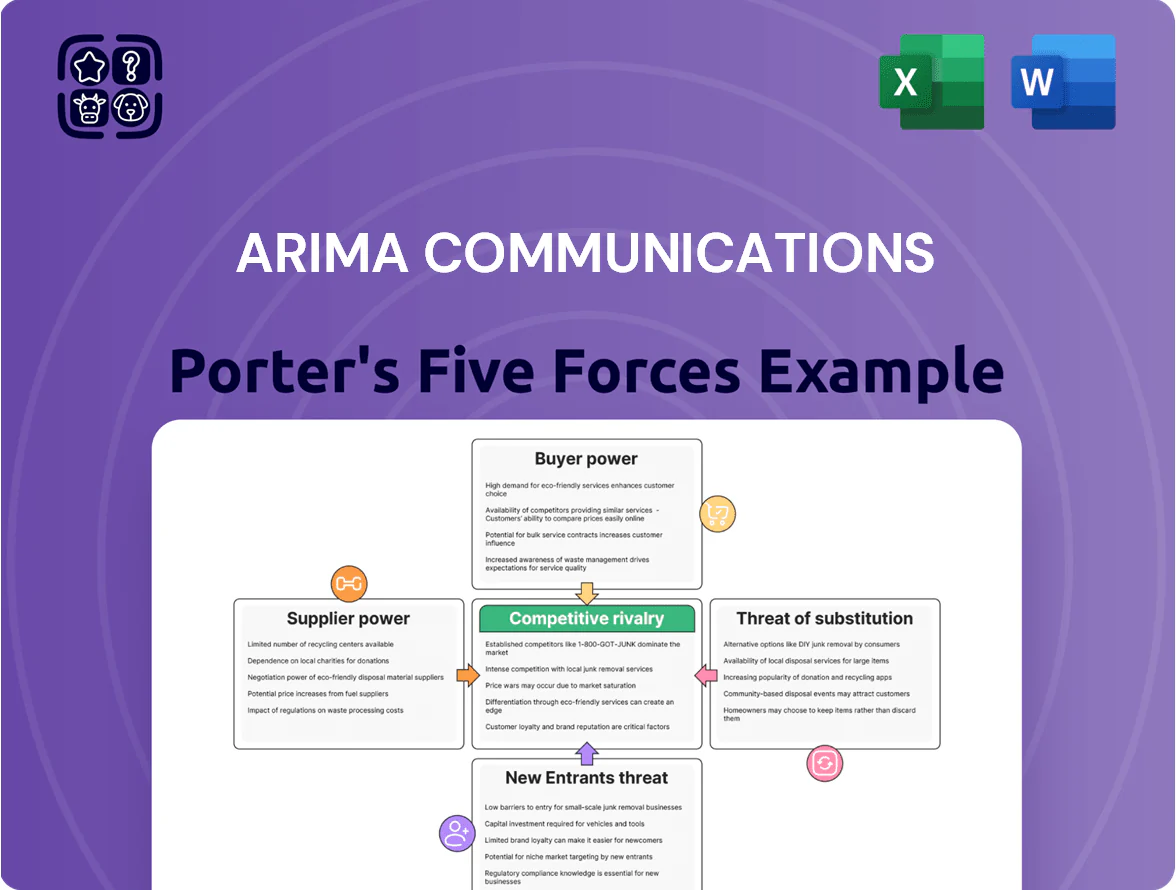

Arima Communications Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

Arima Communications faces moderate rivalry and shifting buyer preferences, while supplier leverage and potential substitutes create selective pressure on margins; regulatory shifts and tech disruption add uncertainty to growth prospects.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Arima Communications’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of semiconductor vendors

The primary components for Arima Communications’ wireless products—specialized chipsets—come from a handful of global semiconductor giants: Qualcomm, MediaTek, and Broadcom together held about 70% of mobile baseband and RF IC market share in 2024, giving them pricing power. Arima depends on these providers for high-performance processors and modems to keep devices competitive, so a single supplier delay can stall product launches. These vendors control key patents and 2024 average gross margins above 40%, enabling leverage over pricing and lead times.

Critical component scarcity

The manufacturing of wireless modules depends on high-grade semiconductors and passives that faced cyclical shortages; global chip lead times averaged 22 weeks in Q3 2025, straining supply.

Automotive and industrial IoT demand stayed strong in late 2025, with automotive semiconductor revenues up 9% year-over-year, letting suppliers prioritize larger clients.

Arima must secure long-term contracts, multi-sourcing, and forecast accuracy to avoid production delays seen across the electronics ecosystem.

Specialized technical requirements

Suppliers of specialized antennas and RF components hold strong leverage because their modules are often proprietary and non-interchangeable, so Arima faces switching costs that can exceed millions in reengineering and 6–12 months of development time.

That technical lock-in ties Arima to supplier roadmaps and pricing: in 2024 niche RF vendor markups averaged 15–30%, and single-source parts can represent >25% of BOM value, boosting supplier bargaining power.

Impact of raw material costs

Volatility in rare earth and precious metal prices — rare earth oxide up ~40% and palladium up ~18% in 2024 — raises Arima Communications’ unit costs for high-frequency circuit boards, squeezing margins.

Suppliers pass hikes down the chain; Arima cannot meaningfully negotiate global commodity prices, so it must absorb costs or lose price-sensitive contracts.

- Rare earth oxide +40% (2024)

- Palladium +18% (2024)

- Weak negotiating power vs global suppliers

- Trade-off: absorb margin vs lose contracts

Limited vertical integration

Arima lacks in-house semiconductor fabs and buys all core processing units externally, making it a price taker for roughly 35–45% of BOM cost tied to chips (industry 2024 average for comms devices).

This limited vertical integration gives suppliers stronger leverage: lead partners control roadmap timing, and Arima’s product margins face pressure when foundry-led node shifts raise chip prices 10–25% (2023–24 wafer price moves).

What this hides: if supplier lead times exceed 12 weeks, Arima risks delayed shipments and higher procurement premiums.

- All core CPUs bought externally

- Chips ≈35–45% of BOM (2024 industry data)

- Foundry-driven price swings +10–25% (2023–24)

- Lead-time >12 weeks raises costs

Supply squeeze: chip concentration, commodity spikes and 6–12mo RF switching hit Arima margins

Suppliers (Qualcomm, MediaTek, Broadcom) held ~70% mobile RF/baseband share in 2024, making Arima a price taker for chips (~35–45% of BOM) and subject to foundry-driven price swings of +10–25% (2023–24). Niche RF/antenna vendors add switching costs of 6–12 months and markups of 15–30%; rare earth +40% and palladium +18% in 2024 squeeze margins—long lead times (>12 weeks) raise premiums.

| Metric | Value |

|---|---|

| Chip market concentration (2024) | ~70% |

| Chips share of BOM | 35–45% |

| Foundry price swing (2023–24) | +10–25% |

| Rare earth / palladium (2024) | +40% / +18% |

| RF vendor markups | 15–30% |

| Switching time/cost | 6–12 months / $MM+ |

What is included in the product

Tailored Porter’s Five Forces analysis for Arima Communications that uncovers competitive drivers, customer and supplier power, entry barriers, substitutes, and emerging threats to inform strategic positioning and investor materials.

A concise, one-sheet Porter's Five Forces summary for Arima Communications—quickly assess competitive pressure and make faster strategic decisions.

Customers Bargaining Power

Concentration of large scale clients

Around 62% of Arima Communications’ 2024 revenue came from five large industrial and consumer-electronics clients, who push for lower unit prices and extended net-90 to net-120 payment terms, squeezing gross margins by an estimated 150–250 basis points; losing any one contract could cut annual revenue by ~12–20% and reduce factory utilization from 88% to near 70%, raising fixed-cost per-unit and cash-flow stress.

Low switching costs for standard modules

In standardized wireless modules, buyers switch easily—over 60% of OEMs surveyed in 2024 considered alternative suppliers within 6 months—so technical parity makes price the main tie-breaker.

Because modules are treated as commodities, Arima must match market price declines (module ASPs fell ~12% YoY in 2024) and offer faster lead times and support to keep customers.

Threat of backward integration

High price sensitivity in consumer markets

- End-user price sensitivity → tougher buyer demands

- 2025 OEM focus: 5–10% COGS cuts

- Arima needs process innovation, automation

- Margin risk: potential drop below mid-20s%

Access to transparent market information

Concentrated Buyers, Falling ASPs: Arima Must Cut Costs or Face Margin Collapse

Buyers hold high leverage: five clients drove 62% of 2024 revenue, can demand net-90/120 terms and trim prices, risking 12–20% revenue loss per contract; OEMs switch suppliers within 6 months (60%+ in 2024) and module ASPs fell ~12% YoY, while OEMs target 5–10% COGS cuts in 2025—Arima must cut costs or see mid-20s% gross margins slip lower.

| Metric | 2024–2025 |

|---|---|

| Revenue concentration | 62% from 5 clients (2024) |

| Loss impact | −12–20% revenue per lost client |

| Buyer switch rate | 60%+ OEMs considered alternatives (6 mo, 2024) |

| ASP change | −12% YoY (2024) |

| OEM COGS target | 5–10% YoY cuts (2025) |

Preview the Actual Deliverable

Arima Communications Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Arima Communications you'll receive after purchase—no placeholders, no samples, just the finished file.

The document displayed is fully formatted and ready for download the moment you buy, containing the same detailed competitor, supplier, buyer, entrant, and substitute assessments shown here.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Arima Communications faces moderate rivalry and shifting buyer preferences, while supplier leverage and potential substitutes create selective pressure on margins; regulatory shifts and tech disruption add uncertainty to growth prospects.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Arima Communications’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of semiconductor vendors

The primary components for Arima Communications’ wireless products—specialized chipsets—come from a handful of global semiconductor giants: Qualcomm, MediaTek, and Broadcom together held about 70% of mobile baseband and RF IC market share in 2024, giving them pricing power. Arima depends on these providers for high-performance processors and modems to keep devices competitive, so a single supplier delay can stall product launches. These vendors control key patents and 2024 average gross margins above 40%, enabling leverage over pricing and lead times.

Critical component scarcity

The manufacturing of wireless modules depends on high-grade semiconductors and passives that faced cyclical shortages; global chip lead times averaged 22 weeks in Q3 2025, straining supply.

Automotive and industrial IoT demand stayed strong in late 2025, with automotive semiconductor revenues up 9% year-over-year, letting suppliers prioritize larger clients.

Arima must secure long-term contracts, multi-sourcing, and forecast accuracy to avoid production delays seen across the electronics ecosystem.

Specialized technical requirements

Suppliers of specialized antennas and RF components hold strong leverage because their modules are often proprietary and non-interchangeable, so Arima faces switching costs that can exceed millions in reengineering and 6–12 months of development time.

That technical lock-in ties Arima to supplier roadmaps and pricing: in 2024 niche RF vendor markups averaged 15–30%, and single-source parts can represent >25% of BOM value, boosting supplier bargaining power.

Impact of raw material costs

Volatility in rare earth and precious metal prices — rare earth oxide up ~40% and palladium up ~18% in 2024 — raises Arima Communications’ unit costs for high-frequency circuit boards, squeezing margins.

Suppliers pass hikes down the chain; Arima cannot meaningfully negotiate global commodity prices, so it must absorb costs or lose price-sensitive contracts.

- Rare earth oxide +40% (2024)

- Palladium +18% (2024)

- Weak negotiating power vs global suppliers

- Trade-off: absorb margin vs lose contracts

Limited vertical integration

Arima lacks in-house semiconductor fabs and buys all core processing units externally, making it a price taker for roughly 35–45% of BOM cost tied to chips (industry 2024 average for comms devices).

This limited vertical integration gives suppliers stronger leverage: lead partners control roadmap timing, and Arima’s product margins face pressure when foundry-led node shifts raise chip prices 10–25% (2023–24 wafer price moves).

What this hides: if supplier lead times exceed 12 weeks, Arima risks delayed shipments and higher procurement premiums.

- All core CPUs bought externally

- Chips ≈35–45% of BOM (2024 industry data)

- Foundry-driven price swings +10–25% (2023–24)

- Lead-time >12 weeks raises costs

Supply squeeze: chip concentration, commodity spikes and 6–12mo RF switching hit Arima margins

Suppliers (Qualcomm, MediaTek, Broadcom) held ~70% mobile RF/baseband share in 2024, making Arima a price taker for chips (~35–45% of BOM) and subject to foundry-driven price swings of +10–25% (2023–24). Niche RF/antenna vendors add switching costs of 6–12 months and markups of 15–30%; rare earth +40% and palladium +18% in 2024 squeeze margins—long lead times (>12 weeks) raise premiums.

| Metric | Value |

|---|---|

| Chip market concentration (2024) | ~70% |

| Chips share of BOM | 35–45% |

| Foundry price swing (2023–24) | +10–25% |

| Rare earth / palladium (2024) | +40% / +18% |

| RF vendor markups | 15–30% |

| Switching time/cost | 6–12 months / $MM+ |

What is included in the product

Tailored Porter’s Five Forces analysis for Arima Communications that uncovers competitive drivers, customer and supplier power, entry barriers, substitutes, and emerging threats to inform strategic positioning and investor materials.

A concise, one-sheet Porter's Five Forces summary for Arima Communications—quickly assess competitive pressure and make faster strategic decisions.

Customers Bargaining Power

Concentration of large scale clients

Around 62% of Arima Communications’ 2024 revenue came from five large industrial and consumer-electronics clients, who push for lower unit prices and extended net-90 to net-120 payment terms, squeezing gross margins by an estimated 150–250 basis points; losing any one contract could cut annual revenue by ~12–20% and reduce factory utilization from 88% to near 70%, raising fixed-cost per-unit and cash-flow stress.

Low switching costs for standard modules

In standardized wireless modules, buyers switch easily—over 60% of OEMs surveyed in 2024 considered alternative suppliers within 6 months—so technical parity makes price the main tie-breaker.

Because modules are treated as commodities, Arima must match market price declines (module ASPs fell ~12% YoY in 2024) and offer faster lead times and support to keep customers.

Threat of backward integration

High price sensitivity in consumer markets

- End-user price sensitivity → tougher buyer demands

- 2025 OEM focus: 5–10% COGS cuts

- Arima needs process innovation, automation

- Margin risk: potential drop below mid-20s%

Access to transparent market information

Concentrated Buyers, Falling ASPs: Arima Must Cut Costs or Face Margin Collapse

Buyers hold high leverage: five clients drove 62% of 2024 revenue, can demand net-90/120 terms and trim prices, risking 12–20% revenue loss per contract; OEMs switch suppliers within 6 months (60%+ in 2024) and module ASPs fell ~12% YoY, while OEMs target 5–10% COGS cuts in 2025—Arima must cut costs or see mid-20s% gross margins slip lower.

| Metric | 2024–2025 |

|---|---|

| Revenue concentration | 62% from 5 clients (2024) |

| Loss impact | −12–20% revenue per lost client |

| Buyer switch rate | 60%+ OEMs considered alternatives (6 mo, 2024) |

| ASP change | −12% YoY (2024) |

| OEM COGS target | 5–10% YoY cuts (2025) |

Preview the Actual Deliverable

Arima Communications Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Arima Communications you'll receive after purchase—no placeholders, no samples, just the finished file.

The document displayed is fully formatted and ready for download the moment you buy, containing the same detailed competitor, supplier, buyer, entrant, and substitute assessments shown here.