Armstrong World Industries Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

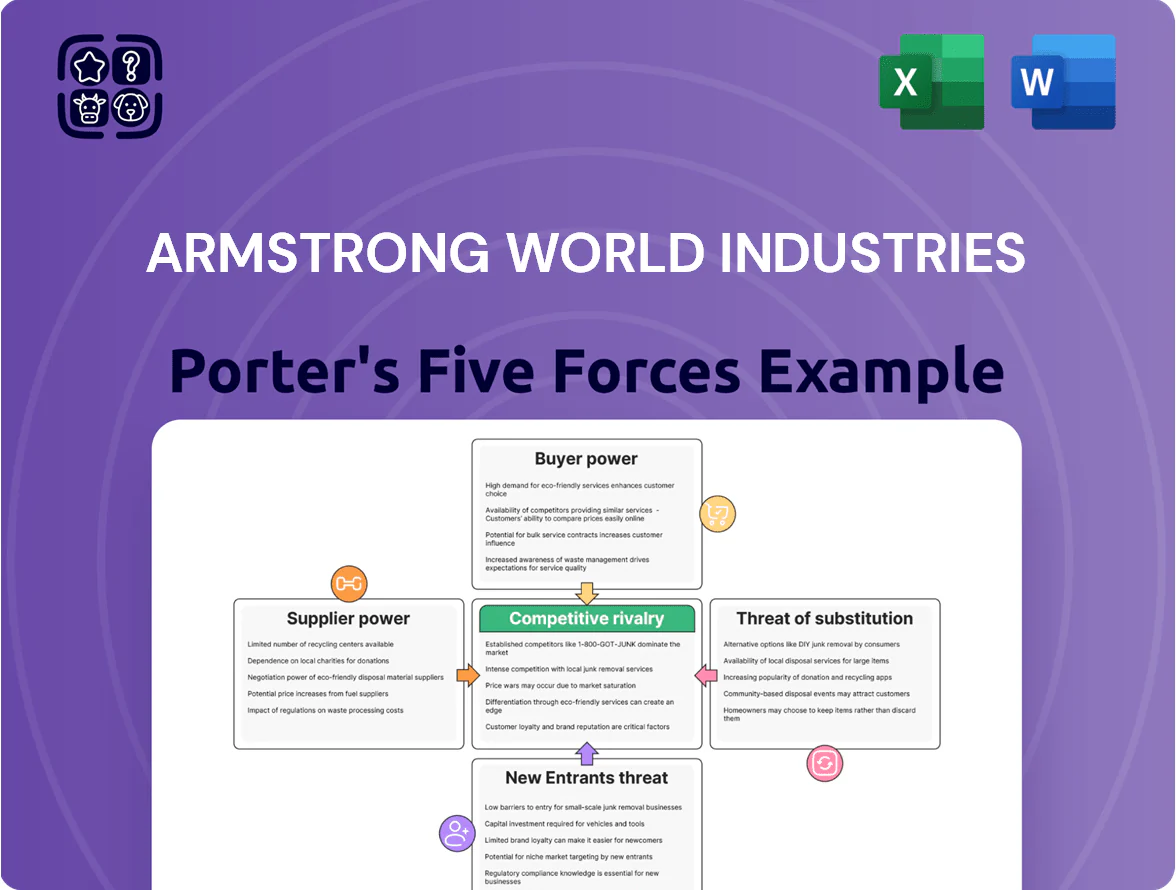

Armstrong World Industries faces moderate supplier power, steady buyer expectations, and rising competitive pressure from low-cost and innovative building-material firms, while regulatory and sustainability trends heighten industry threats and substitute risks.

Suppliers Bargaining Power

Raw Material Commodity Volatility

Armstrong relies on mineral wool, perlite, and steel for ceilings and suspension systems; these inputs made up ~28% of COGS in FY2024.

By Q4 2025, energy-driven freight and base-metal prices pushed per-ton steel input costs up ~14% year-over-year, raising manufacturing costs about 3–4 percentage points of gross margin.

Because these are global commodities traded on LME and ICE, Armstrong has limited pricing power to absorb spikes, increasing supplier bargaining pressure.

Energy Intensity of Manufacturing

Production of ceiling tiles and metal frames uses large amounts of natural gas and electricity, making energy suppliers leverageable; U.S. industrial electricity intensity for building materials averaged ~0.85 MWh/ton in 2023, and natural gas prices rose 34% year-over-year in 2022–23, squeezing margins. The green-energy transition has caused localized supply tightness—utility capex rose 12% in 2024—so Armstrong must tightly manage energy procurement and hedging to protect operating margin targets near 12% (FY2024).

Specialized Chemical Additives

Specialized coatings and fire-retardant additives for Armstrong World Industries come from a concentrated set of specialty chemical makers—three firms supplied ~65% of similar US construction additives in 2024—so switching costs are high due to patented formulations and technical support.

That IP and required validation raise supplier leverage on price and lead times, giving them moderate bargaining power that can squeeze margins; Armstrong reported 2024 gross margin pressures in building products of ~120 basis points versus 2023.

Logistics and Transportation Constraints

The delivery of Armstrong World Industries ceiling panels relies on freight and shipping; US trucking saw a 10% driver shortage in 2024, raising spot rates ~18% year-over-year and increasing carriers' pricing power.

Supply-chain disruptions—2023–24 port congestion and 12% higher diesel costs in 2024—make logistics firms able to push higher rates, which hits Armstrong harder because ceilings are bulky and freight can be 5–12% of product COGS.

- Heavy SKUs raise freight sensitivity

- Trucking driver shortfall ~10% (2024)

- Spot rates up ~18% YoY (2024)

- Diesel +12% (2024) boosts shipping costs

Supplier Concentration in Steel

The steel for Armstrong World Industries ceiling grids is concentrated among a few large mills; global crude steel capacity is dominated by ~20 firms holding over 50% of production as of 2024, limiting supplier options.

High capital and thin margins in steelmaking mean few vendors supply high-quality galvanized coils, and mills passed through a ~30% raw-steel price rise from 2020–2022, showing pricing power.

This concentration lets producers more easily push cost increases onto buyers like Armstrong, raising input-cost volatility risk.

- Few suppliers: top 20 = >50% capacity (2024)

- High capex: steel mill builds >$1B each

- Price pass-through: ~30% steel price rise 2020–22

Rising input costs, concentrated suppliers squeeze margins—steel +14%, inputs ~28% COGS

Suppliers hold moderate-to-high bargaining power: key inputs (mineral wool, perlite, steel) = ~28% of COGS (FY2024); steel input costs +14% YoY by Q4 2025, cutting gross margin ~3–4 ppt; specialty chemicals concentrated (3 firms ≈65% supply, 2024) and energy/trucking cost shocks (natural gas +34% 2022–23; diesel +12% 2024; trucking spot +18% 2024) add pressure.

| Metric | Value |

|---|---|

| Inputs as % COGS (FY2024) | ~28% |

| Steel cost change (Q4 2025 YoY) | +14% |

| Specialty suppliers concentration (2024) | Top 3 ≈65% |

| Natural gas change (2022–23) | +34% |

| Diesel (2024) | +12% |

| Trucking spot rates (2024) | +18% |

What is included in the product

Tailored exclusively for Armstrong World Industries, this Porter's Five Forces overview uncovers key drivers of competition, buyer and supplier influence, entry barriers, substitute threats, and strategic implications for pricing and profitability within the specialty building materials market.

Concise Porter's Five Forces snapshot for Armstrong World Industries—instantly identifies competitive pressures and strategic levers to relieve margin and growth pain points.

Customers Bargaining Power

Concentration of Major Distributors

A significant share of Armstrong World Industries’ 2024 net sales—about 45% of specialty ceilings and suspension systems—flows through large distributors such as ABC Supply and national interior contractors, giving these buyers scale to demand deeper discounts and extended credit; ABC Supply alone accounted for an estimated 8–12% of category volumes in 2023. Their power rises because they can stock rival brands and switch orders quickly, pressuring Armstrong’s margins and forcing promotional allowances and tighter payment terms.

Price Sensitivity in Commercial Real Estate

With office occupancy still ~20–30% below 2019 peaks in major US CBDs by end-2025, developers push cost-efficiency, raising customer price sensitivity for Armstrong World Industries' ceiling systems.

Large commercial projects use competitive bidding—44% of US office build contracts in 2024 were awarded on lowest-price criteria—so price often beats brand in final selection.

Project managers, facing average fit-out capex cuts of 12% in 2023–25, can demand tighter margins and volume discounts from manufacturers to keep bids viable.

Low Switching Costs for Standard Products

For basic acoustic tiles and standard grid systems, customers can switch brands with minimal technical effort, lowering Armstrong World Industries’ bargaining power; industry surveys show commodity-grade tile accounts for ~42% of US volume in 2024, where product differentiation is low. If Armstrong’s prices exceed rivals, buyers—especially contractors—can shift quickly, and Armstrong lost price share in 2023 to lower-cost imports. This ease of switching forces Armstrong to compete on service, logistics, and perceived reliability, keeping gross margins under pressure in commodity segments.

Information Symmetry and Digital Procurement

Modern procurement platforms let contractors compare Armstrong World Industries tile specs and prices in real time, cutting the manufacturer’s information edge; a 2024 McKinsey survey found 68% of construction buyers use digital sourcing tools.

That transparency empowers buyers to demand price parity and faster lead times—Armstrong’s margin pressure rose as materials commoditized, with gross margin slipping to 20.3% in FY2024.

- Real-time price/spec comparison

- 68% buyers use digital sourcing (2024 McKinsey)

- Buyers push for parity, shorter lead times

- Armstrong gross margin 20.3% FY2024

Influence of Architects and Designers

- Architects specify ~38% of nonresidential ceilings in 2024

- Armstrong net sales 2024: $2.9 billion

- Designer preference shifts directly cut pull-through demand

- CEUs, demos, and sustainability data mitigate influence

Distributor leverage, digital sourcing squeeze margins—Armstrong must defend specs

Buyers (distributors, contractors, developers) hold strong leverage—ABC Supply ~8–12% category share (2023); distributors drove ~45% of Armstrong 2024 specialty ceilings sales; gross margin fell to 20.3% FY2024. Commodity tiles (~42% US volume 2024) and digital sourcing (68% buyers 2024) raise price sensitivity; architects specify ~38% nonresidential ceilings (2024), so Armstrong must use CEUs, demos, and sustainability data to defend specs.

| Metric | Value |

|---|---|

| Armstrong 2024 sales | $2.9B |

| Gross margin FY2024 | 20.3% |

| Commodity tile share 2024 | 42% |

| Digital sourcing use 2024 | 68% |

| Architect spec share 2024 | 38% |

Preview Before You Purchase

Armstrong World Industries Porter's Five Forces Analysis

This preview shows the exact Armstrong World Industries Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document is fully formatted, professionally written, and ready for download and use the moment you buy. It contains the complete evaluation of competitive rivalry, threat of new entrants, bargaining power of suppliers and buyers, and substitute threats. What you see is precisely what you'll get.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Armstrong World Industries faces moderate supplier power, steady buyer expectations, and rising competitive pressure from low-cost and innovative building-material firms, while regulatory and sustainability trends heighten industry threats and substitute risks.

Suppliers Bargaining Power

Raw Material Commodity Volatility

Armstrong relies on mineral wool, perlite, and steel for ceilings and suspension systems; these inputs made up ~28% of COGS in FY2024.

By Q4 2025, energy-driven freight and base-metal prices pushed per-ton steel input costs up ~14% year-over-year, raising manufacturing costs about 3–4 percentage points of gross margin.

Because these are global commodities traded on LME and ICE, Armstrong has limited pricing power to absorb spikes, increasing supplier bargaining pressure.

Energy Intensity of Manufacturing

Production of ceiling tiles and metal frames uses large amounts of natural gas and electricity, making energy suppliers leverageable; U.S. industrial electricity intensity for building materials averaged ~0.85 MWh/ton in 2023, and natural gas prices rose 34% year-over-year in 2022–23, squeezing margins. The green-energy transition has caused localized supply tightness—utility capex rose 12% in 2024—so Armstrong must tightly manage energy procurement and hedging to protect operating margin targets near 12% (FY2024).

Specialized Chemical Additives

Specialized coatings and fire-retardant additives for Armstrong World Industries come from a concentrated set of specialty chemical makers—three firms supplied ~65% of similar US construction additives in 2024—so switching costs are high due to patented formulations and technical support.

That IP and required validation raise supplier leverage on price and lead times, giving them moderate bargaining power that can squeeze margins; Armstrong reported 2024 gross margin pressures in building products of ~120 basis points versus 2023.

Logistics and Transportation Constraints

The delivery of Armstrong World Industries ceiling panels relies on freight and shipping; US trucking saw a 10% driver shortage in 2024, raising spot rates ~18% year-over-year and increasing carriers' pricing power.

Supply-chain disruptions—2023–24 port congestion and 12% higher diesel costs in 2024—make logistics firms able to push higher rates, which hits Armstrong harder because ceilings are bulky and freight can be 5–12% of product COGS.

- Heavy SKUs raise freight sensitivity

- Trucking driver shortfall ~10% (2024)

- Spot rates up ~18% YoY (2024)

- Diesel +12% (2024) boosts shipping costs

Supplier Concentration in Steel

The steel for Armstrong World Industries ceiling grids is concentrated among a few large mills; global crude steel capacity is dominated by ~20 firms holding over 50% of production as of 2024, limiting supplier options.

High capital and thin margins in steelmaking mean few vendors supply high-quality galvanized coils, and mills passed through a ~30% raw-steel price rise from 2020–2022, showing pricing power.

This concentration lets producers more easily push cost increases onto buyers like Armstrong, raising input-cost volatility risk.

- Few suppliers: top 20 = >50% capacity (2024)

- High capex: steel mill builds >$1B each

- Price pass-through: ~30% steel price rise 2020–22

Rising input costs, concentrated suppliers squeeze margins—steel +14%, inputs ~28% COGS

Suppliers hold moderate-to-high bargaining power: key inputs (mineral wool, perlite, steel) = ~28% of COGS (FY2024); steel input costs +14% YoY by Q4 2025, cutting gross margin ~3–4 ppt; specialty chemicals concentrated (3 firms ≈65% supply, 2024) and energy/trucking cost shocks (natural gas +34% 2022–23; diesel +12% 2024; trucking spot +18% 2024) add pressure.

| Metric | Value |

|---|---|

| Inputs as % COGS (FY2024) | ~28% |

| Steel cost change (Q4 2025 YoY) | +14% |

| Specialty suppliers concentration (2024) | Top 3 ≈65% |

| Natural gas change (2022–23) | +34% |

| Diesel (2024) | +12% |

| Trucking spot rates (2024) | +18% |

What is included in the product

Tailored exclusively for Armstrong World Industries, this Porter's Five Forces overview uncovers key drivers of competition, buyer and supplier influence, entry barriers, substitute threats, and strategic implications for pricing and profitability within the specialty building materials market.

Concise Porter's Five Forces snapshot for Armstrong World Industries—instantly identifies competitive pressures and strategic levers to relieve margin and growth pain points.

Customers Bargaining Power

Concentration of Major Distributors

A significant share of Armstrong World Industries’ 2024 net sales—about 45% of specialty ceilings and suspension systems—flows through large distributors such as ABC Supply and national interior contractors, giving these buyers scale to demand deeper discounts and extended credit; ABC Supply alone accounted for an estimated 8–12% of category volumes in 2023. Their power rises because they can stock rival brands and switch orders quickly, pressuring Armstrong’s margins and forcing promotional allowances and tighter payment terms.

Price Sensitivity in Commercial Real Estate

With office occupancy still ~20–30% below 2019 peaks in major US CBDs by end-2025, developers push cost-efficiency, raising customer price sensitivity for Armstrong World Industries' ceiling systems.

Large commercial projects use competitive bidding—44% of US office build contracts in 2024 were awarded on lowest-price criteria—so price often beats brand in final selection.

Project managers, facing average fit-out capex cuts of 12% in 2023–25, can demand tighter margins and volume discounts from manufacturers to keep bids viable.

Low Switching Costs for Standard Products

For basic acoustic tiles and standard grid systems, customers can switch brands with minimal technical effort, lowering Armstrong World Industries’ bargaining power; industry surveys show commodity-grade tile accounts for ~42% of US volume in 2024, where product differentiation is low. If Armstrong’s prices exceed rivals, buyers—especially contractors—can shift quickly, and Armstrong lost price share in 2023 to lower-cost imports. This ease of switching forces Armstrong to compete on service, logistics, and perceived reliability, keeping gross margins under pressure in commodity segments.

Information Symmetry and Digital Procurement

Modern procurement platforms let contractors compare Armstrong World Industries tile specs and prices in real time, cutting the manufacturer’s information edge; a 2024 McKinsey survey found 68% of construction buyers use digital sourcing tools.

That transparency empowers buyers to demand price parity and faster lead times—Armstrong’s margin pressure rose as materials commoditized, with gross margin slipping to 20.3% in FY2024.

- Real-time price/spec comparison

- 68% buyers use digital sourcing (2024 McKinsey)

- Buyers push for parity, shorter lead times

- Armstrong gross margin 20.3% FY2024

Influence of Architects and Designers

- Architects specify ~38% of nonresidential ceilings in 2024

- Armstrong net sales 2024: $2.9 billion

- Designer preference shifts directly cut pull-through demand

- CEUs, demos, and sustainability data mitigate influence

Distributor leverage, digital sourcing squeeze margins—Armstrong must defend specs

Buyers (distributors, contractors, developers) hold strong leverage—ABC Supply ~8–12% category share (2023); distributors drove ~45% of Armstrong 2024 specialty ceilings sales; gross margin fell to 20.3% FY2024. Commodity tiles (~42% US volume 2024) and digital sourcing (68% buyers 2024) raise price sensitivity; architects specify ~38% nonresidential ceilings (2024), so Armstrong must use CEUs, demos, and sustainability data to defend specs.

| Metric | Value |

|---|---|

| Armstrong 2024 sales | $2.9B |

| Gross margin FY2024 | 20.3% |

| Commodity tile share 2024 | 42% |

| Digital sourcing use 2024 | 68% |

| Architect spec share 2024 | 38% |

Preview Before You Purchase

Armstrong World Industries Porter's Five Forces Analysis

This preview shows the exact Armstrong World Industries Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document is fully formatted, professionally written, and ready for download and use the moment you buy. It contains the complete evaluation of competitive rivalry, threat of new entrants, bargaining power of suppliers and buyers, and substitute threats. What you see is precisely what you'll get.