Array Networks Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

Array Networks faces moderate supplier power, niche customer bargaining, and evolving threats from cloud-native competitors that compress margins and spur innovation.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Array Networks’s competitive dynamics, market pressures, and strategic advantages in detail.

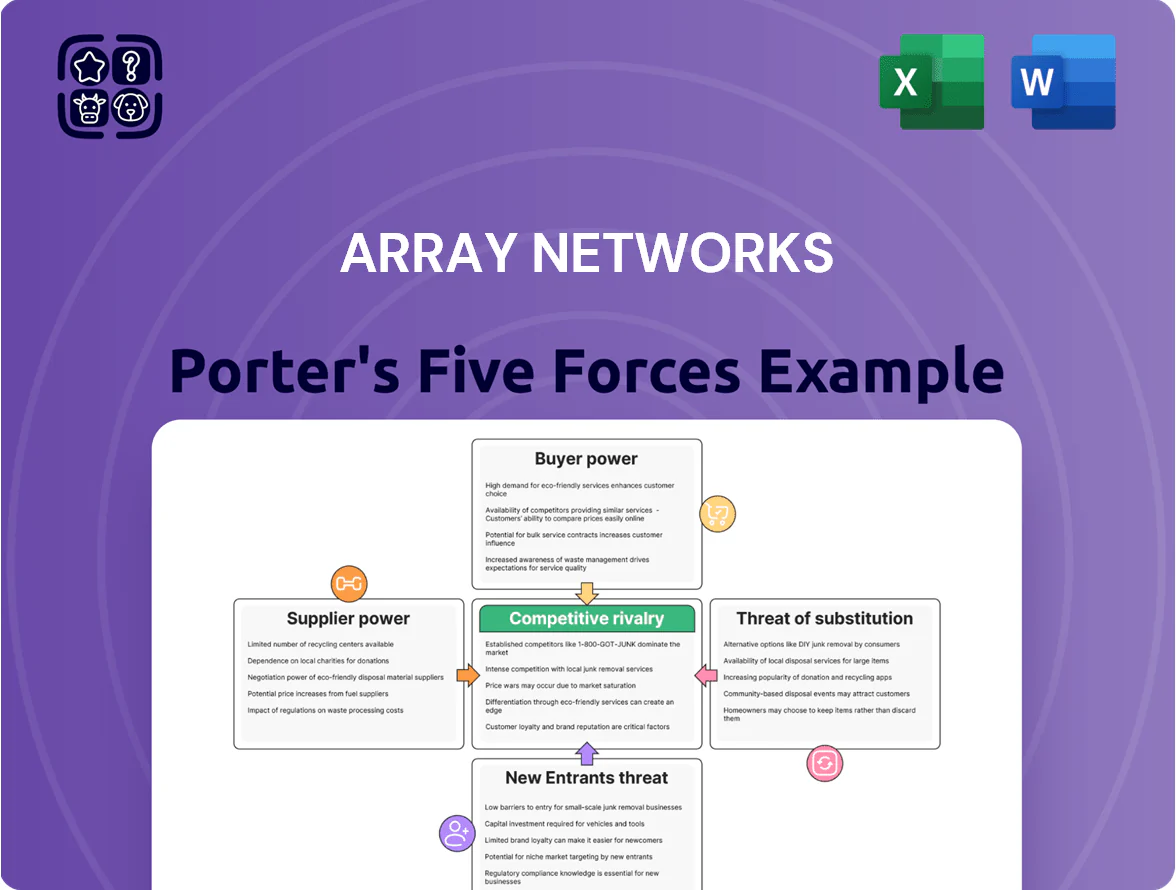

Suppliers Bargaining Power

Concentration of Specialized Component Manufacturers

Array Networks depends on specialized hardware like high-performance processors and NICs, and the market concentration among high-end semiconductor suppliers—Intel and AMD held about 72% share of server CPU shipments in 2024—gives those vendors strong pricing power.

This supplier concentration raises risk: Intel’s supply constraints in Q3 2024 and a 15% year-over-year rise in enterprise CPU prices drove margin pressure across network appliance vendors.

If global demand shifts, concentrated sourcing can cause sudden price spikes or multi-week bottlenecks, as seen in 2021–2024 when lead times for select ASICs stretched past 20 weeks.

Software and Kernel Licensing Dependencies

Array Networks builds proprietary appliances but relies on open-source kernels and third-party crypto/security libraries; shifts in licensing or support—like OpenSSL’s 2023 funding model changes—can raise Array’s development costs and delay roadmaps.

Vendor license shifts often force audits, re-coding, or paid support: industry data show 42% of networking firms faced >$1M remediation costs in 2024 after dependency changes.

The technical burden of migrating OS kernels or libs gives these digital suppliers higher bargaining power, because porting firmware and validating certifications (FIPS, Common Criteria) is time-consuming and costly.

Contract Manufacturing Consolidation

Array relies on a small set of Asian original design manufacturers (ODMs) for physical ADC assembly; these ODMs run specialized lines that cost tens of millions to replicate, giving suppliers significant contract leverage.

In 2024, Taiwan and China plants handled >70% of network hardware output, so a single-site disruption can delay shipments and hit quarterly revenue—Array reported supply-chain constraints trimming FY2024 revenue by ~4%.

Rising Costs of Specialized Engineering Talent

The human capital to build advanced networking and encryption algorithms is a critical supplier; worldwide demand for cybersecurity specialists grew 350,000 net new roles in 2024, tightening supply.

As demand outstrips supply, engineers gain bargaining power, forcing Array Networks to match market pay—US median cybersecurity salary reached $125,000 in 2024—pressuring gross margins.

If Array delays higher pay, rivals like Google and Cisco can poach staff, raising hiring costs and time-to-market risks.

- Critical input: specialized engineers

- 2024 net new cyber roles: +350,000

- US median cyber pay 2024: $125,000

- Margin pressure from higher comp and churn

Proprietary Hardware Interoperability

Proprietary chipsets for SSL acceleration and compression are critical to Array Networks appliances, creating technical lock-in that raises switching costs; Array reported 62% of revenue in 2024 from hardware-plus-software bundles, underscoring dependence on specialized components.

Moving to alternative architectures would need large R&D spend and software re-optimization—industry estimates put redevelopment at $25–40M and 18–24 months for comparable throughput and security validation.

That lock-in lets chipset suppliers keep firm prices; for example, vendors in 2024 maintained 10–15% higher ASPs for specialized crypto ASICs versus commodity NICs, squeezing buyers' bargaining power.

- Proprietary chipsets = high switching cost

- Redevelopment ≈ $25–40M, 18–24 months

- 2024: 62% of Array revenue tied to hardware bundles

- Specialized ASIC ASPs 10–15% above commodity parts

Concentrated suppliers and scarce cyber talent create costly delivery and switching risks

Suppliers hold high power: concentrated CPU/ASIC vendors (Intel/AMD ~72% server CPU share in 2024), ODMs in Taiwan/China supplying >70% hardware, and scarce cybersecurity engineers (net +350,000 roles in 2024; US median pay $125,000) drive price and delivery risk, plus high switching costs (hardware+software bundles = 62% of Array 2024 revenue; redevelop cost $25–40M, 18–24 months).

| Metric | 2024 value |

|---|---|

| Intel/AMD server CPU share | ~72% |

| Taiwan/China hardware output | >70% |

| Net new cyber roles | +350,000 |

| US median cyber pay | $125,000 |

| Hardware+software revenue | 62% |

| Redevelop cost/time | $25–40M; 18–24m |

What is included in the product

Tailored exclusively for Array Networks, this Porter's Five Forces overview uncovers competitive drivers, customer and supplier power, entry barriers, and substitution threats—highlighting disruptive forces and strategic levers that affect its pricing, profitability, and market position.

Concise Porter's Five Forces snapshot for Array Networks—clarify competitive pressures and highlight relief levers for pricing, partnerships, and tech differentiation in one decision-ready view.

Customers Bargaining Power

High Concentration of Enterprise Clients

Array Networks serves large enterprises and government agencies that buy in bulk, so single contracts can account for 10–20% of annual revenue (Array reported $78.6M revenue in FY2024), giving buyers strong leverage to demand custom features, extended SLAs, and steep volume discounts; procurement teams routinely push prices down while requiring multi-year support, raising margin pressure and elongating sales cycles.

Availability of Well-Established Alternatives

Customers can choose among mature ADC and secure access gateway vendors—F5, Citrix, and Fortinet together held around 55% of the global ADC/secure access market in 2024—letting buyers pit suppliers against each other to cut prices.

Public specs, benchmarks, and pricing portals make feature-by-feature comparisons quick; procurement teams commonly narrow suppliers to 2–3 finalists, which raises Array Networks’ pressure to match discounts or add services.

Low Switching Costs for Virtualized Solutions

As enterprises shift to virtual application delivery, switching costs fall: 2024 Cloud Native Computing Foundation data show 62% of orgs run multiple virtual appliances, easing migration between vendors without hardware swaps.

Software-defined networking (SDN) lets firms move workloads quickly; a 2025 IDC survey found 48% of users changed ADC vendors for price or performance in the past 18 months.

That flexibility raises customer bargaining power, pressuring Array Networks to compete on price, features, and integration to avoid churn.

Budget Sensitivity in Mid-Market Segments

Mid-market buyers prioritize total cost of ownership (TCO) over raw performance, so Array must prove ROI or risk losing deals to cheaper rivals; 2024 channel surveys show 62% of mid-market IT buyers cite TCO as primary purchase driver.

This price sensitivity forces Array to keep competitive pricing and value bundles—Array reported ~8% revenue exposure in the SMB/mid-market in FY2024, meaning losing price-sensitive accounts could dent growth.

- 62% mid-market cite TCO as top factor

- Array ~8% FY2024 revenue from mid-market

- Must show clear ROI or face lower-cost substitutes

Informed Buyers and RFP Processes

Decision-makers at client firms are typically senior IT architects and procurement leads who run strict RFPs; 78% of enterprise network purchases in 2024 used formal RFPs or RFIs, per IDC, which compresses vendor margins by eliminating information asymmetry.

These buyers know benchmarks like throughput, latency, and TCAM density and demand SLAs and price concessions; Array Networks faces pressure to offer detailed performance proofs and service guarantees to close deals.

- 78% of enterprise buys used RFPs (IDC, 2024)

- Buyers demand SLAs, benchmarks, and performance proofs

- Information symmetry lowers pricing power and margins

- Vendors must offer value-added services to preserve margins

Buyers Drive Discounts & SLAs—Array Must Prove ROI or Lose Deals

Customers hold strong bargaining power: large contracts (10–20% of Array’s FY2024 $78.6M revenue) and mature rivals (F5/Citrix/Fortinet ~55% market share in 2024) force discounts, SLAs, and long sales cycles; 78% of enterprise buys used RFPs (IDC 2024) and 62% of mid-market buyers cite TCO (2024), so Array must match price, ROI proofs, and services to avoid churn.

| Metric | Value |

|---|---|

| FY2024 revenue | $78.6M |

| Top rivals' share (2024) | ~55% |

| Enterprise RFPs (2024) | 78% |

| Mid-market TCO focus (2024) | 62% |

What You See Is What You Get

Array Networks Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for Array Networks you’ll receive immediately after purchase—no surprises, no placeholders; it’s fully formatted and ready for use.

The document displayed here is the actual deliverable, containing in-depth competitive assessment and actionable insights, and will be available for instant download the moment you complete your purchase.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Array Networks faces moderate supplier power, niche customer bargaining, and evolving threats from cloud-native competitors that compress margins and spur innovation.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Array Networks’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Specialized Component Manufacturers

Array Networks depends on specialized hardware like high-performance processors and NICs, and the market concentration among high-end semiconductor suppliers—Intel and AMD held about 72% share of server CPU shipments in 2024—gives those vendors strong pricing power.

This supplier concentration raises risk: Intel’s supply constraints in Q3 2024 and a 15% year-over-year rise in enterprise CPU prices drove margin pressure across network appliance vendors.

If global demand shifts, concentrated sourcing can cause sudden price spikes or multi-week bottlenecks, as seen in 2021–2024 when lead times for select ASICs stretched past 20 weeks.

Software and Kernel Licensing Dependencies

Array Networks builds proprietary appliances but relies on open-source kernels and third-party crypto/security libraries; shifts in licensing or support—like OpenSSL’s 2023 funding model changes—can raise Array’s development costs and delay roadmaps.

Vendor license shifts often force audits, re-coding, or paid support: industry data show 42% of networking firms faced >$1M remediation costs in 2024 after dependency changes.

The technical burden of migrating OS kernels or libs gives these digital suppliers higher bargaining power, because porting firmware and validating certifications (FIPS, Common Criteria) is time-consuming and costly.

Contract Manufacturing Consolidation

Array relies on a small set of Asian original design manufacturers (ODMs) for physical ADC assembly; these ODMs run specialized lines that cost tens of millions to replicate, giving suppliers significant contract leverage.

In 2024, Taiwan and China plants handled >70% of network hardware output, so a single-site disruption can delay shipments and hit quarterly revenue—Array reported supply-chain constraints trimming FY2024 revenue by ~4%.

Rising Costs of Specialized Engineering Talent

The human capital to build advanced networking and encryption algorithms is a critical supplier; worldwide demand for cybersecurity specialists grew 350,000 net new roles in 2024, tightening supply.

As demand outstrips supply, engineers gain bargaining power, forcing Array Networks to match market pay—US median cybersecurity salary reached $125,000 in 2024—pressuring gross margins.

If Array delays higher pay, rivals like Google and Cisco can poach staff, raising hiring costs and time-to-market risks.

- Critical input: specialized engineers

- 2024 net new cyber roles: +350,000

- US median cyber pay 2024: $125,000

- Margin pressure from higher comp and churn

Proprietary Hardware Interoperability

Proprietary chipsets for SSL acceleration and compression are critical to Array Networks appliances, creating technical lock-in that raises switching costs; Array reported 62% of revenue in 2024 from hardware-plus-software bundles, underscoring dependence on specialized components.

Moving to alternative architectures would need large R&D spend and software re-optimization—industry estimates put redevelopment at $25–40M and 18–24 months for comparable throughput and security validation.

That lock-in lets chipset suppliers keep firm prices; for example, vendors in 2024 maintained 10–15% higher ASPs for specialized crypto ASICs versus commodity NICs, squeezing buyers' bargaining power.

- Proprietary chipsets = high switching cost

- Redevelopment ≈ $25–40M, 18–24 months

- 2024: 62% of Array revenue tied to hardware bundles

- Specialized ASIC ASPs 10–15% above commodity parts

Concentrated suppliers and scarce cyber talent create costly delivery and switching risks

Suppliers hold high power: concentrated CPU/ASIC vendors (Intel/AMD ~72% server CPU share in 2024), ODMs in Taiwan/China supplying >70% hardware, and scarce cybersecurity engineers (net +350,000 roles in 2024; US median pay $125,000) drive price and delivery risk, plus high switching costs (hardware+software bundles = 62% of Array 2024 revenue; redevelop cost $25–40M, 18–24 months).

| Metric | 2024 value |

|---|---|

| Intel/AMD server CPU share | ~72% |

| Taiwan/China hardware output | >70% |

| Net new cyber roles | +350,000 |

| US median cyber pay | $125,000 |

| Hardware+software revenue | 62% |

| Redevelop cost/time | $25–40M; 18–24m |

What is included in the product

Tailored exclusively for Array Networks, this Porter's Five Forces overview uncovers competitive drivers, customer and supplier power, entry barriers, and substitution threats—highlighting disruptive forces and strategic levers that affect its pricing, profitability, and market position.

Concise Porter's Five Forces snapshot for Array Networks—clarify competitive pressures and highlight relief levers for pricing, partnerships, and tech differentiation in one decision-ready view.

Customers Bargaining Power

High Concentration of Enterprise Clients

Array Networks serves large enterprises and government agencies that buy in bulk, so single contracts can account for 10–20% of annual revenue (Array reported $78.6M revenue in FY2024), giving buyers strong leverage to demand custom features, extended SLAs, and steep volume discounts; procurement teams routinely push prices down while requiring multi-year support, raising margin pressure and elongating sales cycles.

Availability of Well-Established Alternatives

Customers can choose among mature ADC and secure access gateway vendors—F5, Citrix, and Fortinet together held around 55% of the global ADC/secure access market in 2024—letting buyers pit suppliers against each other to cut prices.

Public specs, benchmarks, and pricing portals make feature-by-feature comparisons quick; procurement teams commonly narrow suppliers to 2–3 finalists, which raises Array Networks’ pressure to match discounts or add services.

Low Switching Costs for Virtualized Solutions

As enterprises shift to virtual application delivery, switching costs fall: 2024 Cloud Native Computing Foundation data show 62% of orgs run multiple virtual appliances, easing migration between vendors without hardware swaps.

Software-defined networking (SDN) lets firms move workloads quickly; a 2025 IDC survey found 48% of users changed ADC vendors for price or performance in the past 18 months.

That flexibility raises customer bargaining power, pressuring Array Networks to compete on price, features, and integration to avoid churn.

Budget Sensitivity in Mid-Market Segments

Mid-market buyers prioritize total cost of ownership (TCO) over raw performance, so Array must prove ROI or risk losing deals to cheaper rivals; 2024 channel surveys show 62% of mid-market IT buyers cite TCO as primary purchase driver.

This price sensitivity forces Array to keep competitive pricing and value bundles—Array reported ~8% revenue exposure in the SMB/mid-market in FY2024, meaning losing price-sensitive accounts could dent growth.

- 62% mid-market cite TCO as top factor

- Array ~8% FY2024 revenue from mid-market

- Must show clear ROI or face lower-cost substitutes

Informed Buyers and RFP Processes

Decision-makers at client firms are typically senior IT architects and procurement leads who run strict RFPs; 78% of enterprise network purchases in 2024 used formal RFPs or RFIs, per IDC, which compresses vendor margins by eliminating information asymmetry.

These buyers know benchmarks like throughput, latency, and TCAM density and demand SLAs and price concessions; Array Networks faces pressure to offer detailed performance proofs and service guarantees to close deals.

- 78% of enterprise buys used RFPs (IDC, 2024)

- Buyers demand SLAs, benchmarks, and performance proofs

- Information symmetry lowers pricing power and margins

- Vendors must offer value-added services to preserve margins

Buyers Drive Discounts & SLAs—Array Must Prove ROI or Lose Deals

Customers hold strong bargaining power: large contracts (10–20% of Array’s FY2024 $78.6M revenue) and mature rivals (F5/Citrix/Fortinet ~55% market share in 2024) force discounts, SLAs, and long sales cycles; 78% of enterprise buys used RFPs (IDC 2024) and 62% of mid-market buyers cite TCO (2024), so Array must match price, ROI proofs, and services to avoid churn.

| Metric | Value |

|---|---|

| FY2024 revenue | $78.6M |

| Top rivals' share (2024) | ~55% |

| Enterprise RFPs (2024) | 78% |

| Mid-market TCO focus (2024) | 62% |

What You See Is What You Get

Array Networks Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for Array Networks you’ll receive immediately after purchase—no surprises, no placeholders; it’s fully formatted and ready for use.

The document displayed here is the actual deliverable, containing in-depth competitive assessment and actionable insights, and will be available for instant download the moment you complete your purchase.