Arion bank Business Model Canvas

Arion Bank Blueprint: Business Model Canvas of Iceland’s Competitive Strategy

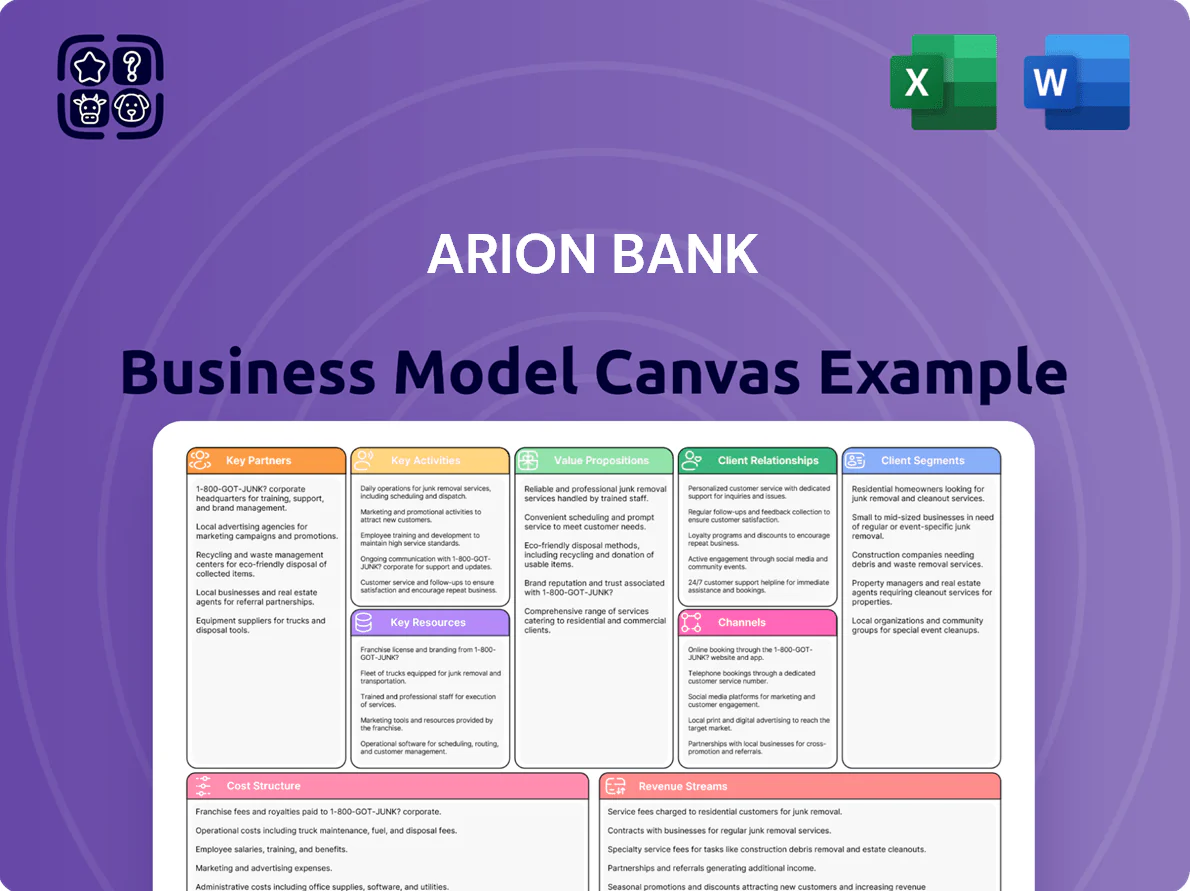

Unlock the full strategic blueprint behind Arion bank’s business model—this concise Business Model Canvas maps customer segments, core value propositions, revenue streams, and key partnerships to show how the bank competes and scales in Iceland’s financial market.

Partnerships

Strategic Insurance Alliance with Vörður

Arion Bank’s strategic bancassurance alliance with Vörður integrates insurance into retail and SME offerings, supplying home, auto, and life coverage at point-of-sale and via digital channels; in 2024 this channel accounted for roughly 12% of Vörður’s gross written premiums in Iceland (≈ISK 3.6bn). By bundling protection with loans and deposits, Arion boosts retention and cross-sell—mortgage-linked insurance lifts product-per-customer by ~0.3 products and reduces churn by an estimated 15%.

Fintech and Technology Providers

Collaboration with global and Icelandic fintechs keeps Arion Bank's digital edge—partnering with firms like Meniga and European cloud providers helped cut payment latency 30% in 2024 and supported a 22% rise in mobile active users to ~180,000. These deals speed integration of payments, analytics, and zero-trust cybersecurity, helping Arion compete with neobanks and sustain a 2024 digital revenue growth of ~18%.

International Correspondent Banking Networks

As a leading Icelandic bank, Arion Bank depends on correspondent relationships with global banks (eg, BNP Paribas, Barclays) to settle cross-border payments and FX; in 2024 these networks supported roughly €4.2bn in outbound payments, supplying short-term liquidity and major currency rails. These alliances give Arion’s corporate clients access to global markets and FX pools, keeping Iceland’s trade flows connected and enabling the bank to act as the primary gateway between the Icelandic economy and international finance.

Government and Regulatory Institutions

- Regular reporting to FME and Central Bank

- CET1 ~18% (2024)

- LCR ~150% (2024)

- Active role in national initiatives

Institutional Pension Fund Collaborations

Arion partners regularly with large Icelandic pension funds—notably Gildi and Lífeyrissjóður verzlunarmanna—for co-investments and project financing, tapping roughly ISK 150–300bn of long-term capital committed to infrastructure and energy since 2020.

This funding complements Arion’s balance sheet, enabling multi‑hundred‑million‑euro domestic developments that bolster Iceland’s economy and de‑risk large projects through shared equity.

- Co-investment range: ISK 150–300bn (2020–2025)

- Typical project size: €50–300m

- Key sectors: energy, infrastructure, renewables

- Benefit: lowers funding cost, extends maturities

Arion’s strategic partners fuel distribution, tech, liquidity and long-term capital

Arion’s key partners—Vörður (bancassurance ~ISK 3.6bn premiums, 2024), Meniga and EU cloud providers (30% lower payment latency; mobile users ~180,000, 2024), BNP Paribas/Barclays (≈€4.2bn outbound payments, 2024), Central Bank/FME (CET1 ~18%, LCR ~150%, 2024), and pension funds (co‑invest ISK 150–300bn, 2020–2025)—support distribution, tech, liquidity, compliance, and long-term funding.

| Partner | Role | Key metric (2024) |

|---|---|---|

| Vörður | Bancassurance | ISK 3.6bn premiums |

| Meniga/Cloud | Digital/Payments | -30% latency; 180k users |

| BNP/Barclays | Correspondent banks | €4.2bn outbound |

| Central Bank/FME | Regulation | CET1 18%; LCR 150% |

| Pension funds | Co-invest | ISK 150–300bn |

What is included in the product

A concise Business Model Canvas for Arion Bank detailing customer segments, channels, value propositions, revenue streams, key resources, partners, activities, cost structure, and customer relationships, reflecting real-world operations and strategic priorities to support investor presentations and strategic planning.

High-level view of Arion Bank’s business model with editable cells to quickly pinpoint how products, channels, and partnerships relieve customer pain points and streamline internal strategy.

Activities

Credit Origination and Loan Management

The bank assesses, grants, and monitors mortgages, corporate revolvers, and project finance focused on Icelandic energy and infrastructure; in 2024 Arion held ~820 billion ISK in loans, with mortgages ~48% and corporate lending ~39%. Effective credit controls target a loan-to-value ratio near 65% and reduced NPLs—Arion reported a 0.9% non-performing loan ratio at Q4 2024.

Digital Product Development and UX Design

Arion Bank invests heavily in continuous refinement of its mobile app and online banking to meet 2025 digital standards, spending ~ISK 4.2bn (2024 capex + R&D) and running 120+ engineers and designers focused on software engineering and user-experience research.

They deploy automated financial management tools (personal finance, savings nudges, robo-advice) that cut branch visits ~30% and aim to lift digital transactions to 92% of volumes, reducing operating costs per customer by an estimated 18%.

Asset and Wealth Management Services

Arion Bank, via its asset management subsidiaries, manages diversified portfolios for retail, private and institutional clients, overseeing ISK 260bn (≈USD 2.0bn) in AUM as of Q4 2025 and running multiple mutual and pension funds; activities include market research, strategic asset allocation and active fund management to target superior risk-adjusted returns aligned to client goals.

Corporate Advisory and Capital Markets

Arion Bank’s investment banking team leads mergers, acquisitions and IPO advisory in Iceland, facilitating capital raises and restructurings—transactions totaled ~ISK 45bn in 2024, with 12+ mandates across energy, fisheries and tech.

- Expert advisory on M&A and IPOs

- Raised ~ISK 45bn (2024)

- 12+ domestic mandates in 2024

- Deep Icelandic industry network

Risk Management and Regulatory Compliance

Continuous monitoring of market, credit, and operational risks—including quarterly stress tests and daily AML (anti-money laundering) screening—sustains Arion Bank’s solvency and license; as of 2024 the Icelandic banking sector CET1 ratio averaged ~21%, so adherence to Basel III and EBA rules keeps Arion’s capital buffers aligned with regulators.

Robust frameworks protect capital and trust via regular portfolio stress scenarios, AML transaction monitoring, and compliance reporting to the Financial Supervisory Authority (FME), reducing regulatory breach risk and preserving funding access.

- Quarterly stress tests

- Daily AML checks

- Basel III CET1 target ~>15%

- Reporting to FME

- Operational risk loss tracking

Arion: ISK 820bn loan book, ISK 260bn AUM, digital-first bank with >15% CET1

Arion originates and services mortgages and corporate loans (ISK ~820bn in 2024; mortgages 48%, corporate 39%), runs digital banking (ISK 4.2bn capex/R&D, 120+ engineers), manages ISK 260bn AUM, and provides M&A/IPO advisory (ISK ~45bn raised in 2024), while enforcing daily AML, quarterly stress tests and CET1 buffers ~>15%.

| Metric | Value |

|---|---|

| Total loans (2024) | ISK 820bn |

| Mortgages | 48% |

| Corporate loans | 39% |

| Digital spend (2024) | ISK 4.2bn |

| Engineers/designers | 120+ |

| AUM (Q4 2025) | ISK 260bn |

| M&A/IPO raises (2024) | ISK 45bn |

| NPL ratio (Q4 2024) | 0.9% |

| CET1 target | >15% |

Full Document Unlocks After Purchase

Business Model Canvas

The document you’re previewing is the exact Arion Bank Business Model Canvas you’ll receive after purchase — not a mockup or sample — and upon ordering you’ll get this same fully editable file ready for use in Word and Excel.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Arion Bank Blueprint: Business Model Canvas of Iceland’s Competitive Strategy

Unlock the full strategic blueprint behind Arion bank’s business model—this concise Business Model Canvas maps customer segments, core value propositions, revenue streams, and key partnerships to show how the bank competes and scales in Iceland’s financial market.

Partnerships

Strategic Insurance Alliance with Vörður

Arion Bank’s strategic bancassurance alliance with Vörður integrates insurance into retail and SME offerings, supplying home, auto, and life coverage at point-of-sale and via digital channels; in 2024 this channel accounted for roughly 12% of Vörður’s gross written premiums in Iceland (≈ISK 3.6bn). By bundling protection with loans and deposits, Arion boosts retention and cross-sell—mortgage-linked insurance lifts product-per-customer by ~0.3 products and reduces churn by an estimated 15%.

Fintech and Technology Providers

Collaboration with global and Icelandic fintechs keeps Arion Bank's digital edge—partnering with firms like Meniga and European cloud providers helped cut payment latency 30% in 2024 and supported a 22% rise in mobile active users to ~180,000. These deals speed integration of payments, analytics, and zero-trust cybersecurity, helping Arion compete with neobanks and sustain a 2024 digital revenue growth of ~18%.

International Correspondent Banking Networks

As a leading Icelandic bank, Arion Bank depends on correspondent relationships with global banks (eg, BNP Paribas, Barclays) to settle cross-border payments and FX; in 2024 these networks supported roughly €4.2bn in outbound payments, supplying short-term liquidity and major currency rails. These alliances give Arion’s corporate clients access to global markets and FX pools, keeping Iceland’s trade flows connected and enabling the bank to act as the primary gateway between the Icelandic economy and international finance.

Government and Regulatory Institutions

- Regular reporting to FME and Central Bank

- CET1 ~18% (2024)

- LCR ~150% (2024)

- Active role in national initiatives

Institutional Pension Fund Collaborations

Arion partners regularly with large Icelandic pension funds—notably Gildi and Lífeyrissjóður verzlunarmanna—for co-investments and project financing, tapping roughly ISK 150–300bn of long-term capital committed to infrastructure and energy since 2020.

This funding complements Arion’s balance sheet, enabling multi‑hundred‑million‑euro domestic developments that bolster Iceland’s economy and de‑risk large projects through shared equity.

- Co-investment range: ISK 150–300bn (2020–2025)

- Typical project size: €50–300m

- Key sectors: energy, infrastructure, renewables

- Benefit: lowers funding cost, extends maturities

Arion’s strategic partners fuel distribution, tech, liquidity and long-term capital

Arion’s key partners—Vörður (bancassurance ~ISK 3.6bn premiums, 2024), Meniga and EU cloud providers (30% lower payment latency; mobile users ~180,000, 2024), BNP Paribas/Barclays (≈€4.2bn outbound payments, 2024), Central Bank/FME (CET1 ~18%, LCR ~150%, 2024), and pension funds (co‑invest ISK 150–300bn, 2020–2025)—support distribution, tech, liquidity, compliance, and long-term funding.

| Partner | Role | Key metric (2024) |

|---|---|---|

| Vörður | Bancassurance | ISK 3.6bn premiums |

| Meniga/Cloud | Digital/Payments | -30% latency; 180k users |

| BNP/Barclays | Correspondent banks | €4.2bn outbound |

| Central Bank/FME | Regulation | CET1 18%; LCR 150% |

| Pension funds | Co-invest | ISK 150–300bn |

What is included in the product

A concise Business Model Canvas for Arion Bank detailing customer segments, channels, value propositions, revenue streams, key resources, partners, activities, cost structure, and customer relationships, reflecting real-world operations and strategic priorities to support investor presentations and strategic planning.

High-level view of Arion Bank’s business model with editable cells to quickly pinpoint how products, channels, and partnerships relieve customer pain points and streamline internal strategy.

Activities

Credit Origination and Loan Management

The bank assesses, grants, and monitors mortgages, corporate revolvers, and project finance focused on Icelandic energy and infrastructure; in 2024 Arion held ~820 billion ISK in loans, with mortgages ~48% and corporate lending ~39%. Effective credit controls target a loan-to-value ratio near 65% and reduced NPLs—Arion reported a 0.9% non-performing loan ratio at Q4 2024.

Digital Product Development and UX Design

Arion Bank invests heavily in continuous refinement of its mobile app and online banking to meet 2025 digital standards, spending ~ISK 4.2bn (2024 capex + R&D) and running 120+ engineers and designers focused on software engineering and user-experience research.

They deploy automated financial management tools (personal finance, savings nudges, robo-advice) that cut branch visits ~30% and aim to lift digital transactions to 92% of volumes, reducing operating costs per customer by an estimated 18%.

Asset and Wealth Management Services

Arion Bank, via its asset management subsidiaries, manages diversified portfolios for retail, private and institutional clients, overseeing ISK 260bn (≈USD 2.0bn) in AUM as of Q4 2025 and running multiple mutual and pension funds; activities include market research, strategic asset allocation and active fund management to target superior risk-adjusted returns aligned to client goals.

Corporate Advisory and Capital Markets

Arion Bank’s investment banking team leads mergers, acquisitions and IPO advisory in Iceland, facilitating capital raises and restructurings—transactions totaled ~ISK 45bn in 2024, with 12+ mandates across energy, fisheries and tech.

- Expert advisory on M&A and IPOs

- Raised ~ISK 45bn (2024)

- 12+ domestic mandates in 2024

- Deep Icelandic industry network

Risk Management and Regulatory Compliance

Continuous monitoring of market, credit, and operational risks—including quarterly stress tests and daily AML (anti-money laundering) screening—sustains Arion Bank’s solvency and license; as of 2024 the Icelandic banking sector CET1 ratio averaged ~21%, so adherence to Basel III and EBA rules keeps Arion’s capital buffers aligned with regulators.

Robust frameworks protect capital and trust via regular portfolio stress scenarios, AML transaction monitoring, and compliance reporting to the Financial Supervisory Authority (FME), reducing regulatory breach risk and preserving funding access.

- Quarterly stress tests

- Daily AML checks

- Basel III CET1 target ~>15%

- Reporting to FME

- Operational risk loss tracking

Arion: ISK 820bn loan book, ISK 260bn AUM, digital-first bank with >15% CET1

Arion originates and services mortgages and corporate loans (ISK ~820bn in 2024; mortgages 48%, corporate 39%), runs digital banking (ISK 4.2bn capex/R&D, 120+ engineers), manages ISK 260bn AUM, and provides M&A/IPO advisory (ISK ~45bn raised in 2024), while enforcing daily AML, quarterly stress tests and CET1 buffers ~>15%.

| Metric | Value |

|---|---|

| Total loans (2024) | ISK 820bn |

| Mortgages | 48% |

| Corporate loans | 39% |

| Digital spend (2024) | ISK 4.2bn |

| Engineers/designers | 120+ |

| AUM (Q4 2025) | ISK 260bn |

| M&A/IPO raises (2024) | ISK 45bn |

| NPL ratio (Q4 2024) | 0.9% |

| CET1 target | >15% |

Full Document Unlocks After Purchase

Business Model Canvas

The document you’re previewing is the exact Arion Bank Business Model Canvas you’ll receive after purchase — not a mockup or sample — and upon ordering you’ll get this same fully editable file ready for use in Word and Excel.