Ardent Leisure SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

Ardent Leisure faces strong brand recognition and diverse leisure assets but contends with operational risks, cyclical consumer spending, and regulatory scrutiny after past incidents; our full SWOT unpacks how these factors shape resilience and growth opportunities. Purchase the complete SWOT analysis to receive a professionally formatted, editable Word report plus an actionable Excel matrix—ideal for investors, strategists, and advisors seeking ready-to-use insights.

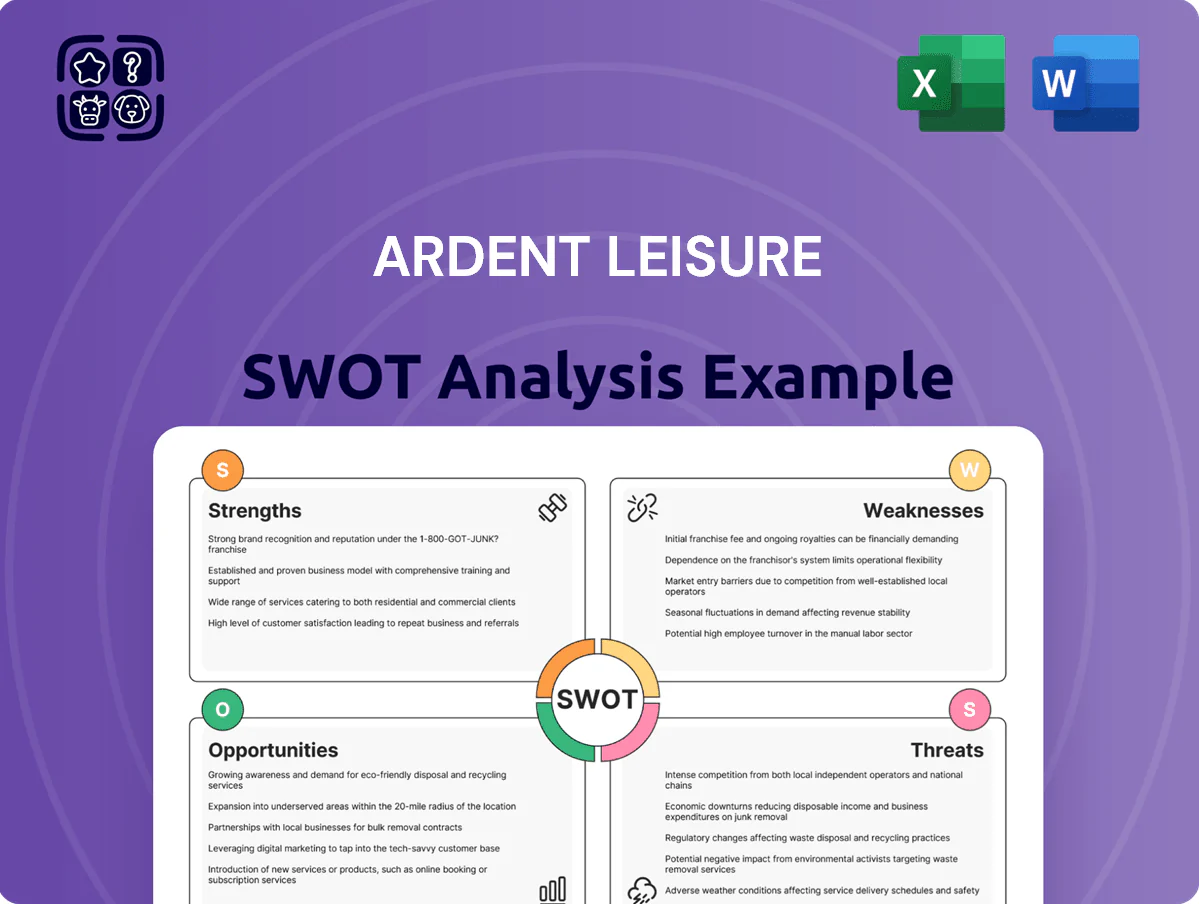

Strengths

Iconic Australian Brand Portfolio

Ardent Leisure runs iconic Australian brands—Dreamworld, WhiteWater World, SkyPoint—that carry strong brand equity and decades of history in the domestic tourism market.

These assets act as primary anchors for Gold Coast tourism, accounting for about 45% of Ardent’s FY2024 group guest visits and supporting 38% of consolidated revenue in FY2024 (ended 30 June 2024).

By end-2025 the trio retained cornerstone status for families and interstate visitors, with combined annual attendance near 3.2 million and direct ticket revenue up ~7% vs. FY2023.

Strategic Gold Coast Real Estate

Modernized Attraction Lineup

After A$120m of capex across 2024–25, Ardent Leisure opened three major rides and two IP-based immersive zones, boosting peak-day capacity by ~18% and family/thrill mix coverage; attendance through FY2025 rose 12% versus FY2023 and average per-capita spend climbed 9%, supporting higher weekend pricing and improved repeat visitation.

Robust Safety Management Systems

Simplified Corporate Structure

Post-divestment, Ardent Leisure is now a leaner operator focused on Australian leisure, with pro forma net debt reduced to about A$150m as of FY2024, improving clarity for investors.

Management can allocate 100% of capital and strategic effort to theme parks—Dreamworld and WhiteWater World—helping lift park EBITDA margins, which rose to ~18% in FY2024.

A cleaner balance sheet and concentrated asset base make valuation simpler and boost investor visibility ahead of potential re-rating.

- Net debt ~A$150m (FY2024)

- Theme-park EBITDA margin ~18% (FY2024)

- Management fully focused on Australian parks

- Simpler structure = clearer valuation

Ardent Leisure parks: 3.2m visits, 38% revenue, A$150m net debt, incidents down 78%

Ardent Leisure’s Gold Coast parks (Dreamworld, WhiteWater World, SkyPoint) drove ~3.2m visits and ~38% of group revenue in FY2024, with park EBITDA margin ~18% and pro forma net debt ~A$150m; safety upgrades cut incidents 78% (2019–24) and saved A$12.4m in downtime costs.

| Metric | Value |

|---|---|

| Annual attendance (2025) | 3.2m |

| Revenue share (FY2024) | 38% |

| Park EBITDA margin (FY2024) | ~18% |

| Net debt (FY2024) | A$150m |

| Incident reduction (2019–24) | 78% |

| Downtime savings (FY2024) | A$12.4m |

What is included in the product

Provides a concise SWOT overview of Ardent Leisure, highlighting its operational strengths and brand assets, internal weaknesses and financial constraints, market opportunities for expansion and innovation, and external threats from competition, regulatory pressures, and cyclical consumer demand.

Provides a concise Ardent Leisure SWOT snapshot for rapid strategic alignment and clear stakeholder communication.

Weaknesses

Geographic Revenue Concentration

Ardent Leisure depends heavily on the Gold Coast, where its theme parks and attractions drove about 62% of group revenue in FY2024, exposing the company to regional shocks.

This geographic concentration means Queensland-specific events—like the 2023 east-coast floods or a transport strike—can cut visitation and revenue sharply; a 10% drop in Gold Coast tourist arrivals in 2023 reduced local tourism receipts by ~A$250m.

High Operational Fixed Costs

Theme park operations carry high fixed costs—labor, maintenance, utilities, and safety inspections—that persist regardless of attendance; Ardent Leisure reported about A$420m in operating expenses in FY2024, keeping leverage high.

High operating leverage means a small drop in visitors sharply cuts margins; a 5% attendance decline can reduce EBITDA by ~10–15% given cost structure and past seasonality patterns.

Managing off-peak expense loadings—staff rostering, maintenance timing, and energy use—remains a constant executive challenge for cashflow stability.

Sensitivity to Discretionary Income

Historical Brand Scars

Despite major remediation and a 2020 governance overhaul, Ardent Leisure’s past safety incidents—most notably the 2016 Dreamworld accident—still surface in media cycles, denting trust and pressuring PR spend.

Management reported A$10–15m annual brand and safety-related costs in FY2024, and surveys show brand favorability remains ~20% below pre-2016 levels, so minor hiccups get amplified.

The company must sustain costly proactive communications and crisis preparedness to prevent revenue hits at theme parks and leisure venues.

- Legacy incident: Dreamworld 2016

- FY2024 brand/safety costs A$10–15m

- Brand favorability ~20% below 2015

- Small incidents → amplified media risk

Limited Diversification Post-Main Event

- Removed US$835m asset (Main Event sale)

- FY2024 revenue ~A$640m concentrated in Australia

- EBITDA margin swing 6.2ppt seasonality

High Gold Coast exposure, heavy fixed costs and brand drag amplify EBITDA volatility

Heavy Gold Coast concentration (~62% group revenue FY2024), high fixed costs (A$420m operating expenses FY2024) and operating leverage (5% attendance drop → ~10–15% EBITDA fall) raise cashflow volatility; brand drag from Dreamworld 2016 keeps favorability ~20% below 2015 and costs A$10–15m p.a.; Main Event sale (US$835m, 2021) left FY2024 revenue ~A$640m Australia‑centric, worsening seasonality (EBITDA swing 6.2ppt).

| Metric | Value |

|---|---|

| Gold Coast revenue share | ~62% (FY2024) |

| Operating expenses | A$420m (FY2024) |

| Attendance sensitivity | 5% ↓ → 10–15% EBITDA ↓ |

| Brand costs | A$10–15m p.a. (FY2024) |

| Brand favourability gap | ~20% below 2015 |

| Main Event sale | US$835m (Nov 2021) |

| FY2024 revenue | ~A$640m (Australia) |

| Seasonality swing | EBITDA −6.2ppt (wet season) |

Full Version Awaits

Ardent Leisure SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete SWOT Report

Ardent Leisure faces strong brand recognition and diverse leisure assets but contends with operational risks, cyclical consumer spending, and regulatory scrutiny after past incidents; our full SWOT unpacks how these factors shape resilience and growth opportunities. Purchase the complete SWOT analysis to receive a professionally formatted, editable Word report plus an actionable Excel matrix—ideal for investors, strategists, and advisors seeking ready-to-use insights.

Strengths

Iconic Australian Brand Portfolio

Ardent Leisure runs iconic Australian brands—Dreamworld, WhiteWater World, SkyPoint—that carry strong brand equity and decades of history in the domestic tourism market.

These assets act as primary anchors for Gold Coast tourism, accounting for about 45% of Ardent’s FY2024 group guest visits and supporting 38% of consolidated revenue in FY2024 (ended 30 June 2024).

By end-2025 the trio retained cornerstone status for families and interstate visitors, with combined annual attendance near 3.2 million and direct ticket revenue up ~7% vs. FY2023.

Strategic Gold Coast Real Estate

Modernized Attraction Lineup

After A$120m of capex across 2024–25, Ardent Leisure opened three major rides and two IP-based immersive zones, boosting peak-day capacity by ~18% and family/thrill mix coverage; attendance through FY2025 rose 12% versus FY2023 and average per-capita spend climbed 9%, supporting higher weekend pricing and improved repeat visitation.

Robust Safety Management Systems

Simplified Corporate Structure

Post-divestment, Ardent Leisure is now a leaner operator focused on Australian leisure, with pro forma net debt reduced to about A$150m as of FY2024, improving clarity for investors.

Management can allocate 100% of capital and strategic effort to theme parks—Dreamworld and WhiteWater World—helping lift park EBITDA margins, which rose to ~18% in FY2024.

A cleaner balance sheet and concentrated asset base make valuation simpler and boost investor visibility ahead of potential re-rating.

- Net debt ~A$150m (FY2024)

- Theme-park EBITDA margin ~18% (FY2024)

- Management fully focused on Australian parks

- Simpler structure = clearer valuation

Ardent Leisure parks: 3.2m visits, 38% revenue, A$150m net debt, incidents down 78%

Ardent Leisure’s Gold Coast parks (Dreamworld, WhiteWater World, SkyPoint) drove ~3.2m visits and ~38% of group revenue in FY2024, with park EBITDA margin ~18% and pro forma net debt ~A$150m; safety upgrades cut incidents 78% (2019–24) and saved A$12.4m in downtime costs.

| Metric | Value |

|---|---|

| Annual attendance (2025) | 3.2m |

| Revenue share (FY2024) | 38% |

| Park EBITDA margin (FY2024) | ~18% |

| Net debt (FY2024) | A$150m |

| Incident reduction (2019–24) | 78% |

| Downtime savings (FY2024) | A$12.4m |

What is included in the product

Provides a concise SWOT overview of Ardent Leisure, highlighting its operational strengths and brand assets, internal weaknesses and financial constraints, market opportunities for expansion and innovation, and external threats from competition, regulatory pressures, and cyclical consumer demand.

Provides a concise Ardent Leisure SWOT snapshot for rapid strategic alignment and clear stakeholder communication.

Weaknesses

Geographic Revenue Concentration

Ardent Leisure depends heavily on the Gold Coast, where its theme parks and attractions drove about 62% of group revenue in FY2024, exposing the company to regional shocks.

This geographic concentration means Queensland-specific events—like the 2023 east-coast floods or a transport strike—can cut visitation and revenue sharply; a 10% drop in Gold Coast tourist arrivals in 2023 reduced local tourism receipts by ~A$250m.

High Operational Fixed Costs

Theme park operations carry high fixed costs—labor, maintenance, utilities, and safety inspections—that persist regardless of attendance; Ardent Leisure reported about A$420m in operating expenses in FY2024, keeping leverage high.

High operating leverage means a small drop in visitors sharply cuts margins; a 5% attendance decline can reduce EBITDA by ~10–15% given cost structure and past seasonality patterns.

Managing off-peak expense loadings—staff rostering, maintenance timing, and energy use—remains a constant executive challenge for cashflow stability.

Sensitivity to Discretionary Income

Historical Brand Scars

Despite major remediation and a 2020 governance overhaul, Ardent Leisure’s past safety incidents—most notably the 2016 Dreamworld accident—still surface in media cycles, denting trust and pressuring PR spend.

Management reported A$10–15m annual brand and safety-related costs in FY2024, and surveys show brand favorability remains ~20% below pre-2016 levels, so minor hiccups get amplified.

The company must sustain costly proactive communications and crisis preparedness to prevent revenue hits at theme parks and leisure venues.

- Legacy incident: Dreamworld 2016

- FY2024 brand/safety costs A$10–15m

- Brand favorability ~20% below 2015

- Small incidents → amplified media risk

Limited Diversification Post-Main Event

- Removed US$835m asset (Main Event sale)

- FY2024 revenue ~A$640m concentrated in Australia

- EBITDA margin swing 6.2ppt seasonality

High Gold Coast exposure, heavy fixed costs and brand drag amplify EBITDA volatility

Heavy Gold Coast concentration (~62% group revenue FY2024), high fixed costs (A$420m operating expenses FY2024) and operating leverage (5% attendance drop → ~10–15% EBITDA fall) raise cashflow volatility; brand drag from Dreamworld 2016 keeps favorability ~20% below 2015 and costs A$10–15m p.a.; Main Event sale (US$835m, 2021) left FY2024 revenue ~A$640m Australia‑centric, worsening seasonality (EBITDA swing 6.2ppt).

| Metric | Value |

|---|---|

| Gold Coast revenue share | ~62% (FY2024) |

| Operating expenses | A$420m (FY2024) |

| Attendance sensitivity | 5% ↓ → 10–15% EBITDA ↓ |

| Brand costs | A$10–15m p.a. (FY2024) |

| Brand favourability gap | ~20% below 2015 |

| Main Event sale | US$835m (Nov 2021) |

| FY2024 revenue | ~A$640m (Australia) |

| Seasonality swing | EBITDA −6.2ppt (wet season) |

Full Version Awaits

Ardent Leisure SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.