Assurant Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

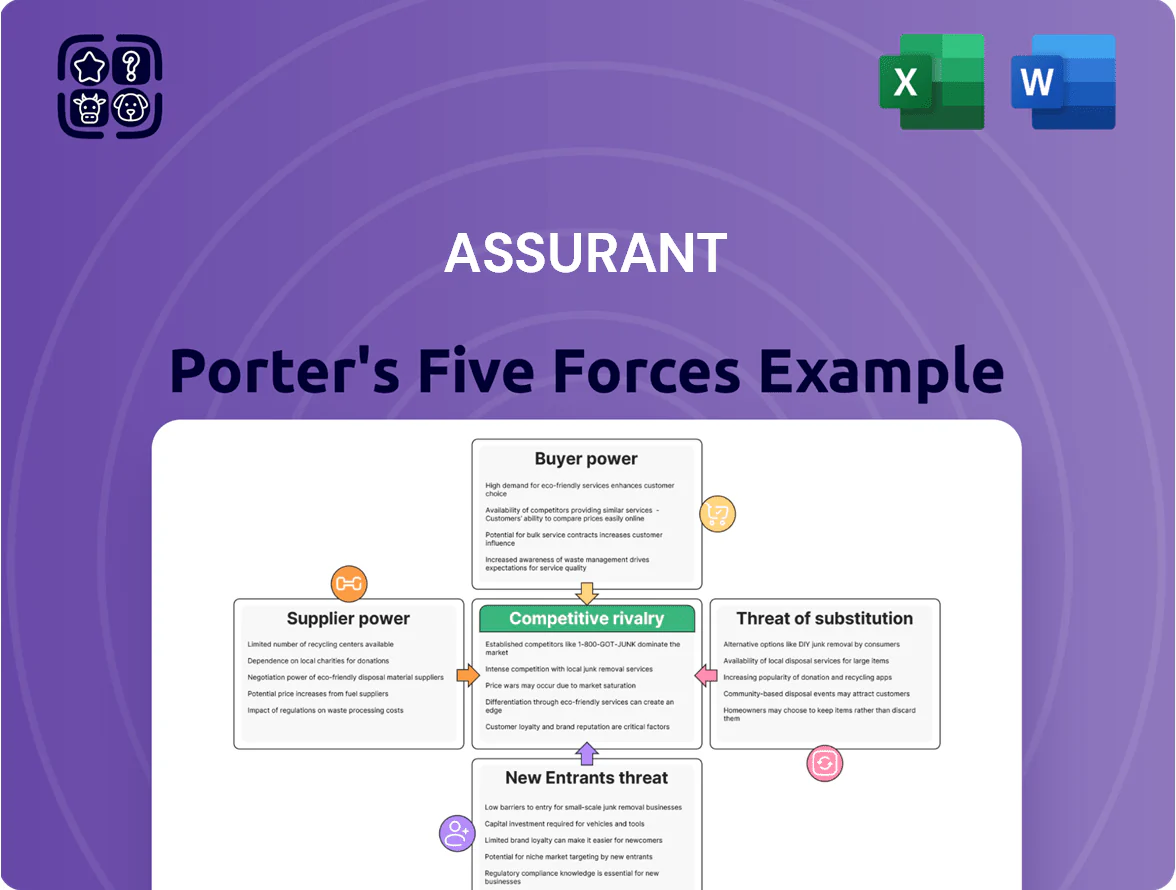

Assurant faces moderate buyer power, concentrated suppliers for some tech-driven services, and steady competitive rivalry from insurers and fintech entrants that pressure margins and innovation.

Regulatory scrutiny and capital requirements raise barriers, yet digital disruptors and white-label providers keep the threat of new entrants and substitutes meaningful.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Assurant’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Mobile Original Equipment Manufacturers

Assurant depends on partnerships with Apple and Samsung, which together held ~68% global smartphone market share in 2025, concentrating supplier power and embedment of protection plans into device ecosystems.

These OEMs set proprietary designs and warranty rules that set parts pricing and authorized-repair access, making Assurant's unit repair cost and margins hinge on OEM policies.

By end-2025, few giants' dominance raised exposure: a 2024–25 policy shift could swing Assurant's service costs by an estimated 8–12% per claim, increasing strategic vulnerability.

Reliance on Reinsurance Providers

As a housing and specialty insurer, Assurant shifts large loss exposure to global reinsurers; in 2025 reinsurer bargaining power is high after climate-driven losses tightened capacity and pushed average property-cat reinsurance rates up roughly 30% year-over-year. Assurant can either pay higher ceded-premium costs—squeezing combined ratios—or retain more risk, which would raise required capital and volatility. Moody’s estimated 2024–25 global catastrophe insured losses climbed to about $120 billion, keeping upward pressure on 2025 treaty pricing. Accepting higher reinsurance costs would directly cut Assurant’s underwriting margin unless offset by rate increases or expense savings.

Availability of Skilled Technical Labor

The fulfillment of Assurant extended service contracts for appliances and electronics relies on a vast network of third‑party repair technicians and logistics providers, and in 2025 a documented 18% shortage in specialized technical talent has allowed these suppliers to demand higher fees, raising unit service costs by about 5–8% vs 2023; Assurant must preserve these relationships to keep customer satisfaction high and claims turnaround near its target of <7 days.

Data and Cloud Infrastructure Providers

Assurant’s digital shift ties core mobile-diagnostic and automated-claims workflows to major cloud and analytics vendors, creating heavy reliance on their platforms.

Global hyperscaler fees rose ~18% YoY in 2024; switching cloud providers would mean months of migration and multiyear rearchitecting, so suppliers keep strong pricing leverage over Assurant’s IT budget.

Here’s the quick math: a 10% cloud-cost increase on a $200M annual cloud spend adds $20M to operating costs, directly pressuring margins.

- Dependence: core systems run on hyperscalers

- Switching cost: months–years, high rearchitecture risk

- Pricing power: vendors raised fees ~18% in 2024

- Impact: $200M cloud spend → $20M cost per 10% hike

Automotive Dealership and Repair Networks

Assurant relies on dealership and authorized-repair networks as the primary gateway to sell and service vehicle-protection plans; in 2024 dealers accounted for roughly 65% of policy sales in U.S. vehicle protection channels.

These providers can steer customers to specific plans and, with rising vehicle electronics complexity by 2025, repair shops have pushed reimbursement increases—industry reports show average labor rates up 6–8% and parts surcharges for advanced driver-assistance systems (ADAS) adding $200–$1,200 per repair.

Higher reimbursements squeeze Assurant’s margins unless it renegotiates fees, which is hard because top dealer groups control large local market shares and service bay capacity.

- Dealers = ~65% of U.S. policy distribution (2024)

- Labor rates +6–8% (recent industry data)

- ADAS parts add $200–$1,200 per repair

- Reimbursement pressure reduces Assurant margins

Supplier power squeezes margins: OEMs, hyperscalers, reinsurers drive 8–12% cost swings

Suppliers hold strong power: OEMs (Apple, Samsung ~68% share in 2025) and hyperscalers raised fees ~18% in 2024, while reinsurers pushed reinsurance rates ~30% YoY and global cat losses ~ $120B (2024–25), together risking 8–12% per-claim cost swings and $20M per 10% cloud hike on $200M spend.

| Supplier | 2024–25 metric | Impact on Assurant |

|---|---|---|

| OEMs | Apple+Samsung ~68% market share (2025) | Proprietary parts/pricing → 8–12% cost swing |

| Hyperscalers | Fees +18% (2024) | $200M cloud → $20M/10% increase |

| Reinsurers | Reinsurance rates +30% YoY; global cat losses ~$120B | Higher ceded premiums or retained risk → margin pressure |

What is included in the product

Tailored Porter's Five Forces analysis for Assurant that uncovers competitive drivers, supplier and buyer power, entry barriers, substitution risks, and strategic recommendations to protect market share and profitability.

Assurant Porter's Five Forces one-sheet clarifies competitive pressures in insurance and specialty housing markets, letting you quickly spot threats and opportunities for strategic moves.

Customers Bargaining Power

Concentration of Major Mobile Carrier Partners

A significant portion of Assurant’s revenue comes from a handful of major mobile network operators that bundle device protection with plans; in 2024 carriers accounted for roughly 55–65% of Assurant’s protection revenue, giving these partners outsized leverage. These enterprise customers can push for lower wholesale rates or richer profit-share splits at renewals, squeezing margins; contract concessions in 2023–24 trimmed coverage GP% by an estimated 150–250 basis points. Continued telecom consolidation through 2025—mergers reducing large U.S. carriers to three national players—further limits Assurant’s alternative large-scale partners and raises customer bargaining power.

Low Switching Costs for Individual Policyholders

Individual renters and mobile-protection customers face very low switching costs, with online quote tools letting shoppers compare monthly premiums and deductibles across 10+ providers in minutes; a 2024 J.D. Power study found 42% of renters switched carriers within 12 months when price or service dipped. In 2025’s transparent digital market, Assurant must keep pricing within ~5–10% of competitors and sustain Net Promoter Scores above industry median to limit churn.

Influence of Large Mortgage Lenders

In lender-placed insurance, Assurant serves large banks and mortgage servicers that manage over $10 trillion in US mortgage balances (2024); these clients run formal competitive bids and request detailed loss-run data.

Their power comes from shifting whole portfolios—Assurant lost market share to rivals in 2023 when servicers re-bid, pressuring pricing and tightening SLAs; contract concessions often reduce margins by several percentage points.

Rising Demand for Transparent Claims Processes

Modern consumers in 2025 demand transparent, fast claims experiences set by digital-native rivals; 72% of insurance customers expect real-time updates, per a 2024 McKinsey survey, pushing Assurant to upgrade mobile UX and implement real-time tracking.

Assurant’s tech investments—estimated $120–150M in 2024–25 IT spend—aim to cut claim resolution time by 30%; failure risks rapid market-share loss as convenience beats brand legacy.

- 72% expect real-time updates (McKinsey 2024)

- $120–150M IT spend, 2024–25 (company disclosures)

- Target: −30% claim resolution time

Retailer Leverage in Extended Warranty Segments

Large US retail chains like Best Buy and Costco control prime in-store and online placement for extended warranties, letting them set commission rates that trimmed warranty provider margins by up to 150–300 basis points in 2024; Assurant pays high placement fees to keep shelf space and sales flow.

Assurant competes with Allstate and SquareTrade for these slots, driving sales costs higher—Assurant reported service contract revenue of $2.8B in 2024, but rising retailer fees pressured operating margins.

Customers Dictate Terms: Carriers, Renters & Retailers Squeeze Protection Margins

Customers hold high bargaining power: carriers drove 55–65% of protection revenue in 2024, enabling rate concessions that cut GP% ~150–250 bps; renters switch 42% yearly (J.D. Power 2024) forcing price parity ±5–10%; servicers control $10T+ mortgages (2024) and rebids shifted share in 2023; retailers’ placement trimmed warranty margins 150–300 bps; Assurant spent $120–150M on IT (2024–25) to cut claim time ~30%.

| Metric | Value |

|---|---|

| Carrier share of protection rev (2024) | 55–65% |

| Renters switching (2024) | 42% |

| Retailer margin impact (2024) | 150–300 bps |

| IT spend (2024–25) | $120–150M |

Preview the Actual Deliverable

Assurant Porter's Five Forces Analysis

This preview shows the exact Assurant Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted, professionally written, and ready for use with no placeholders or samples.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Assurant faces moderate buyer power, concentrated suppliers for some tech-driven services, and steady competitive rivalry from insurers and fintech entrants that pressure margins and innovation.

Regulatory scrutiny and capital requirements raise barriers, yet digital disruptors and white-label providers keep the threat of new entrants and substitutes meaningful.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Assurant’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Mobile Original Equipment Manufacturers

Assurant depends on partnerships with Apple and Samsung, which together held ~68% global smartphone market share in 2025, concentrating supplier power and embedment of protection plans into device ecosystems.

These OEMs set proprietary designs and warranty rules that set parts pricing and authorized-repair access, making Assurant's unit repair cost and margins hinge on OEM policies.

By end-2025, few giants' dominance raised exposure: a 2024–25 policy shift could swing Assurant's service costs by an estimated 8–12% per claim, increasing strategic vulnerability.

Reliance on Reinsurance Providers

As a housing and specialty insurer, Assurant shifts large loss exposure to global reinsurers; in 2025 reinsurer bargaining power is high after climate-driven losses tightened capacity and pushed average property-cat reinsurance rates up roughly 30% year-over-year. Assurant can either pay higher ceded-premium costs—squeezing combined ratios—or retain more risk, which would raise required capital and volatility. Moody’s estimated 2024–25 global catastrophe insured losses climbed to about $120 billion, keeping upward pressure on 2025 treaty pricing. Accepting higher reinsurance costs would directly cut Assurant’s underwriting margin unless offset by rate increases or expense savings.

Availability of Skilled Technical Labor

The fulfillment of Assurant extended service contracts for appliances and electronics relies on a vast network of third‑party repair technicians and logistics providers, and in 2025 a documented 18% shortage in specialized technical talent has allowed these suppliers to demand higher fees, raising unit service costs by about 5–8% vs 2023; Assurant must preserve these relationships to keep customer satisfaction high and claims turnaround near its target of <7 days.

Data and Cloud Infrastructure Providers

Assurant’s digital shift ties core mobile-diagnostic and automated-claims workflows to major cloud and analytics vendors, creating heavy reliance on their platforms.

Global hyperscaler fees rose ~18% YoY in 2024; switching cloud providers would mean months of migration and multiyear rearchitecting, so suppliers keep strong pricing leverage over Assurant’s IT budget.

Here’s the quick math: a 10% cloud-cost increase on a $200M annual cloud spend adds $20M to operating costs, directly pressuring margins.

- Dependence: core systems run on hyperscalers

- Switching cost: months–years, high rearchitecture risk

- Pricing power: vendors raised fees ~18% in 2024

- Impact: $200M cloud spend → $20M cost per 10% hike

Automotive Dealership and Repair Networks

Assurant relies on dealership and authorized-repair networks as the primary gateway to sell and service vehicle-protection plans; in 2024 dealers accounted for roughly 65% of policy sales in U.S. vehicle protection channels.

These providers can steer customers to specific plans and, with rising vehicle electronics complexity by 2025, repair shops have pushed reimbursement increases—industry reports show average labor rates up 6–8% and parts surcharges for advanced driver-assistance systems (ADAS) adding $200–$1,200 per repair.

Higher reimbursements squeeze Assurant’s margins unless it renegotiates fees, which is hard because top dealer groups control large local market shares and service bay capacity.

- Dealers = ~65% of U.S. policy distribution (2024)

- Labor rates +6–8% (recent industry data)

- ADAS parts add $200–$1,200 per repair

- Reimbursement pressure reduces Assurant margins

Supplier power squeezes margins: OEMs, hyperscalers, reinsurers drive 8–12% cost swings

Suppliers hold strong power: OEMs (Apple, Samsung ~68% share in 2025) and hyperscalers raised fees ~18% in 2024, while reinsurers pushed reinsurance rates ~30% YoY and global cat losses ~ $120B (2024–25), together risking 8–12% per-claim cost swings and $20M per 10% cloud hike on $200M spend.

| Supplier | 2024–25 metric | Impact on Assurant |

|---|---|---|

| OEMs | Apple+Samsung ~68% market share (2025) | Proprietary parts/pricing → 8–12% cost swing |

| Hyperscalers | Fees +18% (2024) | $200M cloud → $20M/10% increase |

| Reinsurers | Reinsurance rates +30% YoY; global cat losses ~$120B | Higher ceded premiums or retained risk → margin pressure |

What is included in the product

Tailored Porter's Five Forces analysis for Assurant that uncovers competitive drivers, supplier and buyer power, entry barriers, substitution risks, and strategic recommendations to protect market share and profitability.

Assurant Porter's Five Forces one-sheet clarifies competitive pressures in insurance and specialty housing markets, letting you quickly spot threats and opportunities for strategic moves.

Customers Bargaining Power

Concentration of Major Mobile Carrier Partners

A significant portion of Assurant’s revenue comes from a handful of major mobile network operators that bundle device protection with plans; in 2024 carriers accounted for roughly 55–65% of Assurant’s protection revenue, giving these partners outsized leverage. These enterprise customers can push for lower wholesale rates or richer profit-share splits at renewals, squeezing margins; contract concessions in 2023–24 trimmed coverage GP% by an estimated 150–250 basis points. Continued telecom consolidation through 2025—mergers reducing large U.S. carriers to three national players—further limits Assurant’s alternative large-scale partners and raises customer bargaining power.

Low Switching Costs for Individual Policyholders

Individual renters and mobile-protection customers face very low switching costs, with online quote tools letting shoppers compare monthly premiums and deductibles across 10+ providers in minutes; a 2024 J.D. Power study found 42% of renters switched carriers within 12 months when price or service dipped. In 2025’s transparent digital market, Assurant must keep pricing within ~5–10% of competitors and sustain Net Promoter Scores above industry median to limit churn.

Influence of Large Mortgage Lenders

In lender-placed insurance, Assurant serves large banks and mortgage servicers that manage over $10 trillion in US mortgage balances (2024); these clients run formal competitive bids and request detailed loss-run data.

Their power comes from shifting whole portfolios—Assurant lost market share to rivals in 2023 when servicers re-bid, pressuring pricing and tightening SLAs; contract concessions often reduce margins by several percentage points.

Rising Demand for Transparent Claims Processes

Modern consumers in 2025 demand transparent, fast claims experiences set by digital-native rivals; 72% of insurance customers expect real-time updates, per a 2024 McKinsey survey, pushing Assurant to upgrade mobile UX and implement real-time tracking.

Assurant’s tech investments—estimated $120–150M in 2024–25 IT spend—aim to cut claim resolution time by 30%; failure risks rapid market-share loss as convenience beats brand legacy.

- 72% expect real-time updates (McKinsey 2024)

- $120–150M IT spend, 2024–25 (company disclosures)

- Target: −30% claim resolution time

Retailer Leverage in Extended Warranty Segments

Large US retail chains like Best Buy and Costco control prime in-store and online placement for extended warranties, letting them set commission rates that trimmed warranty provider margins by up to 150–300 basis points in 2024; Assurant pays high placement fees to keep shelf space and sales flow.

Assurant competes with Allstate and SquareTrade for these slots, driving sales costs higher—Assurant reported service contract revenue of $2.8B in 2024, but rising retailer fees pressured operating margins.

Customers Dictate Terms: Carriers, Renters & Retailers Squeeze Protection Margins

Customers hold high bargaining power: carriers drove 55–65% of protection revenue in 2024, enabling rate concessions that cut GP% ~150–250 bps; renters switch 42% yearly (J.D. Power 2024) forcing price parity ±5–10%; servicers control $10T+ mortgages (2024) and rebids shifted share in 2023; retailers’ placement trimmed warranty margins 150–300 bps; Assurant spent $120–150M on IT (2024–25) to cut claim time ~30%.

| Metric | Value |

|---|---|

| Carrier share of protection rev (2024) | 55–65% |

| Renters switching (2024) | 42% |

| Retailer margin impact (2024) | 150–300 bps |

| IT spend (2024–25) | $120–150M |

Preview the Actual Deliverable

Assurant Porter's Five Forces Analysis

This preview shows the exact Assurant Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted, professionally written, and ready for use with no placeholders or samples.