Asbury Automotive Group Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

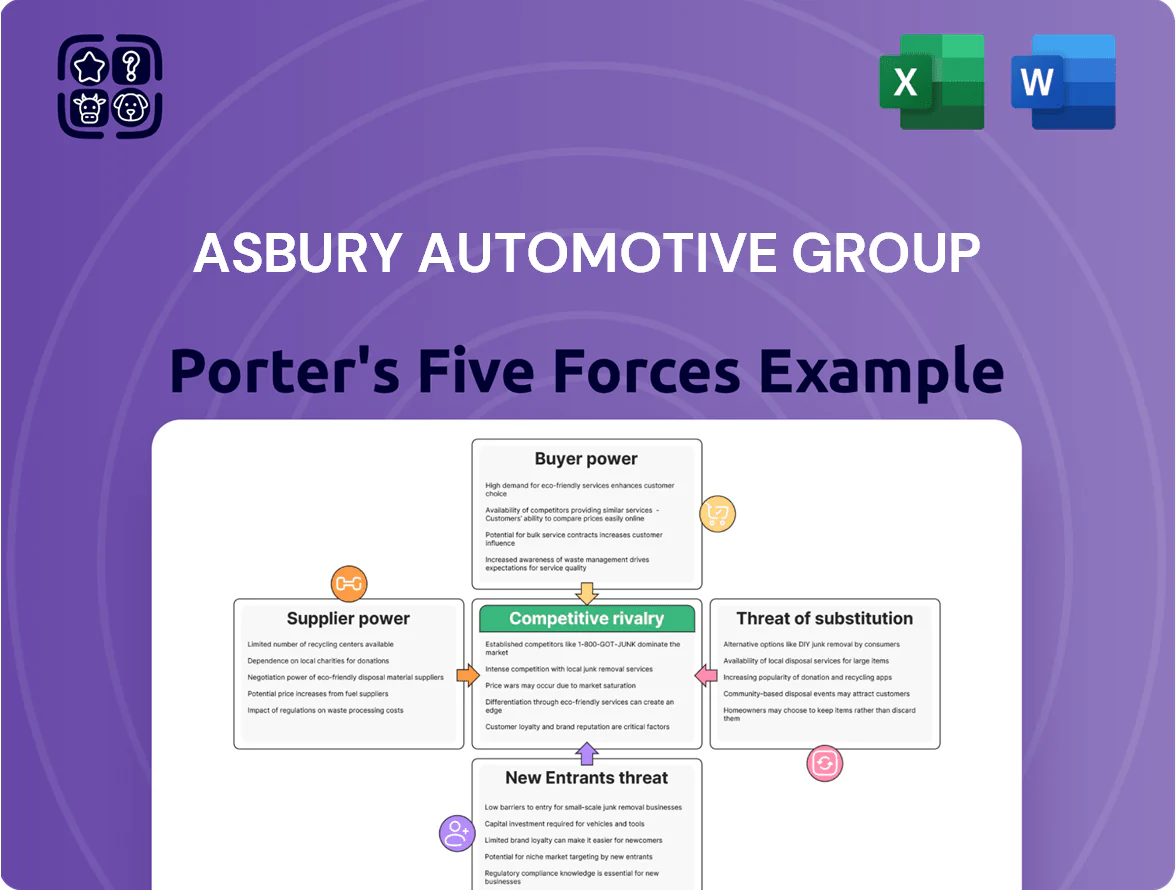

Asbury Automotive Group faces moderate buyer power, intense competition among dealerships, and evolving substitute threats from online retail and subscription models, while supplier influence and entry barriers shape margins and scale advantages.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Asbury Automotive Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

OEM Concentration and Influence

Major OEMs—Toyota, Honda, Ford—hold leverage by controlling top-selling models; Toyota sold 8.6M vehicles globally in 2024, so Asbury’s new-vehicle mix depends on OEM allocations and model availability.

Asbury’s inventory and margins fluctuate with OEM production schedules; in 2024 dealer vehicle shortages raised wholesale prices 18%, squeezing dealer gross profit.

By late 2025 EVs amplify supplier power: OEMs impose dealership EV infrastructure requirements and charging targets; Cox Automotive reported 42% of franchised dealers lacked full EV readiness in 2024.

Franchise Agreement Constraints

Inventory Allocation Systems

Manufacturers set algorithmic inventory allocation using dealership performance and regional sales; Asbury’s access to high-margin SUVs/trucks is therefore partly controlled by suppliers, constraining revenue upside.

In 2024–2025 logistics volatility—chip shortages easing but transport delays up 12% in 2024—boosted OEM leverage, with top 5 automakers allocating 18–25% of limited SUV/truck units to higher-performing dealers.

Certified Parts Monopolies

Asbury depends on OEM-certified parts and proprietary diagnostic software for its high-margin service and repair business; OEMs therefore exert price-setting power because using genuine parts is often required to preserve manufacturer warranties.

In 2024 Asbury reported parts and service gross profit of $1.1 billion, so OEM pricing policies directly influence a material slice of service margins and cost of goods sold.

- OEMs control certified parts and software

- Warranties force use of genuine parts

- 2024 parts & service GP: $1.1B

- Supplier pricing limits Asbury margin upside

Tiered Incentive Structures

Tiered incentives from manufacturers supply a large share of dealership profits—manufacturer holdbacks, dealer incentives, and volume bonuses accounted for about 18–22% of U.S. franchise dealer gross profit in 2024, letting suppliers steer Asbury toward specific SKUs and CSI (customer satisfaction index) targets.

This financial entanglement gives manufacturers indirect control over Asbury’s stocking, marketing, and staffing priorities, since missing volume thresholds can cut bonuses materially (often 1–3% of unit price).

- 18–22% dealer gross from OEM incentives (2024)

- Bonuses tied to volume/CSI often 1–3% per unit

- Incentives shift Asbury promotions and inventory mix

OEMs Dictate Margins & Access: Toyota Scale, Heavy Incentives, Asbury Capex Strain

Suppliers (OEMs) hold high bargaining power: they control allocations, parts/software, and incentives—Toyota sold 8.6M vehicles in 2024, OEM incentives made 18–22% of dealer gross in 2024, and Asbury’s parts & service GP was $1.1B (2024), forcing capex (Asbury capex $312M, 2024) and constraining access to high-margin SUVs/trucks.

| Metric | 2024 value |

|---|---|

| Toyota global sales | 8.6M |

| OEM incentive share of dealer gross | 18–22% |

| Asbury parts & service GP | $1.1B |

| Asbury capex (PPE additions) | $312M |

What is included in the product

Tailored Porter's Five Forces analysis for Asbury Automotive Group, uncovering competitive drivers, buyer/supplier power, entry barriers, substitutes, and disruptive threats to inform strategic positioning and profitability.

Compact Porter's Five Forces summary tailored to Asbury Automotive Group—quickly spot supplier, buyer, and competitive pressures to guide dealership strategy and M&A decisions.

Customers Bargaining Power

Digital Price Transparency

By late 2025, online comparison tools covering 90% of US metro markets give buyers real-time pricing, invoice figures, dealer incentives, and trade-in estimates; customers now enter Asbury Automotive Group (NYSE: ABG) negotiations knowing competitor discounts and regional MSRP spreads. This information symmetry compresses margins—new-vehicle gross profit per unit fell industry-wide from $1,200 in 2019 to ~$820 in 2024—and forces Asbury to fight on price rather than upsell services.

Low Switching Costs

Consumers face minimal financial hurdles to switch dealerships—average US new-vehicle transaction fees are under $1,000 and 2024 Kelley Blue Book data shows 68% of buyers cite price/finance over brand when choosing a dealer.

Many brands now match features and reliability; JD Power 2024 reported only a 12-point gap in initial quality across top brands, so loyalty yields to price and terms.

Asbury must boost service, digital sales, and captive finance offers—its 2024 net income margin of 3.1% means small price moves can hurt, so experience retention is vital.

Financing Independence

Information Access via Vehicle History

Information access via vehicle history reports (Carfax, AutoCheck) lets buyers verify accidents, title issues, and odometer records, reducing asymmetric information and pressuring Asbury Automotive Group to back used-car pricing with documentation and reconditioning proof.

Transparency caps Asbury’s ability to charge premiums; industry data show 72% of used-buyers cite history reports as purchase drivers (2024 Cox Automotive), enabling customers to demand discounts for even minor flaws.

- 72% buyers use reports (Cox 2024)

- Accident/clean-title splits shift price by 5–12%

- Proof of reconditioning raises sale price, lack of it forces concessions

Service Department Alternatives

Customers can choose independent shops and national chains like Midas or Firestone; 2024 U.S. independent repair shops performed ~70% of non-warranty maintenance, cutting into dealership share.

Once vehicles exit warranty (typically 3–5 years), consumers shop for lower labor rates—dealer average labor rate in 2024 was ~$120/hour vs independent ~$90/hour—shifting bargaining power to buyers.

Asbury must prove higher premiums via tech and convenience—digital service scheduling, OEM parts availability, and 1–2 hour express lanes—to retain a mobile customer base.

- Independent shops do ~70% non-warranty work

- Dealer labor ~$120/hr vs independent ~$90/hr (2024)

- Warranty drop at 3–5 years tilts power to consumers

- Asbury needs tech + convenience to justify premiums

Buyers' leverage soars: price tools, fintech loans, and service options force price play

Buyers hold strong leverage: real-time price tools cover ~90% US metros (2025), new-vehicle gross profit/unit fell to ~$820 (2024), fintech auto-loans hit 22% of originations (2024), and 72% of used buyers use history reports (Cox 2024); low switch costs and independent service share (~70% non-warranty work) force Asbury to compete on price, service convenience, and preapproved finance matching.

| Metric | Value |

|---|---|

| Price-tool coverage | ~90% (2025) |

| New-vehicle GP/unit | ~$820 (2024) |

| Fintech loan share | 22% (2024) |

| Used buyers using reports | 72% (Cox 2024) |

| Independent non-warranty work | ~70% (2024) |

Preview the Actual Deliverable

Asbury Automotive Group Porter's Five Forces Analysis

This preview shows the exact Asbury Automotive Group Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders, no mockups, fully formatted and ready for use. The document covers supplier and buyer power, competitive rivalry, threat of new entrants, and substitutes with data-backed insights and strategic implications. Purchase grants instant access to this identical, professionally written file.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Asbury Automotive Group faces moderate buyer power, intense competition among dealerships, and evolving substitute threats from online retail and subscription models, while supplier influence and entry barriers shape margins and scale advantages.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Asbury Automotive Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

OEM Concentration and Influence

Major OEMs—Toyota, Honda, Ford—hold leverage by controlling top-selling models; Toyota sold 8.6M vehicles globally in 2024, so Asbury’s new-vehicle mix depends on OEM allocations and model availability.

Asbury’s inventory and margins fluctuate with OEM production schedules; in 2024 dealer vehicle shortages raised wholesale prices 18%, squeezing dealer gross profit.

By late 2025 EVs amplify supplier power: OEMs impose dealership EV infrastructure requirements and charging targets; Cox Automotive reported 42% of franchised dealers lacked full EV readiness in 2024.

Franchise Agreement Constraints

Inventory Allocation Systems

Manufacturers set algorithmic inventory allocation using dealership performance and regional sales; Asbury’s access to high-margin SUVs/trucks is therefore partly controlled by suppliers, constraining revenue upside.

In 2024–2025 logistics volatility—chip shortages easing but transport delays up 12% in 2024—boosted OEM leverage, with top 5 automakers allocating 18–25% of limited SUV/truck units to higher-performing dealers.

Certified Parts Monopolies

Asbury depends on OEM-certified parts and proprietary diagnostic software for its high-margin service and repair business; OEMs therefore exert price-setting power because using genuine parts is often required to preserve manufacturer warranties.

In 2024 Asbury reported parts and service gross profit of $1.1 billion, so OEM pricing policies directly influence a material slice of service margins and cost of goods sold.

- OEMs control certified parts and software

- Warranties force use of genuine parts

- 2024 parts & service GP: $1.1B

- Supplier pricing limits Asbury margin upside

Tiered Incentive Structures

Tiered incentives from manufacturers supply a large share of dealership profits—manufacturer holdbacks, dealer incentives, and volume bonuses accounted for about 18–22% of U.S. franchise dealer gross profit in 2024, letting suppliers steer Asbury toward specific SKUs and CSI (customer satisfaction index) targets.

This financial entanglement gives manufacturers indirect control over Asbury’s stocking, marketing, and staffing priorities, since missing volume thresholds can cut bonuses materially (often 1–3% of unit price).

- 18–22% dealer gross from OEM incentives (2024)

- Bonuses tied to volume/CSI often 1–3% per unit

- Incentives shift Asbury promotions and inventory mix

OEMs Dictate Margins & Access: Toyota Scale, Heavy Incentives, Asbury Capex Strain

Suppliers (OEMs) hold high bargaining power: they control allocations, parts/software, and incentives—Toyota sold 8.6M vehicles in 2024, OEM incentives made 18–22% of dealer gross in 2024, and Asbury’s parts & service GP was $1.1B (2024), forcing capex (Asbury capex $312M, 2024) and constraining access to high-margin SUVs/trucks.

| Metric | 2024 value |

|---|---|

| Toyota global sales | 8.6M |

| OEM incentive share of dealer gross | 18–22% |

| Asbury parts & service GP | $1.1B |

| Asbury capex (PPE additions) | $312M |

What is included in the product

Tailored Porter's Five Forces analysis for Asbury Automotive Group, uncovering competitive drivers, buyer/supplier power, entry barriers, substitutes, and disruptive threats to inform strategic positioning and profitability.

Compact Porter's Five Forces summary tailored to Asbury Automotive Group—quickly spot supplier, buyer, and competitive pressures to guide dealership strategy and M&A decisions.

Customers Bargaining Power

Digital Price Transparency

By late 2025, online comparison tools covering 90% of US metro markets give buyers real-time pricing, invoice figures, dealer incentives, and trade-in estimates; customers now enter Asbury Automotive Group (NYSE: ABG) negotiations knowing competitor discounts and regional MSRP spreads. This information symmetry compresses margins—new-vehicle gross profit per unit fell industry-wide from $1,200 in 2019 to ~$820 in 2024—and forces Asbury to fight on price rather than upsell services.

Low Switching Costs

Consumers face minimal financial hurdles to switch dealerships—average US new-vehicle transaction fees are under $1,000 and 2024 Kelley Blue Book data shows 68% of buyers cite price/finance over brand when choosing a dealer.

Many brands now match features and reliability; JD Power 2024 reported only a 12-point gap in initial quality across top brands, so loyalty yields to price and terms.

Asbury must boost service, digital sales, and captive finance offers—its 2024 net income margin of 3.1% means small price moves can hurt, so experience retention is vital.

Financing Independence

Information Access via Vehicle History

Information access via vehicle history reports (Carfax, AutoCheck) lets buyers verify accidents, title issues, and odometer records, reducing asymmetric information and pressuring Asbury Automotive Group to back used-car pricing with documentation and reconditioning proof.

Transparency caps Asbury’s ability to charge premiums; industry data show 72% of used-buyers cite history reports as purchase drivers (2024 Cox Automotive), enabling customers to demand discounts for even minor flaws.

- 72% buyers use reports (Cox 2024)

- Accident/clean-title splits shift price by 5–12%

- Proof of reconditioning raises sale price, lack of it forces concessions

Service Department Alternatives

Customers can choose independent shops and national chains like Midas or Firestone; 2024 U.S. independent repair shops performed ~70% of non-warranty maintenance, cutting into dealership share.

Once vehicles exit warranty (typically 3–5 years), consumers shop for lower labor rates—dealer average labor rate in 2024 was ~$120/hour vs independent ~$90/hour—shifting bargaining power to buyers.

Asbury must prove higher premiums via tech and convenience—digital service scheduling, OEM parts availability, and 1–2 hour express lanes—to retain a mobile customer base.

- Independent shops do ~70% non-warranty work

- Dealer labor ~$120/hr vs independent ~$90/hr (2024)

- Warranty drop at 3–5 years tilts power to consumers

- Asbury needs tech + convenience to justify premiums

Buyers' leverage soars: price tools, fintech loans, and service options force price play

Buyers hold strong leverage: real-time price tools cover ~90% US metros (2025), new-vehicle gross profit/unit fell to ~$820 (2024), fintech auto-loans hit 22% of originations (2024), and 72% of used buyers use history reports (Cox 2024); low switch costs and independent service share (~70% non-warranty work) force Asbury to compete on price, service convenience, and preapproved finance matching.

| Metric | Value |

|---|---|

| Price-tool coverage | ~90% (2025) |

| New-vehicle GP/unit | ~$820 (2024) |

| Fintech loan share | 22% (2024) |

| Used buyers using reports | 72% (Cox 2024) |

| Independent non-warranty work | ~70% (2024) |

Preview the Actual Deliverable

Asbury Automotive Group Porter's Five Forces Analysis

This preview shows the exact Asbury Automotive Group Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders, no mockups, fully formatted and ready for use. The document covers supplier and buyer power, competitive rivalry, threat of new entrants, and substitutes with data-backed insights and strategic implications. Purchase grants instant access to this identical, professionally written file.