Ardagh Group SA Boston Consulting Group Matrix

See the Bigger Picture

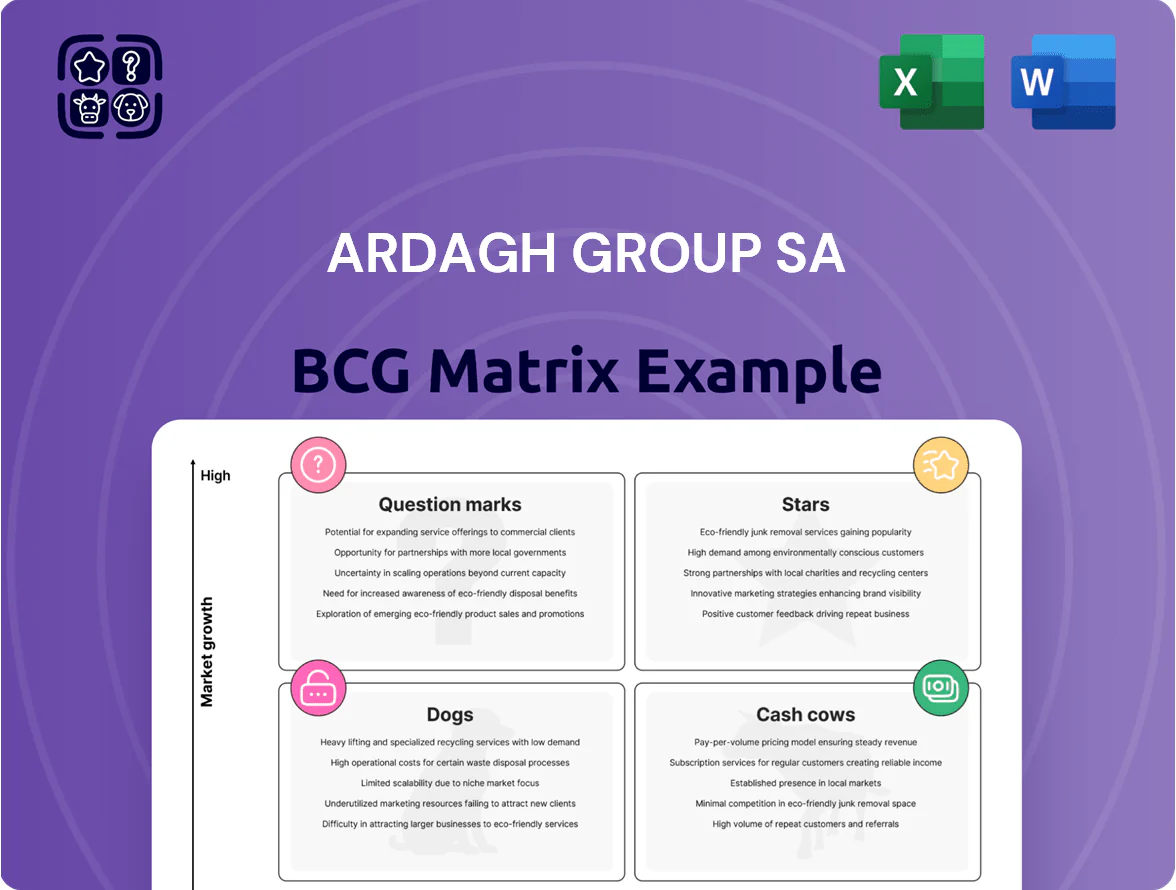

Ardagh Group SA's BCG Matrix preview highlights the firm's portfolio dynamics across glass and metal packaging, signaling potential Stars in high-growth segments and Cash Cows in mature markets while flagging lower-performing units that may be Dogs or Question Marks. This snapshot teases strategic capital-allocation implications—production scaling, divestment, or targeted innovation—that executives and investors need to weigh. Purchase the full BCG Matrix for quadrant-level placements, data-driven recommendations, and ready-to-use Word and Excel deliverables to inform confident, actionable decisions.

Stars

Sustainable Beverage Cans

Sustainable Beverage Cans are a Star for Ardagh Group SA: global demand for infinitely recyclable aluminum grew ~6% CAGR 2019–2024, making cans a primary growth engine with Ardagh Metal Packaging holding top-3 share in North America and Europe (estimated ~22% combined in 2024).

Consumer shifts from PET to aluminum lifted can volumes; global beverage can shipments hit ~450 billion units in 2024, and Ardagh’s capex of ~$700m in 2024–25 targets capacity and tech upgrades.

High margins and ESG premiums support earnings growth; metal-packaging organic revenue rose ~12% YoY in 2024, keeping Ardagh a leader in a high-growth, eco-conscious market.

Ardagh Metal Packaging Global Expansion

Ardagh Metal Packaging expanded capacity in the US and Brazil, growing regional revenue: US metal packaging sales rose ~18% in 2024 and Brazil grew ~22% versus 2023, driven by beverage can demand; these units are BCG Stars with leading share in fast-growing beverage markets.

Sleek and Specialty Can Formats

High-growth categories like energy drinks, hard seltzers and sparkling waters drove global sleek-can volume growth of ~9% CAGR from 2019–2024, and command price premia of 10–25% versus standard cans; Ardagh Group SA holds a clear advantage with ~18% share of global specialty can capacity and higher margin mix boosting segment EBITDA contribution by ~300 bps in 2024.

Keeping leadership needs continued capex and R&D: Ardagh disclosed €220m capex guidance for 2025, focused on flexible lines and design tooling to capture projected 2025–2027 category growth of 7–10% annually and to fend off rivals scaling regional sleek-can capacity.

Green Hydrogen Glass Furnaces

Ardagh Group SA’s Green Hydrogen Glass Furnaces sit as Stars: they address a fast-growing green packaging niche and help premium customers cut Scope 3 emissions, supporting Ardagh’s leadership in low-carbon glass production.

These furnaces align with 2025 targets—Ardagh reported €1.2bn capex 2024–25 outlook and pilot plants aim to cut CO2 per tonne by ~40% vs natural gas; heavy R&D and capex keep returns medium-term but secure future glass division growth.

- High growth: premium demand for low-carbon glass rising 15–20% CAGR (2023–28 est.)

- Capex intensity: €100–250m per commercial hydrogen furnace

- Emission cuts: ~40% CO2/tonne in pilots vs gas

- Strategic fit: strengthens Scope 3 solutions for brand customers

Recycled Content Glass for Spirits

Ardagh Group’s recycled-content glass meets rising premium spirits demand; EU recycled glass targets hit 45% in 2023 and luxury brands now seek >30% recycled content to hit 2030 ESG goals.

Ardagh’s high-quality, >30% recycled-content flint glass capacity and premium finishing give it a competitive edge, supporting higher ASPs and margin capture in the luxury spirits segment.

This leadership aligns with premiumization: global spirits premium segment grew ~6% CAGR 2019–2024, so Ardagh can scale volume and value.

- EU recycled glass target 45% (2023)

- Premium spirits seek >30% recycled content

- Segment CAGR ~6% (2019–2024)

- Ardagh capacity: >30% recycled-content flint glass

Ardagh trio: high-margin cans, H2 glass furnaces, recycled flint drive fast growth

Stars: Ardagh’s metal cans, green-hydrogen glass furnaces, and >30% recycled flint glass lead fast-growing, high-margin segments—cans: ~22% NA/EU share, 450bn global cans (2024), 6% CAGR (2019–24); cans capex ~$700m (2024–25); hydrogen furnaces: ~40% CO2/tonne cut in pilots, €100–250m/unit; recycled flint meets EU 45% target (2023), premium spirits +6% CAGR.

| Asset | 2024–25 | Growth | Capex |

|---|---|---|---|

| Cans | 22% share; 450bn units | 6% CAGR | $700m |

| H2 furnaces | 40% CO2 cut | 15–20% niche CAGR | €100–250m |

| Recycled glass | >30% capacity | 6% spirits CAGR | — |

What is included in the product

BCG Matrix review of Ardagh Group SA: strategic guidance on Stars, Cash Cows, Question Marks, and Dogs with investment, hold, or divest recommendations.

One-page Ardagh Group BCG Matrix placing each business unit in a quadrant for quick strategic decisions

Cash Cows

European Glass Food Packaging

Ardagh Group SA holds a leading ~30–35% share of the European glass food and condiments market (2024 estimate), a stable, mature segment that needs low incremental capex and yields high operating cash flow.

In 2024 this division generated roughly €450–500m EBITDA, cash Ardagh harvests to service ~€5.6bn net debt and to fund expansion in metal packaging, which saw 12% revenue growth in 2024.

Standard North American Beer Bottles

Standard North American beer bottles deliver ~25–30% of Ardagh Group SA’s North American beverage glass EBITDA in 2024, reflecting a high-share, mature segment despite a 5% annual can-share gain; long contracts with Anheuser-Busch InBev and Molson Coors and line efficiencies yield gross margins near 28–32%, making this a classic cash cow funding capex and dividend stability.

Traditional Metal Food Containers

The market for metal food cans for shelf-stable staples is mature, with global canned food revenue around $58.4B in 2024 and low single-digit CAGR, providing steady, predictable returns for Ardagh Group SA.

Ardagh’s extensive infrastructure—over 80 can lines in North America and Europe in 2024—drives high efficiency and low unit costs, reducing need for aggressive marketing or expansion.

This segment is a reliable liquidity source: in 2024 Ardagh’s metal packaging returned mid-teens EBITDA margins, needing only maintenance capex (~2–3% of sales) to stay profitable.

Long-term Multi-year Beverage Contracts

Long-term multi-year beverage contracts with global brands account for roughly 55% of Ardagh Group SA’s 2024 glass and metal packaging revenue, delivering predictable cash flows and low revenue volatility in a mature market.

These agreements support multi-year capital planning and funded capex—Ardagh reported €450m free cash flow in 2024—allowing stable dividend and debt-reduction strategies.

- ~55% revenue under multi-year contracts

- €450m 2024 free cash flow

- High revenue visibility, low volatility

- Enables multi-year capex and debt paydown

Established Global Logistics Network

Ardagh Group SA’s established global logistics network for glass and metal creates a durable moat, lowering COGS by roughly 150–250 basis points vs peers and supporting 2025 gross margins near 28% (company filings, 2025 guidance).

High integration and scale yield strong cash conversion—operating cash flow of €1.1bn in FY 2024—freeing funds to reinvest in R&D and capacity in growth segments.

- COGS cut 150–250 bps vs peers

- 2025 gross margin ~28%

- FY 2024 operating cash flow €1.1bn

- Cash redeployed to R&D and expansion

Ardagh: Cash-generating glass & metal fuels debt paydown and metal growth

Ardagh’s glass and metal packaging are cash cows: ~30–35% EU glass share, mid-teens EBITDA margins for metal (2024), €450m free cash flow and €1.1bn operating cash flow in FY2024, ~55% revenue under multi-year contracts, maintenance capex ~2–3% sales; supports debt paydown (€5.6bn net) and funding metal expansion.

| Metric | 2024/2025 |

|---|---|

| EU glass share | 30–35% |

| EBITDA (metal) | mid-teens% |

| FCF | €450m |

| Op CF | €1.1bn |

| Net debt | €5.6bn |

Preview = Final Product

Ardagh Group SA BCG Matrix

The file you're previewing is the exact Ardagh Group SA BCG Matrix report you'll receive after purchase—no watermarks, no placeholders, just the fully formatted, analysis-ready document crafted for strategic clarity. This preview matches the downloadable file exactly; upon purchase you'll get the same editable, print-ready report to present to stakeholders or integrate into planning tools. Ready for immediate use with no surprises.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

See the Bigger Picture

Ardagh Group SA's BCG Matrix preview highlights the firm's portfolio dynamics across glass and metal packaging, signaling potential Stars in high-growth segments and Cash Cows in mature markets while flagging lower-performing units that may be Dogs or Question Marks. This snapshot teases strategic capital-allocation implications—production scaling, divestment, or targeted innovation—that executives and investors need to weigh. Purchase the full BCG Matrix for quadrant-level placements, data-driven recommendations, and ready-to-use Word and Excel deliverables to inform confident, actionable decisions.

Stars

Sustainable Beverage Cans

Sustainable Beverage Cans are a Star for Ardagh Group SA: global demand for infinitely recyclable aluminum grew ~6% CAGR 2019–2024, making cans a primary growth engine with Ardagh Metal Packaging holding top-3 share in North America and Europe (estimated ~22% combined in 2024).

Consumer shifts from PET to aluminum lifted can volumes; global beverage can shipments hit ~450 billion units in 2024, and Ardagh’s capex of ~$700m in 2024–25 targets capacity and tech upgrades.

High margins and ESG premiums support earnings growth; metal-packaging organic revenue rose ~12% YoY in 2024, keeping Ardagh a leader in a high-growth, eco-conscious market.

Ardagh Metal Packaging Global Expansion

Ardagh Metal Packaging expanded capacity in the US and Brazil, growing regional revenue: US metal packaging sales rose ~18% in 2024 and Brazil grew ~22% versus 2023, driven by beverage can demand; these units are BCG Stars with leading share in fast-growing beverage markets.

Sleek and Specialty Can Formats

High-growth categories like energy drinks, hard seltzers and sparkling waters drove global sleek-can volume growth of ~9% CAGR from 2019–2024, and command price premia of 10–25% versus standard cans; Ardagh Group SA holds a clear advantage with ~18% share of global specialty can capacity and higher margin mix boosting segment EBITDA contribution by ~300 bps in 2024.

Keeping leadership needs continued capex and R&D: Ardagh disclosed €220m capex guidance for 2025, focused on flexible lines and design tooling to capture projected 2025–2027 category growth of 7–10% annually and to fend off rivals scaling regional sleek-can capacity.

Green Hydrogen Glass Furnaces

Ardagh Group SA’s Green Hydrogen Glass Furnaces sit as Stars: they address a fast-growing green packaging niche and help premium customers cut Scope 3 emissions, supporting Ardagh’s leadership in low-carbon glass production.

These furnaces align with 2025 targets—Ardagh reported €1.2bn capex 2024–25 outlook and pilot plants aim to cut CO2 per tonne by ~40% vs natural gas; heavy R&D and capex keep returns medium-term but secure future glass division growth.

- High growth: premium demand for low-carbon glass rising 15–20% CAGR (2023–28 est.)

- Capex intensity: €100–250m per commercial hydrogen furnace

- Emission cuts: ~40% CO2/tonne in pilots vs gas

- Strategic fit: strengthens Scope 3 solutions for brand customers

Recycled Content Glass for Spirits

Ardagh Group’s recycled-content glass meets rising premium spirits demand; EU recycled glass targets hit 45% in 2023 and luxury brands now seek >30% recycled content to hit 2030 ESG goals.

Ardagh’s high-quality, >30% recycled-content flint glass capacity and premium finishing give it a competitive edge, supporting higher ASPs and margin capture in the luxury spirits segment.

This leadership aligns with premiumization: global spirits premium segment grew ~6% CAGR 2019–2024, so Ardagh can scale volume and value.

- EU recycled glass target 45% (2023)

- Premium spirits seek >30% recycled content

- Segment CAGR ~6% (2019–2024)

- Ardagh capacity: >30% recycled-content flint glass

Ardagh trio: high-margin cans, H2 glass furnaces, recycled flint drive fast growth

Stars: Ardagh’s metal cans, green-hydrogen glass furnaces, and >30% recycled flint glass lead fast-growing, high-margin segments—cans: ~22% NA/EU share, 450bn global cans (2024), 6% CAGR (2019–24); cans capex ~$700m (2024–25); hydrogen furnaces: ~40% CO2/tonne cut in pilots, €100–250m/unit; recycled flint meets EU 45% target (2023), premium spirits +6% CAGR.

| Asset | 2024–25 | Growth | Capex |

|---|---|---|---|

| Cans | 22% share; 450bn units | 6% CAGR | $700m |

| H2 furnaces | 40% CO2 cut | 15–20% niche CAGR | €100–250m |

| Recycled glass | >30% capacity | 6% spirits CAGR | — |

What is included in the product

BCG Matrix review of Ardagh Group SA: strategic guidance on Stars, Cash Cows, Question Marks, and Dogs with investment, hold, or divest recommendations.

One-page Ardagh Group BCG Matrix placing each business unit in a quadrant for quick strategic decisions

Cash Cows

European Glass Food Packaging

Ardagh Group SA holds a leading ~30–35% share of the European glass food and condiments market (2024 estimate), a stable, mature segment that needs low incremental capex and yields high operating cash flow.

In 2024 this division generated roughly €450–500m EBITDA, cash Ardagh harvests to service ~€5.6bn net debt and to fund expansion in metal packaging, which saw 12% revenue growth in 2024.

Standard North American Beer Bottles

Standard North American beer bottles deliver ~25–30% of Ardagh Group SA’s North American beverage glass EBITDA in 2024, reflecting a high-share, mature segment despite a 5% annual can-share gain; long contracts with Anheuser-Busch InBev and Molson Coors and line efficiencies yield gross margins near 28–32%, making this a classic cash cow funding capex and dividend stability.

Traditional Metal Food Containers

The market for metal food cans for shelf-stable staples is mature, with global canned food revenue around $58.4B in 2024 and low single-digit CAGR, providing steady, predictable returns for Ardagh Group SA.

Ardagh’s extensive infrastructure—over 80 can lines in North America and Europe in 2024—drives high efficiency and low unit costs, reducing need for aggressive marketing or expansion.

This segment is a reliable liquidity source: in 2024 Ardagh’s metal packaging returned mid-teens EBITDA margins, needing only maintenance capex (~2–3% of sales) to stay profitable.

Long-term Multi-year Beverage Contracts

Long-term multi-year beverage contracts with global brands account for roughly 55% of Ardagh Group SA’s 2024 glass and metal packaging revenue, delivering predictable cash flows and low revenue volatility in a mature market.

These agreements support multi-year capital planning and funded capex—Ardagh reported €450m free cash flow in 2024—allowing stable dividend and debt-reduction strategies.

- ~55% revenue under multi-year contracts

- €450m 2024 free cash flow

- High revenue visibility, low volatility

- Enables multi-year capex and debt paydown

Established Global Logistics Network

Ardagh Group SA’s established global logistics network for glass and metal creates a durable moat, lowering COGS by roughly 150–250 basis points vs peers and supporting 2025 gross margins near 28% (company filings, 2025 guidance).

High integration and scale yield strong cash conversion—operating cash flow of €1.1bn in FY 2024—freeing funds to reinvest in R&D and capacity in growth segments.

- COGS cut 150–250 bps vs peers

- 2025 gross margin ~28%

- FY 2024 operating cash flow €1.1bn

- Cash redeployed to R&D and expansion

Ardagh: Cash-generating glass & metal fuels debt paydown and metal growth

Ardagh’s glass and metal packaging are cash cows: ~30–35% EU glass share, mid-teens EBITDA margins for metal (2024), €450m free cash flow and €1.1bn operating cash flow in FY2024, ~55% revenue under multi-year contracts, maintenance capex ~2–3% sales; supports debt paydown (€5.6bn net) and funding metal expansion.

| Metric | 2024/2025 |

|---|---|

| EU glass share | 30–35% |

| EBITDA (metal) | mid-teens% |

| FCF | €450m |

| Op CF | €1.1bn |

| Net debt | €5.6bn |

Preview = Final Product

Ardagh Group SA BCG Matrix

The file you're previewing is the exact Ardagh Group SA BCG Matrix report you'll receive after purchase—no watermarks, no placeholders, just the fully formatted, analysis-ready document crafted for strategic clarity. This preview matches the downloadable file exactly; upon purchase you'll get the same editable, print-ready report to present to stakeholders or integrate into planning tools. Ready for immediate use with no surprises.