Ascendis Health Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

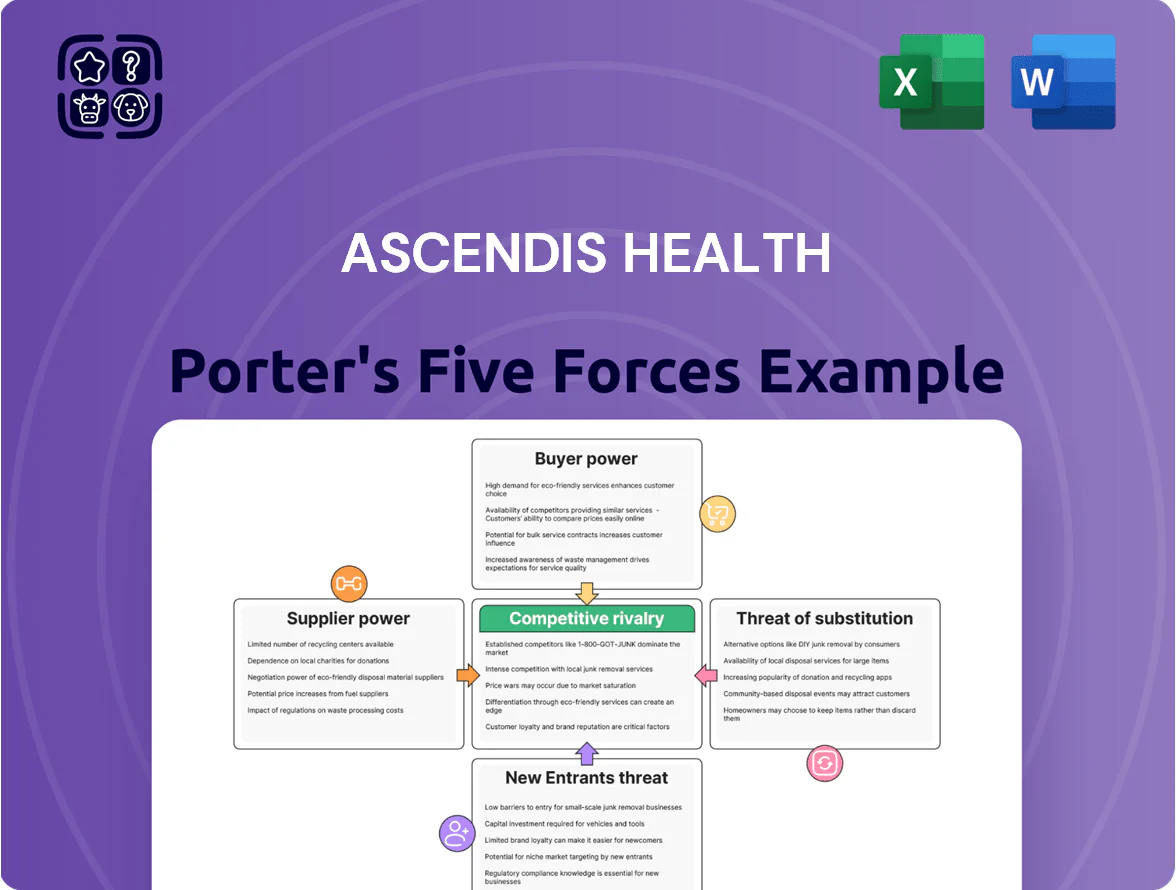

Ascendis Health faces moderate buyer power and high competitive rivalry as it navigates price-sensitive payers and rapid biotech innovation, while supplier leverage and regulatory hurdles add measurable strain; substitutes and new entrants pose evolving threats tied to novel therapies and partnerships.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Ascendis Health’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of API Manufacturers

Ascendis Health depends on a small set of API manufacturers, mainly in India and China, sourcing over 70% of key active ingredients from these regions as of 2025; that concentration raises supply risk.

Disruptions or export curbs in those countries or a 10–25% raw-material price swing seen in 2023–24 could raise COGS materially.

With few certified vendors for some inputs, Ascendis has limited price leverage and faces supplier-driven margin pressure.

Regulatory Compliance Standards

Suppliers must meet strict South African Health Products Regulatory Authority (SAHPRA) and WHO Good Manufacturing Practice standards, shrinking eligible vendors and raising supplier leverage over Ascendis Health.

Compliance reduces supplier pool by an estimated 40–60% in pharma sectors; certified suppliers charge 5–15% premiums for proven quality and traceability.

Switching costs are high: re‑certification audits take 6–12 months and can cost $50k–$200k, entrenching compliant suppliers’ bargaining power.

Impact of Currency Volatility

Because Ascendis Health imports key active pharmaceutical ingredients, supplier power rises as the South African Rand fell about 14% vs the US Dollar in 2023–2024, forcing suppliers to pass FX costs through price increases of 8–12% on average.

Specialized Ingredient Scarcity

Suppliers of proprietary or seasonally limited ingredients for Ascendis Healths consumer and animal health divisions command strong leverage; few alternatives match required efficacy, letting suppliers set prices and 8–14 week lead times during peak demand.

This concentrated sourcing risk contributed to a 2024 COGS uptick of ~6% year-over-year in the consumer segment and forced spot purchases that raised input costs by ~10% in Q3 2024.

- Limited vendors: top 3 suppliers supply >70% of niche inputs

- Lead times: typical 8–14 weeks, extendable to 20+ weeks

- Price impact: spot premiums ~10% during 2024 peaks

- Operational risk: 6% rise in consumer COGS in 2024

Logistical Integration Costs

- High setup cost: USD 5–15m

- Delivery cost uplift: 20–30%

- Supplier price premium: 3–7%

- Rely on cold-chain capacity for biologics

Supplier squeeze: Top-3 >70% share, certification costs and FX lift COGS +6% in 2024

Ascendis Health faces high supplier power: top 3 vendors supply >70% of niche APIs, certified suppliers charge 5–15% premiums, and re‑certification takes 6–12 months costing $50k–$200k, raising switching costs; FX moves (Rand −14% vs USD in 2023–24) and 8–14 week lead times pushed 2024 consumer COGS +6% and spot premiums ~10%.

| Metric | Value |

|---|---|

| Top-3 supplier share | >70% |

| Certified supplier premium | 5–15% |

| Re-certification time/cost | 6–12 months / $50k–$200k |

| Rand vs USD (2023–24) | ≈−14% |

| 2024 consumer COGS change | +6% |

| Spot premium 2024 peaks | ~10% |

What is included in the product

Tailored Porter's Five Forces for Ascendis Health analyzing competitive rivalry, supplier and buyer power, threat of substitutes and new entrants, and identifying disruptive threats and protective market dynamics to inform strategic positioning and valuation.

A concise Porter's Five Forces snapshot for Ascendis Health—quickly gauge competitive pressure and strategic risks to guide M&A, pricing, and expansion decisions.

Customers Bargaining Power

Dominance of Retail Pharmacy Chains

Major retail groups Clicks Group (3 2024 stores) and Dis-Chem (pre-IPO 170+ stores by 2024) dominate South Africa’s pharmacy retail, giving them strong leverage to demand discounts up to mid‑teens percent and extended payment terms in vendor reports; shelf placement and promo support are routinely traded for price concessions.

Ascendis Health must balance margin pressure with access—losing prime shelf space would cut mass‑market reach for brands that drove R3.2bn revenue in 2024—so contract negotiations and targeted co‑funded promotions are critical.

State Procurement and Tenders

The South African government buys pharma via large public-health tenders and accounted for about 40% of national medicine spend in 2024, giving it strong bargaining power to push prices down on bulk contracts.

Because tenders award large volumes, buyers can demand steep discounts; public-sector pricing pressure compressed margins across local suppliers to single-digit EBITDA in 2024.

Losing one major government contract can cut a pharma division’s revenue by 10–30% depending on product mix—so Ascendis Health faces high revenue concentration risk from state procurement.

Private Hospital Group Influence

Large private hospital groups like Netcare and Mediclinic use centralized procurement to secure bulk discounts, cutting supplier margins; in 2024 Netcare’s group purchasing reportedly reduced drug spend by ~12% year-on-year, pressuring makers such as Ascendis.

The hospitals’ ability to switch to generics and local suppliers raises buyer power: Mediclinic's tender wins show generic substitution rates above 30% in key therapeutic classes, intensifying price competition for Ascendis.

Low Consumer Switching Costs

In consumer health, brand loyalty often yields to price and availability, so customers switch vitamins or supplements freely with no financial or functional penalty.

This forces Ascendis Health to spend on marketing and competitive pricing; global supplement sales hit $155bn in 2024 and US retail price promotions rose 12% YoY, pressuring margins.

- Low switching costs → higher churn

- 2024 global supplement market $155bn

- US promo intensity +12% YoY (2024)

- Requires sustained marketing spend, margin compression

Price Sensitivity in Local Markets

Rising inflation and 2024 real wage declines in South Africa pushed households toward cheaper healthcare; generics now account for ~60% of private-sector volumes, increasing price pressure on Ascendis Health.

Buyers compare prices online and through pharmacies; 2025 surveys show 47% of patients prioritize cost over brand, so manufacturers must prove quality to keep premiums.

Manufacturers face margin squeeze: a 5–8% average price discount by retailers in 2024 forced tighter gross margins across the sector.

- Generics ~60% of private volumes

- 47% of patients prioritize cost (2025 survey)

- Retailer discounts 5–8% in 2024

Retailer leverage forces Ascendis into margin trade‑offs: discounts, promos, shelf access

Major retailers (Clicks ~3650 stores 2024; Dis-Chem 170+ by 2024) and public tenders (~40% of medicine spend 2024) give buyers high leverage, forcing mid‑teens discounts, 5–8% retailer price cuts (2024) and margin squeeze; generics ~60% private volumes and 47% of patients prioritize cost (2025), so Ascendis must trade margin for shelf access and co‑funded promos.

| Metric | 2024/25 |

|---|---|

| Retailer stores | Clicks 3650; Dis‑Chem 170+ |

| Public spend | ~40% |

| Retailer discounts | 5–8% |

| Generics share | ~60% |

| Cost‑first patients | 47% (2025) |

Preview the Actual Deliverable

Ascendis Health Porter's Five Forces Analysis

This preview shows the exact Ascendis Health Porter’s Five Forces analysis you'll receive after purchase—no placeholders or mockups. It is the professionally written, fully formatted document ready for immediate download and use the moment you buy. The content covers competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry with actionable insights. What you see is what you get—instantly accessible upon payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Ascendis Health faces moderate buyer power and high competitive rivalry as it navigates price-sensitive payers and rapid biotech innovation, while supplier leverage and regulatory hurdles add measurable strain; substitutes and new entrants pose evolving threats tied to novel therapies and partnerships.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Ascendis Health’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of API Manufacturers

Ascendis Health depends on a small set of API manufacturers, mainly in India and China, sourcing over 70% of key active ingredients from these regions as of 2025; that concentration raises supply risk.

Disruptions or export curbs in those countries or a 10–25% raw-material price swing seen in 2023–24 could raise COGS materially.

With few certified vendors for some inputs, Ascendis has limited price leverage and faces supplier-driven margin pressure.

Regulatory Compliance Standards

Suppliers must meet strict South African Health Products Regulatory Authority (SAHPRA) and WHO Good Manufacturing Practice standards, shrinking eligible vendors and raising supplier leverage over Ascendis Health.

Compliance reduces supplier pool by an estimated 40–60% in pharma sectors; certified suppliers charge 5–15% premiums for proven quality and traceability.

Switching costs are high: re‑certification audits take 6–12 months and can cost $50k–$200k, entrenching compliant suppliers’ bargaining power.

Impact of Currency Volatility

Because Ascendis Health imports key active pharmaceutical ingredients, supplier power rises as the South African Rand fell about 14% vs the US Dollar in 2023–2024, forcing suppliers to pass FX costs through price increases of 8–12% on average.

Specialized Ingredient Scarcity

Suppliers of proprietary or seasonally limited ingredients for Ascendis Healths consumer and animal health divisions command strong leverage; few alternatives match required efficacy, letting suppliers set prices and 8–14 week lead times during peak demand.

This concentrated sourcing risk contributed to a 2024 COGS uptick of ~6% year-over-year in the consumer segment and forced spot purchases that raised input costs by ~10% in Q3 2024.

- Limited vendors: top 3 suppliers supply >70% of niche inputs

- Lead times: typical 8–14 weeks, extendable to 20+ weeks

- Price impact: spot premiums ~10% during 2024 peaks

- Operational risk: 6% rise in consumer COGS in 2024

Logistical Integration Costs

- High setup cost: USD 5–15m

- Delivery cost uplift: 20–30%

- Supplier price premium: 3–7%

- Rely on cold-chain capacity for biologics

Supplier squeeze: Top-3 >70% share, certification costs and FX lift COGS +6% in 2024

Ascendis Health faces high supplier power: top 3 vendors supply >70% of niche APIs, certified suppliers charge 5–15% premiums, and re‑certification takes 6–12 months costing $50k–$200k, raising switching costs; FX moves (Rand −14% vs USD in 2023–24) and 8–14 week lead times pushed 2024 consumer COGS +6% and spot premiums ~10%.

| Metric | Value |

|---|---|

| Top-3 supplier share | >70% |

| Certified supplier premium | 5–15% |

| Re-certification time/cost | 6–12 months / $50k–$200k |

| Rand vs USD (2023–24) | ≈−14% |

| 2024 consumer COGS change | +6% |

| Spot premium 2024 peaks | ~10% |

What is included in the product

Tailored Porter's Five Forces for Ascendis Health analyzing competitive rivalry, supplier and buyer power, threat of substitutes and new entrants, and identifying disruptive threats and protective market dynamics to inform strategic positioning and valuation.

A concise Porter's Five Forces snapshot for Ascendis Health—quickly gauge competitive pressure and strategic risks to guide M&A, pricing, and expansion decisions.

Customers Bargaining Power

Dominance of Retail Pharmacy Chains

Major retail groups Clicks Group (3 2024 stores) and Dis-Chem (pre-IPO 170+ stores by 2024) dominate South Africa’s pharmacy retail, giving them strong leverage to demand discounts up to mid‑teens percent and extended payment terms in vendor reports; shelf placement and promo support are routinely traded for price concessions.

Ascendis Health must balance margin pressure with access—losing prime shelf space would cut mass‑market reach for brands that drove R3.2bn revenue in 2024—so contract negotiations and targeted co‑funded promotions are critical.

State Procurement and Tenders

The South African government buys pharma via large public-health tenders and accounted for about 40% of national medicine spend in 2024, giving it strong bargaining power to push prices down on bulk contracts.

Because tenders award large volumes, buyers can demand steep discounts; public-sector pricing pressure compressed margins across local suppliers to single-digit EBITDA in 2024.

Losing one major government contract can cut a pharma division’s revenue by 10–30% depending on product mix—so Ascendis Health faces high revenue concentration risk from state procurement.

Private Hospital Group Influence

Large private hospital groups like Netcare and Mediclinic use centralized procurement to secure bulk discounts, cutting supplier margins; in 2024 Netcare’s group purchasing reportedly reduced drug spend by ~12% year-on-year, pressuring makers such as Ascendis.

The hospitals’ ability to switch to generics and local suppliers raises buyer power: Mediclinic's tender wins show generic substitution rates above 30% in key therapeutic classes, intensifying price competition for Ascendis.

Low Consumer Switching Costs

In consumer health, brand loyalty often yields to price and availability, so customers switch vitamins or supplements freely with no financial or functional penalty.

This forces Ascendis Health to spend on marketing and competitive pricing; global supplement sales hit $155bn in 2024 and US retail price promotions rose 12% YoY, pressuring margins.

- Low switching costs → higher churn

- 2024 global supplement market $155bn

- US promo intensity +12% YoY (2024)

- Requires sustained marketing spend, margin compression

Price Sensitivity in Local Markets

Rising inflation and 2024 real wage declines in South Africa pushed households toward cheaper healthcare; generics now account for ~60% of private-sector volumes, increasing price pressure on Ascendis Health.

Buyers compare prices online and through pharmacies; 2025 surveys show 47% of patients prioritize cost over brand, so manufacturers must prove quality to keep premiums.

Manufacturers face margin squeeze: a 5–8% average price discount by retailers in 2024 forced tighter gross margins across the sector.

- Generics ~60% of private volumes

- 47% of patients prioritize cost (2025 survey)

- Retailer discounts 5–8% in 2024

Retailer leverage forces Ascendis into margin trade‑offs: discounts, promos, shelf access

Major retailers (Clicks ~3650 stores 2024; Dis-Chem 170+ by 2024) and public tenders (~40% of medicine spend 2024) give buyers high leverage, forcing mid‑teens discounts, 5–8% retailer price cuts (2024) and margin squeeze; generics ~60% private volumes and 47% of patients prioritize cost (2025), so Ascendis must trade margin for shelf access and co‑funded promos.

| Metric | 2024/25 |

|---|---|

| Retailer stores | Clicks 3650; Dis‑Chem 170+ |

| Public spend | ~40% |

| Retailer discounts | 5–8% |

| Generics share | ~60% |

| Cost‑first patients | 47% (2025) |

Preview the Actual Deliverable

Ascendis Health Porter's Five Forces Analysis

This preview shows the exact Ascendis Health Porter’s Five Forces analysis you'll receive after purchase—no placeholders or mockups. It is the professionally written, fully formatted document ready for immediate download and use the moment you buy. The content covers competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry with actionable insights. What you see is what you get—instantly accessible upon payment.