Ardagh Group SA Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

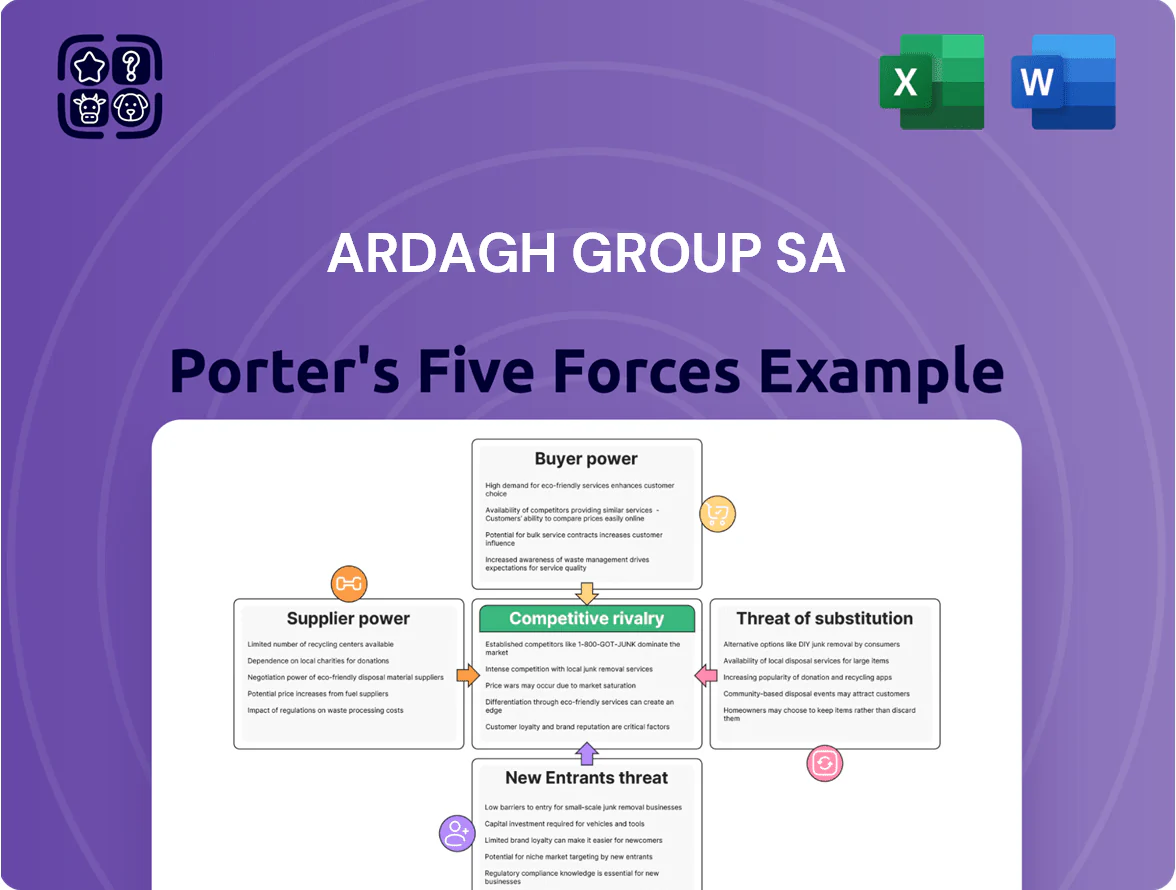

Ardagh Group SA faces intense rivalry from global packaging players, moderate supplier power for raw materials, and steady buyer leverage from large beverage and food clients, while capital barriers limit new entrants and substitutes pose niche threats from alternative packaging formats.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Ardagh Group SA’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw Material Price Volatility

The cost of aluminum and steel account for roughly 40–50% of Ardagh Group SA’s manufacturing costs, so global commodity swings materially affect margins; LME aluminum rose ~18% in 2024, increasing input risk. Suppliers are concentrated—top metal producers control large share—so pass-through pricing pressure is common. Ardagh uses hedging (forward contracts) and multi-year supply agreements to smooth costs; in 2024 about 60% of purchases were covered by contracts. What this estimate hides: regional freight and scrap premiums can still spike near-term.

Energy Dependency for Glass Production

Glass making is highly energy-intensive, with furnaces using ~60–70% of plant energy; natural gas and electricity cost 15–25% of COGS for European glassmakers in 2024, giving suppliers clear leverage.

European energy tightness—Russian gas cuts and 2022–24 price volatility—pushed industrial gas prices up 30–80% at times, raising Ardagh Group SA’s input risk.

Ardagh’s shift to renewables—targeting 40% onsite/contracted low‑carbon energy by 2026—aims to cut exposure and stabilize margins, lowering energy spend volatility.

Specialized Machinery and Technology

The production of high-quality metal and glass containers relies on specialized machinery and proprietary tech from few engineering firms; global suppliers like Krones and Sidel control key presses and IS machines, keeping supplier concentration high.

These suppliers exert power via deep technical expertise and high switching costs—retooling lines can cost tens of millions and take 6–18 months, raising lock-in for Ardagh Group SA (Ardagh reported €7.6bn capex incl. M&A 2023–2024).

Ardagh must keep strong vendor partnerships, long-term service contracts, and co-development deals to secure uptime, efficiency gains, and access to innovations such as lightweighting and digital process controls.

Availability of Recycled Materials

As demand for recycled cullet and aluminum scrap rises with circular-economy targets, suppliers gain pricing leverage—global recycled aluminum premiums reached about $300–$500/ton above primary in 2024, tightening margins for packagers.

Ardagh mitigates supplier power by investing in in-house recycling: in 2023 it processed ~800 kt of recycled glass/aluminum, lowering external scrap spend and stabilizing recycled-content supply for brand contracts.

- Higher supplier leverage: recycled premiums $300–$500/ton (2024)

- Brands demand >30–50% recycled content in some markets

- Ardagh recycled ~800 kt in 2023 to secure supply

- In-house recycling cuts exposure to volatile scrap markets

Logistical and Transportation Constraints

Shipping heavy glass and metal needs specialized carriers; global freight rates rose ~35% in 2021–22 and fuel still drove volatility, raising Ardagh Group SA's transport cost intensity—management reported logistics + raw materials pushed 2023 adjusted EBITDA margin pressure by ~120 basis points.

Logistics firms can squeeze margins during peak demand or strikes; Ardagh uses a 100+ location global footprint to reroute, consolidate loads, and cut per-unit transport, limiting exposure to spot freight spikes.

- Specialized logistics required; fuel volatility up to +/-20% impact on costs

- Freight rate surge 2021–22: ~35% increase

- Ardagh footprint: 100+ sites for route optimization

- Logistics added ~120 bps margin pressure in 2023

High supplier power: metals/glass drive costs; Ardagh hedges, boosts recycling & low‑carbon energy

Suppliers hold high bargaining power: metals/glass/energy account for ~40–50% of COGS, recycled premiums were $300–$500/ton in 2024, energy up 30–80% at peaks, and switching costs (retooling 6–18 months) are large; Ardagh hedges ~60% purchases, processed ~800 kt recycled in 2023, and targets 40% low‑carbon energy by 2026 to reduce supplier risk.

| Metric | 2023–24 |

|---|---|

| Metals/glass % of COGS | 40–50% |

| Recycled premium | $300–$500/ton (2024) |

| Recycled processed | ~800 kt (2023) |

| Purchases hedged | ~60% (2024) |

| Energy price spikes | +30–80% peaks |

What is included in the product

Tailored Porter's Five Forces for Ardagh Group SA, identifying competitive rivalry, supplier and buyer power, threat of substitutes, and entry barriers, highlighting disruptive packaging innovations, pricing pressures, and strategic defenses that shape its profitability and market position.

Concise Porter's Five Forces snapshot for Ardagh Group SA—ideal for rapid strategic decisions and investor briefings.

Customers Bargaining Power

Concentration of Large Global Brands

Ardagh serves multinational beverage and food giants like Coca‑Cola and Nestlé, whose purchasing power lets them demand volume discounts and extended payment terms; in 2024 Ardagh reported 2024 revenue of €9.1bn, so losing one large regional contract (often 5–10% of regional sales) would materially hit revenue and margins.

Multi-Year Contractual Agreements

Multi-year contracts give Ardagh Group SA predictable revenue—about 60% of FY2024 metal packaging sales were covered by multi-year deals—but fixed pricing and cost-pass-through clauses shift raw-material spike risk to Ardagh and cap margin upside. Customers, especially large beverage firms, use these clauses to shield against aluminum price swings (up 18% in 2024) and press for price resets at renewal. That creates a symbiotic but asymmetrical leverage: renewals favor sophisticated buyers and can compress Ardagh’s EBIT margins.

Low Switching Costs for Standard Products

Sustainability and ESG Mandates

- Customers demand low-carbon, high-recyclability packaging

- EU target: 65% glass recycling by 2030

- Ardagh 2023 emissions ~3.1 Mt CO2e

- R&D alignment required to avoid supplier switching

Backward Integration Threats

Large beverage firms like Coca-Cola and PepsiCo, with 2024 revenues of $46.0B and $86.6B respectively, can capex into in-house can/glass lines, creating a real backward-integration threat that limits Ardagh Group SA’s pricing power.

Ardagh mitigates this by selling scale: its 2024 adjusted EBITDA margin (~17%) and global engineering know-how deliver lower per-unit costs and faster innovation cycles that are hard for brands to replicate internally.

- High capex barrier but possible for top players

- 2024: Ardagh adj. EBITDA margin ~17%

- Threat caps price increases

- Ardagh’s scale, efficiency, tech expertise defend share

Buyers squeeze margins as Ardagh faces rising costs, emissions pressure, and glass overcapacity

Customers (Coca‑Cola, Nestlé) wield strong bargaining power: single contracts can be 5–10% regional sales; 2024 revenue €9.1bn; 60% metal sales on multi‑year deals; aluminum +18% in 2024; global glass overcapacity ~8%; Ardagh 2024 adj. EBITDA ~17%; 2023 emissions ~3.1 Mt CO2e—buyers push low‑carbon solutions, price discounts, and renewal resets, raising margin pressure.

| Metric | Value |

|---|---|

| 2024 revenue | €9.1bn |

| Metal sales multi‑year | 60% |

| Adj. EBITDA 2024 | ~17% |

| Aluminum 2024 | +18% |

| Glass overcapacity | ~8% |

| Emissions 2023 | ~3.1 Mt CO2e |

Preview Before You Purchase

Ardagh Group SA Porter's Five Forces Analysis

This preview shows the exact Ardagh Group SA Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders, no edits needed.

The document displayed here is the same professionally formatted file you'll be able to download and use the moment you buy, complete with conclusions and strategic implications.

You're viewing the final, ready-to-use analysis; once payment is complete you'll get instant access to this identical document.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Ardagh Group SA faces intense rivalry from global packaging players, moderate supplier power for raw materials, and steady buyer leverage from large beverage and food clients, while capital barriers limit new entrants and substitutes pose niche threats from alternative packaging formats.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Ardagh Group SA’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw Material Price Volatility

The cost of aluminum and steel account for roughly 40–50% of Ardagh Group SA’s manufacturing costs, so global commodity swings materially affect margins; LME aluminum rose ~18% in 2024, increasing input risk. Suppliers are concentrated—top metal producers control large share—so pass-through pricing pressure is common. Ardagh uses hedging (forward contracts) and multi-year supply agreements to smooth costs; in 2024 about 60% of purchases were covered by contracts. What this estimate hides: regional freight and scrap premiums can still spike near-term.

Energy Dependency for Glass Production

Glass making is highly energy-intensive, with furnaces using ~60–70% of plant energy; natural gas and electricity cost 15–25% of COGS for European glassmakers in 2024, giving suppliers clear leverage.

European energy tightness—Russian gas cuts and 2022–24 price volatility—pushed industrial gas prices up 30–80% at times, raising Ardagh Group SA’s input risk.

Ardagh’s shift to renewables—targeting 40% onsite/contracted low‑carbon energy by 2026—aims to cut exposure and stabilize margins, lowering energy spend volatility.

Specialized Machinery and Technology

The production of high-quality metal and glass containers relies on specialized machinery and proprietary tech from few engineering firms; global suppliers like Krones and Sidel control key presses and IS machines, keeping supplier concentration high.

These suppliers exert power via deep technical expertise and high switching costs—retooling lines can cost tens of millions and take 6–18 months, raising lock-in for Ardagh Group SA (Ardagh reported €7.6bn capex incl. M&A 2023–2024).

Ardagh must keep strong vendor partnerships, long-term service contracts, and co-development deals to secure uptime, efficiency gains, and access to innovations such as lightweighting and digital process controls.

Availability of Recycled Materials

As demand for recycled cullet and aluminum scrap rises with circular-economy targets, suppliers gain pricing leverage—global recycled aluminum premiums reached about $300–$500/ton above primary in 2024, tightening margins for packagers.

Ardagh mitigates supplier power by investing in in-house recycling: in 2023 it processed ~800 kt of recycled glass/aluminum, lowering external scrap spend and stabilizing recycled-content supply for brand contracts.

- Higher supplier leverage: recycled premiums $300–$500/ton (2024)

- Brands demand >30–50% recycled content in some markets

- Ardagh recycled ~800 kt in 2023 to secure supply

- In-house recycling cuts exposure to volatile scrap markets

Logistical and Transportation Constraints

Shipping heavy glass and metal needs specialized carriers; global freight rates rose ~35% in 2021–22 and fuel still drove volatility, raising Ardagh Group SA's transport cost intensity—management reported logistics + raw materials pushed 2023 adjusted EBITDA margin pressure by ~120 basis points.

Logistics firms can squeeze margins during peak demand or strikes; Ardagh uses a 100+ location global footprint to reroute, consolidate loads, and cut per-unit transport, limiting exposure to spot freight spikes.

- Specialized logistics required; fuel volatility up to +/-20% impact on costs

- Freight rate surge 2021–22: ~35% increase

- Ardagh footprint: 100+ sites for route optimization

- Logistics added ~120 bps margin pressure in 2023

High supplier power: metals/glass drive costs; Ardagh hedges, boosts recycling & low‑carbon energy

Suppliers hold high bargaining power: metals/glass/energy account for ~40–50% of COGS, recycled premiums were $300–$500/ton in 2024, energy up 30–80% at peaks, and switching costs (retooling 6–18 months) are large; Ardagh hedges ~60% purchases, processed ~800 kt recycled in 2023, and targets 40% low‑carbon energy by 2026 to reduce supplier risk.

| Metric | 2023–24 |

|---|---|

| Metals/glass % of COGS | 40–50% |

| Recycled premium | $300–$500/ton (2024) |

| Recycled processed | ~800 kt (2023) |

| Purchases hedged | ~60% (2024) |

| Energy price spikes | +30–80% peaks |

What is included in the product

Tailored Porter's Five Forces for Ardagh Group SA, identifying competitive rivalry, supplier and buyer power, threat of substitutes, and entry barriers, highlighting disruptive packaging innovations, pricing pressures, and strategic defenses that shape its profitability and market position.

Concise Porter's Five Forces snapshot for Ardagh Group SA—ideal for rapid strategic decisions and investor briefings.

Customers Bargaining Power

Concentration of Large Global Brands

Ardagh serves multinational beverage and food giants like Coca‑Cola and Nestlé, whose purchasing power lets them demand volume discounts and extended payment terms; in 2024 Ardagh reported 2024 revenue of €9.1bn, so losing one large regional contract (often 5–10% of regional sales) would materially hit revenue and margins.

Multi-Year Contractual Agreements

Multi-year contracts give Ardagh Group SA predictable revenue—about 60% of FY2024 metal packaging sales were covered by multi-year deals—but fixed pricing and cost-pass-through clauses shift raw-material spike risk to Ardagh and cap margin upside. Customers, especially large beverage firms, use these clauses to shield against aluminum price swings (up 18% in 2024) and press for price resets at renewal. That creates a symbiotic but asymmetrical leverage: renewals favor sophisticated buyers and can compress Ardagh’s EBIT margins.

Low Switching Costs for Standard Products

Sustainability and ESG Mandates

- Customers demand low-carbon, high-recyclability packaging

- EU target: 65% glass recycling by 2030

- Ardagh 2023 emissions ~3.1 Mt CO2e

- R&D alignment required to avoid supplier switching

Backward Integration Threats

Large beverage firms like Coca-Cola and PepsiCo, with 2024 revenues of $46.0B and $86.6B respectively, can capex into in-house can/glass lines, creating a real backward-integration threat that limits Ardagh Group SA’s pricing power.

Ardagh mitigates this by selling scale: its 2024 adjusted EBITDA margin (~17%) and global engineering know-how deliver lower per-unit costs and faster innovation cycles that are hard for brands to replicate internally.

- High capex barrier but possible for top players

- 2024: Ardagh adj. EBITDA margin ~17%

- Threat caps price increases

- Ardagh’s scale, efficiency, tech expertise defend share

Buyers squeeze margins as Ardagh faces rising costs, emissions pressure, and glass overcapacity

Customers (Coca‑Cola, Nestlé) wield strong bargaining power: single contracts can be 5–10% regional sales; 2024 revenue €9.1bn; 60% metal sales on multi‑year deals; aluminum +18% in 2024; global glass overcapacity ~8%; Ardagh 2024 adj. EBITDA ~17%; 2023 emissions ~3.1 Mt CO2e—buyers push low‑carbon solutions, price discounts, and renewal resets, raising margin pressure.

| Metric | Value |

|---|---|

| 2024 revenue | €9.1bn |

| Metal sales multi‑year | 60% |

| Adj. EBITDA 2024 | ~17% |

| Aluminum 2024 | +18% |

| Glass overcapacity | ~8% |

| Emissions 2023 | ~3.1 Mt CO2e |

Preview Before You Purchase

Ardagh Group SA Porter's Five Forces Analysis

This preview shows the exact Ardagh Group SA Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders, no edits needed.

The document displayed here is the same professionally formatted file you'll be able to download and use the moment you buy, complete with conclusions and strategic implications.

You're viewing the final, ready-to-use analysis; once payment is complete you'll get instant access to this identical document.