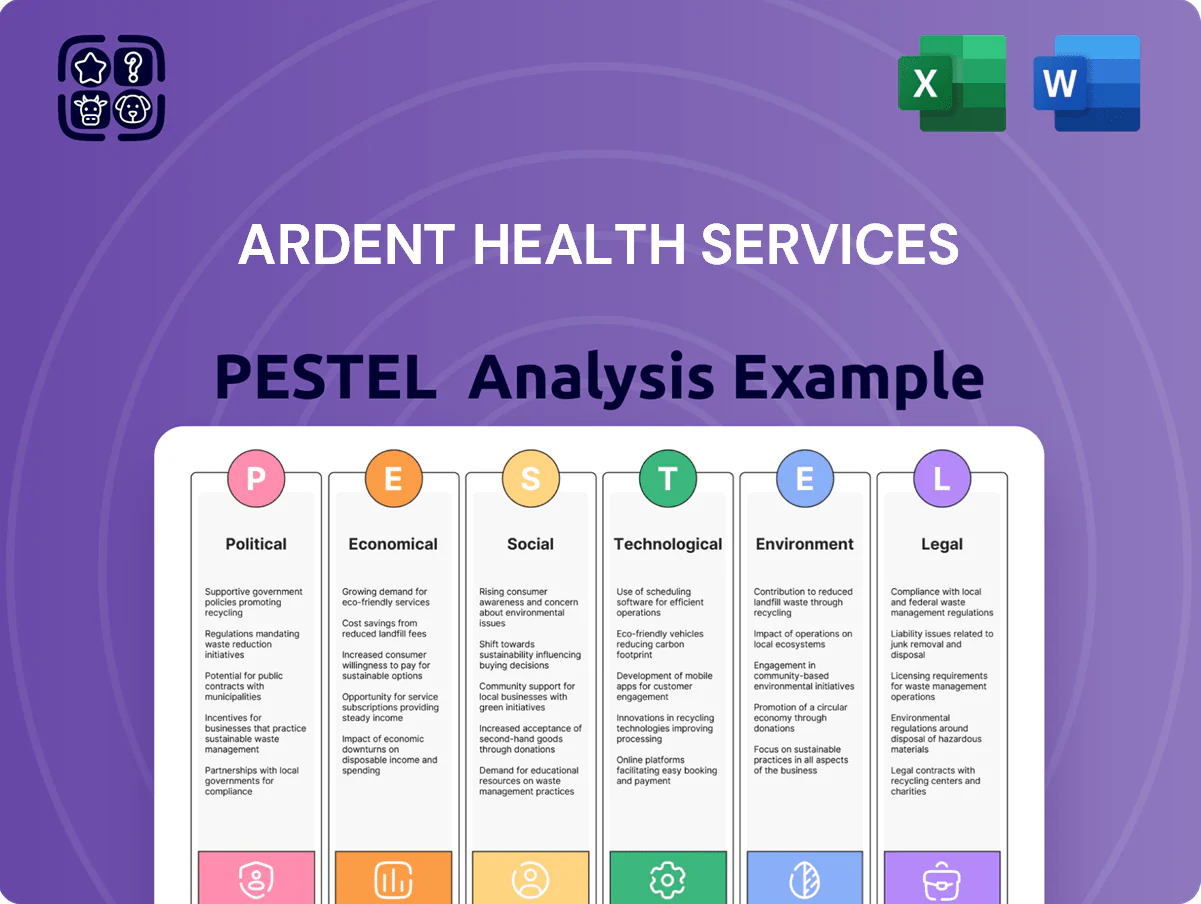

Ardent Health Services PESTLE Analysis

Your Competitive Advantage Starts with This Report

Discover how political shifts, regulatory pressures, and technological advances are reshaping Ardent Health Services’ strategic landscape—our concise PESTLE snapshot highlights risks and growth levers you need to know. Purchase the full PESTLE Analysis to access actionable insights, detailed evidence, and ready-to-use charts for investment, strategy, or competitive planning.

Political factors

Federal Healthcare Policy and Reimbursement Rates

Decisions by CMS on Medicare and Medicaid reimbursement rates directly affect Ardent’s revenue—Medicare accounted for about 28% of US hospital inpatient revenue in 2023, so rate adjustments can swing margins materially.

By late 2025 CMS accelerated value-based payments, with Medicare VBP penetrations rising toward 40% of payments, forcing Ardent to retool billing, care pathways, and IT to protect revenue.

Ongoing congressional debates over the Affordable Care Act sustain policy uncertainty, complicating Ardent’s multi-year capital and network expansion plans.

State-Level Certificate of Need Regulations

Ardent operates in 16 states where Certificate of Need (CON) rules vary; 12 states have active CON programs that can restrict new hospital beds or specialty services, potentially slowing Ardent’s planned expansions and impacting capital allocation (2024 capex trends show US hospital construction down ~8%).

CON laws can deter competitors from entering some markets but also limit Ardent’s quick scaling—delays can add months and increase project costs by an estimated 5–12% in regional healthcare builds.

Mitigating this requires targeted state lobbying, maintaining relationships with 50+ state/regional health planning bodies Ardent engages, and deploying legal/regulatory teams versed in local healthcare planning to accelerate approvals.

Governmental Support for Rural Healthcare

Many of Ardent Health Services facilities operate in mid-sized and rural markets that depend on federal and state grants—rural hospitals received about $14.2 billion in grant/relief funding 2023–2024—creating avenues for Ardent to tap targeted programs reducing healthcare disparities. Recent federal initiatives, including the 2024 Rural Health Strategy, expand funding streams, but political shifts risk sudden subsidy cuts that could endanger smaller regional clinics.

Trade Policies and Medical Supply Chain Security

Political tensions and trade policies raising tariffs and export controls increased Ardent Health Services’ imported medical equipment costs by an estimated 4–6% in 2024, pressuring margins and capex plans.

Federal mandates by end-2025 to onshore critical-medical manufacturing—backed by $3.5bn in federal incentives in 2024–25—force Ardent to diversify suppliers and incur higher procurement and inventory costs.

Instability in key supplier regions produced shipment delays that raised inventory days by ~8% in 2024, risking timely care delivery during peak demand periods.

- Tariff-driven cost increase: 4–6% (2024)

- Federal onshoring incentives: $3.5bn (2024–25)

- Inventory days up ~8% due to regional instability (2024)

Public Health Funding and Pandemic Preparedness

Government allocations to public health infrastructure shape Ardent’s emergency readiness; federal COVID-19 preparedness grants totaled about $10.5B in FY2024, affecting hospital funding flows and capital for surge capacity.

State and federal emphasis on mental health and opioid programs—e.g., $5B federal investments in 2024-25 behavioral health initiatives—creates growth opportunities for Ardent’s specialized service lines.

State-level political shifts can swing Medicaid expansion and public health budgets—Medicaid spending rose ~6% YoY in 2024—causing revenue and service-planning variability for Ardent.

- FY2024 federal preparedness grants ~$10.5B

- $5B federal behavioral health investment 2024-25

- Medicaid spend +6% YoY 2024 impacting hospital reimbursements

Policy shifts, costs and grants reshape Ardent’s revenue outlook—VBP, tariffs, incentives

CMS reimbursement shifts, Medicare VBP rise (~40% by 2025) and Medicaid spend (+6% YoY 2024) materially affect Ardent revenue; CON laws in 12 states slow expansions (adds 5–12% project costs); tariffs raised equipment costs 4–6% (2024) while federal onshoring incentives $3.5B (2024–25) and $10.5B preparedness grants (FY2024) create both costs and funding opportunities.

| Metric | Value |

|---|---|

| Medicare VBP | ~40% (2025) |

| Medicaid spend | +6% YoY (2024) |

| Tariff cost rise | 4–6% (2024) |

| Onshoring incentives | $3.5B (2024–25) |

What is included in the product

Explores how macro-environmental forces uniquely affect Ardent Health Services across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific examples to identify threats and opportunities for executives and investors.

A concise PESTLE summary of Ardent Health Services that’s visually segmented for quick interpretation, ideal for dropping into presentations or sharing across teams to streamline external risk discussions and strategic planning.

Economic factors

Inflationary Pressures on Labor and Supplies

Rising medical supply prices and a tight labor market pushed Ardent Health Services' operating expenses up an estimated 6–8% annually through 2025, with national hospital wage growth near 5.2% in 2024 and U.S. healthcare commodity inflation at ~7% year-over-year.

Higher inflation raised Ardent's cost of capital for new builds—mortgage spreads and construction costs up ~10% in 2024—while accelerating maintenance and replacement cycles for medical technology.

To protect margins, Ardent must pursue aggressive cost-management—supply-chain consolidation, labor productivity programs, and targeted capital deferrals—while preserving clinical quality metrics and patient outcomes.

Interest Rate Environment and Debt Servicing

As of late 2025, the US Federal Funds Rate near 5.25–5.50% has pushed Ardent Health Services' borrowing costs higher, squeezing acquisition firepower and raising interest expense on its ~3.2 billion USD reported long-term liabilities.

Higher rates elevate debt servicing costs, constraining expansion and capital deployment; analysts track Ardent's debt-to-equity (~2.1x trailing) to gauge vulnerability to credit-market shifts and refinancing risk.

Regional Economic Health and Payer Mix

Regional economic health shapes Ardent Health Services payer mix: prosperous markets saw employer-sponsored coverage rise to 58–62% in 2024, yielding higher commercial reimbursements versus Medicaid. In regions with slower growth or job losses, Medicaid and uninsured shares climbed—Medicaid enrollment grew about 3.5% nationally in 2023–24—pressuring margins. Local downturns also increased uncompensated care; hospitals reported median uncompensated care ratios rising to ~1.8% of net patient revenue in 2024.

Consumer Healthcare Spending Patterns

As high-deductible health plans cover 34% of US workers in 2024, patients behave as price-sensitive consumers, pressuring Ardent to increase price transparency and emphasize bundled-value care and patient experience to retain volumes.

In 2023–24 economic softness saw elective procedure volumes fall 6–9% industry-wide, risking margin erosion for Ardent since electives drive higher hospital EBITDA.

- 34% of US workers in HDHPs (2024)

- Elective volumes down 6–9% (2023–24)

- Need for transparent pricing, value-based offerings

Consolidation Trends in the Healthcare Market

Economic pressures are driving consolidation: U.S. hospital M&A deal value reached about $52.6 billion in 2023 and continued into 2024–25, pushing larger systems to acquire independents to cut costs and expand market share.

Ardent must choose between acquisitions or joint ventures to realize scale economies and lower per-patient costs while balancing integration risk.

Consolidation boosts supplier bargaining power and payor leverage but raises antitrust scrutiny—FTC hospital investigations rose notably after 2022.

- 2023 U.S. hospital M&A deal value ~ $52.6B

- Scale reduces per-patient cost, improves negotiating leverage

- Increased antitrust enforcement risk (FTC investigations uptick post-2022)

Rising costs, higher rates, and shrinking elective volumes squeeze Ardent—M&A heats up

Rising input costs and wage inflation (~5.2% wage growth, ~7% commodity inflation in 2024) raised Ardent's operating costs 6–8% annually; Fed funds ~5.25–5.50% (late 2025) increased borrowing costs against ~$3.2B long-term liabilities and ~2.1x debt/equity; elective volumes fell 6–9% (2023–24) while HDHPs hit 34% (2024), pressuring margins and driving M&A (~$52.6B deal value in 2023).

| Metric | Value |

|---|---|

| Wage growth (2024) | 5.2% |

| Commodity inflation (2024) | ~7% |

| Fed funds (late 2025) | 5.25–5.50% |

| Long-term liabilities | $3.2B |

| Debt/Equity (trailing) | ~2.1x |

| HDHP prevalence (2024) | 34% |

| Elective volume change (2023–24) | -6 to -9% |

| Hospital M&A (2023) | $52.6B |

Preview the Actual Deliverable

Ardent Health Services PESTLE Analysis

The preview shown here is the exact Ardent Health Services PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or investor review.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Discover how political shifts, regulatory pressures, and technological advances are reshaping Ardent Health Services’ strategic landscape—our concise PESTLE snapshot highlights risks and growth levers you need to know. Purchase the full PESTLE Analysis to access actionable insights, detailed evidence, and ready-to-use charts for investment, strategy, or competitive planning.

Political factors

Federal Healthcare Policy and Reimbursement Rates

Decisions by CMS on Medicare and Medicaid reimbursement rates directly affect Ardent’s revenue—Medicare accounted for about 28% of US hospital inpatient revenue in 2023, so rate adjustments can swing margins materially.

By late 2025 CMS accelerated value-based payments, with Medicare VBP penetrations rising toward 40% of payments, forcing Ardent to retool billing, care pathways, and IT to protect revenue.

Ongoing congressional debates over the Affordable Care Act sustain policy uncertainty, complicating Ardent’s multi-year capital and network expansion plans.

State-Level Certificate of Need Regulations

Ardent operates in 16 states where Certificate of Need (CON) rules vary; 12 states have active CON programs that can restrict new hospital beds or specialty services, potentially slowing Ardent’s planned expansions and impacting capital allocation (2024 capex trends show US hospital construction down ~8%).

CON laws can deter competitors from entering some markets but also limit Ardent’s quick scaling—delays can add months and increase project costs by an estimated 5–12% in regional healthcare builds.

Mitigating this requires targeted state lobbying, maintaining relationships with 50+ state/regional health planning bodies Ardent engages, and deploying legal/regulatory teams versed in local healthcare planning to accelerate approvals.

Governmental Support for Rural Healthcare

Many of Ardent Health Services facilities operate in mid-sized and rural markets that depend on federal and state grants—rural hospitals received about $14.2 billion in grant/relief funding 2023–2024—creating avenues for Ardent to tap targeted programs reducing healthcare disparities. Recent federal initiatives, including the 2024 Rural Health Strategy, expand funding streams, but political shifts risk sudden subsidy cuts that could endanger smaller regional clinics.

Trade Policies and Medical Supply Chain Security

Political tensions and trade policies raising tariffs and export controls increased Ardent Health Services’ imported medical equipment costs by an estimated 4–6% in 2024, pressuring margins and capex plans.

Federal mandates by end-2025 to onshore critical-medical manufacturing—backed by $3.5bn in federal incentives in 2024–25—force Ardent to diversify suppliers and incur higher procurement and inventory costs.

Instability in key supplier regions produced shipment delays that raised inventory days by ~8% in 2024, risking timely care delivery during peak demand periods.

- Tariff-driven cost increase: 4–6% (2024)

- Federal onshoring incentives: $3.5bn (2024–25)

- Inventory days up ~8% due to regional instability (2024)

Public Health Funding and Pandemic Preparedness

Government allocations to public health infrastructure shape Ardent’s emergency readiness; federal COVID-19 preparedness grants totaled about $10.5B in FY2024, affecting hospital funding flows and capital for surge capacity.

State and federal emphasis on mental health and opioid programs—e.g., $5B federal investments in 2024-25 behavioral health initiatives—creates growth opportunities for Ardent’s specialized service lines.

State-level political shifts can swing Medicaid expansion and public health budgets—Medicaid spending rose ~6% YoY in 2024—causing revenue and service-planning variability for Ardent.

- FY2024 federal preparedness grants ~$10.5B

- $5B federal behavioral health investment 2024-25

- Medicaid spend +6% YoY 2024 impacting hospital reimbursements

Policy shifts, costs and grants reshape Ardent’s revenue outlook—VBP, tariffs, incentives

CMS reimbursement shifts, Medicare VBP rise (~40% by 2025) and Medicaid spend (+6% YoY 2024) materially affect Ardent revenue; CON laws in 12 states slow expansions (adds 5–12% project costs); tariffs raised equipment costs 4–6% (2024) while federal onshoring incentives $3.5B (2024–25) and $10.5B preparedness grants (FY2024) create both costs and funding opportunities.

| Metric | Value |

|---|---|

| Medicare VBP | ~40% (2025) |

| Medicaid spend | +6% YoY (2024) |

| Tariff cost rise | 4–6% (2024) |

| Onshoring incentives | $3.5B (2024–25) |

What is included in the product

Explores how macro-environmental forces uniquely affect Ardent Health Services across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific examples to identify threats and opportunities for executives and investors.

A concise PESTLE summary of Ardent Health Services that’s visually segmented for quick interpretation, ideal for dropping into presentations or sharing across teams to streamline external risk discussions and strategic planning.

Economic factors

Inflationary Pressures on Labor and Supplies

Rising medical supply prices and a tight labor market pushed Ardent Health Services' operating expenses up an estimated 6–8% annually through 2025, with national hospital wage growth near 5.2% in 2024 and U.S. healthcare commodity inflation at ~7% year-over-year.

Higher inflation raised Ardent's cost of capital for new builds—mortgage spreads and construction costs up ~10% in 2024—while accelerating maintenance and replacement cycles for medical technology.

To protect margins, Ardent must pursue aggressive cost-management—supply-chain consolidation, labor productivity programs, and targeted capital deferrals—while preserving clinical quality metrics and patient outcomes.

Interest Rate Environment and Debt Servicing

As of late 2025, the US Federal Funds Rate near 5.25–5.50% has pushed Ardent Health Services' borrowing costs higher, squeezing acquisition firepower and raising interest expense on its ~3.2 billion USD reported long-term liabilities.

Higher rates elevate debt servicing costs, constraining expansion and capital deployment; analysts track Ardent's debt-to-equity (~2.1x trailing) to gauge vulnerability to credit-market shifts and refinancing risk.

Regional Economic Health and Payer Mix

Regional economic health shapes Ardent Health Services payer mix: prosperous markets saw employer-sponsored coverage rise to 58–62% in 2024, yielding higher commercial reimbursements versus Medicaid. In regions with slower growth or job losses, Medicaid and uninsured shares climbed—Medicaid enrollment grew about 3.5% nationally in 2023–24—pressuring margins. Local downturns also increased uncompensated care; hospitals reported median uncompensated care ratios rising to ~1.8% of net patient revenue in 2024.

Consumer Healthcare Spending Patterns

As high-deductible health plans cover 34% of US workers in 2024, patients behave as price-sensitive consumers, pressuring Ardent to increase price transparency and emphasize bundled-value care and patient experience to retain volumes.

In 2023–24 economic softness saw elective procedure volumes fall 6–9% industry-wide, risking margin erosion for Ardent since electives drive higher hospital EBITDA.

- 34% of US workers in HDHPs (2024)

- Elective volumes down 6–9% (2023–24)

- Need for transparent pricing, value-based offerings

Consolidation Trends in the Healthcare Market

Economic pressures are driving consolidation: U.S. hospital M&A deal value reached about $52.6 billion in 2023 and continued into 2024–25, pushing larger systems to acquire independents to cut costs and expand market share.

Ardent must choose between acquisitions or joint ventures to realize scale economies and lower per-patient costs while balancing integration risk.

Consolidation boosts supplier bargaining power and payor leverage but raises antitrust scrutiny—FTC hospital investigations rose notably after 2022.

- 2023 U.S. hospital M&A deal value ~ $52.6B

- Scale reduces per-patient cost, improves negotiating leverage

- Increased antitrust enforcement risk (FTC investigations uptick post-2022)

Rising costs, higher rates, and shrinking elective volumes squeeze Ardent—M&A heats up

Rising input costs and wage inflation (~5.2% wage growth, ~7% commodity inflation in 2024) raised Ardent's operating costs 6–8% annually; Fed funds ~5.25–5.50% (late 2025) increased borrowing costs against ~$3.2B long-term liabilities and ~2.1x debt/equity; elective volumes fell 6–9% (2023–24) while HDHPs hit 34% (2024), pressuring margins and driving M&A (~$52.6B deal value in 2023).

| Metric | Value |

|---|---|

| Wage growth (2024) | 5.2% |

| Commodity inflation (2024) | ~7% |

| Fed funds (late 2025) | 5.25–5.50% |

| Long-term liabilities | $3.2B |

| Debt/Equity (trailing) | ~2.1x |

| HDHP prevalence (2024) | 34% |

| Elective volume change (2023–24) | -6 to -9% |

| Hospital M&A (2023) | $52.6B |

Preview the Actual Deliverable

Ardent Health Services PESTLE Analysis

The preview shown here is the exact Ardent Health Services PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or investor review.