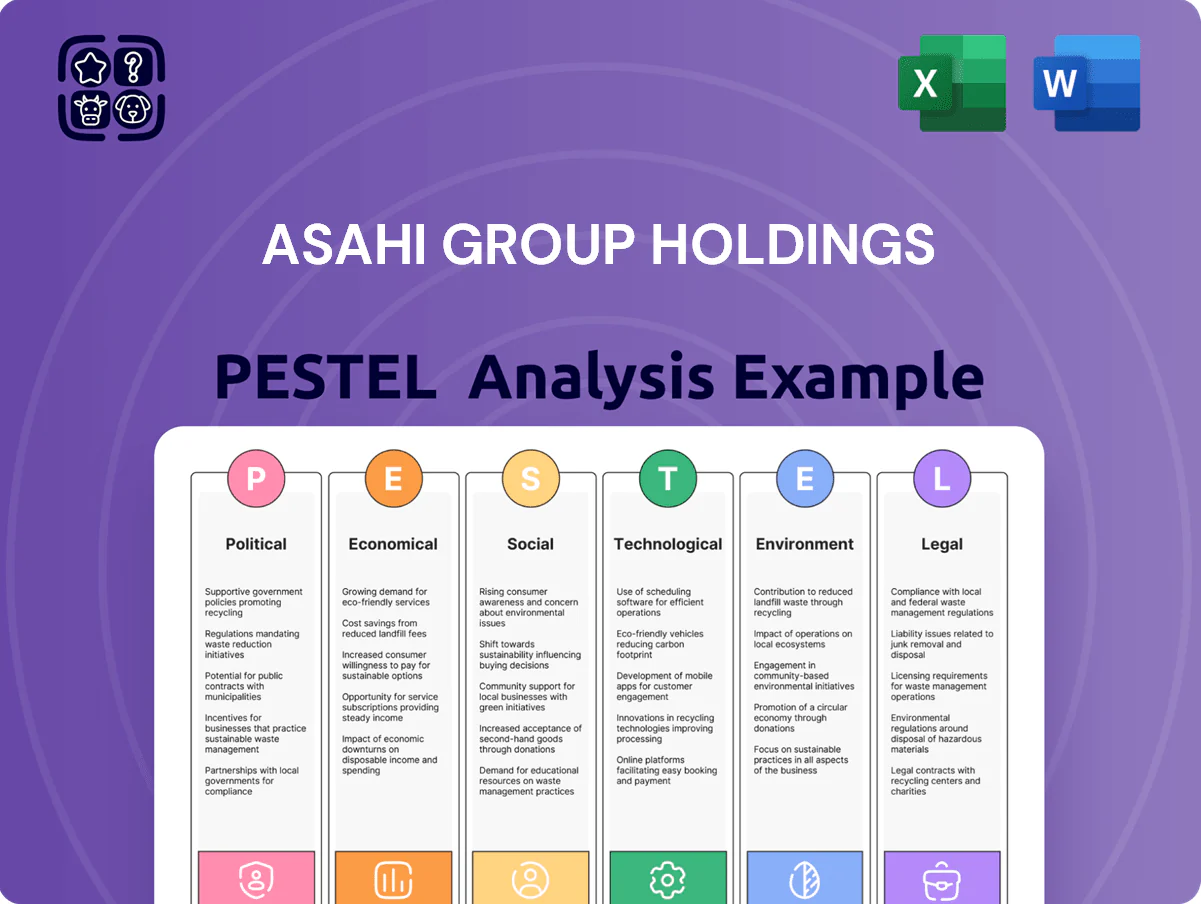

Asahi Group Holdings PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Uncover how political shifts, economic cycles, social trends, and technological change shape Asahi Group Holdings' strategic outlook with our concise PESTLE snapshot—perfect for investors and strategists seeking actionable context. Purchase the full PESTLE for a complete, downloadable analysis with regulatory, environmental, and legal deep dives to inform smarter decisions today.

Political factors

Geopolitical Trade Relations

Asahi Group Holdings operates across Europe, Oceania and Southeast Asia, making it vulnerable to shifting trade agreements and geopolitical tensions that in 2024 affected 32% of its international revenue exposure; tariff changes between Japan and EU/ASEAN partners could raise input costs and logistics expenses.

In 2025, container freight rates volatility—up to a 45% swing year-on-year on some routes—can compress margins on exports like Super Dry.

The company must monitor regional stability and trade policy changes to protect supply chains and maintain profitability on cross-border shipments.

Global Alcohol Taxation Policies

Governments raised excise on alcohol in 2024–25; OECD average beer tax up ~6% YoY, while EU increases pushed retail prices by 3–5%, forcing Asahi to absorb or pass on costs across markets representing ~40% of 2025 revenue. Varying tax regimes complicate pricing and demand elasticity management, with high-tax countries seeing volume declines up to 4–7% annually. Asahi is shifting portfolio toward low-/no-alcohol SKUs—these grew 18% in 2025—to protect market share.

Regulatory Stability in Emerging Markets

Expansion into Southeast Asia exposes Asahi to varying political stability and regulatory transparency across markets like Vietnam, Philippines, Indonesia and Thailand, where the World Bank’s 2023 Governance Indicators show control of corruption scores ranging from -0.12 to 0.45. Sudden shifts in local governance or foreign investment rules—Indonesia revised its negative investment list in 2021 and Indonesia/Philippines saw increased scrutiny in 2023—can threaten infrastructure and JV returns. Maintaining strong local partners and real-time political risk monitoring is essential to safeguard Asahi’s FY2024 CAPEX of JPY ~150bn earmarked for regional growth and protect long-term capital in these high-growth markets.

Government Health Initiatives

Public health mandates to curb alcohol consumption shape Asahi’s product mix and marketing; Japan’s 2019 Healthy Japan 21 targets and rising calls for stricter limits led Asahi to shift toward low-/no-alcohol lines, which grew 14% CAGR in Japan 2020–2024.

Regulatory pressure for advertising limits and mandatory health labels forces changes to communication strategies; in 2024 EU proposals on alcohol labeling prompted Asahi to preemptively reform packaging across 12 markets.

Asahi invests in its Smart Drinking campaign—allocating about JPY 3.2 billion (2023–2024) to responsible-drinking programs—to align with global health policy and protect long-term demand.

- Low/no-alcohol portfolio up 14% CAGR (2020–2024)

- JPY 3.2bn invested in Smart Drinking (2023–2024)

- Packaging changes across 12 markets in response to 2024 EU labeling proposals

Sustainability and Climate Policy

Asahi faces strict EU Green Deal targets—net-zero by 2050 and a 55% emissions cut by 2030—pushing investments in energy efficiency; Asahi Europe reported a 12% reduction in CO2 intensity from 2019–2023 after €120m in sustainability capex.

Compliance with tightened packaging-waste rules and Extended Producer Responsibility is mandatory to retain operating licenses, affecting supply-chain and packaging costs estimated to rise 3–6% across European operations.

Asahi embeds these mandates into strategy to lower legal risk and boost reputation, linking 15% of executive bonuses to sustainability KPIs and targeting 30% recycled PET in bottles by 2027.

- €120m sustainability capex (2019–2023)

- 12% CO2 intensity reduction (2019–2023)

- 3–6% projected packaging cost increase

- 15% exec bonus tied to sustainability

- 30% recycled PET target by 2027

Global costs, shifting demand: 32% intl exposure, tax hikes, CAPEX JPY~150bn

Political risks (trade/tariffs, excise, stability, health regs, sustainability) raised costs and shifted demand: 32% international revenue exposure (2024); OECD beer tax +6% YoY (2024); container rates ±45% (2025); low/no-alcohol sales +18% (2025); JPY 3.2bn responsible-drinking spend (2023–24); FY2024 CAPEX JPY ~150bn.

| Metric | Value |

|---|---|

| Intl revenue exposure (2024) | 32% |

| OECD beer tax change (2024) | +6% YoY |

| Container rate volatility (2025) | ±45% |

| Low/no-alc sales growth (2025) | +18% |

| Responsible-drinking spend (2023–24) | JPY 3.2bn |

| FY2024 CAPEX for regional growth | JPY ~150bn |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact Asahi Group Holdings, linking each dimension to industry-specific trends, regional regulatory dynamics and supply-chain considerations to surface strategic risks and opportunities.

Condensed PESTLE insights for Asahi Group Holdings, arranged by category for quick reference, ideal for slide decks or meeting briefs to support risk discussions and strategic alignment across teams.

Economic factors

Fluctuations in Foreign Exchange Rates

Asahi Group, a Japan-based brewer earning roughly 25-30% of revenue outside Japan (notably Euros and AUD), faces material FX risk as yen moves alter translation of overseas profits and import costs; a 10% yen appreciation in 2022 trimmed reported overseas EBITDA by mid-single digits for peers. The yen's 2023–2025 volatility—ranging ~130–150 JPY/USD—affected raw material import costs and margins. Asahi employs forward contracts and natural hedges, reporting hedged revenues covering a substantial portion of foreign-currency exposure to stabilize results.

Global Inflation and Input Costs

Interest Rate Volatility

Interest rate volatility affects Asahi’s cost of debt and M&A capacity; a 100 bp rise in global rates would increase annual interest expense on ¥200bn net debt by roughly ¥2bn, constraining large-scale acquisitions and capex.

Higher borrowing costs in 2024–25 prompted tighter capex plans and a push to cut net debt from ¥198bn in FY2023 toward targeted leverage ratios, prioritizing deleveraging.

Management tracks BOJ, ECB and Fed moves across Japan, Europe and Australia to optimize capital structure and hedge interest expense.

Economic Growth in Key Markets

The demand for premium beer correlates with disposable income and GDP growth; Japan's 2024 real GDP grew 1.4% while EU GDP grew 0.7% (2024), supporting higher-margin segments.

Economic downturns prompt trade-downs and lower out-of-home spending—Japan's household real disposable income fell 0.8% in 2023 and Euro area consumer confidence remained subdued in 2024.

Asahi's premium positioning boosts resilience—premium brands delivered higher ASPs and margins in 2024—but prolonged stagnation would compress volumes and pricing power.

- Premium demand tied to GDP/disposable income

- Japan/EU slowdowns reduce out-of-home and cause trade-downs

- Asahi benefits from premium ASPs but is vulnerable to prolonged stagnation

Supply Chain Resilience and Logistics Costs

Economic disruptions in global shipping and labor markets raised Asahi Group's logistics costs; container freight rates spiked to peaks above $8,000 per FEU in 2021–22 and remained elevated into 2024, contributing to higher COGS and intermittent product shortages.

Asahi has increased local production—investing in regional breweries and a 2023 EUR 230m upgrade in Europe—to cut transportation spend and exposure to volatile ocean freight.

The company deploys efficient inventory management and multi-sourcing; by 2024, days inventory held rose to ~110 days in some segments to buffer bottlenecks while supplier diversification lowered single-source dependency to under 20%.

- Freight spikes > $8,000/FEU (2021–24)

- EUR 230m Europe production investment (2023)

- Inventory ~110 days in some segments (2024)

- Single-source dependency < 20% (2024)

Asahi hit by FX, input inflation and rate pain—price hikes and deleveraging under way

Asahi faces FX exposure (Yen 130–150/USD in 2023–25) and hedges a large share of foreign revenue; rising input costs—energy +35%, aluminum +22%, barley +18% and hops +15% in 2024—squeezed margins, prompting 3–5% price hikes and cost cuts; higher rates raised interest expense (100bp → ~¥2bn pa on ¥200bn debt), slowing capex and accelerating deleveraging (net debt ¥198bn FY2023).

| Metric | 2024/2025 |

|---|---|

| Yen/USD | 130–150 |

| Energy inflation | +35% |

| Aluminum | +22% |

| Barley | +18% |

| Hops | +15% |

| Price hikes | 3–5% |

| Net debt (FY2023) | ¥198bn |

| Interest sensitivity | 100bp ≈ ¥2bn/yr |

Same Document Delivered

Asahi Group Holdings PESTLE Analysis

The preview shown here is the exact Asahi Group Holdings PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Uncover how political shifts, economic cycles, social trends, and technological change shape Asahi Group Holdings' strategic outlook with our concise PESTLE snapshot—perfect for investors and strategists seeking actionable context. Purchase the full PESTLE for a complete, downloadable analysis with regulatory, environmental, and legal deep dives to inform smarter decisions today.

Political factors

Geopolitical Trade Relations

Asahi Group Holdings operates across Europe, Oceania and Southeast Asia, making it vulnerable to shifting trade agreements and geopolitical tensions that in 2024 affected 32% of its international revenue exposure; tariff changes between Japan and EU/ASEAN partners could raise input costs and logistics expenses.

In 2025, container freight rates volatility—up to a 45% swing year-on-year on some routes—can compress margins on exports like Super Dry.

The company must monitor regional stability and trade policy changes to protect supply chains and maintain profitability on cross-border shipments.

Global Alcohol Taxation Policies

Governments raised excise on alcohol in 2024–25; OECD average beer tax up ~6% YoY, while EU increases pushed retail prices by 3–5%, forcing Asahi to absorb or pass on costs across markets representing ~40% of 2025 revenue. Varying tax regimes complicate pricing and demand elasticity management, with high-tax countries seeing volume declines up to 4–7% annually. Asahi is shifting portfolio toward low-/no-alcohol SKUs—these grew 18% in 2025—to protect market share.

Regulatory Stability in Emerging Markets

Expansion into Southeast Asia exposes Asahi to varying political stability and regulatory transparency across markets like Vietnam, Philippines, Indonesia and Thailand, where the World Bank’s 2023 Governance Indicators show control of corruption scores ranging from -0.12 to 0.45. Sudden shifts in local governance or foreign investment rules—Indonesia revised its negative investment list in 2021 and Indonesia/Philippines saw increased scrutiny in 2023—can threaten infrastructure and JV returns. Maintaining strong local partners and real-time political risk monitoring is essential to safeguard Asahi’s FY2024 CAPEX of JPY ~150bn earmarked for regional growth and protect long-term capital in these high-growth markets.

Government Health Initiatives

Public health mandates to curb alcohol consumption shape Asahi’s product mix and marketing; Japan’s 2019 Healthy Japan 21 targets and rising calls for stricter limits led Asahi to shift toward low-/no-alcohol lines, which grew 14% CAGR in Japan 2020–2024.

Regulatory pressure for advertising limits and mandatory health labels forces changes to communication strategies; in 2024 EU proposals on alcohol labeling prompted Asahi to preemptively reform packaging across 12 markets.

Asahi invests in its Smart Drinking campaign—allocating about JPY 3.2 billion (2023–2024) to responsible-drinking programs—to align with global health policy and protect long-term demand.

- Low/no-alcohol portfolio up 14% CAGR (2020–2024)

- JPY 3.2bn invested in Smart Drinking (2023–2024)

- Packaging changes across 12 markets in response to 2024 EU labeling proposals

Sustainability and Climate Policy

Asahi faces strict EU Green Deal targets—net-zero by 2050 and a 55% emissions cut by 2030—pushing investments in energy efficiency; Asahi Europe reported a 12% reduction in CO2 intensity from 2019–2023 after €120m in sustainability capex.

Compliance with tightened packaging-waste rules and Extended Producer Responsibility is mandatory to retain operating licenses, affecting supply-chain and packaging costs estimated to rise 3–6% across European operations.

Asahi embeds these mandates into strategy to lower legal risk and boost reputation, linking 15% of executive bonuses to sustainability KPIs and targeting 30% recycled PET in bottles by 2027.

- €120m sustainability capex (2019–2023)

- 12% CO2 intensity reduction (2019–2023)

- 3–6% projected packaging cost increase

- 15% exec bonus tied to sustainability

- 30% recycled PET target by 2027

Global costs, shifting demand: 32% intl exposure, tax hikes, CAPEX JPY~150bn

Political risks (trade/tariffs, excise, stability, health regs, sustainability) raised costs and shifted demand: 32% international revenue exposure (2024); OECD beer tax +6% YoY (2024); container rates ±45% (2025); low/no-alcohol sales +18% (2025); JPY 3.2bn responsible-drinking spend (2023–24); FY2024 CAPEX JPY ~150bn.

| Metric | Value |

|---|---|

| Intl revenue exposure (2024) | 32% |

| OECD beer tax change (2024) | +6% YoY |

| Container rate volatility (2025) | ±45% |

| Low/no-alc sales growth (2025) | +18% |

| Responsible-drinking spend (2023–24) | JPY 3.2bn |

| FY2024 CAPEX for regional growth | JPY ~150bn |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact Asahi Group Holdings, linking each dimension to industry-specific trends, regional regulatory dynamics and supply-chain considerations to surface strategic risks and opportunities.

Condensed PESTLE insights for Asahi Group Holdings, arranged by category for quick reference, ideal for slide decks or meeting briefs to support risk discussions and strategic alignment across teams.

Economic factors

Fluctuations in Foreign Exchange Rates

Asahi Group, a Japan-based brewer earning roughly 25-30% of revenue outside Japan (notably Euros and AUD), faces material FX risk as yen moves alter translation of overseas profits and import costs; a 10% yen appreciation in 2022 trimmed reported overseas EBITDA by mid-single digits for peers. The yen's 2023–2025 volatility—ranging ~130–150 JPY/USD—affected raw material import costs and margins. Asahi employs forward contracts and natural hedges, reporting hedged revenues covering a substantial portion of foreign-currency exposure to stabilize results.

Global Inflation and Input Costs

Interest Rate Volatility

Interest rate volatility affects Asahi’s cost of debt and M&A capacity; a 100 bp rise in global rates would increase annual interest expense on ¥200bn net debt by roughly ¥2bn, constraining large-scale acquisitions and capex.

Higher borrowing costs in 2024–25 prompted tighter capex plans and a push to cut net debt from ¥198bn in FY2023 toward targeted leverage ratios, prioritizing deleveraging.

Management tracks BOJ, ECB and Fed moves across Japan, Europe and Australia to optimize capital structure and hedge interest expense.

Economic Growth in Key Markets

The demand for premium beer correlates with disposable income and GDP growth; Japan's 2024 real GDP grew 1.4% while EU GDP grew 0.7% (2024), supporting higher-margin segments.

Economic downturns prompt trade-downs and lower out-of-home spending—Japan's household real disposable income fell 0.8% in 2023 and Euro area consumer confidence remained subdued in 2024.

Asahi's premium positioning boosts resilience—premium brands delivered higher ASPs and margins in 2024—but prolonged stagnation would compress volumes and pricing power.

- Premium demand tied to GDP/disposable income

- Japan/EU slowdowns reduce out-of-home and cause trade-downs

- Asahi benefits from premium ASPs but is vulnerable to prolonged stagnation

Supply Chain Resilience and Logistics Costs

Economic disruptions in global shipping and labor markets raised Asahi Group's logistics costs; container freight rates spiked to peaks above $8,000 per FEU in 2021–22 and remained elevated into 2024, contributing to higher COGS and intermittent product shortages.

Asahi has increased local production—investing in regional breweries and a 2023 EUR 230m upgrade in Europe—to cut transportation spend and exposure to volatile ocean freight.

The company deploys efficient inventory management and multi-sourcing; by 2024, days inventory held rose to ~110 days in some segments to buffer bottlenecks while supplier diversification lowered single-source dependency to under 20%.

- Freight spikes > $8,000/FEU (2021–24)

- EUR 230m Europe production investment (2023)

- Inventory ~110 days in some segments (2024)

- Single-source dependency < 20% (2024)

Asahi hit by FX, input inflation and rate pain—price hikes and deleveraging under way

Asahi faces FX exposure (Yen 130–150/USD in 2023–25) and hedges a large share of foreign revenue; rising input costs—energy +35%, aluminum +22%, barley +18% and hops +15% in 2024—squeezed margins, prompting 3–5% price hikes and cost cuts; higher rates raised interest expense (100bp → ~¥2bn pa on ¥200bn debt), slowing capex and accelerating deleveraging (net debt ¥198bn FY2023).

| Metric | 2024/2025 |

|---|---|

| Yen/USD | 130–150 |

| Energy inflation | +35% |

| Aluminum | +22% |

| Barley | +18% |

| Hops | +15% |

| Price hikes | 3–5% |

| Net debt (FY2023) | ¥198bn |

| Interest sensitivity | 100bp ≈ ¥2bn/yr |

Same Document Delivered

Asahi Group Holdings PESTLE Analysis

The preview shown here is the exact Asahi Group Holdings PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.