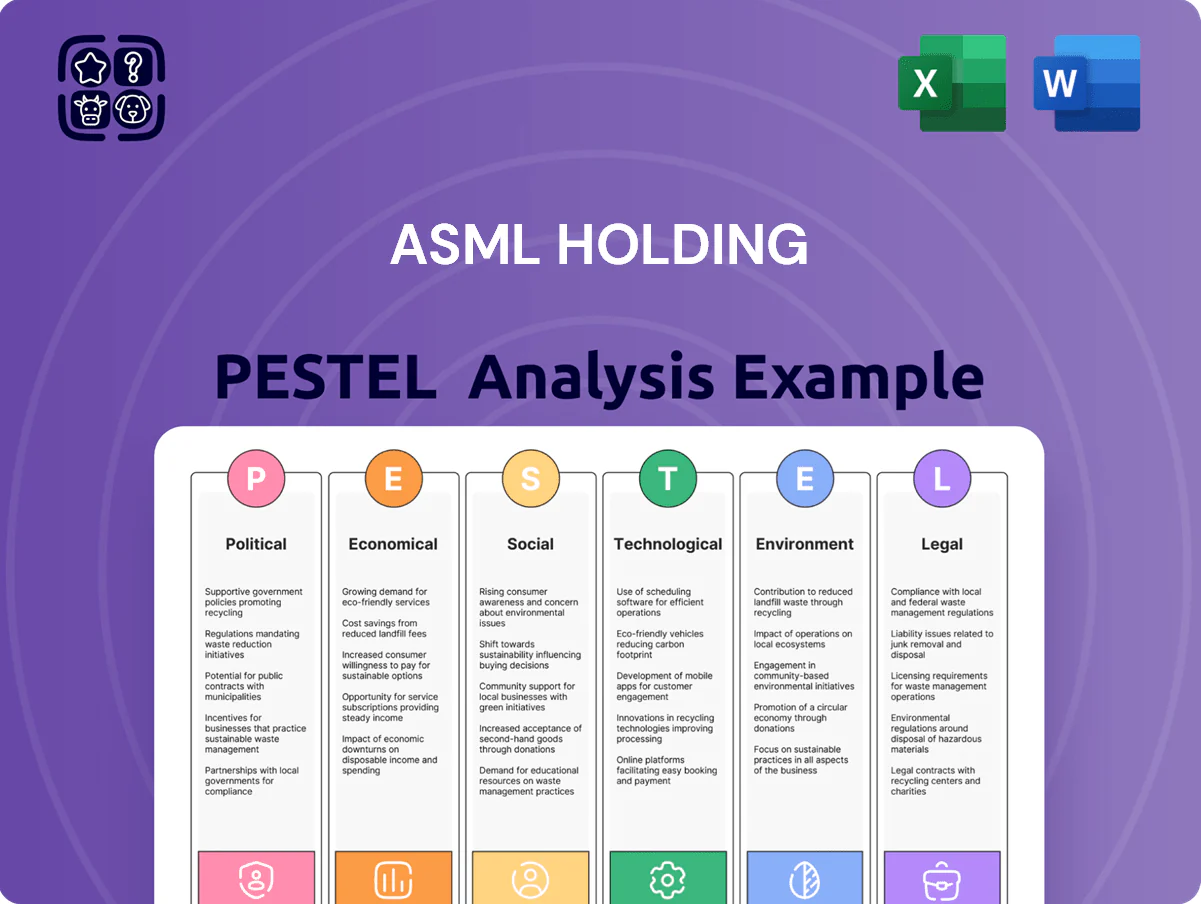

ASML Holding PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock strategic foresight with our concise PESTLE snapshot on ASML Holding—discover how geopolitics, supply-chain risks, tech innovation, and regulatory shifts could alter its growth trajectory; buy the full PESTLE for a complete, actionable breakdown you can use in investment decisions and strategy decks.

Political factors

Export control intensification

The Dutch government, pressured by the United States, tightened export licenses for advanced lithography to China, restricting sales beyond EUV to several DUV classes by late 2025, cutting ASML's China revenue exposure — China accounted for about 14% (€2.1bn) of ASML's 2024 net sales of €14.8bn. The moves force ASML to treat its systems as strategic national-security assets, complicating supply chains and customer contracts. ASML estimates potential near-term revenue impact in the high hundreds of millions of euros annually as orders are delayed or rerouted. The company must balance compliance, shareholder returns, and long-term R&D investment amid escalating geopolitics.

Strategic autonomy initiatives

Major powers like the US and EU have deployed multi-billion dollar Chip Acts—US CHIPS and Science Act ($52.7bn in manufacturing incentives) and the EU’s €43bn European Chips Act—to subsidize fabs, directly supporting ASML customers and stabilizing long-term lithography demand.

These subsidies accelerate onshoring: the US expects $200bn+ in private fab investment through 2030, and the EU targets doubling its global market share by 2030, which de-risks ASML’s revenue visibility.

By reducing reliance on East Asian hubs, these policies lower geopolitical supply-chain risks for ASML and its clients, supporting backlog convertibility and capital expenditure cycles for advanced EUV and DUV tools.

Geopolitical tensions in Asia

The ongoing Taiwan tensions pose a major political risk for ASML, given TSMC—ASML’s largest customer with 2024 revenues of about $64 billion—relies on ASML’s EUV systems for leading-node production. Any escalation could disrupt installation and maintenance of ~200 EUV machines globally and halt output of chips that account for over 60% of advanced logic capacity. ASML must maintain contingency plans for service personnel, alternate supply routes, and insurance to protect ~€32.5 billion 2024 market cap exposure.

Government subsidies for fabs

Political support for semiconductor self-sufficiency has driven over 50 new fab projects since 2022, many needing ASML’s EUV and DUV systems, underpinning multi-year demand.

Japan and South Korea have announced tax incentives and subsidies exceeding $30 billion combined (2023–2025) to attract cutting-edge chip production, boosting ASML order visibility.

Geopolitical competition for technological supremacy secures a steady ASML order pipeline, supporting its long-term revenue growth and backlog expansion.

- 50+ new fabs announced since 2022

- $30B+ in Japan/South Korea incentives (2023–2025)

- Higher order visibility for EUV/DUV systems

Trade policy volatility

Frequent shifts in trade agreements and tariffs heighten uncertainty for ASML’s global supply chain, which in 2025 sourced components from over 300 suppliers across 20+ countries; WTO and tariff changes can add 3–7% to component costs or create weeks-long delays.

Such volatility risks production slowdowns for EUV systems that generated €26.0bn revenue in 2024, so ASML’s leadership invests in continuous diplomatic and regulatory engagement to secure cross-border movement of parts and finished systems.

- 300+ suppliers across 20+ countries

- 3–7% potential cost increase from trade barriers

- Weeks-long shipment delays risk vs €26.0bn 2024 revenue

- Ongoing diplomatic/regulatory engagement required

Geopolitics, chip subsidies and supply‑risk reshape ASML — China exposure, 200 EUVs at stake

Heightened export controls cut China exposure (14% of 2024 sales, €2.1bn) and may cost ASML high‑hundreds of millions annually; US/EU chip subsidies (US $52.7bn; EU €43bn) and 50+ new fabs since 2022 raise order visibility for EUV/DUV; Taiwan tensions threaten service/installation of ~200 EUV machines and disrupt customers like TSMC ($64bn 2024 revenue); 300+ suppliers across 20+ countries create 3–7% cost risk from trade barriers.

| Metric | Value (2024/2025) |

|---|---|

| China share | 14% (€2.1bn) |

| ASML EUV units at risk | ~200 |

| TSMC 2024 revenue | $64bn |

| Suppliers/countries | 300+/20+ |

| Chip Acts | US $52.7bn / EU €43bn |

What is included in the product

Explores how macro-environmental forces—Political, Economic, Social, Technological, Environmental, and Legal—specifically impact ASML Holding’s competitive position in the semiconductor equipment industry, with data-backed trends and forward-looking implications for strategy, risk mitigation, and investment decisions.

A concise ASML PESTLE summary that’s visually segmented for quick meeting reference, easily editable for regional or business-line notes, and formatted for drop-in PowerPoints or team sharing to streamline risk discussions and strategic alignment.

Economic factors

Semiconductor cycle recovery

By end-2025 the semiconductor industry shifted from inventory correction to robust growth led by HPC, with global fab capex rising to an estimated $95–100 billion in 2025 vs ~$85B in 2023, boosting orders from Intel, Samsung and TSMC.

ASML benefits directly as customers expand EUV and DUV investment—ASML revenue guidance for 2025 points to mid-to-high single-digit growth with backlog near a record €40–45 billion.

High capital expenditure requirements

The transition to High-NA EUV demands massive investment: ASML’s NXE machines cost ~€150–€200m each and upcoming High-NA systems are projected higher, making capital spending cyclical and sensitive to interest rates; ASML recorded R&D of €4.7bn in 2024, requiring tight cost control to protect margins while customers like TSMC, Samsung and Intel must secure multi‑billion dollar financing to expand capacity.

Inflation and supply costs

Global inflation pushed input costs up sharply: commodity and energy inflation raised materials and power expenses for ASML, with semiconductor-grade components prices rising an estimated 8-12% in 2023–2024 and logistics costs up ~20% year-over-year.

To protect margins ASML introduced price escalators and service pass-throughs while targeting operational improvements that lifted factory productivity and reduced unit cost by roughly 5% in 2024.

Controlling these rising input costs is critical for ASML to stay on track for its 2025 mid-cycle margin goals and 2030 revenue and EBIT targets disclosed in its 2024 annual report.

Currency exchange risk

As a Euro-reporting Dutch firm with ~80% revenue from non-Euro markets (2024 sales €26.2bn), ASML faces transaction and translation risks as many contracts and customers price in USD; a 10% EUR/USD appreciation would materially reduce reported euro revenue and hurt competitiveness versus US-priced rivals.

ASML actively uses forward contracts, options and natural hedges; in FY2024 it reported net foreign-exchange gains/losses variability and disclosed hedging programs covering a substantial portion of expected USD inflows to stabilize margins.

- ~80% revenue outside Eurozone (FY2024: €26.2bn)

- High exposure to USD-denominated sales—EUR/USD swings directly affect pricing & translated revenue

- Hedging via forwards/options and operational natural hedges to reduce volatility

AI-driven market growth

The explosive AI application growth drove global chip demand: AI accelerator shipments grew ~45% in 2024 and the AI silicon market reached an estimated $60–70 billion in 2024, fueling demand for advanced logic and memory chips.

ASML benefits as AI chips require extreme ultraviolet (EUV) and high-NA lithography; ASML held ~80–90% global market share in EUV systems in 2024 and reported 2024 net sales of €29.4 billion, reflecting this tailwind.

As the sole supplier of production-grade EUV tools and advancing high-NA development, ASML is uniquely positioned to enable AI hardware scaling worldwide.

- AI silicon market ~ $60–70B (2024)

- AI accelerator shipments +45% (2024)

- ASML 2024 net sales €29.4B

- ASML ~80–90% EUV market share (2024)

ASML rides AI capex surge: 2025 backlog €40–45B, sales €29.4B, R&D €4.7B

Economic tailwinds from AI/HPC raised fab capex to ~$95–100B in 2025 (vs ~$85B in 2023), lifting ASML 2025 guidance to mid‑to‑high single‑digit revenue growth and backlog ~€40–45bn; 2024 net sales €29.4bn. Inflation pushed component costs +8–12% (2023–24) and logistics +20%, while R&D was €4.7bn (2024). FX risk high: ~80% revenue outside Eurozone (FY2024: €26.2bn), hedged via forwards/options.

| Metric | Value |

|---|---|

| Fab capex 2025 | $95–100B |

| ASML 2024 sales | €29.4B |

| Backlog 2025 | €40–45B |

| R&D 2024 | €4.7B |

| Revenue outside Euro | ~80% (FY2024: €26.2B) |

Full Version Awaits

ASML Holding PESTLE Analysis

The preview shown here is the exact ASML Holding PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic analysis and decision-making.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock strategic foresight with our concise PESTLE snapshot on ASML Holding—discover how geopolitics, supply-chain risks, tech innovation, and regulatory shifts could alter its growth trajectory; buy the full PESTLE for a complete, actionable breakdown you can use in investment decisions and strategy decks.

Political factors

Export control intensification

The Dutch government, pressured by the United States, tightened export licenses for advanced lithography to China, restricting sales beyond EUV to several DUV classes by late 2025, cutting ASML's China revenue exposure — China accounted for about 14% (€2.1bn) of ASML's 2024 net sales of €14.8bn. The moves force ASML to treat its systems as strategic national-security assets, complicating supply chains and customer contracts. ASML estimates potential near-term revenue impact in the high hundreds of millions of euros annually as orders are delayed or rerouted. The company must balance compliance, shareholder returns, and long-term R&D investment amid escalating geopolitics.

Strategic autonomy initiatives

Major powers like the US and EU have deployed multi-billion dollar Chip Acts—US CHIPS and Science Act ($52.7bn in manufacturing incentives) and the EU’s €43bn European Chips Act—to subsidize fabs, directly supporting ASML customers and stabilizing long-term lithography demand.

These subsidies accelerate onshoring: the US expects $200bn+ in private fab investment through 2030, and the EU targets doubling its global market share by 2030, which de-risks ASML’s revenue visibility.

By reducing reliance on East Asian hubs, these policies lower geopolitical supply-chain risks for ASML and its clients, supporting backlog convertibility and capital expenditure cycles for advanced EUV and DUV tools.

Geopolitical tensions in Asia

The ongoing Taiwan tensions pose a major political risk for ASML, given TSMC—ASML’s largest customer with 2024 revenues of about $64 billion—relies on ASML’s EUV systems for leading-node production. Any escalation could disrupt installation and maintenance of ~200 EUV machines globally and halt output of chips that account for over 60% of advanced logic capacity. ASML must maintain contingency plans for service personnel, alternate supply routes, and insurance to protect ~€32.5 billion 2024 market cap exposure.

Government subsidies for fabs

Political support for semiconductor self-sufficiency has driven over 50 new fab projects since 2022, many needing ASML’s EUV and DUV systems, underpinning multi-year demand.

Japan and South Korea have announced tax incentives and subsidies exceeding $30 billion combined (2023–2025) to attract cutting-edge chip production, boosting ASML order visibility.

Geopolitical competition for technological supremacy secures a steady ASML order pipeline, supporting its long-term revenue growth and backlog expansion.

- 50+ new fabs announced since 2022

- $30B+ in Japan/South Korea incentives (2023–2025)

- Higher order visibility for EUV/DUV systems

Trade policy volatility

Frequent shifts in trade agreements and tariffs heighten uncertainty for ASML’s global supply chain, which in 2025 sourced components from over 300 suppliers across 20+ countries; WTO and tariff changes can add 3–7% to component costs or create weeks-long delays.

Such volatility risks production slowdowns for EUV systems that generated €26.0bn revenue in 2024, so ASML’s leadership invests in continuous diplomatic and regulatory engagement to secure cross-border movement of parts and finished systems.

- 300+ suppliers across 20+ countries

- 3–7% potential cost increase from trade barriers

- Weeks-long shipment delays risk vs €26.0bn 2024 revenue

- Ongoing diplomatic/regulatory engagement required

Geopolitics, chip subsidies and supply‑risk reshape ASML — China exposure, 200 EUVs at stake

Heightened export controls cut China exposure (14% of 2024 sales, €2.1bn) and may cost ASML high‑hundreds of millions annually; US/EU chip subsidies (US $52.7bn; EU €43bn) and 50+ new fabs since 2022 raise order visibility for EUV/DUV; Taiwan tensions threaten service/installation of ~200 EUV machines and disrupt customers like TSMC ($64bn 2024 revenue); 300+ suppliers across 20+ countries create 3–7% cost risk from trade barriers.

| Metric | Value (2024/2025) |

|---|---|

| China share | 14% (€2.1bn) |

| ASML EUV units at risk | ~200 |

| TSMC 2024 revenue | $64bn |

| Suppliers/countries | 300+/20+ |

| Chip Acts | US $52.7bn / EU €43bn |

What is included in the product

Explores how macro-environmental forces—Political, Economic, Social, Technological, Environmental, and Legal—specifically impact ASML Holding’s competitive position in the semiconductor equipment industry, with data-backed trends and forward-looking implications for strategy, risk mitigation, and investment decisions.

A concise ASML PESTLE summary that’s visually segmented for quick meeting reference, easily editable for regional or business-line notes, and formatted for drop-in PowerPoints or team sharing to streamline risk discussions and strategic alignment.

Economic factors

Semiconductor cycle recovery

By end-2025 the semiconductor industry shifted from inventory correction to robust growth led by HPC, with global fab capex rising to an estimated $95–100 billion in 2025 vs ~$85B in 2023, boosting orders from Intel, Samsung and TSMC.

ASML benefits directly as customers expand EUV and DUV investment—ASML revenue guidance for 2025 points to mid-to-high single-digit growth with backlog near a record €40–45 billion.

High capital expenditure requirements

The transition to High-NA EUV demands massive investment: ASML’s NXE machines cost ~€150–€200m each and upcoming High-NA systems are projected higher, making capital spending cyclical and sensitive to interest rates; ASML recorded R&D of €4.7bn in 2024, requiring tight cost control to protect margins while customers like TSMC, Samsung and Intel must secure multi‑billion dollar financing to expand capacity.

Inflation and supply costs

Global inflation pushed input costs up sharply: commodity and energy inflation raised materials and power expenses for ASML, with semiconductor-grade components prices rising an estimated 8-12% in 2023–2024 and logistics costs up ~20% year-over-year.

To protect margins ASML introduced price escalators and service pass-throughs while targeting operational improvements that lifted factory productivity and reduced unit cost by roughly 5% in 2024.

Controlling these rising input costs is critical for ASML to stay on track for its 2025 mid-cycle margin goals and 2030 revenue and EBIT targets disclosed in its 2024 annual report.

Currency exchange risk

As a Euro-reporting Dutch firm with ~80% revenue from non-Euro markets (2024 sales €26.2bn), ASML faces transaction and translation risks as many contracts and customers price in USD; a 10% EUR/USD appreciation would materially reduce reported euro revenue and hurt competitiveness versus US-priced rivals.

ASML actively uses forward contracts, options and natural hedges; in FY2024 it reported net foreign-exchange gains/losses variability and disclosed hedging programs covering a substantial portion of expected USD inflows to stabilize margins.

- ~80% revenue outside Eurozone (FY2024: €26.2bn)

- High exposure to USD-denominated sales—EUR/USD swings directly affect pricing & translated revenue

- Hedging via forwards/options and operational natural hedges to reduce volatility

AI-driven market growth

The explosive AI application growth drove global chip demand: AI accelerator shipments grew ~45% in 2024 and the AI silicon market reached an estimated $60–70 billion in 2024, fueling demand for advanced logic and memory chips.

ASML benefits as AI chips require extreme ultraviolet (EUV) and high-NA lithography; ASML held ~80–90% global market share in EUV systems in 2024 and reported 2024 net sales of €29.4 billion, reflecting this tailwind.

As the sole supplier of production-grade EUV tools and advancing high-NA development, ASML is uniquely positioned to enable AI hardware scaling worldwide.

- AI silicon market ~ $60–70B (2024)

- AI accelerator shipments +45% (2024)

- ASML 2024 net sales €29.4B

- ASML ~80–90% EUV market share (2024)

ASML rides AI capex surge: 2025 backlog €40–45B, sales €29.4B, R&D €4.7B

Economic tailwinds from AI/HPC raised fab capex to ~$95–100B in 2025 (vs ~$85B in 2023), lifting ASML 2025 guidance to mid‑to‑high single‑digit revenue growth and backlog ~€40–45bn; 2024 net sales €29.4bn. Inflation pushed component costs +8–12% (2023–24) and logistics +20%, while R&D was €4.7bn (2024). FX risk high: ~80% revenue outside Eurozone (FY2024: €26.2bn), hedged via forwards/options.

| Metric | Value |

|---|---|

| Fab capex 2025 | $95–100B |

| ASML 2024 sales | €29.4B |

| Backlog 2025 | €40–45B |

| R&D 2024 | €4.7B |

| Revenue outside Euro | ~80% (FY2024: €26.2B) |

Full Version Awaits

ASML Holding PESTLE Analysis

The preview shown here is the exact ASML Holding PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic analysis and decision-making.