AsiaInfo Technologies Boston Consulting Group Matrix

Download Your Competitive Advantage

AsiaInfo Technologies sits at an inflection point—some product lines exhibit strong market share in growing segments while others risk becoming resource drains as competition intensifies; our preview highlights key trends and likely quadrant shifts. Dive deeper into this company’s BCG Matrix and gain a clear view of where its products stand—Stars, Cash Cows, Dogs, or Question Marks. Purchase the full version for a complete breakdown, quadrant-by-quadrant recommendations, and ready-to-use Word and Excel deliverables to guide strategic allocation and investment decisions.

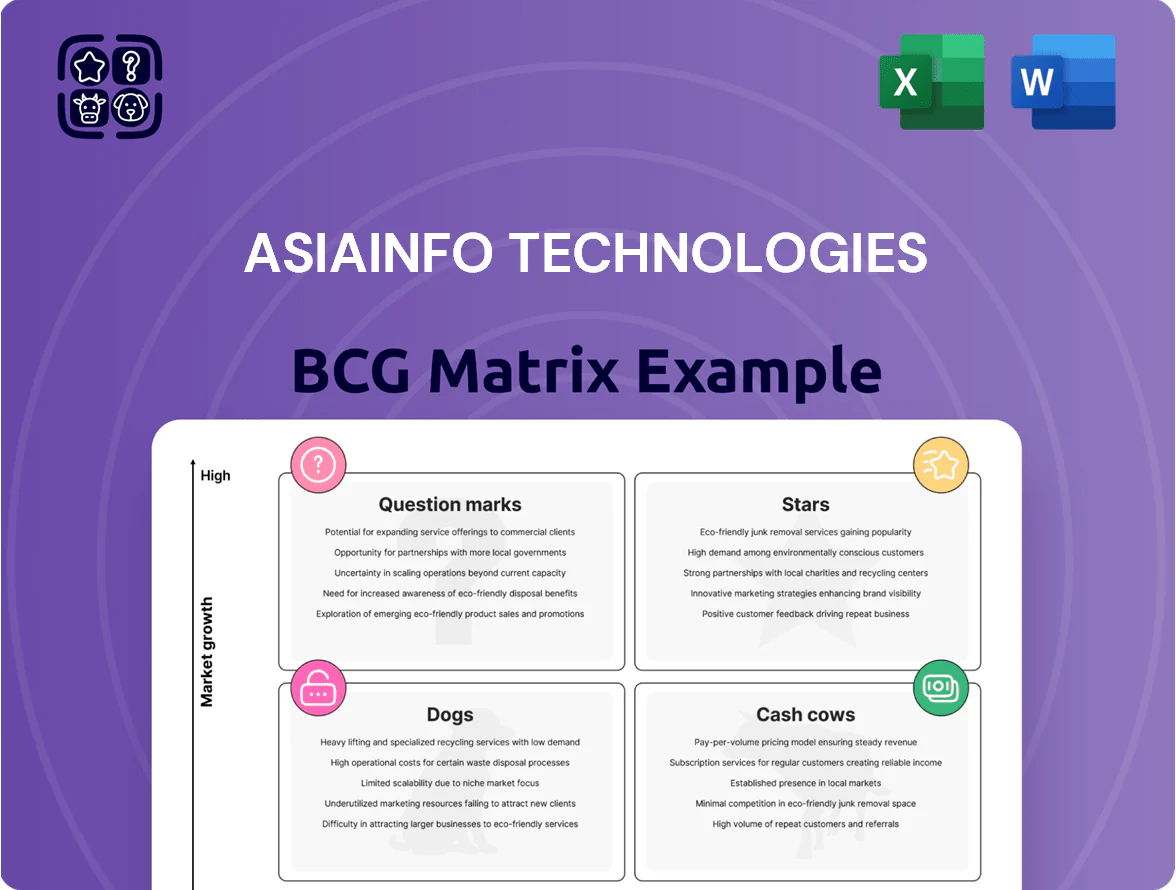

Stars

AI Large Model Application and Delivery

AI Large Model Application and Delivery surged in 2025, with revenue and orders up >70x year-on-year by mid-2025, driving roughly RMB 1.2 billion in bookings H1 2025 and contributing ~35% of AsiaInfo Technologiesʼ incremental revenue.

As a first-to-market leader in industrial large model solutions across China, AsiaInfo captures AI-native transformation demand from telcos and enterprises, but its R&D spend rose ~4x in 2025 to protect the tech lead.

Despite heavy capex, this segment is the companyʼs top high-growth engine, projected to deliver 40–60% CAGR through 2027 under current contracts and pilot-to-production conversion rates near 30% by Q3 2025.

5G Private Network Solutions

AsiaInfo leads in customized 5G private networks for nuclear, wind, and mining, with H1 2025 orders up over 50% year‑on‑year, driven by a >30% market share in China’s industrial private 5G segment (estimated RMB 18–22 billion TAM in 2025).

Cloud-Network Integration Products

The Cloud-Network product system, covering 5G network intelligence and autonomous network suites, is a high-growth leader as carriers shift to 5G-Advanced; AsiaInfo reported a 28% YoY uplift in cloud-network revenue in FY2024, driven by new operator contracts in China and Southeast Asia.

New client acquisitions rose 35% in 2024, reflecting demand for complex compute and network orchestration; the segment holds ~45% domestic market share but requires ongoing R&D spend—AsiaInfo increased cloud-network R&D by 22% in 2024 to sustain innovation.

Digital Intelligence-Driven Operations

Digital Intelligence-Driven Operations targets automotive, finance, and consumer sectors with advanced data governance and algorithm-based services and in 2025 shifted strongly to results- and commission-based pricing, which now exceed one-third (≈35%) of BU revenue, driving higher gross margins.

Its non-telecom client mix—40% automotive, 35% finance, 25% consumer—makes it a star in AsiaInfo’s BCG Matrix, diversifying the firm’s legacy telecom income and delivering 22% YoY revenue growth in 2025.

- Results/commission revenue ≈35% of BU sales in 2025

- 2025 YoY revenue growth 22%

- Client mix: 40% auto, 35% finance, 25% consumer

- Higher gross margins vs legacy services; key growth engine

Vertical Industry Digitization

By leveraging deep domain skills in finance and energy, AsiaInfo drove double-digit order growth in vertical industry digital transformation, with finance orders up nearly 50% in 2025, making AsiaInfo a primary enterprise digitalization partner.

The vertical industry segment is capturing share in the fast-growing enterprise software market and needs steady promotion and placement support to sustain momentum and margin expansion.

- Double-digit total order growth (2025)

- Finance orders +~50% in 2025

- Energy sector strong pipeline

- Needs ongoing GTM and placement support

AsiaInfo surges: AI bookings RMB1.2bn H1’25, Cloud‑Network +28%, Digital Ops +22%

AsiaInfo’s Stars: AI Large Model, Cloud‑Network, and Digital Intelligence drove rapid growth—AI bookings ~RMB1.2bn H1 2025 (+70x YoY), segment CAGR 40–60% to 2027; Cloud‑Network revenue +28% YoY FY2024, 45% domestic share; Digital Ops revenue +22% YoY 2025 with 35% commission-based sales.

| Metric | 2024/25 |

|---|---|

| AI bookings H1 2025 | RMB1.2bn |

| AI YoY growth | ~70x |

| Cloud‑Network rev YoY | +28% |

| Digital Ops rev YoY | +22% |

| Commission sales | 35% |

What is included in the product

Comprehensive BCG Matrix review of AsiaInfo’s units with strategic moves—invest, hold, or divest—plus competitive and market trend context.

One-page BCG Matrix placing AsiaInfo business units in quadrants for quick C-level decisions and printable A4/PDF sharing

Cash Cows

Business Support Systems (BSS)

Business Support Systems (BSS) remains AsiaInfo Technologies’ cash cow, holding ~45% share of China’s OSS/BSS market in 2024 and generating ~RMB 3.2 bn operating cash flow in FY2024 despite revenue decline from operator cost cuts.

High gross margins (~38% in FY2024) keep BSS highly profitable; AsiaInfo plows this steady cash into AI and 5G R&D, funding ~RMB 800 mn of capex and new-product investment in 2024.

Legacy Operations Support Systems (OSS)

AsiaInfo Technologies’ Legacy Operations Support Systems (OSS) are a mature market leader, serving major APAC telcos with tools for network management and maintenance; in 2024 OSS accounted for roughly 28% of group revenue (~RMB 1.1bn / USD 150m) and maintained ~85% gross renewal rates.

Growth in legacy OSS slowed to low single digits in 2023–24, but multi-year contracts and entrenched deployments yield predictable, passive cash flows, supporting EBITDA margins near 22% for the segment.

Minimal incremental capex is needed for baseline upkeep, so management can reliably milk OSS cash to fund R&D and cloud/AI initiatives where they budgeted ~RMB 400m (2024) for innovation.

Telecom ICT Support Services

Maintaining a leading market share in telecom ICT support, AsiaInfo Technologies’ support services powered ~38% of Chinese operator OSS/BSS contracts in 2024, providing the backbone for operator efficiency and customer management.

Despite a 2025 cyclical downturn—operator capex down ~8% year-on-year—this unit stayed profitable, with a 2024 adjusted EBIT margin near 15% from mature cost controls and multi-year SLAs.

It reliably generated operating cash flow covering >100% of group SG&A in 2024 and funded dividends, contributing roughly RMB 420–480 million in free cash flow that underpins shareholder payouts.

Standard Software Product Licensing

AsiaInfo’s middleware and database licenses serve a mature telecom market with high entry barriers; in 2024 they accounted for roughly 34% of software revenue and sustained gross margins near 68% on recurring license and renewal fees.

Low ongoing promotion and 85%+ renewal rates keep CAC modest and these products contributed an estimated CNY 620 million to net operating cash flow in FY2024, making them stable cash cows.

- Mature market, high barriers to entry

- ~34% of software revenue (2024)

- ~68% gross margin on licenses

- ~85% renewal rate; CNY 620M operating cash (FY2024)

Managed Maintenance and Professional Services

Managed maintenance and professional services for AsiaInfo Technologies deliver steady, high-margin recurring revenue—about RMB 3.2 billion in 2024 services revenue (≈28% of group revenue)—with low growth, making them a classic cash cow that funds debt servicing and dividends.

These contracts drive client retention and operational stability with minimal marketing or R&D spend, keeping EBITDA margins near 28% and free cash flow positive.

- 2024 services revenue ~RMB 3.2B

- ~28% of group revenue

- EBITDA margin ~28%

- Low growth, high cash conversion

AsiaInfo’s OSS/BSS cash cow: 45% share, RMB3.2bn cash, funding AI/5G R&D

BSS/OSS services are AsiaInfo’s cash cows: ~45% OSS/BSS market share, ~RMB 3.2bn operating cash flow (FY2024), ~38% gross margin for BSS, OSS ≈RMB 1.1bn (28% revenue) with ~85% renewal, services revenue ≈RMB 3.2bn (28% group) and EBITDA ~28%—funding AI/5G R&D (~RMB 800m) and dividends.

| Metric | 2024 |

|---|---|

| Operating cash | RMB 3.2bn |

| Market share | 45% |

| Gross margin (BSS) | 38% |

| Services rev | RMB 3.2bn |

Full Transparency, Always

AsiaInfo Technologies BCG Matrix

The file you're previewing is the exact AsiaInfo Technologies BCG Matrix report you'll receive after purchase—no watermarks, no placeholders—just a fully formatted, analysis-ready document designed for strategic clarity and professional presentation.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Download Your Competitive Advantage

AsiaInfo Technologies sits at an inflection point—some product lines exhibit strong market share in growing segments while others risk becoming resource drains as competition intensifies; our preview highlights key trends and likely quadrant shifts. Dive deeper into this company’s BCG Matrix and gain a clear view of where its products stand—Stars, Cash Cows, Dogs, or Question Marks. Purchase the full version for a complete breakdown, quadrant-by-quadrant recommendations, and ready-to-use Word and Excel deliverables to guide strategic allocation and investment decisions.

Stars

AI Large Model Application and Delivery

AI Large Model Application and Delivery surged in 2025, with revenue and orders up >70x year-on-year by mid-2025, driving roughly RMB 1.2 billion in bookings H1 2025 and contributing ~35% of AsiaInfo Technologiesʼ incremental revenue.

As a first-to-market leader in industrial large model solutions across China, AsiaInfo captures AI-native transformation demand from telcos and enterprises, but its R&D spend rose ~4x in 2025 to protect the tech lead.

Despite heavy capex, this segment is the companyʼs top high-growth engine, projected to deliver 40–60% CAGR through 2027 under current contracts and pilot-to-production conversion rates near 30% by Q3 2025.

5G Private Network Solutions

AsiaInfo leads in customized 5G private networks for nuclear, wind, and mining, with H1 2025 orders up over 50% year‑on‑year, driven by a >30% market share in China’s industrial private 5G segment (estimated RMB 18–22 billion TAM in 2025).

Cloud-Network Integration Products

The Cloud-Network product system, covering 5G network intelligence and autonomous network suites, is a high-growth leader as carriers shift to 5G-Advanced; AsiaInfo reported a 28% YoY uplift in cloud-network revenue in FY2024, driven by new operator contracts in China and Southeast Asia.

New client acquisitions rose 35% in 2024, reflecting demand for complex compute and network orchestration; the segment holds ~45% domestic market share but requires ongoing R&D spend—AsiaInfo increased cloud-network R&D by 22% in 2024 to sustain innovation.

Digital Intelligence-Driven Operations

Digital Intelligence-Driven Operations targets automotive, finance, and consumer sectors with advanced data governance and algorithm-based services and in 2025 shifted strongly to results- and commission-based pricing, which now exceed one-third (≈35%) of BU revenue, driving higher gross margins.

Its non-telecom client mix—40% automotive, 35% finance, 25% consumer—makes it a star in AsiaInfo’s BCG Matrix, diversifying the firm’s legacy telecom income and delivering 22% YoY revenue growth in 2025.

- Results/commission revenue ≈35% of BU sales in 2025

- 2025 YoY revenue growth 22%

- Client mix: 40% auto, 35% finance, 25% consumer

- Higher gross margins vs legacy services; key growth engine

Vertical Industry Digitization

By leveraging deep domain skills in finance and energy, AsiaInfo drove double-digit order growth in vertical industry digital transformation, with finance orders up nearly 50% in 2025, making AsiaInfo a primary enterprise digitalization partner.

The vertical industry segment is capturing share in the fast-growing enterprise software market and needs steady promotion and placement support to sustain momentum and margin expansion.

- Double-digit total order growth (2025)

- Finance orders +~50% in 2025

- Energy sector strong pipeline

- Needs ongoing GTM and placement support

AsiaInfo surges: AI bookings RMB1.2bn H1’25, Cloud‑Network +28%, Digital Ops +22%

AsiaInfo’s Stars: AI Large Model, Cloud‑Network, and Digital Intelligence drove rapid growth—AI bookings ~RMB1.2bn H1 2025 (+70x YoY), segment CAGR 40–60% to 2027; Cloud‑Network revenue +28% YoY FY2024, 45% domestic share; Digital Ops revenue +22% YoY 2025 with 35% commission-based sales.

| Metric | 2024/25 |

|---|---|

| AI bookings H1 2025 | RMB1.2bn |

| AI YoY growth | ~70x |

| Cloud‑Network rev YoY | +28% |

| Digital Ops rev YoY | +22% |

| Commission sales | 35% |

What is included in the product

Comprehensive BCG Matrix review of AsiaInfo’s units with strategic moves—invest, hold, or divest—plus competitive and market trend context.

One-page BCG Matrix placing AsiaInfo business units in quadrants for quick C-level decisions and printable A4/PDF sharing

Cash Cows

Business Support Systems (BSS)

Business Support Systems (BSS) remains AsiaInfo Technologies’ cash cow, holding ~45% share of China’s OSS/BSS market in 2024 and generating ~RMB 3.2 bn operating cash flow in FY2024 despite revenue decline from operator cost cuts.

High gross margins (~38% in FY2024) keep BSS highly profitable; AsiaInfo plows this steady cash into AI and 5G R&D, funding ~RMB 800 mn of capex and new-product investment in 2024.

Legacy Operations Support Systems (OSS)

AsiaInfo Technologies’ Legacy Operations Support Systems (OSS) are a mature market leader, serving major APAC telcos with tools for network management and maintenance; in 2024 OSS accounted for roughly 28% of group revenue (~RMB 1.1bn / USD 150m) and maintained ~85% gross renewal rates.

Growth in legacy OSS slowed to low single digits in 2023–24, but multi-year contracts and entrenched deployments yield predictable, passive cash flows, supporting EBITDA margins near 22% for the segment.

Minimal incremental capex is needed for baseline upkeep, so management can reliably milk OSS cash to fund R&D and cloud/AI initiatives where they budgeted ~RMB 400m (2024) for innovation.

Telecom ICT Support Services

Maintaining a leading market share in telecom ICT support, AsiaInfo Technologies’ support services powered ~38% of Chinese operator OSS/BSS contracts in 2024, providing the backbone for operator efficiency and customer management.

Despite a 2025 cyclical downturn—operator capex down ~8% year-on-year—this unit stayed profitable, with a 2024 adjusted EBIT margin near 15% from mature cost controls and multi-year SLAs.

It reliably generated operating cash flow covering >100% of group SG&A in 2024 and funded dividends, contributing roughly RMB 420–480 million in free cash flow that underpins shareholder payouts.

Standard Software Product Licensing

AsiaInfo’s middleware and database licenses serve a mature telecom market with high entry barriers; in 2024 they accounted for roughly 34% of software revenue and sustained gross margins near 68% on recurring license and renewal fees.

Low ongoing promotion and 85%+ renewal rates keep CAC modest and these products contributed an estimated CNY 620 million to net operating cash flow in FY2024, making them stable cash cows.

- Mature market, high barriers to entry

- ~34% of software revenue (2024)

- ~68% gross margin on licenses

- ~85% renewal rate; CNY 620M operating cash (FY2024)

Managed Maintenance and Professional Services

Managed maintenance and professional services for AsiaInfo Technologies deliver steady, high-margin recurring revenue—about RMB 3.2 billion in 2024 services revenue (≈28% of group revenue)—with low growth, making them a classic cash cow that funds debt servicing and dividends.

These contracts drive client retention and operational stability with minimal marketing or R&D spend, keeping EBITDA margins near 28% and free cash flow positive.

- 2024 services revenue ~RMB 3.2B

- ~28% of group revenue

- EBITDA margin ~28%

- Low growth, high cash conversion

AsiaInfo’s OSS/BSS cash cow: 45% share, RMB3.2bn cash, funding AI/5G R&D

BSS/OSS services are AsiaInfo’s cash cows: ~45% OSS/BSS market share, ~RMB 3.2bn operating cash flow (FY2024), ~38% gross margin for BSS, OSS ≈RMB 1.1bn (28% revenue) with ~85% renewal, services revenue ≈RMB 3.2bn (28% group) and EBITDA ~28%—funding AI/5G R&D (~RMB 800m) and dividends.

| Metric | 2024 |

|---|---|

| Operating cash | RMB 3.2bn |

| Market share | 45% |

| Gross margin (BSS) | 38% |

| Services rev | RMB 3.2bn |

Full Transparency, Always

AsiaInfo Technologies BCG Matrix

The file you're previewing is the exact AsiaInfo Technologies BCG Matrix report you'll receive after purchase—no watermarks, no placeholders—just a fully formatted, analysis-ready document designed for strategic clarity and professional presentation.