Associated Bank PESTLE Analysis

Your Competitive Advantage Starts with This Report

Discover how political shifts, economic cycles, and emerging technologies are shaping Associated Bank’s strategy and risk profile with our concise PESTLE analysis—designed for investors, advisors, and executives seeking actionable insights. Purchase the full report to access a detailed breakdown of regulatory threats, market opportunities, and social trends, ready for immediate use in strategy, research, or investment decisions.

Political factors

Post-Election Regulatory Shifts

The 2024 U.S. presidential outcome triggered regulatory shifts entering 2025, with new CFPB and OCC leadership proposing tougher capital buffers for regional banks—industry estimates suggest a 50–150 bps increase in risk-weighted capital targets for banks sized like Associated Bank (assets ~$50B in 2024).

Midwestern State Fiscal Policies

As a primary player in Wisconsin, Illinois, and Minnesota, Associated Bank is exposed to state-level political stability and tax regimes that shape its operating costs; in 2024 Wisconsin cut corporate tax rate to 7.9% while Illinois maintained 9.5%, affecting regional profitability spreads. Legislative changes to corporate taxation and small-business incentives—Minnesota allocated $200m in 2025 for small business tax credits—directly influence commercial lending demand. Political alignment between governors and legislatures affects infrastructure and workforce policies that drive loan growth and credit quality across the bank’s footprint.

Government Lending Programs

Associated Bank's participation in SBA and other government-backed lending hinges on federal appropriations; FY2024 SBA lending nationally was $34.8bn, and shifts in 2025 budget priorities could tighten available guarantees affecting originations.

Reprioritization between agricultural and urban development subsidies can reshape Associated's portfolio mix—USDA farm loans fell 6% in 2024 while urban redevelopment grants rose 12%, altering regional demand.

Political backing for community development financial institutions remains pivotal; CDFI Fund awards totaled $1.5bn in 2024, supporting Associated's localized growth initiatives in underserved Midwest markets.

Trade Policy Impact on Clients

Federal trade policies and tariffs heavily affect Associated Bank's commercial clients in the Upper Midwest, where manufacturing and agriculture represent roughly 18% of regional GDP; tariffs on steel and soybeans in 2024 raised input costs and reduced export volumes by up to 7% for some clients.

Ongoing geopolitical tensions in 2025 lowered US agricultural exports to key markets by ~5–10%, increasing commercial loan delinquencies in affected counties and pressuring demand for trade finance.

The bank must closely monitor tariff changes and export restrictions to adjust credit underwriting, stress-test portfolios, and limit concentration risk in exposed sectors.

- Manufacturing/agriculture ≈18% regional GDP

- Tariff-driven cost rises up to 7% (2024)

- Export declines 5–10% (2025)

- Increased delinquency and trade finance pressure

Housing and Urban Development Policy

- Increased CRA-driven mortgage lending due to 3.8M U.S. housing shortfall

- $6.5B+ in subsidies and tax credits enabling first-time buyer products

- $45B federal urban renewal funds shifting capital to urban mixed-use lending

Regulatory tightening, tax shifts and trade hits squeeze mid‑sized banks’ capital & margins

Regulatory tightening in 2025 (CFPB/OCC) may push risk-weighted capital targets +50–150 bps for ~$50bn banks like Associated; state tax spreads (WI 7.9% vs IL 9.5% in 2024) and MN $200m small‑biz credits (2025) affect margins and loan demand; FY2024 SBA lending $34.8bn and CDFI awards $1.5bn support originations; tariffs and export declines (5–10% in 2025) raised sector delinquencies.

| Metric | 2024/2025 |

|---|---|

| Assoc Bank assets (2024) | $50bn |

| Capital target change | +50–150 bps |

| WI vs IL corporate tax (2024) | 7.9% / 9.5% |

| MN small‑biz credits (2025) | $200m |

| FY2024 SBA lending | $34.8bn |

| CDFI Fund awards (2024) | $1.5bn |

| Export decline (2025) | 5–10% |

What is included in the product

Explores how macro-environmental factors uniquely affect Associated Bank across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific examples to identify threats and opportunities for executives and investors.

A concise, shareable PESTLE summary tailored for Associated Bank that’s visually segmented for quick interpretation, making it easy to drop into presentations, support risk discussions, and align teams during planning sessions.

Economic factors

Interest Rate Environment Stabilization

After multi-year volatility, the 2025 federal funds rate settled around 5.00–5.25%, narrowing quarterly NII swings; Associated Bank faces compressed net interest margin trends with 2024 industry NIM averaging ~2.50%. The bank must tightly manage deposit costs—retail savings/cD rates rose ~1.2 percentage points since 2022—while preserving loan yields (commercial avg. yields ~6.0%) to sustain ROA targets. Fed policy pacing remains the primary driver of retail and commercial pricing.

Regional Employment and Income Levels

The Midwest economy, led by Wisconsin and Minnesota manufacturing and healthcare hubs, supported deposit growth at regional banks; Wisconsin's unemployment fell to 2.6% and Minnesota's median household income rose to about $79,000 in 2024, boosting Associated Bank's retail deposits and lowering delinquencies.

Inflationary Pressure on Operating Costs

Persistent inflation—US CPI running 3.4% year-over-year in 2025 Q4—raises Associated Bank’s overhead via higher wages and 10–15% year-on-year increases in IT procurement and cloud costs, squeezing margins.

Higher inflation can lift nominal interest income as Fed funds averaged ~5.1% in 2025, but also raises loan servicing and branch maintenance costs, increasing provision and operating expense.

Keeping efficiency ratio near 60% (2024 reported ~58%) is critical to offset rising operational expenses and preserve ROA/ROE.

Commercial Real Estate Market Health

The ongoing shift in office utilization has pushed downtown Milwaukee and Minneapolis vacancy rates to about 17–20% in 2024, pressuring valuations and loan performance for Associated Bank.

Associated Bank’s CRE exposure necessitates monitoring occupancy and valuation trends as average office cap rates in the Midwest rose to ~7.5% in 2024, increasing credit risk.

Growth in mixed-use and industrial demand—Midwest industrial vacancy near 4% and rents up ~6% YoY—offers diversification paths to mitigate CRE concentration risk.

- Milwaukee/Minneapolis office vacancy ~17–20% (2024)

- Midwest office cap rates ~7.5% (2024)

- Industrial vacancy ~4%, rents +6% YoY (2024)

- Action: monitor occupancy, valuations, shift lending to mixed-use/industrial

Consumer Spending and Debt Levels

Rising consumer credit utilization—U.S. credit card balances grew 14% y/y to about $1.16 trillion in 2024—boosts demand for Associated Bank’s personal loan and credit card offerings but increases loss exposure.

As households target lower debt-to-income ratios after peak 2022 inflation, Associated Bank must recalibrate credit-scoring and loss given default assumptions to reflect tighter repayment capacity.

Strong consumer spending—retail sales up 4.5% y/y in 2024—supports merchant services and transaction fee income, underpinning noninterest revenue growth.

- Credit card balances +14% y/y (2024)

- Retail sales +4.5% y/y (2024)

- Need to adjust credit scoring and loss parameters

Macro snapshot: Sticky rates, tight labor, rising credit and divergent CRE markets

Fed funds ~5.00–5.25% (2025); industry NIM ~2.5% (2024); retail deposit rates +1.2ppt since 2022; commercial yields ~6.0%; Wisconsin unemployment 2.6% (2024); US CPI 3.4% YoY (2025 Q4); office vacancy 17–20% (2024); Midwest office cap rate ~7.5% (2024); industrial vacancy ~4%, rents +6% YoY (2024); credit card balances +14% y/y to $1.16T (2024).

| Metric | Value |

|---|---|

| Fed funds (2025) | 5.00–5.25% |

| Industry NIM (2024) | ~2.5% |

| WI unemployment (2024) | 2.6% |

| US CPI (2025 Q4) | 3.4% YoY |

| Office vacancy (Midwest, 2024) | 17–20% |

| Office cap rate (Midwest, 2024) | ~7.5% |

| Industrial vacancy (2024) | ~4% |

| Credit card balances (2024) | $1.16T (+14% YoY) |

Preview the Actual Deliverable

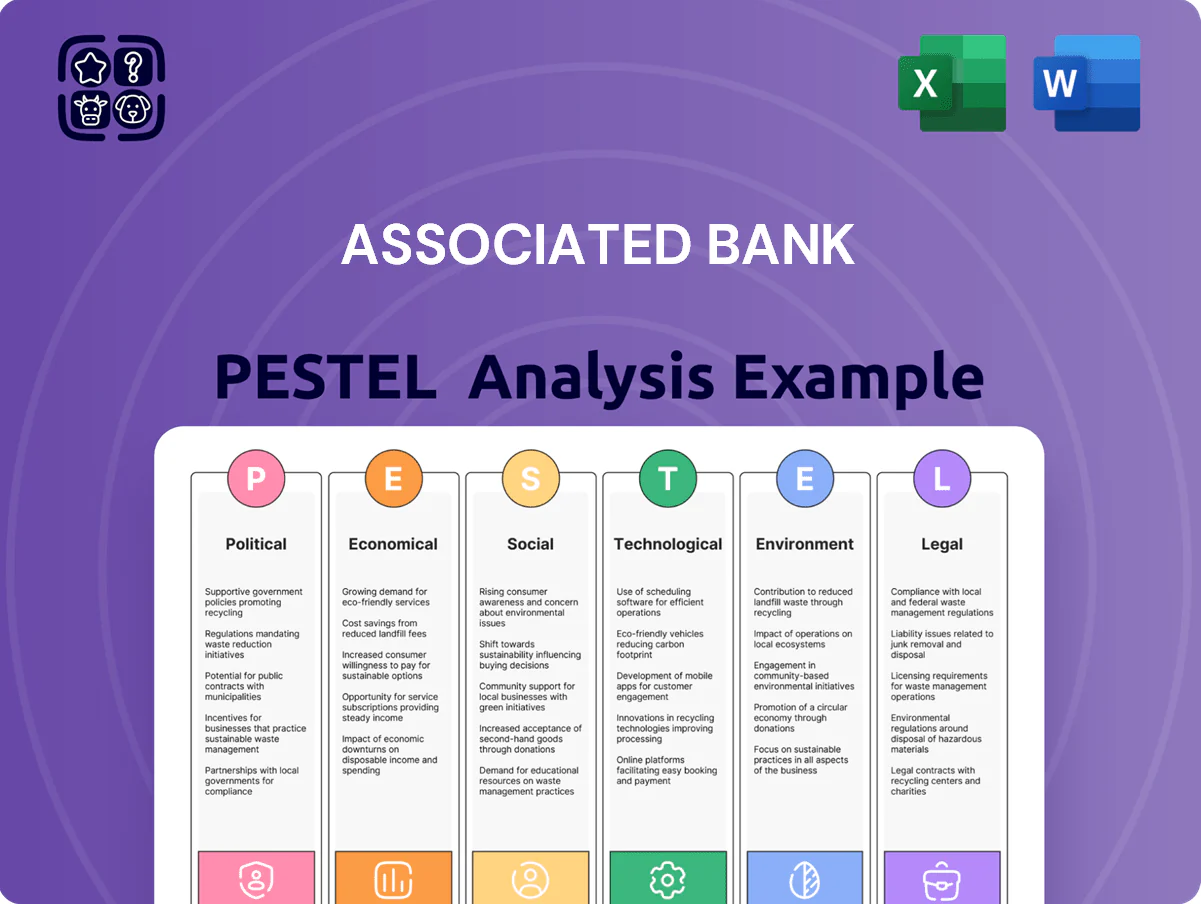

Associated Bank PESTLE Analysis

The preview shown here is the exact Associated Bank PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use.

The layout, content, and structure visible are identical to the downloadable file you’ll get immediately after checkout—no placeholders, no surprises.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Discover how political shifts, economic cycles, and emerging technologies are shaping Associated Bank’s strategy and risk profile with our concise PESTLE analysis—designed for investors, advisors, and executives seeking actionable insights. Purchase the full report to access a detailed breakdown of regulatory threats, market opportunities, and social trends, ready for immediate use in strategy, research, or investment decisions.

Political factors

Post-Election Regulatory Shifts

The 2024 U.S. presidential outcome triggered regulatory shifts entering 2025, with new CFPB and OCC leadership proposing tougher capital buffers for regional banks—industry estimates suggest a 50–150 bps increase in risk-weighted capital targets for banks sized like Associated Bank (assets ~$50B in 2024).

Midwestern State Fiscal Policies

As a primary player in Wisconsin, Illinois, and Minnesota, Associated Bank is exposed to state-level political stability and tax regimes that shape its operating costs; in 2024 Wisconsin cut corporate tax rate to 7.9% while Illinois maintained 9.5%, affecting regional profitability spreads. Legislative changes to corporate taxation and small-business incentives—Minnesota allocated $200m in 2025 for small business tax credits—directly influence commercial lending demand. Political alignment between governors and legislatures affects infrastructure and workforce policies that drive loan growth and credit quality across the bank’s footprint.

Government Lending Programs

Associated Bank's participation in SBA and other government-backed lending hinges on federal appropriations; FY2024 SBA lending nationally was $34.8bn, and shifts in 2025 budget priorities could tighten available guarantees affecting originations.

Reprioritization between agricultural and urban development subsidies can reshape Associated's portfolio mix—USDA farm loans fell 6% in 2024 while urban redevelopment grants rose 12%, altering regional demand.

Political backing for community development financial institutions remains pivotal; CDFI Fund awards totaled $1.5bn in 2024, supporting Associated's localized growth initiatives in underserved Midwest markets.

Trade Policy Impact on Clients

Federal trade policies and tariffs heavily affect Associated Bank's commercial clients in the Upper Midwest, where manufacturing and agriculture represent roughly 18% of regional GDP; tariffs on steel and soybeans in 2024 raised input costs and reduced export volumes by up to 7% for some clients.

Ongoing geopolitical tensions in 2025 lowered US agricultural exports to key markets by ~5–10%, increasing commercial loan delinquencies in affected counties and pressuring demand for trade finance.

The bank must closely monitor tariff changes and export restrictions to adjust credit underwriting, stress-test portfolios, and limit concentration risk in exposed sectors.

- Manufacturing/agriculture ≈18% regional GDP

- Tariff-driven cost rises up to 7% (2024)

- Export declines 5–10% (2025)

- Increased delinquency and trade finance pressure

Housing and Urban Development Policy

- Increased CRA-driven mortgage lending due to 3.8M U.S. housing shortfall

- $6.5B+ in subsidies and tax credits enabling first-time buyer products

- $45B federal urban renewal funds shifting capital to urban mixed-use lending

Regulatory tightening, tax shifts and trade hits squeeze mid‑sized banks’ capital & margins

Regulatory tightening in 2025 (CFPB/OCC) may push risk-weighted capital targets +50–150 bps for ~$50bn banks like Associated; state tax spreads (WI 7.9% vs IL 9.5% in 2024) and MN $200m small‑biz credits (2025) affect margins and loan demand; FY2024 SBA lending $34.8bn and CDFI awards $1.5bn support originations; tariffs and export declines (5–10% in 2025) raised sector delinquencies.

| Metric | 2024/2025 |

|---|---|

| Assoc Bank assets (2024) | $50bn |

| Capital target change | +50–150 bps |

| WI vs IL corporate tax (2024) | 7.9% / 9.5% |

| MN small‑biz credits (2025) | $200m |

| FY2024 SBA lending | $34.8bn |

| CDFI Fund awards (2024) | $1.5bn |

| Export decline (2025) | 5–10% |

What is included in the product

Explores how macro-environmental factors uniquely affect Associated Bank across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific examples to identify threats and opportunities for executives and investors.

A concise, shareable PESTLE summary tailored for Associated Bank that’s visually segmented for quick interpretation, making it easy to drop into presentations, support risk discussions, and align teams during planning sessions.

Economic factors

Interest Rate Environment Stabilization

After multi-year volatility, the 2025 federal funds rate settled around 5.00–5.25%, narrowing quarterly NII swings; Associated Bank faces compressed net interest margin trends with 2024 industry NIM averaging ~2.50%. The bank must tightly manage deposit costs—retail savings/cD rates rose ~1.2 percentage points since 2022—while preserving loan yields (commercial avg. yields ~6.0%) to sustain ROA targets. Fed policy pacing remains the primary driver of retail and commercial pricing.

Regional Employment and Income Levels

The Midwest economy, led by Wisconsin and Minnesota manufacturing and healthcare hubs, supported deposit growth at regional banks; Wisconsin's unemployment fell to 2.6% and Minnesota's median household income rose to about $79,000 in 2024, boosting Associated Bank's retail deposits and lowering delinquencies.

Inflationary Pressure on Operating Costs

Persistent inflation—US CPI running 3.4% year-over-year in 2025 Q4—raises Associated Bank’s overhead via higher wages and 10–15% year-on-year increases in IT procurement and cloud costs, squeezing margins.

Higher inflation can lift nominal interest income as Fed funds averaged ~5.1% in 2025, but also raises loan servicing and branch maintenance costs, increasing provision and operating expense.

Keeping efficiency ratio near 60% (2024 reported ~58%) is critical to offset rising operational expenses and preserve ROA/ROE.

Commercial Real Estate Market Health

The ongoing shift in office utilization has pushed downtown Milwaukee and Minneapolis vacancy rates to about 17–20% in 2024, pressuring valuations and loan performance for Associated Bank.

Associated Bank’s CRE exposure necessitates monitoring occupancy and valuation trends as average office cap rates in the Midwest rose to ~7.5% in 2024, increasing credit risk.

Growth in mixed-use and industrial demand—Midwest industrial vacancy near 4% and rents up ~6% YoY—offers diversification paths to mitigate CRE concentration risk.

- Milwaukee/Minneapolis office vacancy ~17–20% (2024)

- Midwest office cap rates ~7.5% (2024)

- Industrial vacancy ~4%, rents +6% YoY (2024)

- Action: monitor occupancy, valuations, shift lending to mixed-use/industrial

Consumer Spending and Debt Levels

Rising consumer credit utilization—U.S. credit card balances grew 14% y/y to about $1.16 trillion in 2024—boosts demand for Associated Bank’s personal loan and credit card offerings but increases loss exposure.

As households target lower debt-to-income ratios after peak 2022 inflation, Associated Bank must recalibrate credit-scoring and loss given default assumptions to reflect tighter repayment capacity.

Strong consumer spending—retail sales up 4.5% y/y in 2024—supports merchant services and transaction fee income, underpinning noninterest revenue growth.

- Credit card balances +14% y/y (2024)

- Retail sales +4.5% y/y (2024)

- Need to adjust credit scoring and loss parameters

Macro snapshot: Sticky rates, tight labor, rising credit and divergent CRE markets

Fed funds ~5.00–5.25% (2025); industry NIM ~2.5% (2024); retail deposit rates +1.2ppt since 2022; commercial yields ~6.0%; Wisconsin unemployment 2.6% (2024); US CPI 3.4% YoY (2025 Q4); office vacancy 17–20% (2024); Midwest office cap rate ~7.5% (2024); industrial vacancy ~4%, rents +6% YoY (2024); credit card balances +14% y/y to $1.16T (2024).

| Metric | Value |

|---|---|

| Fed funds (2025) | 5.00–5.25% |

| Industry NIM (2024) | ~2.5% |

| WI unemployment (2024) | 2.6% |

| US CPI (2025 Q4) | 3.4% YoY |

| Office vacancy (Midwest, 2024) | 17–20% |

| Office cap rate (Midwest, 2024) | ~7.5% |

| Industrial vacancy (2024) | ~4% |

| Credit card balances (2024) | $1.16T (+14% YoY) |

Preview the Actual Deliverable

Associated Bank PESTLE Analysis

The preview shown here is the exact Associated Bank PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use.

The layout, content, and structure visible are identical to the downloadable file you’ll get immediately after checkout—no placeholders, no surprises.