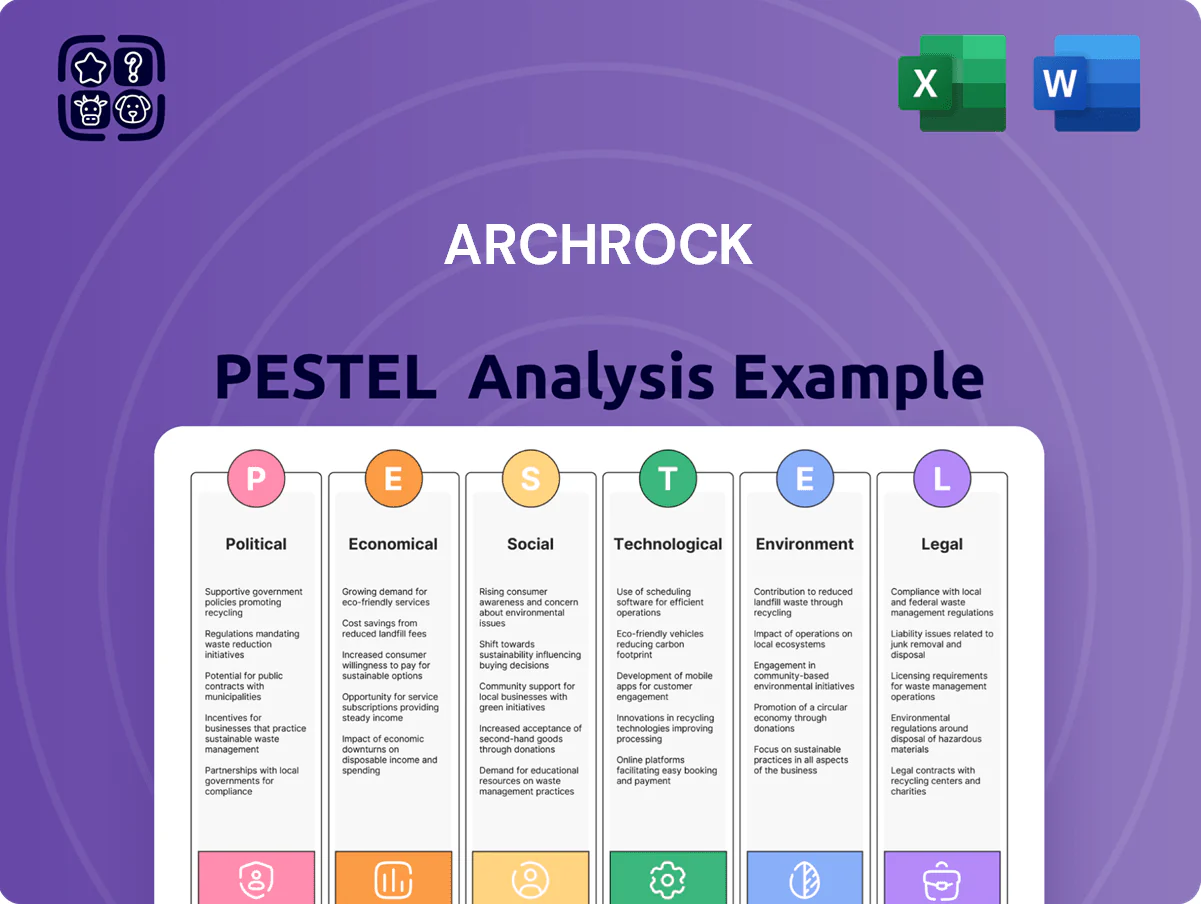

Archrock PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, energy markets, and environmental regulations shape Archrock’s strategic outlook in our concise PESTLE snapshot—ideal for investors and strategists who need fast, actionable context. Purchase the full PESTLE for a detailed breakdown of risks, opportunities, and forecasts that you can plug straight into your model or presentation.

Political factors

Federal Energy Regulatory Policy

The federal energy policy mix in late 2025 balances boosting U.S. natural gas output with climate targets; federal leasing fell 12% YoY in 2024 and BLM permit processing delays grew 18%, reducing feedstock for compression services.

Changes in drilling permits on public lands can cut midstream volumes; US EIA reported dry natural gas marketed production at 101 Bcf/d in 2024, down 2% from 2023, affecting demand for Archrock’s rental and service revenue.

Shifts in executive priorities accelerate or stall interstate pipeline approvals—FERC backlog and slower NEPA reviews delayed several projects, compressing 2025 midstream CAPEX and influencing Archrock’s project timing and EBITDA visibility.

LNG Export Approval Volatility

The federal government’s stance on LNG export permits drives US gas production; US LNG exports reached about 12.8 Bcf/d in 2024, so pauses in terminal approvals can reduce feedstock and pressure upstream activity.

Political acceleration of terminal approvals raises demand for gathering and compression; the US had 12 operational export trains and ~70 mtpa capacity by end-2024, affecting midstream utilization rates.

Archrock’s long-term contract stability ties to US export leadership: with the US supplying roughly 30% of global LNG trade in 2024, policy shifts could materially alter contract renewals and utilization.

Geopolitical Energy Security

Global instability and allies' push for energy independence have elevated US natural gas policy, with US LNG exports reaching ~11.2 Bcf/d in 2025, reinforcing political support for increased production that benefits compression services.

Pro-production domestic policy drives higher pipeline throughput and compression demand; US gas production averaged ~100 Bcf/d in 2024, boosting service needs for firms like Archrock.

Archrock capitalizes by securing multi-year contracts—over 60% of 2024 revenue tied to long-term service agreements—positioning it to meet rising international demand.

Infrastructure Permitting Reform

- Federal proposals target ~30% shorter review timelines

- Past delays added 12–18 months to projects

- Faster permits could improve capital turnover and EBITDA

Tax Incentives and Subsidies

Government fiscal policies, notably the Inflation Reduction Act, provide tax credits up to $85/ton for carbon capture and incentives for methane reduction that shape Archrock’s capex and product roadmap.

Political support for these measures has helped customers invest in cleaner compression; U.S. tax incentives and grant programs contributed to a projected 15-20% increase in demand for low-emission compressor upgrades in 2024–2025.

Archrock actively monitors federal and state incentives to time capital deployment, prioritizing projects eligible for investment tax credits and grants to improve ROI and accelerate adoption.

- IRA carbon capture credits up to $85/ton

- Estimated 15–20% demand lift for low-emission compressors (2024–25)

- Capex aligned to projects qualifying for ITCs and state grants

Policy shifts boost low‑emission compressor demand; Archrock poised with 60% LT revenue

Federal policy and permitting shifts directly alter U.S. gas production and midstream CAPEX: 2024 marketed gas ~101 Bcf/d, LNG exports ~12.8 Bcf/d (2024) and ~11.2 Bcf/d (2025) drove compression demand; BLM leasing -12% YoY (2024) and permit delays +18% hit feedstock. IRA incentives (up to $85/ton CC) and ~15–20% uplift in low-emission compressor demand (2024–25) favor Archrock’s long-term contracts (60% revenue LT).

| Metric | Value |

|---|---|

| US marketed gas (2024) | 101 Bcf/d |

| US LNG exports (2024) | 12.8 Bcf/d |

| US LNG exports (2025) | 11.2 Bcf/d |

| BLM leasing change (2024) | -12% YoY |

| Permit delays (2024) | +18% |

| IRA CC credit | up to $85/ton |

| Demand uplift for low‑emission | 15–20% (2024–25) |

| Archrock LT revenue | ~60% (2024) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Archrock across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to inform scenario planning and strategy for executives, investors, and consultants.

A concise, shareable Archrock PESTLE summary that highlights key external risks and opportunities for quick reference in meetings or presentations, helping teams align on strategy and risk mitigation.

Economic factors

Interest Rate Environment

As a capital-intensive provider of gas compression services, Archrock is highly sensitive to borrowing costs; its 2024 net debt was about $1.1B, so a 100 bp rise in rates would materially increase interest expense and depress free cash flow.

By end-2025, rate trajectory determines feasibility of fleet expansion and refinancing; with U.S. 10-year at ~4.0% in Feb 2026 and Fed funds near 5.25% then, higher rates could delay capex.

Investors track these dynamics for dividend sustainability: Archrock paid $0.18 per share in 2024 and rising rates could compress distributable cash and raise leverage risk.

Natural Gas Price Volatility

While Archrock’s fee-based model cushions revenue, extreme natural gas price swings affect customer drilling: Henry Hub fell to ~$2.30/MMBtu in 2020 then averaged ~$3.50–$4.00 in 2024–2025, and prolonged lows can cut E&P capex, reducing demand for new compression horsepower.

Conversely, high prices—Henry Hub spikes above $6/MMBtu in 2022–2023—boost production in Permian and SCOOP/STACK, where Archrock holds significant share, increasing utilization and rental demand.

Capital Expenditure Trends

As energy firms tighten capital discipline, 2024 industry capex fell ~12% YoY, pushing operators toward service contracts; Archrock benefits as 60–70% of producers prefer renting compression over owning to avoid balance-sheet intensity.

Labor Market Inflation

The specialized maintenance of high-horsepower compression engines demands skilled technicians; U.S. bureau data show median annual wage for heavy vehicle and mobile equipment service technicians rose ~6.5% in 2024, tightening supply for field roles and pressuring Archrock’s labor costs.

Wage inflation and a 2024-2025 oilfield technician vacancy rate near 8–10% can raise operating expenses, forcing Archrock to balance higher pay against efficiency to preserve margins.

- Median wage +6.5% (2024)

- Field technician vacancy ~8–10% (2024–25)

- Higher labor costs risk margin compression without efficiency gains

Global Energy Demand Cycles

The health of the global economy directly affects industrial and residential natural gas demand; IMF projected 2025 world GDP growth at 3.0% (Oct 2024) influencing gas consumption trends and LNG imports.

Economic slowdowns in major importers like China or EU can create domestic US supply gluts, lowering throughput in midstream assets and pressuring spot prices—US Henry Hub averaged 3.70 USD/MMBtu in 2024.

Archrock’s performance through 2026 ties to resilience of global energy consumption: weaker demand reduces utilization of compressor fleets, while a 2024 US natural gas production near 100 Bcf/d supports capacity but risks oversupply.

- IMF 2025 world GDP growth ~3.0%

- Henry Hub 2024 avg ~3.70 USD/MMBtu

- US production ~100 Bcf/d in 2024

Higher rates, $1.1B debt and tight labor squeeze dividend coverage

Higher rates and $1.1B net debt in 2024 increase interest burden; Fed funds ~5.25% (Feb 2026) and US 10y ~4.0% affect refinancing and capex timing, pressuring dividend coverage. Henry Hub avg ~$3.70/MMBtu in 2024; spikes >$6 boost Permian demand while prolonged lows reduce rental need. Wage inflation (+6.5% median technician pay 2024) and 8–10% vacancy raise Opex, risking margins.

| Metric | Value (2024–25) |

|---|---|

| Net debt | $1.1B |

| Fed funds / 10y (Feb 2026) | ~5.25% / ~4.0% |

| Henry Hub avg | $3.70/MMBtu |

| Technician wage change | +6.5% |

| Technician vacancy | 8–10% |

Full Version Awaits

Archrock PESTLE Analysis

The preview shown here is the exact Archrock PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. This file is the final version with complete content, structure, and professional layout, not a teaser or placeholder. After checkout you’ll instantly download the same document visible in the preview, prepared for immediate application in research or strategic planning.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, energy markets, and environmental regulations shape Archrock’s strategic outlook in our concise PESTLE snapshot—ideal for investors and strategists who need fast, actionable context. Purchase the full PESTLE for a detailed breakdown of risks, opportunities, and forecasts that you can plug straight into your model or presentation.

Political factors

Federal Energy Regulatory Policy

The federal energy policy mix in late 2025 balances boosting U.S. natural gas output with climate targets; federal leasing fell 12% YoY in 2024 and BLM permit processing delays grew 18%, reducing feedstock for compression services.

Changes in drilling permits on public lands can cut midstream volumes; US EIA reported dry natural gas marketed production at 101 Bcf/d in 2024, down 2% from 2023, affecting demand for Archrock’s rental and service revenue.

Shifts in executive priorities accelerate or stall interstate pipeline approvals—FERC backlog and slower NEPA reviews delayed several projects, compressing 2025 midstream CAPEX and influencing Archrock’s project timing and EBITDA visibility.

LNG Export Approval Volatility

The federal government’s stance on LNG export permits drives US gas production; US LNG exports reached about 12.8 Bcf/d in 2024, so pauses in terminal approvals can reduce feedstock and pressure upstream activity.

Political acceleration of terminal approvals raises demand for gathering and compression; the US had 12 operational export trains and ~70 mtpa capacity by end-2024, affecting midstream utilization rates.

Archrock’s long-term contract stability ties to US export leadership: with the US supplying roughly 30% of global LNG trade in 2024, policy shifts could materially alter contract renewals and utilization.

Geopolitical Energy Security

Global instability and allies' push for energy independence have elevated US natural gas policy, with US LNG exports reaching ~11.2 Bcf/d in 2025, reinforcing political support for increased production that benefits compression services.

Pro-production domestic policy drives higher pipeline throughput and compression demand; US gas production averaged ~100 Bcf/d in 2024, boosting service needs for firms like Archrock.

Archrock capitalizes by securing multi-year contracts—over 60% of 2024 revenue tied to long-term service agreements—positioning it to meet rising international demand.

Infrastructure Permitting Reform

- Federal proposals target ~30% shorter review timelines

- Past delays added 12–18 months to projects

- Faster permits could improve capital turnover and EBITDA

Tax Incentives and Subsidies

Government fiscal policies, notably the Inflation Reduction Act, provide tax credits up to $85/ton for carbon capture and incentives for methane reduction that shape Archrock’s capex and product roadmap.

Political support for these measures has helped customers invest in cleaner compression; U.S. tax incentives and grant programs contributed to a projected 15-20% increase in demand for low-emission compressor upgrades in 2024–2025.

Archrock actively monitors federal and state incentives to time capital deployment, prioritizing projects eligible for investment tax credits and grants to improve ROI and accelerate adoption.

- IRA carbon capture credits up to $85/ton

- Estimated 15–20% demand lift for low-emission compressors (2024–25)

- Capex aligned to projects qualifying for ITCs and state grants

Policy shifts boost low‑emission compressor demand; Archrock poised with 60% LT revenue

Federal policy and permitting shifts directly alter U.S. gas production and midstream CAPEX: 2024 marketed gas ~101 Bcf/d, LNG exports ~12.8 Bcf/d (2024) and ~11.2 Bcf/d (2025) drove compression demand; BLM leasing -12% YoY (2024) and permit delays +18% hit feedstock. IRA incentives (up to $85/ton CC) and ~15–20% uplift in low-emission compressor demand (2024–25) favor Archrock’s long-term contracts (60% revenue LT).

| Metric | Value |

|---|---|

| US marketed gas (2024) | 101 Bcf/d |

| US LNG exports (2024) | 12.8 Bcf/d |

| US LNG exports (2025) | 11.2 Bcf/d |

| BLM leasing change (2024) | -12% YoY |

| Permit delays (2024) | +18% |

| IRA CC credit | up to $85/ton |

| Demand uplift for low‑emission | 15–20% (2024–25) |

| Archrock LT revenue | ~60% (2024) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Archrock across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to inform scenario planning and strategy for executives, investors, and consultants.

A concise, shareable Archrock PESTLE summary that highlights key external risks and opportunities for quick reference in meetings or presentations, helping teams align on strategy and risk mitigation.

Economic factors

Interest Rate Environment

As a capital-intensive provider of gas compression services, Archrock is highly sensitive to borrowing costs; its 2024 net debt was about $1.1B, so a 100 bp rise in rates would materially increase interest expense and depress free cash flow.

By end-2025, rate trajectory determines feasibility of fleet expansion and refinancing; with U.S. 10-year at ~4.0% in Feb 2026 and Fed funds near 5.25% then, higher rates could delay capex.

Investors track these dynamics for dividend sustainability: Archrock paid $0.18 per share in 2024 and rising rates could compress distributable cash and raise leverage risk.

Natural Gas Price Volatility

While Archrock’s fee-based model cushions revenue, extreme natural gas price swings affect customer drilling: Henry Hub fell to ~$2.30/MMBtu in 2020 then averaged ~$3.50–$4.00 in 2024–2025, and prolonged lows can cut E&P capex, reducing demand for new compression horsepower.

Conversely, high prices—Henry Hub spikes above $6/MMBtu in 2022–2023—boost production in Permian and SCOOP/STACK, where Archrock holds significant share, increasing utilization and rental demand.

Capital Expenditure Trends

As energy firms tighten capital discipline, 2024 industry capex fell ~12% YoY, pushing operators toward service contracts; Archrock benefits as 60–70% of producers prefer renting compression over owning to avoid balance-sheet intensity.

Labor Market Inflation

The specialized maintenance of high-horsepower compression engines demands skilled technicians; U.S. bureau data show median annual wage for heavy vehicle and mobile equipment service technicians rose ~6.5% in 2024, tightening supply for field roles and pressuring Archrock’s labor costs.

Wage inflation and a 2024-2025 oilfield technician vacancy rate near 8–10% can raise operating expenses, forcing Archrock to balance higher pay against efficiency to preserve margins.

- Median wage +6.5% (2024)

- Field technician vacancy ~8–10% (2024–25)

- Higher labor costs risk margin compression without efficiency gains

Global Energy Demand Cycles

The health of the global economy directly affects industrial and residential natural gas demand; IMF projected 2025 world GDP growth at 3.0% (Oct 2024) influencing gas consumption trends and LNG imports.

Economic slowdowns in major importers like China or EU can create domestic US supply gluts, lowering throughput in midstream assets and pressuring spot prices—US Henry Hub averaged 3.70 USD/MMBtu in 2024.

Archrock’s performance through 2026 ties to resilience of global energy consumption: weaker demand reduces utilization of compressor fleets, while a 2024 US natural gas production near 100 Bcf/d supports capacity but risks oversupply.

- IMF 2025 world GDP growth ~3.0%

- Henry Hub 2024 avg ~3.70 USD/MMBtu

- US production ~100 Bcf/d in 2024

Higher rates, $1.1B debt and tight labor squeeze dividend coverage

Higher rates and $1.1B net debt in 2024 increase interest burden; Fed funds ~5.25% (Feb 2026) and US 10y ~4.0% affect refinancing and capex timing, pressuring dividend coverage. Henry Hub avg ~$3.70/MMBtu in 2024; spikes >$6 boost Permian demand while prolonged lows reduce rental need. Wage inflation (+6.5% median technician pay 2024) and 8–10% vacancy raise Opex, risking margins.

| Metric | Value (2024–25) |

|---|---|

| Net debt | $1.1B |

| Fed funds / 10y (Feb 2026) | ~5.25% / ~4.0% |

| Henry Hub avg | $3.70/MMBtu |

| Technician wage change | +6.5% |

| Technician vacancy | 8–10% |

Full Version Awaits

Archrock PESTLE Analysis

The preview shown here is the exact Archrock PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. This file is the final version with complete content, structure, and professional layout, not a teaser or placeholder. After checkout you’ll instantly download the same document visible in the preview, prepared for immediate application in research or strategic planning.