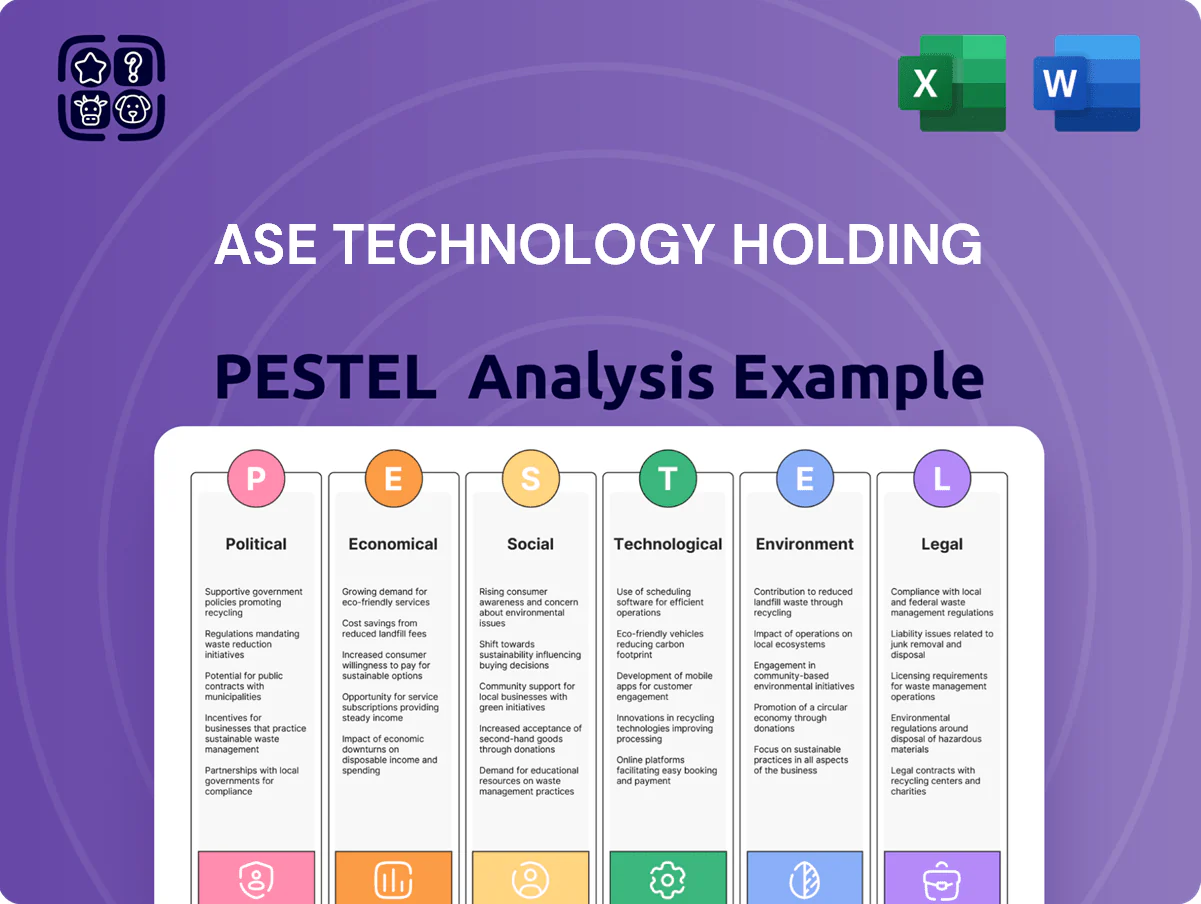

ASE Technology Holding PESTLE Analysis

Your Competitive Advantage Starts with This Report

Gain a strategic advantage with our PESTLE Analysis of ASE Technology Holding—uncover how political shifts, economic cycles, social trends, technological advances, legal risks, and environmental pressures shape the company’s prospects; buy the full report to access actionable insights, ready-to-use slides, and data-driven recommendations for investors and strategists.

Political factors

Geopolitical Trade Restrictions

The US-China trade tensions have led to tighter export controls on advanced semiconductor equipment, with US Entity List actions cutting chip-tool supply by an estimated 15-20% to China in 2023–24; ASE Technology Holding must ensure compliance across its $14.5B 2024 revenue base while serving clients in US, China and Taiwan. ASE is diversifying manufacturing footprint—shifting higher-margin advanced packaging work to Taiwan and Singapore—to reduce sanction exposure and sustain its global customer mix.

Taiwan Strait Stability

As a Taiwan-headquartered company, ASE faces direct exposure to cross-strait dynamics; in 2024 Taiwan accounted for over 60% of global semiconductor front-end and back-end capacity, amplifying risk to ASE’s assembly and test operations.

Escalation in tensions could interrupt the global supply chain—Taiwan’s semiconductor exports were valued at about $125 billion in 2024—risking order delays and revenue volatility for ASE.

By late 2025 investors and management emphasize geographic diversification: ASE expanded non-Taiwan capacity to roughly 30% of throughput and increased business continuity reserves equivalent to several months of operating cash flow.

Government Incentive Programs

The proliferation of semiconductor-focused laws like the US CHIPS Act (authorizing $280B nationwide, $52B for chips) and EU Chips Act (EUR 43B mobilization) creates material subsidy opportunities for ASE Technology Holding to fund regional expansion; ASE has signaled facility investments outside Taiwan to align with host-country domestic supply‑chain aims. Capturing incentives is critical to offsetting labor and capex differentials—e.g., US/EU incentives can cover significant portions of new-plant capex and OPEX in high-cost regions.

Supply Chain Regionalization Trends

Political pressure for supply chain resilience is shifting firms from global efficiency to regional security; ASE is expanding in Southeast Asia, adding capacity in Malaysia and Vietnam to offer China Plus One options amid 2024–25 reshoring incentives.

These moves align with Western clients' mandates to cut single-source risk—ASE reported Southeast Asia revenue growth of about 12% YoY in 2024 as regional capacity investments rose to roughly $400–500m.

- ASE expanding Malaysia, Vietnam capacity

- ~12% Southeast Asia revenue growth in 2024

- $400–500m regional investment through 2024–25

- Supports Western clients’ China Plus One political requirements

Regulatory Oversight on Dual-Use Tech

Rising political scrutiny of dual-use tech—up 28% in export-control actions globally from 2021–2024—forces ASE to tighten vetting for HPC chip packaging and testing to avoid links to restricted military programs.

These compliance costs, estimated at ~0.4–0.7% of revenue for comparable EMS firms, require ASE to coordinate continuously with Wassenaar Arrangement members and OFAC/EU trade authorities to preserve market access.

- Export-control actions +28% (2021–2024)

- Compliance burden ~0.4–0.7% of revenue

- Ongoing coordination: Wassenaar, OFAC, EU authorities

ASE pivots supply chain: Taiwan-centric to SE Asia amid US chip-tool curbs

US export controls cut chip-tool supply to China ~15–20% (2023–24); ASE must comply across $14.5B 2024 revenue while shifting advanced packaging to Taiwan/Singapore and expanding Malaysia/Vietnam (30% non-Taiwan throughput by 2025). Taiwan accounted for ~60%+ capacity; ASE SE Asia revenue +12% in 2024 with $400–500m investment; compliance costs ~0.4–0.7% of revenue.

| Metric | Value |

|---|---|

| 2024 Revenue | $14.5B |

| China tool supply drop | 15–20% |

| SE Asia rev growth 2024 | +12% |

| Regional investment | $400–500m |

| Compliance cost | 0.4–0.7% rev |

What is included in the product

Explores how macro-environmental factors uniquely affect ASE Technology Holding across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights tailored to support executives, investors, and strategists in identifying risks, opportunities, and actionable scenarios.

A concise, visually segmented ASE Technology Holding PESTLE summary that fits into presentations and strategy packs, enabling quick alignment across teams and streamlined risk discussions during planning sessions.

Economic factors

AI-Driven Demand Surge

The exponential growth of generative AI and high-performance computing is a key economic driver for ASE through 2026, with the global AI chip market forecasted to exceed $200 billion by 2026, boosting demand for advanced packaging. ASE is pivoting to 2.5D and 3D IC solutions that carry higher gross margins—often 5–10 percentage points above legacy wire-bonding—supporting a shift in revenue mix toward premium segments. This shift helps offset single-digit growth in traditional consumer electronics, with ASE reporting rising ASPs and a growing share of advanced packaging in its 2024–25 revenue mix.

Global Inflation and Operating Costs

Persistent inflationary pressures—energy up ~8% yoy in 2024 and semiconductor-grade chemical prices rising ~12%—have compressed ASE Technology Holding’s gross margin, with reported 2024 H1 gross margin at 12.4% vs 14.1% in 2023 H1.

ASE accelerates automated smart-factory rollout (targeting >30% lines by 2026) and lean initiatives to cut unit costs, yielding a reported ~4% YoY improvement in manufacturing efficiency in 2024.

ASE has modestly increased end-customer pricing, contributing to a 3–5% realized price uplift in 2024, but intense OSAT competition and ~3% industry overcapacity cap pricing power and margin recovery.

Currency Exchange Rate Volatility

ASE operates in a multi-currency environment, making its financial performance sensitive to fluctuations between the New Taiwan Dollar and the US Dollar; in 2024 a 1 NT$/USD move altered reported operating margins by roughly 0.4 percentage points. A significant portion of revenue is USD-denominated while many costs remain NT$, so exchange shifts can produce sizable non-operating gains or losses—ASE reported NT$3.2 billion FX gains in 2023. The company employs forward contracts and options as sophisticated hedges to manage translation and transaction risk, helping stabilize quarterly earnings volatility.

Capital Expenditure Intensity

ASE faces high capital expenditure intensity as the semiconductor sector demands continual investment to follow Moore's Law and advanced packaging; in 2024 ASE invested about $1.2 billion in CAPEX and R&D, balancing growth with profitability.

Economic cycles dictate CAPEX timing, and ASE is prioritizing capacity expansions for silicon photonics and co-packaged optics to capture rising demand, while managing leverage and shareholder returns.

- 2024 CAPEX ≈ $1.2B; R&D significant

- Focus: silicon photonics, co-packaged optics capacity

- Investment timing tied to economic cycles and demand

- Balance CAPEX with healthy balance sheet and returns

Cyclicality of Consumer Electronics

Despite AI growth, ~40% of ASE Technology Holding’s revenue in 2024 remained linked to smartphones, PCs and wearables; these segments are highly cyclical and sensitive to consumer spending shifts.

Economic downturns lowered utilization of ASE’s testing and packaging lines to ~75% in mid-2023 from >90% during 2021 peaks, directly pressuring margins.

Diversification into automotive and industrial (accounting for ~28% of 2024 revenue) provides a hedge, with automotive packaging demand growing ~12% YoY in 2024.

- ~40% revenue from consumer electronics (2024)

- Utilization fell to ~75% in 2023

- Automotive/industrial ~28% of revenue (2024)

- Automotive packaging +12% YoY (2024)

ASE's 2.5D/3D push taps $200B+ AI chip boom, boosting ASPs and auto/industrial growth

ASE's advanced-packaging pivot (2.5D/3D) rides AI/HPC demand—AI chip market >$200B by 2026—boosting ASPs and margins; 2024 advanced-packaging share rose, offsetting single-digit consumer declines. 2024 CAPEX ≈ $1.2B; gross margin 12.4% H1 2024 vs 14.1% H1 2023 due to energy (+8%) and chemical (+12%) inflation; utilization ~75% mid-2023; automotive/industrial ≈28% revenue (+12% YoY).

| Metric | 2024 |

|---|---|

| CAPEX | $1.2B |

| Gross margin H1 | 12.4% |

| Utilization | ~75% |

| Auto/Industrial rev | 28% |

What You See Is What You Get

ASE Technology Holding PESTLE Analysis

The preview shown here is the exact PESTLE analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for ASE Technology Holding.

No placeholders or teasers: the content, layout, and insights visible now are the final file you’ll download immediately after payment.

Everything displayed is part of the finished product, providing a complete political, economic, social, technological, legal, and environmental assessment for decision-making.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Gain a strategic advantage with our PESTLE Analysis of ASE Technology Holding—uncover how political shifts, economic cycles, social trends, technological advances, legal risks, and environmental pressures shape the company’s prospects; buy the full report to access actionable insights, ready-to-use slides, and data-driven recommendations for investors and strategists.

Political factors

Geopolitical Trade Restrictions

The US-China trade tensions have led to tighter export controls on advanced semiconductor equipment, with US Entity List actions cutting chip-tool supply by an estimated 15-20% to China in 2023–24; ASE Technology Holding must ensure compliance across its $14.5B 2024 revenue base while serving clients in US, China and Taiwan. ASE is diversifying manufacturing footprint—shifting higher-margin advanced packaging work to Taiwan and Singapore—to reduce sanction exposure and sustain its global customer mix.

Taiwan Strait Stability

As a Taiwan-headquartered company, ASE faces direct exposure to cross-strait dynamics; in 2024 Taiwan accounted for over 60% of global semiconductor front-end and back-end capacity, amplifying risk to ASE’s assembly and test operations.

Escalation in tensions could interrupt the global supply chain—Taiwan’s semiconductor exports were valued at about $125 billion in 2024—risking order delays and revenue volatility for ASE.

By late 2025 investors and management emphasize geographic diversification: ASE expanded non-Taiwan capacity to roughly 30% of throughput and increased business continuity reserves equivalent to several months of operating cash flow.

Government Incentive Programs

The proliferation of semiconductor-focused laws like the US CHIPS Act (authorizing $280B nationwide, $52B for chips) and EU Chips Act (EUR 43B mobilization) creates material subsidy opportunities for ASE Technology Holding to fund regional expansion; ASE has signaled facility investments outside Taiwan to align with host-country domestic supply‑chain aims. Capturing incentives is critical to offsetting labor and capex differentials—e.g., US/EU incentives can cover significant portions of new-plant capex and OPEX in high-cost regions.

Supply Chain Regionalization Trends

Political pressure for supply chain resilience is shifting firms from global efficiency to regional security; ASE is expanding in Southeast Asia, adding capacity in Malaysia and Vietnam to offer China Plus One options amid 2024–25 reshoring incentives.

These moves align with Western clients' mandates to cut single-source risk—ASE reported Southeast Asia revenue growth of about 12% YoY in 2024 as regional capacity investments rose to roughly $400–500m.

- ASE expanding Malaysia, Vietnam capacity

- ~12% Southeast Asia revenue growth in 2024

- $400–500m regional investment through 2024–25

- Supports Western clients’ China Plus One political requirements

Regulatory Oversight on Dual-Use Tech

Rising political scrutiny of dual-use tech—up 28% in export-control actions globally from 2021–2024—forces ASE to tighten vetting for HPC chip packaging and testing to avoid links to restricted military programs.

These compliance costs, estimated at ~0.4–0.7% of revenue for comparable EMS firms, require ASE to coordinate continuously with Wassenaar Arrangement members and OFAC/EU trade authorities to preserve market access.

- Export-control actions +28% (2021–2024)

- Compliance burden ~0.4–0.7% of revenue

- Ongoing coordination: Wassenaar, OFAC, EU authorities

ASE pivots supply chain: Taiwan-centric to SE Asia amid US chip-tool curbs

US export controls cut chip-tool supply to China ~15–20% (2023–24); ASE must comply across $14.5B 2024 revenue while shifting advanced packaging to Taiwan/Singapore and expanding Malaysia/Vietnam (30% non-Taiwan throughput by 2025). Taiwan accounted for ~60%+ capacity; ASE SE Asia revenue +12% in 2024 with $400–500m investment; compliance costs ~0.4–0.7% of revenue.

| Metric | Value |

|---|---|

| 2024 Revenue | $14.5B |

| China tool supply drop | 15–20% |

| SE Asia rev growth 2024 | +12% |

| Regional investment | $400–500m |

| Compliance cost | 0.4–0.7% rev |

What is included in the product

Explores how macro-environmental factors uniquely affect ASE Technology Holding across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights tailored to support executives, investors, and strategists in identifying risks, opportunities, and actionable scenarios.

A concise, visually segmented ASE Technology Holding PESTLE summary that fits into presentations and strategy packs, enabling quick alignment across teams and streamlined risk discussions during planning sessions.

Economic factors

AI-Driven Demand Surge

The exponential growth of generative AI and high-performance computing is a key economic driver for ASE through 2026, with the global AI chip market forecasted to exceed $200 billion by 2026, boosting demand for advanced packaging. ASE is pivoting to 2.5D and 3D IC solutions that carry higher gross margins—often 5–10 percentage points above legacy wire-bonding—supporting a shift in revenue mix toward premium segments. This shift helps offset single-digit growth in traditional consumer electronics, with ASE reporting rising ASPs and a growing share of advanced packaging in its 2024–25 revenue mix.

Global Inflation and Operating Costs

Persistent inflationary pressures—energy up ~8% yoy in 2024 and semiconductor-grade chemical prices rising ~12%—have compressed ASE Technology Holding’s gross margin, with reported 2024 H1 gross margin at 12.4% vs 14.1% in 2023 H1.

ASE accelerates automated smart-factory rollout (targeting >30% lines by 2026) and lean initiatives to cut unit costs, yielding a reported ~4% YoY improvement in manufacturing efficiency in 2024.

ASE has modestly increased end-customer pricing, contributing to a 3–5% realized price uplift in 2024, but intense OSAT competition and ~3% industry overcapacity cap pricing power and margin recovery.

Currency Exchange Rate Volatility

ASE operates in a multi-currency environment, making its financial performance sensitive to fluctuations between the New Taiwan Dollar and the US Dollar; in 2024 a 1 NT$/USD move altered reported operating margins by roughly 0.4 percentage points. A significant portion of revenue is USD-denominated while many costs remain NT$, so exchange shifts can produce sizable non-operating gains or losses—ASE reported NT$3.2 billion FX gains in 2023. The company employs forward contracts and options as sophisticated hedges to manage translation and transaction risk, helping stabilize quarterly earnings volatility.

Capital Expenditure Intensity

ASE faces high capital expenditure intensity as the semiconductor sector demands continual investment to follow Moore's Law and advanced packaging; in 2024 ASE invested about $1.2 billion in CAPEX and R&D, balancing growth with profitability.

Economic cycles dictate CAPEX timing, and ASE is prioritizing capacity expansions for silicon photonics and co-packaged optics to capture rising demand, while managing leverage and shareholder returns.

- 2024 CAPEX ≈ $1.2B; R&D significant

- Focus: silicon photonics, co-packaged optics capacity

- Investment timing tied to economic cycles and demand

- Balance CAPEX with healthy balance sheet and returns

Cyclicality of Consumer Electronics

Despite AI growth, ~40% of ASE Technology Holding’s revenue in 2024 remained linked to smartphones, PCs and wearables; these segments are highly cyclical and sensitive to consumer spending shifts.

Economic downturns lowered utilization of ASE’s testing and packaging lines to ~75% in mid-2023 from >90% during 2021 peaks, directly pressuring margins.

Diversification into automotive and industrial (accounting for ~28% of 2024 revenue) provides a hedge, with automotive packaging demand growing ~12% YoY in 2024.

- ~40% revenue from consumer electronics (2024)

- Utilization fell to ~75% in 2023

- Automotive/industrial ~28% of revenue (2024)

- Automotive packaging +12% YoY (2024)

ASE's 2.5D/3D push taps $200B+ AI chip boom, boosting ASPs and auto/industrial growth

ASE's advanced-packaging pivot (2.5D/3D) rides AI/HPC demand—AI chip market >$200B by 2026—boosting ASPs and margins; 2024 advanced-packaging share rose, offsetting single-digit consumer declines. 2024 CAPEX ≈ $1.2B; gross margin 12.4% H1 2024 vs 14.1% H1 2023 due to energy (+8%) and chemical (+12%) inflation; utilization ~75% mid-2023; automotive/industrial ≈28% revenue (+12% YoY).

| Metric | 2024 |

|---|---|

| CAPEX | $1.2B |

| Gross margin H1 | 12.4% |

| Utilization | ~75% |

| Auto/Industrial rev | 28% |

What You See Is What You Get

ASE Technology Holding PESTLE Analysis

The preview shown here is the exact PESTLE analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for ASE Technology Holding.

No placeholders or teasers: the content, layout, and insights visible now are the final file you’ll download immediately after payment.

Everything displayed is part of the finished product, providing a complete political, economic, social, technological, legal, and environmental assessment for decision-making.