus $300 target fares.

| Metric | Value |

|---|---|

| FY2023 cash burn | $442M |

| Cash end-2024 | $423M |

| 2025 production target | 100+ aircraft/yr |

| Battery energy density | 300–350 Wh/kg (vs >500 Wh/kg need) |

What You See Is What You Get

Archer Aviation SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get, and the content shown is the real, editable file included in your download. Buy now to unlock the entire, detailed version immediately after checkout.