ARC Resources Business Model Canvas

ARC Resources Business Model Canvas: Strategic Playbook for Investors & Strategists

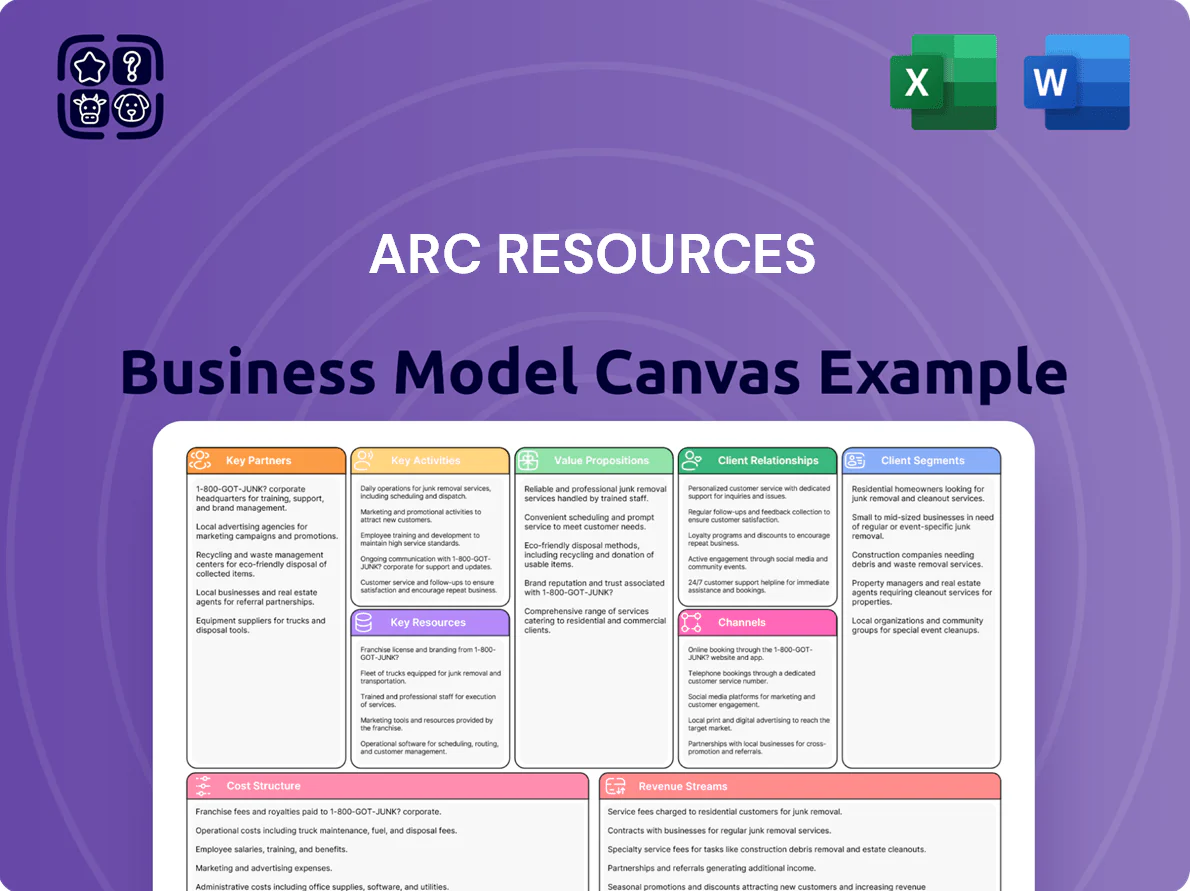

Unlock the full strategic blueprint behind ARC Resources’s business model—this concise Business Model Canvas maps value propositions, key partners, revenue streams, and cost structure to show how the company scales and sustains competitive advantage; perfect for investors, consultants, and strategists seeking actionable insights—download the complete Word/Excel canvas for a section-by-section playbook you can use for benchmarking, presentations, or strategic planning.

Partnerships

Midstream Infrastructure Providers

ARC Resources secures firm transportation capacity with midstream giants TC Energy and Enbridge, moving Montney gas and NGLs to key North American hubs; in 2024 ARC reported ~1.1 Bcf/d of net production and relies on contracted takeaway to protect realizations.

LNG Export Consortiums

ARC Resources holds strategic agreements with partners in LNG Canada and West Coast export projects, giving access to international LNG pricing and linking volumes to Henry Hub plus maritime premiums; in 2024 ARC disclosed ~10–15% of marketed volumes earmarked for export pathways, targeting higher Asian benchmarks near $12–16/MMBtu vs North American $3–6/MMBtu.

Indigenous Community Partners

Collaborative agreements with First Nations in BC and Alberta—covering ~15 communities and joint-venture stakes worth C$120–150M annually—provide economic participation, local hiring targets (30% of new roles) and funded stewardship programs that cut reclamation liabilities and help preserve ARC Resources’ social license to operate.

Technology and Service Vendors

ARC Resources partners with specialized oilfield service and tech firms to deploy advanced drilling and completion methods that cut well costs ~10–20% and lift initial production by ~15% in Montney plays (2024 pilot data).

These alliances also enable methane detection and carbon capture pilots, supporting ARC’s 2030 target to reduce methane intensity to <0.1% and pursue scope‑1/2 emissions cuts of ~30% vs 2019.

- 10–20% cost reduction

- ~15% higher initial production

- Methane intensity target <0.1% by 2030

- ~30% scope‑1/2 emissions cut vs 2019

Financial and Banking Institutions

Strong ties with a syndicate of tier-one banks (including RBC, TD, and CIBC) give ARC Resources CAD 1.2–1.5 billion in committed credit and liquidity as of Q4 2025, funding capital programs and M&A while supporting working capital.

These banks provide hedging products covering ~60% of 2026 gas volumes, reducing commodity-price risk so ARC can execute multi-year development projects and keep leverage near target net debt/EBITDA ~1.0–1.5x.

- Committed credit: CAD 1.2–1.5B

- Hedged volumes: ~60% of 2026 gas

- Target leverage: net debt/EBITDA 1.0–1.5x

ARC locks 1.1 Bcf/d, LNG exports lift realizations; CAD1.2–1.5B credit, FN pacts

ARC secures takeaway with TC Energy and Enbridge, sells ~1.1 Bcf/d (2024), and routes 10–15% of volumes to LNG exports (priced $12–16/MMBtu vs $3–6 NA); First Nations pacts cover ~15 communities and C$120–150M/year; service partners cut well costs 10–20% and boost IPs ~15%; bank syndicate (RBC, TD, CIBC) provides CAD1.2–1.5B credit and hedges ~60% of 2026 gas to keep net debt/EBITDA ~1.0–1.5x.

| Metric | 2024/2026 |

|---|---|

| Net production | ~1.1 Bcf/d (2024) |

| Export share | 10–15% |

| Well cost cut | 10–20% |

| IP uplift | ~15% |

| FN agreements | ~15 communities; C$120–150M/yr |

| Committed credit | CAD1.2–1.5B |

| Hedged volumes | ~60% of 2026 gas |

| Target leverage | Net debt/EBITDA 1.0–1.5x |

What is included in the product

A concise, company-specific Business Model Canvas for ARC Resources covering customer segments, channels, value propositions, revenue streams, key activities, resources, partnerships, cost structure, and governance—aligned with real-world upstream oil & gas operations and growth strategy to support investor presentations and strategic planning.

High-level view of ARC Resources’ business model with editable cells, condensing upstream strategy, revenue streams, and cost drivers into a one-page snapshot ideal for boardrooms, investor reviews, or team collaboration.

Activities

Montney Resource Development

ARC Resources focuses on systematic exploration, drilling, and completion in the Montney, running ~70+ Montney wells in 2024 and targeting 80–100 gross wells for 2025 to sustain ~230,000 boe/d production; it uses multi-well pad drilling and high-intensity hydraulic fracturing to cut per-well capital by ~15–25% and boost EURs (estimated ultimate recoveries) per well.

Processing and Infrastructure Management

ARC Resources owns and operates ~2,300 km of gathering pipelines and multiple gas processing plants, which contributed to a 2024 adjusted operating cost advantage—cash operating costs per boe of C$11.85 in 2024—helping sustain free cash flow; tight control of uptime (plant availability >95% in 2024) lets ARC convert raw gas into condensate and NGLs, protecting volumes and margin.

Environmental and Social Governance

ARC Resources invests heavily in ESG: in 2024 it cut methane intensity to 0.08% and spent C$120m on water treatment and emission controls, with ESG capex ~12% of total 2024 capital spending. The company issues annual TCFD-aligned climate reports, meets evolving Canadian federal methane regs, and uses ESG credentials to win offtake with buyers seeking lower-carbon natural gas.

Market Access and Trading

ARC Resources actively manages commodity marketing and transportation to boost realized prices, evaluating sales hubs and export routes—helping capture margins such as Q4 2025 realized natural gas prices averaging CAD 4.20/GJ and condensate at CAD 84/bbl.

They use advanced hedging and long-term contracts with global counterparties; in 2024 ARC hedged ~40% of 2025 gas volumes and held marketing agreements covering ~500 mcf/d of liquids.

- Optimize routes to highest netback

- Hedge ~40% near-term volumes

- Negotiate long-term sales worldwide

- Focus on hubs and export margin capture

Strategic Capital Allocation

The executive team prioritizes disciplined capital allocation, weighing new-project IRRs against a 6.5% weighted average cost of capital (2025 guidance) and considering share buybacks when free cash flow exceeds C$600m annual targets.

By timing investments to maximize NPV while keeping net debt/adjusted EBITDA near the 1.0–1.2x target range, ARC preserves balance-sheet flexibility and steady shareholder returns.

- IRR vs WACC (6.5%)

- Free cash flow trigger: C$600m+

- Net debt/adj. EBITDA target: 1.0–1.2x

- Buybacks considered when balance sheet strong

ARC accelerates Montney growth: 80–100 wells, C$11.85/boe opex, >C$600m FCF target

ARC runs aggressive Montney drilling (70+ wells in 2024; 80–100 planned 2025) using multi‑well pads and high‑intensity fracs to cut per‑well capex ~15–25% and lift EURs, owns ~2,300 km gathering lines and gas plants (plant availability >95% in 2024) keeping cash opex C$11.85/boe and methane intensity 0.08% (2024); hedges ~40% near‑term volumes, targets net debt/adj. EBITDA 1.0–1.2x and FCF >C$600m for buybacks.

| Metric | 2024 | 2025 guide |

|---|---|---|

| Montney wells | 70+ | 80–100 |

| Production | ~230,000 boe/d | ~230,000 boe/d |

| Cash opex | C$11.85/boe | - |

| Methane intensity | 0.08% | - |

| Hedge | ~40% 2025 volumes | - |

| Net debt/Adj. EBITDA | - | 1.0–1.2x target |

| FCF buyback trigger | - | >C$600m |

Delivered as Displayed

Business Model Canvas

The document you're previewing is the actual ARC Resources Business Model Canvas you’ll receive—no mockup, no sample. When you complete your purchase, you’ll get this same professionally formatted file, ready to edit and present in Word and Excel formats. What you see is what you’ll own: the full, final deliverable with all content and sections included.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

ARC Resources Business Model Canvas: Strategic Playbook for Investors & Strategists

Unlock the full strategic blueprint behind ARC Resources’s business model—this concise Business Model Canvas maps value propositions, key partners, revenue streams, and cost structure to show how the company scales and sustains competitive advantage; perfect for investors, consultants, and strategists seeking actionable insights—download the complete Word/Excel canvas for a section-by-section playbook you can use for benchmarking, presentations, or strategic planning.

Partnerships

Midstream Infrastructure Providers

ARC Resources secures firm transportation capacity with midstream giants TC Energy and Enbridge, moving Montney gas and NGLs to key North American hubs; in 2024 ARC reported ~1.1 Bcf/d of net production and relies on contracted takeaway to protect realizations.

LNG Export Consortiums

ARC Resources holds strategic agreements with partners in LNG Canada and West Coast export projects, giving access to international LNG pricing and linking volumes to Henry Hub plus maritime premiums; in 2024 ARC disclosed ~10–15% of marketed volumes earmarked for export pathways, targeting higher Asian benchmarks near $12–16/MMBtu vs North American $3–6/MMBtu.

Indigenous Community Partners

Collaborative agreements with First Nations in BC and Alberta—covering ~15 communities and joint-venture stakes worth C$120–150M annually—provide economic participation, local hiring targets (30% of new roles) and funded stewardship programs that cut reclamation liabilities and help preserve ARC Resources’ social license to operate.

Technology and Service Vendors

ARC Resources partners with specialized oilfield service and tech firms to deploy advanced drilling and completion methods that cut well costs ~10–20% and lift initial production by ~15% in Montney plays (2024 pilot data).

These alliances also enable methane detection and carbon capture pilots, supporting ARC’s 2030 target to reduce methane intensity to <0.1% and pursue scope‑1/2 emissions cuts of ~30% vs 2019.

- 10–20% cost reduction

- ~15% higher initial production

- Methane intensity target <0.1% by 2030

- ~30% scope‑1/2 emissions cut vs 2019

Financial and Banking Institutions

Strong ties with a syndicate of tier-one banks (including RBC, TD, and CIBC) give ARC Resources CAD 1.2–1.5 billion in committed credit and liquidity as of Q4 2025, funding capital programs and M&A while supporting working capital.

These banks provide hedging products covering ~60% of 2026 gas volumes, reducing commodity-price risk so ARC can execute multi-year development projects and keep leverage near target net debt/EBITDA ~1.0–1.5x.

- Committed credit: CAD 1.2–1.5B

- Hedged volumes: ~60% of 2026 gas

- Target leverage: net debt/EBITDA 1.0–1.5x

ARC locks 1.1 Bcf/d, LNG exports lift realizations; CAD1.2–1.5B credit, FN pacts

ARC secures takeaway with TC Energy and Enbridge, sells ~1.1 Bcf/d (2024), and routes 10–15% of volumes to LNG exports (priced $12–16/MMBtu vs $3–6 NA); First Nations pacts cover ~15 communities and C$120–150M/year; service partners cut well costs 10–20% and boost IPs ~15%; bank syndicate (RBC, TD, CIBC) provides CAD1.2–1.5B credit and hedges ~60% of 2026 gas to keep net debt/EBITDA ~1.0–1.5x.

| Metric | 2024/2026 |

|---|---|

| Net production | ~1.1 Bcf/d (2024) |

| Export share | 10–15% |

| Well cost cut | 10–20% |

| IP uplift | ~15% |

| FN agreements | ~15 communities; C$120–150M/yr |

| Committed credit | CAD1.2–1.5B |

| Hedged volumes | ~60% of 2026 gas |

| Target leverage | Net debt/EBITDA 1.0–1.5x |

What is included in the product

A concise, company-specific Business Model Canvas for ARC Resources covering customer segments, channels, value propositions, revenue streams, key activities, resources, partnerships, cost structure, and governance—aligned with real-world upstream oil & gas operations and growth strategy to support investor presentations and strategic planning.

High-level view of ARC Resources’ business model with editable cells, condensing upstream strategy, revenue streams, and cost drivers into a one-page snapshot ideal for boardrooms, investor reviews, or team collaboration.

Activities

Montney Resource Development

ARC Resources focuses on systematic exploration, drilling, and completion in the Montney, running ~70+ Montney wells in 2024 and targeting 80–100 gross wells for 2025 to sustain ~230,000 boe/d production; it uses multi-well pad drilling and high-intensity hydraulic fracturing to cut per-well capital by ~15–25% and boost EURs (estimated ultimate recoveries) per well.

Processing and Infrastructure Management

ARC Resources owns and operates ~2,300 km of gathering pipelines and multiple gas processing plants, which contributed to a 2024 adjusted operating cost advantage—cash operating costs per boe of C$11.85 in 2024—helping sustain free cash flow; tight control of uptime (plant availability >95% in 2024) lets ARC convert raw gas into condensate and NGLs, protecting volumes and margin.

Environmental and Social Governance

ARC Resources invests heavily in ESG: in 2024 it cut methane intensity to 0.08% and spent C$120m on water treatment and emission controls, with ESG capex ~12% of total 2024 capital spending. The company issues annual TCFD-aligned climate reports, meets evolving Canadian federal methane regs, and uses ESG credentials to win offtake with buyers seeking lower-carbon natural gas.

Market Access and Trading

ARC Resources actively manages commodity marketing and transportation to boost realized prices, evaluating sales hubs and export routes—helping capture margins such as Q4 2025 realized natural gas prices averaging CAD 4.20/GJ and condensate at CAD 84/bbl.

They use advanced hedging and long-term contracts with global counterparties; in 2024 ARC hedged ~40% of 2025 gas volumes and held marketing agreements covering ~500 mcf/d of liquids.

- Optimize routes to highest netback

- Hedge ~40% near-term volumes

- Negotiate long-term sales worldwide

- Focus on hubs and export margin capture

Strategic Capital Allocation

The executive team prioritizes disciplined capital allocation, weighing new-project IRRs against a 6.5% weighted average cost of capital (2025 guidance) and considering share buybacks when free cash flow exceeds C$600m annual targets.

By timing investments to maximize NPV while keeping net debt/adjusted EBITDA near the 1.0–1.2x target range, ARC preserves balance-sheet flexibility and steady shareholder returns.

- IRR vs WACC (6.5%)

- Free cash flow trigger: C$600m+

- Net debt/adj. EBITDA target: 1.0–1.2x

- Buybacks considered when balance sheet strong

ARC accelerates Montney growth: 80–100 wells, C$11.85/boe opex, >C$600m FCF target

ARC runs aggressive Montney drilling (70+ wells in 2024; 80–100 planned 2025) using multi‑well pads and high‑intensity fracs to cut per‑well capex ~15–25% and lift EURs, owns ~2,300 km gathering lines and gas plants (plant availability >95% in 2024) keeping cash opex C$11.85/boe and methane intensity 0.08% (2024); hedges ~40% near‑term volumes, targets net debt/adj. EBITDA 1.0–1.2x and FCF >C$600m for buybacks.

| Metric | 2024 | 2025 guide |

|---|---|---|

| Montney wells | 70+ | 80–100 |

| Production | ~230,000 boe/d | ~230,000 boe/d |

| Cash opex | C$11.85/boe | - |

| Methane intensity | 0.08% | - |

| Hedge | ~40% 2025 volumes | - |

| Net debt/Adj. EBITDA | - | 1.0–1.2x target |

| FCF buyback trigger | - | >C$600m |

Delivered as Displayed

Business Model Canvas

The document you're previewing is the actual ARC Resources Business Model Canvas you’ll receive—no mockup, no sample. When you complete your purchase, you’ll get this same professionally formatted file, ready to edit and present in Word and Excel formats. What you see is what you’ll own: the full, final deliverable with all content and sections included.