Arion bank Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

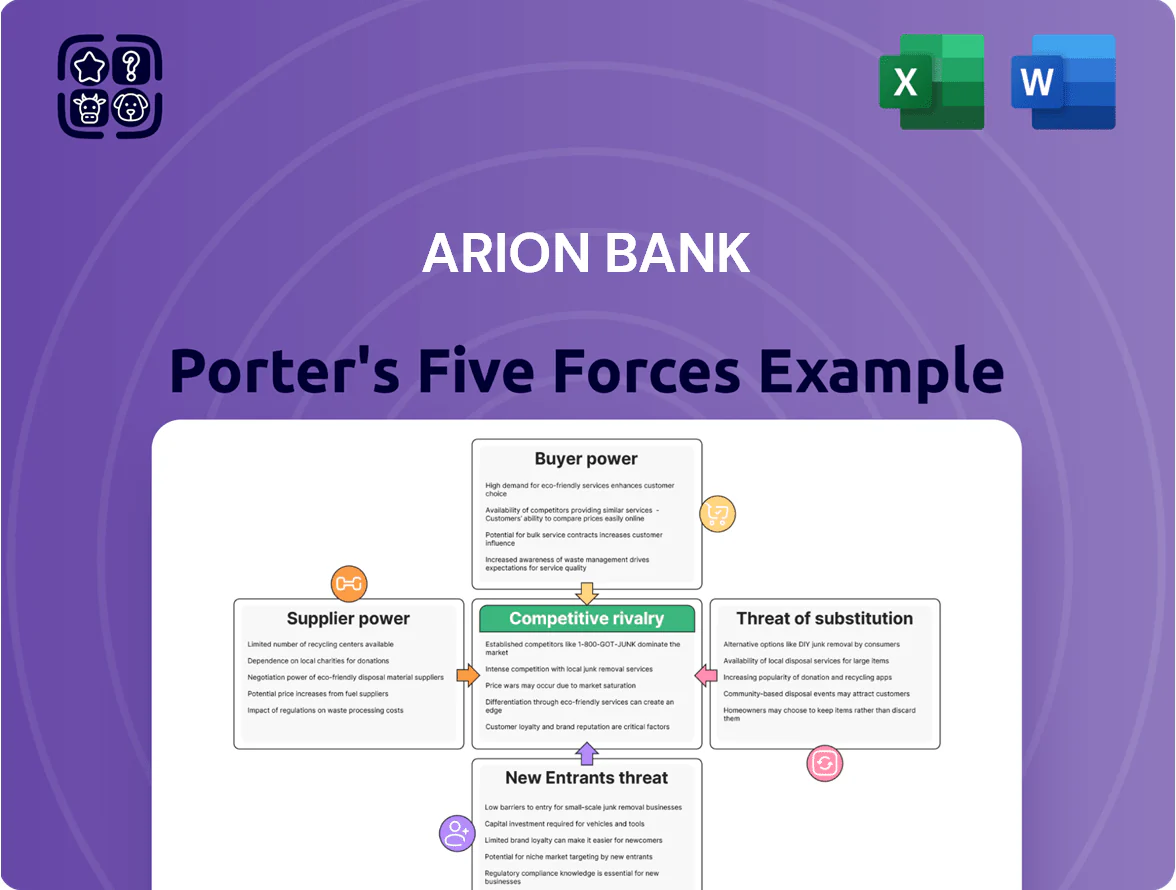

Arion bank faces moderate rivalry and regulatory scrutiny, with digital incumbents and local customer loyalty shaping competitive dynamics; supplier and buyer power are balanced, while barriers to entry remain medium due to regulatory costs and fintech disruption. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Arion bank’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Funding Sources and Depositors

The primary suppliers of capital for Arion Bank are retail and corporate depositors who fund lending; retail deposits made up about 56% of liabilities and corporate deposits 22% of liabilities as of Q3 2025, per the bank’s report.

Large depositors can shift funds quickly to Íslandsbanki or Landsbankinn if rates lag, giving them leverage; Arion’s LCR (liquidity coverage ratio) was 165% in Sep 2025, so the Central Bank closely watches outflows.

Reliance on Global Technology and Infrastructure Providers

Arion Bank relies on third-party core-banking, cloud, and cybersecurity vendors—notably Microsoft and AWS—creating high supplier power because switching costs and integration time exceed 12–24 months and can cost €5–20m.

In 2024 cloud spend categories rose ~18% industrywide; a 10% price rise from major providers would lift Arion’s IT opex materially and slow digital initiatives.

Availability of Specialized Financial Talent

Iceland’s labor pool has about 370,000 workers (2024), so specialists in data science, compliance, and fintech are scarce; Arion Bank competes with Íslandsbanki, Landsbankinn, and remote roles paying 15–30% premium for tech talent.

Access to International Wholesale Funding Markets

Arion Bank taps international wholesale markets for large projects, issuing green bonds and debt; in 2024 it issued EUR 300m equivalent in green bonds, supporting capital adequacy and lending capacity.

Funding terms hinge on global credit ratings and investor sentiment toward Iceland; Arion’s BBB+ (S&P-equivalent) keeps access broad, but a 100bp rise in global risk premia would raise borrowing costs materially.

A sudden dip in risk appetite could shrink tenor and increase spreads, forcing shorter maturities or higher coupon issuance and pressuring regulatory capital ratios.

- 2024 green bond issuance ~EUR 300m

- Rating: BBB+ (S&P-equivalent)

- 100bp risk-premium shock → higher funding cost

- Investor sentiment tied to Iceland macro (GDP, tourism)

Regulatory Influence of the Central Bank of Iceland

The Central Bank of Iceland supplies systemic stability and liquidity; its policy rate (7.25% in Dec 2025) and countercyclical capital buffer (2.5% since 2023) directly set Arion Bank’s funding cost and capital requirements, leaving the bank little room to negotiate these terms.

The regulator’s mandates thus act as a dominant upstream force shaping margins, credit supply and balance-sheet strategy for Arion Bank.

- Policy rate 7.25% (Dec 2025)

- Countercyclical buffer 2.5% (since 2023)

- Reserve/liquidity rules set funding floor

Strong liquidity (LCR165%) and deposit base, but margins squeezed by tech costs & rates

Suppliers of funds and services exert medium-high power: retail deposits 56% and corporate 22% of liabilities (Q3 2025), LCR 165% (Sep 2025), BBB+ rating, EUR 300m green bonds (2024), policy rate 7.25% and countercyclical buffer 2.5% (Dec 2025); cloud/vendor switching costs 12–24 months (€5–20m) and tech wage premiums 15–30% tighten margins.

| Metric | Value |

|---|---|

| Retail deposits | 56% |

| Corporate deposits | 22% |

| LCR | 165% (Sep 2025) |

| Rating | BBB+ |

| Green bonds | EUR 300m (2024) |

| Policy rate | 7.25% (Dec 2025) |

What is included in the product

Tailored Porter's Five Forces analysis for Arion bank that uncovers competitive intensity, customer and supplier bargaining power, entry barriers, substitute threats, and emerging disruptors, with strategic commentary to inform pricing, profitability, and defensive positioning.

Concise Porter's Five Forces snapshot for Arion Bank—clear, one-sheet insights to speed strategic decisions and boardroom discussions.

Customers Bargaining Power

Low Switching Costs for Retail Banking Clients

In 2025 Icelandic retail clients face very low switching costs thanks to standardized electronic IDs (e-ID) and account portability between the big three banks, so Arion Bank must match market rates—household deposit rates averaged 1.2% in 2024—to avoid outflows. The bank needs top-tier mobile features; 88% of Icelandic adults used mobile banking in 2024, boosting churn risk if apps lag. Real-time fee transparency lets customers compare prices instantly, increasing their bargaining power.

Leverage of Large Corporate and Institutional Clients

Corporate and institutional clients account for roughly 45% of Arion Bank’s loan book and 52% of assets under management as of Dec 2025, giving them strong bargaining power.

They demand bespoke deals, lower margins, and advisory packages; Arion often concedes rates or fees to protect high-volume revenue.

If a major client shifts to rival Landsbankinn, Arion may cut spreads or add services to retain business, squeezing profitability.

Consumer Awareness and Demand for Sustainable Finance

By end-2025 Icelandic consumers show high ESG sensitivity: 62% prioritize green products and 48% would switch banks for sustainable options (Capacent/Maskína 2024–25 surveys). Demand for green mortgages and ethical funds forces Arion Bank to expand ESG offerings or risk reputational harm and market-share loss to greener rivals; missed targets could cut retail deposits and new mortgage origination by mid-single digits.

Influence of Pension Funds on the Mortgage Market

Icelandic pension funds (largest: the four universal funds and large occupational funds) held about ISK 4,200bn in assets at end-2024 and offered mortgage rates ~0.25–0.75 percentage points below bank averages, creating a strong non-bank alternative that forces Arion Bank to keep mortgage pricing competitive.

Their market moves boost buyer bargaining power: in 2024 pension-funded mortgages accounted for ~15–20% of new mortgage originations, so Arion must match rates or risk margin erosion.

- Pension funds’ assets: ~ISK 4,200bn (end-2024)

- Rate gap vs banks: ~0.25–0.75 pp (2024)

- Share of new mortgages: ~15–20% (2024)

- Effect: raises buyer bargaining power, compresses Arion margins

Digital Transparency and Price Comparison Tools

High customer leverage: mobile-first switching, corporate loans & pension mortgage pressure

Customers hold high bargaining power: retail switching is easy due to e-ID and portability, with household deposit rates 1.2% in 2024 and mobile banking use 88% (2024). Corporates drive ~45% of loan book and 52% AUM (Dec 2025), forcing bespoke pricing. Pension funds held ~ISK 4,200bn (end‑2024) and offered mortgages 0.25–0.75pp cheaper, taking 15–20% of new originations (2024).

| Metric | Value |

|---|---|

| Retail deposit rate (2024) | 1.2% |

| Mobile banking use (2024) | 88% |

| Corporate share of loan book | ~45% (Dec 2025) |

| AUM share corporate | 52% (Dec 2025) |

| Pension fund assets | ~ISK 4,200bn (end‑2024) |

| Pension mortgage rate gap | 0.25–0.75 pp (2024) |

| Pension share new mortgages | 15–20% (2024) |

Preview the Actual Deliverable

Arion bank Porter's Five Forces Analysis

This preview shows the exact Arion Bank Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the same professionally written, fully formatted file ready for download and immediate use upon payment.

No mockups or samples: this is the final deliverable, complete and ready for your analysis or presentation.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Arion bank faces moderate rivalry and regulatory scrutiny, with digital incumbents and local customer loyalty shaping competitive dynamics; supplier and buyer power are balanced, while barriers to entry remain medium due to regulatory costs and fintech disruption. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Arion bank’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Funding Sources and Depositors

The primary suppliers of capital for Arion Bank are retail and corporate depositors who fund lending; retail deposits made up about 56% of liabilities and corporate deposits 22% of liabilities as of Q3 2025, per the bank’s report.

Large depositors can shift funds quickly to Íslandsbanki or Landsbankinn if rates lag, giving them leverage; Arion’s LCR (liquidity coverage ratio) was 165% in Sep 2025, so the Central Bank closely watches outflows.

Reliance on Global Technology and Infrastructure Providers

Arion Bank relies on third-party core-banking, cloud, and cybersecurity vendors—notably Microsoft and AWS—creating high supplier power because switching costs and integration time exceed 12–24 months and can cost €5–20m.

In 2024 cloud spend categories rose ~18% industrywide; a 10% price rise from major providers would lift Arion’s IT opex materially and slow digital initiatives.

Availability of Specialized Financial Talent

Iceland’s labor pool has about 370,000 workers (2024), so specialists in data science, compliance, and fintech are scarce; Arion Bank competes with Íslandsbanki, Landsbankinn, and remote roles paying 15–30% premium for tech talent.

Access to International Wholesale Funding Markets

Arion Bank taps international wholesale markets for large projects, issuing green bonds and debt; in 2024 it issued EUR 300m equivalent in green bonds, supporting capital adequacy and lending capacity.

Funding terms hinge on global credit ratings and investor sentiment toward Iceland; Arion’s BBB+ (S&P-equivalent) keeps access broad, but a 100bp rise in global risk premia would raise borrowing costs materially.

A sudden dip in risk appetite could shrink tenor and increase spreads, forcing shorter maturities or higher coupon issuance and pressuring regulatory capital ratios.

- 2024 green bond issuance ~EUR 300m

- Rating: BBB+ (S&P-equivalent)

- 100bp risk-premium shock → higher funding cost

- Investor sentiment tied to Iceland macro (GDP, tourism)

Regulatory Influence of the Central Bank of Iceland

The Central Bank of Iceland supplies systemic stability and liquidity; its policy rate (7.25% in Dec 2025) and countercyclical capital buffer (2.5% since 2023) directly set Arion Bank’s funding cost and capital requirements, leaving the bank little room to negotiate these terms.

The regulator’s mandates thus act as a dominant upstream force shaping margins, credit supply and balance-sheet strategy for Arion Bank.

- Policy rate 7.25% (Dec 2025)

- Countercyclical buffer 2.5% (since 2023)

- Reserve/liquidity rules set funding floor

Strong liquidity (LCR165%) and deposit base, but margins squeezed by tech costs & rates

Suppliers of funds and services exert medium-high power: retail deposits 56% and corporate 22% of liabilities (Q3 2025), LCR 165% (Sep 2025), BBB+ rating, EUR 300m green bonds (2024), policy rate 7.25% and countercyclical buffer 2.5% (Dec 2025); cloud/vendor switching costs 12–24 months (€5–20m) and tech wage premiums 15–30% tighten margins.

| Metric | Value |

|---|---|

| Retail deposits | 56% |

| Corporate deposits | 22% |

| LCR | 165% (Sep 2025) |

| Rating | BBB+ |

| Green bonds | EUR 300m (2024) |

| Policy rate | 7.25% (Dec 2025) |

What is included in the product

Tailored Porter's Five Forces analysis for Arion bank that uncovers competitive intensity, customer and supplier bargaining power, entry barriers, substitute threats, and emerging disruptors, with strategic commentary to inform pricing, profitability, and defensive positioning.

Concise Porter's Five Forces snapshot for Arion Bank—clear, one-sheet insights to speed strategic decisions and boardroom discussions.

Customers Bargaining Power

Low Switching Costs for Retail Banking Clients

In 2025 Icelandic retail clients face very low switching costs thanks to standardized electronic IDs (e-ID) and account portability between the big three banks, so Arion Bank must match market rates—household deposit rates averaged 1.2% in 2024—to avoid outflows. The bank needs top-tier mobile features; 88% of Icelandic adults used mobile banking in 2024, boosting churn risk if apps lag. Real-time fee transparency lets customers compare prices instantly, increasing their bargaining power.

Leverage of Large Corporate and Institutional Clients

Corporate and institutional clients account for roughly 45% of Arion Bank’s loan book and 52% of assets under management as of Dec 2025, giving them strong bargaining power.

They demand bespoke deals, lower margins, and advisory packages; Arion often concedes rates or fees to protect high-volume revenue.

If a major client shifts to rival Landsbankinn, Arion may cut spreads or add services to retain business, squeezing profitability.

Consumer Awareness and Demand for Sustainable Finance

By end-2025 Icelandic consumers show high ESG sensitivity: 62% prioritize green products and 48% would switch banks for sustainable options (Capacent/Maskína 2024–25 surveys). Demand for green mortgages and ethical funds forces Arion Bank to expand ESG offerings or risk reputational harm and market-share loss to greener rivals; missed targets could cut retail deposits and new mortgage origination by mid-single digits.

Influence of Pension Funds on the Mortgage Market

Icelandic pension funds (largest: the four universal funds and large occupational funds) held about ISK 4,200bn in assets at end-2024 and offered mortgage rates ~0.25–0.75 percentage points below bank averages, creating a strong non-bank alternative that forces Arion Bank to keep mortgage pricing competitive.

Their market moves boost buyer bargaining power: in 2024 pension-funded mortgages accounted for ~15–20% of new mortgage originations, so Arion must match rates or risk margin erosion.

- Pension funds’ assets: ~ISK 4,200bn (end-2024)

- Rate gap vs banks: ~0.25–0.75 pp (2024)

- Share of new mortgages: ~15–20% (2024)

- Effect: raises buyer bargaining power, compresses Arion margins

Digital Transparency and Price Comparison Tools

High customer leverage: mobile-first switching, corporate loans & pension mortgage pressure

Customers hold high bargaining power: retail switching is easy due to e-ID and portability, with household deposit rates 1.2% in 2024 and mobile banking use 88% (2024). Corporates drive ~45% of loan book and 52% AUM (Dec 2025), forcing bespoke pricing. Pension funds held ~ISK 4,200bn (end‑2024) and offered mortgages 0.25–0.75pp cheaper, taking 15–20% of new originations (2024).

| Metric | Value |

|---|---|

| Retail deposit rate (2024) | 1.2% |

| Mobile banking use (2024) | 88% |

| Corporate share of loan book | ~45% (Dec 2025) |

| AUM share corporate | 52% (Dec 2025) |

| Pension fund assets | ~ISK 4,200bn (end‑2024) |

| Pension mortgage rate gap | 0.25–0.75 pp (2024) |

| Pension share new mortgages | 15–20% (2024) |

Preview the Actual Deliverable

Arion bank Porter's Five Forces Analysis

This preview shows the exact Arion Bank Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the same professionally written, fully formatted file ready for download and immediate use upon payment.

No mockups or samples: this is the final deliverable, complete and ready for your analysis or presentation.