Assured Guaranty Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

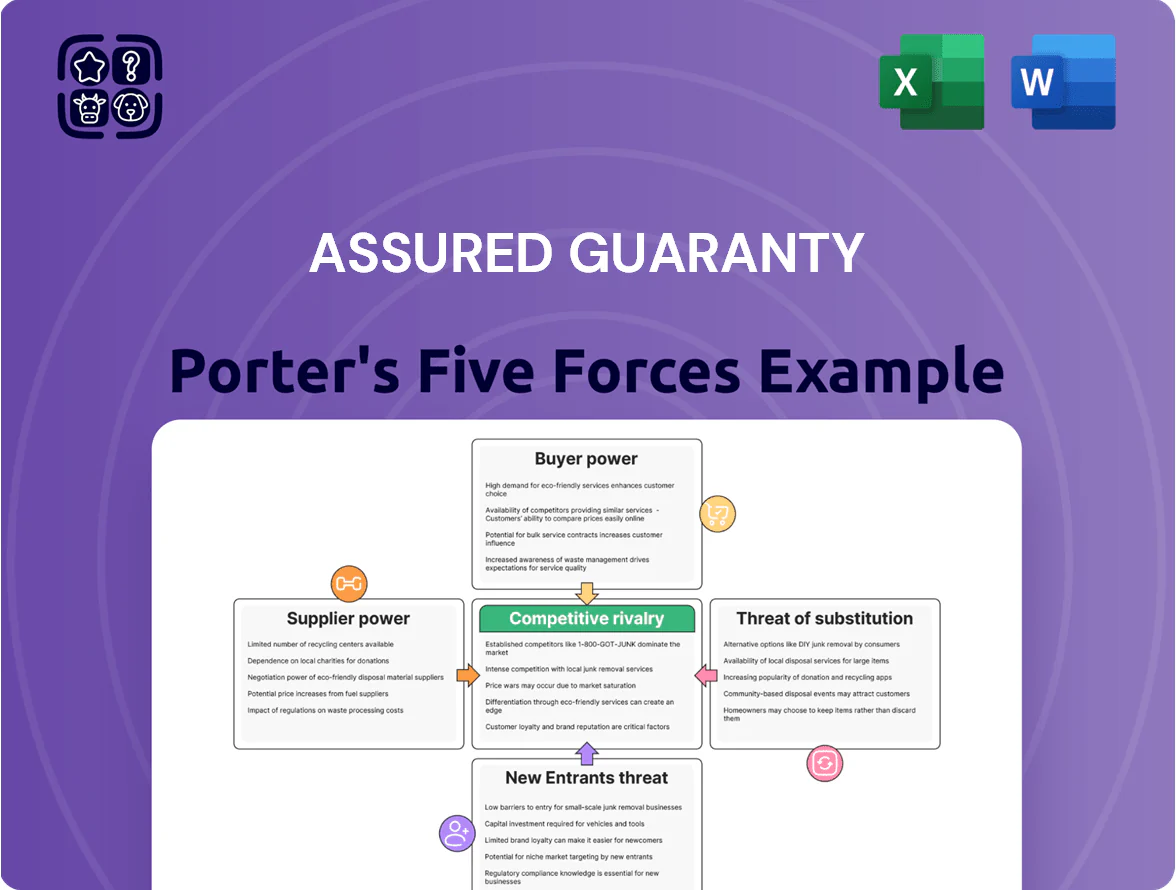

Assured Guaranty faces nuanced competitive pressures—from concentrated buyer power in municipal issuers to regulatory and credit-cycle risks that temper entrant threats—while its guarantee expertise and diversified portfolio underpin resilience; this snapshot scratches the surface. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights tailored to Assured Guaranty’s strategic and investment implications.

Suppliers Bargaining Power

Credit Rating Agencies

Credit ratings from S&P, Moody’s, and Kroll are essential validation for Assured Guaranty’s insurance; as of Dec 31, 2025 S&P A, Moody’s A2 and Kroll A indicate high-grade backing for roughly $50 billion of insured par.

These agencies hold outsized power: a one-notch downgrade historically cuts insured bond market value by ~5–15% and would raise claims funding costs and collateral needs immediately.

Assured must meet agency capital and risk-based requirements—regulatory and rating-model capital targets above $1.5 billion of statutory surplus in 2025—to preserve its business model.

Reinsurance Providers

Assured Guaranty uses reinsurance to cut risk concentration and improve capital efficiency; in 2024 it ceded about 18% of net written premiums, showing reliance on external capacity. Highly rated reinsurance is concentrated among a few global groups (Munich Re, Swiss Re, Berkshire-linked units), so suppliers hold moderate pricing leverage—benchmark treaty rates rose ~12% in 2023–24—affecting Assured’s cost to offload risk and its regulatory capital ratios.

Specialized Financial Talent

The expertise for infrastructure and municipal credit underwriting and risk modeling is highly specialized, and global demand lifted quant and credit analyst pay 14–22% above median finance roles in 2024 (e.g., median quant pay ~$190k in US).

Investment banks, hedge funds, and private equity poach talent, raising bargaining power of this supplier group and pushing Assured Guaranty to match market premiums to compete.

Retaining edge requires hiring staff with deep tax, bond covenants, and conduit knowledge—roles that see 10–15% turnover risk if compensation or training lags.

Capital Market Investors

As a public company, Assured Guaranty relies on debt and equity markets for liquidity and growth capital; in 2024 its debt-to-equity stance and cost of capital reflected investment-grade spreads near 150–250 bps and a stock beta around 1.2, so investor sentiment matters.

Capital providers set rates based on views of the monoline insurance sector and macro risks—rising Treasury yields in 2024 pushed funding costs higher and compressed valuation multiples.

Because market perception of Assured Guaranty’s risk profile alters borrowing rates, equity valuation, and access to capital, these investors hold significant bargaining power over the company’s financial flexibility.

- 2024 credit spreads ~150–250 bps

- stock beta ≈1.2 in 2024

- higher Treasury yields raised funding costs in 2024

Information and Data Providers

Accurate, timely financial data is vital for Assured Guaranty’s actuarial models and risk pricing; vendors like S&P Global and Bloomberg (2024 revenues $12.9B and $12.6B) hold leverage because switching costs and integration with pricing engines are high.

Loss of continuous high-quality feeds would impair loss-reserving and pricing accuracy, raising underwriting risk and capital strain; third-party analytics fees represent a small but critical share of operating costs.

- High dependence on providers

- High switching/integration costs

- Continuous data needed for pricing

- Vendors hold pricing leverage

Suppliers Hold Strong Leverage: Ratings, Reinsurance, Capital & Data Raise Costs

Suppliers (rating agencies, reinsurers, talent, data vendors, capital providers) exert strong to moderate bargaining power—downgrades cut insured value ~5–15%, reinsurance cessions ~18% (2024), treaty rates rose ~12% (2023–24), debt spreads ~150–250 bps (2024), stock beta ~1.2 (2024), and vendor revenues (S&P $12.9B, Bloomberg $12.6B, 2024) reflect high switching costs.

| Supplier | Key metric | 2024–25 figure |

|---|---|---|

| Rating agencies | Downgrade impact | −5–15% insured value |

| Reinsurers | Ceded premiums | 18% (2024) |

| Reinsurance pricing | Rate change | +12% (2023–24) |

| Capital providers | Credit spreads | 150–250 bps (2024) |

| Data vendors | Revenue | S&P $12.9B; Bloomberg $12.6B (2024) |

What is included in the product

Uncovers Assured Guaranty’s competitive strengths and vulnerabilities by analyzing rivalry, buyer and supplier power, threats from entrants and substitutes, and regulatory/disruption risks affecting its municipal bond insurance franchise.

Compact Porter's Five Forces summary for Assured Guaranty—rapidly highlights competitive pressures and risk drivers to expedite credit and strategic decisions.

Customers Bargaining Power

Municipal Bond Issuers

Municipal issuers—cities, states, and local authorities—hold strong bargaining power since they only buy insurance if the wrap cuts net interest cost; in 2024 muni yields fell to ~3.5% (Bloomberg Barclays muni index) so many issuers negotiated lower Assured Guaranty premiums or skipped insurance.

Institutional Bond Investors

Large pension funds and mutual funds often require credit enhancement to meet safety mandates, and in 2024 US public pensions held about $5.6 trillion in assets, giving them heavy buying power. These investors can refuse bonds not wrapped by top-rated insurers, pressuring underwriters to use Assured Guaranty (A+/A1 ratings as of Dec 31, 2024). Their insurer preference boosts demand and lets them influence policy pricing and terms.

Investment Banking Intermediaries

Financial advisors and underwriters act as gatekeepers, steering bond issuers to insurers during deal structuring; in 2024 global bond underwritings totaled about $8.3 trillion, concentrating influence in top banks.

These intermediaries control deal flow and can favor preferred insurers, so Assured Guaranty must secure placement via strong bank relationships; Assured reported $1.1 billion in premium revenue in 2024, so lost access risks meaningful deal exclusion.

Infrastructure Project Developers

Private infrastructure and energy developers need credit enhancement to access long-term, low-cost debt; Assured Guaranty faces clients who demand tailored wrap terms for projects often worth $200M–$2B, raising customer leverage.

These developers shop a small insurer pool, compare pricing, and use project visibility—many are public-facing PPPs or flagged ESG assets—to press for better rates and bespoke covenants, increasing bargaining power.

- High ticket size: $200M–$2B projects

- Few insurers: concentrated supply

- Custom needs: bespoke covenants

- Visibility/ESG: stronger negotiating leverage

Secondary Market Participants

Secondary market investors holding uninsured bonds seek insurance wraps to boost liquidity and ratings, but transact only when the wrap cost is well below the expected uplift in bond price; in 2025 average wrap-sensitive yields tightened by ~15–40 basis points for investment-grade municipals.

This customer group is highly price-sensitive, forcing Assured Guaranty into intense price competition and producing steady yet opportunistic revenue—wraps accounted for roughly 12% of annual revenue in 2024 for comparable guarantors.

Buyers, underwriters, and infra demand compress wrap yields—placement is make-or-break

Customers hold strong bargaining power: muni issuers and large pensions ($5.6T AUM in 2024) push lower premiums; intermediaries control $8.3T global underwritings (2024) gatekeep deals; infra projects ($200M–$2B) demand bespoke wraps; secondary investors tighten yields 15–40 bps (2025). Assured Guaranty earned $1.1B premiums (2024), making placement and pricing critical.

| Metric | 2024–25 |

|---|---|

| Public pension AUM | $5.6T |

| Global underwritings | $8.3T |

| Muni yield (2024) | ~3.5% |

| Assured premiums | $1.1B |

| Wrap yield impact | 15–40 bps (2025) |

What You See Is What You Get

Assured Guaranty Porter's Five Forces Analysis

This preview shows the exact Assured Guaranty Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders, no mockups, fully formatted and ready for use.

You're viewing the actual deliverable: a professionally written, download-ready file that becomes instantly accessible once your purchase is complete.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Assured Guaranty faces nuanced competitive pressures—from concentrated buyer power in municipal issuers to regulatory and credit-cycle risks that temper entrant threats—while its guarantee expertise and diversified portfolio underpin resilience; this snapshot scratches the surface. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights tailored to Assured Guaranty’s strategic and investment implications.

Suppliers Bargaining Power

Credit Rating Agencies

Credit ratings from S&P, Moody’s, and Kroll are essential validation for Assured Guaranty’s insurance; as of Dec 31, 2025 S&P A, Moody’s A2 and Kroll A indicate high-grade backing for roughly $50 billion of insured par.

These agencies hold outsized power: a one-notch downgrade historically cuts insured bond market value by ~5–15% and would raise claims funding costs and collateral needs immediately.

Assured must meet agency capital and risk-based requirements—regulatory and rating-model capital targets above $1.5 billion of statutory surplus in 2025—to preserve its business model.

Reinsurance Providers

Assured Guaranty uses reinsurance to cut risk concentration and improve capital efficiency; in 2024 it ceded about 18% of net written premiums, showing reliance on external capacity. Highly rated reinsurance is concentrated among a few global groups (Munich Re, Swiss Re, Berkshire-linked units), so suppliers hold moderate pricing leverage—benchmark treaty rates rose ~12% in 2023–24—affecting Assured’s cost to offload risk and its regulatory capital ratios.

Specialized Financial Talent

The expertise for infrastructure and municipal credit underwriting and risk modeling is highly specialized, and global demand lifted quant and credit analyst pay 14–22% above median finance roles in 2024 (e.g., median quant pay ~$190k in US).

Investment banks, hedge funds, and private equity poach talent, raising bargaining power of this supplier group and pushing Assured Guaranty to match market premiums to compete.

Retaining edge requires hiring staff with deep tax, bond covenants, and conduit knowledge—roles that see 10–15% turnover risk if compensation or training lags.

Capital Market Investors

As a public company, Assured Guaranty relies on debt and equity markets for liquidity and growth capital; in 2024 its debt-to-equity stance and cost of capital reflected investment-grade spreads near 150–250 bps and a stock beta around 1.2, so investor sentiment matters.

Capital providers set rates based on views of the monoline insurance sector and macro risks—rising Treasury yields in 2024 pushed funding costs higher and compressed valuation multiples.

Because market perception of Assured Guaranty’s risk profile alters borrowing rates, equity valuation, and access to capital, these investors hold significant bargaining power over the company’s financial flexibility.

- 2024 credit spreads ~150–250 bps

- stock beta ≈1.2 in 2024

- higher Treasury yields raised funding costs in 2024

Information and Data Providers

Accurate, timely financial data is vital for Assured Guaranty’s actuarial models and risk pricing; vendors like S&P Global and Bloomberg (2024 revenues $12.9B and $12.6B) hold leverage because switching costs and integration with pricing engines are high.

Loss of continuous high-quality feeds would impair loss-reserving and pricing accuracy, raising underwriting risk and capital strain; third-party analytics fees represent a small but critical share of operating costs.

- High dependence on providers

- High switching/integration costs

- Continuous data needed for pricing

- Vendors hold pricing leverage

Suppliers Hold Strong Leverage: Ratings, Reinsurance, Capital & Data Raise Costs

Suppliers (rating agencies, reinsurers, talent, data vendors, capital providers) exert strong to moderate bargaining power—downgrades cut insured value ~5–15%, reinsurance cessions ~18% (2024), treaty rates rose ~12% (2023–24), debt spreads ~150–250 bps (2024), stock beta ~1.2 (2024), and vendor revenues (S&P $12.9B, Bloomberg $12.6B, 2024) reflect high switching costs.

| Supplier | Key metric | 2024–25 figure |

|---|---|---|

| Rating agencies | Downgrade impact | −5–15% insured value |

| Reinsurers | Ceded premiums | 18% (2024) |

| Reinsurance pricing | Rate change | +12% (2023–24) |

| Capital providers | Credit spreads | 150–250 bps (2024) |

| Data vendors | Revenue | S&P $12.9B; Bloomberg $12.6B (2024) |

What is included in the product

Uncovers Assured Guaranty’s competitive strengths and vulnerabilities by analyzing rivalry, buyer and supplier power, threats from entrants and substitutes, and regulatory/disruption risks affecting its municipal bond insurance franchise.

Compact Porter's Five Forces summary for Assured Guaranty—rapidly highlights competitive pressures and risk drivers to expedite credit and strategic decisions.

Customers Bargaining Power

Municipal Bond Issuers

Municipal issuers—cities, states, and local authorities—hold strong bargaining power since they only buy insurance if the wrap cuts net interest cost; in 2024 muni yields fell to ~3.5% (Bloomberg Barclays muni index) so many issuers negotiated lower Assured Guaranty premiums or skipped insurance.

Institutional Bond Investors

Large pension funds and mutual funds often require credit enhancement to meet safety mandates, and in 2024 US public pensions held about $5.6 trillion in assets, giving them heavy buying power. These investors can refuse bonds not wrapped by top-rated insurers, pressuring underwriters to use Assured Guaranty (A+/A1 ratings as of Dec 31, 2024). Their insurer preference boosts demand and lets them influence policy pricing and terms.

Investment Banking Intermediaries

Financial advisors and underwriters act as gatekeepers, steering bond issuers to insurers during deal structuring; in 2024 global bond underwritings totaled about $8.3 trillion, concentrating influence in top banks.

These intermediaries control deal flow and can favor preferred insurers, so Assured Guaranty must secure placement via strong bank relationships; Assured reported $1.1 billion in premium revenue in 2024, so lost access risks meaningful deal exclusion.

Infrastructure Project Developers

Private infrastructure and energy developers need credit enhancement to access long-term, low-cost debt; Assured Guaranty faces clients who demand tailored wrap terms for projects often worth $200M–$2B, raising customer leverage.

These developers shop a small insurer pool, compare pricing, and use project visibility—many are public-facing PPPs or flagged ESG assets—to press for better rates and bespoke covenants, increasing bargaining power.

- High ticket size: $200M–$2B projects

- Few insurers: concentrated supply

- Custom needs: bespoke covenants

- Visibility/ESG: stronger negotiating leverage

Secondary Market Participants

Secondary market investors holding uninsured bonds seek insurance wraps to boost liquidity and ratings, but transact only when the wrap cost is well below the expected uplift in bond price; in 2025 average wrap-sensitive yields tightened by ~15–40 basis points for investment-grade municipals.

This customer group is highly price-sensitive, forcing Assured Guaranty into intense price competition and producing steady yet opportunistic revenue—wraps accounted for roughly 12% of annual revenue in 2024 for comparable guarantors.

Buyers, underwriters, and infra demand compress wrap yields—placement is make-or-break

Customers hold strong bargaining power: muni issuers and large pensions ($5.6T AUM in 2024) push lower premiums; intermediaries control $8.3T global underwritings (2024) gatekeep deals; infra projects ($200M–$2B) demand bespoke wraps; secondary investors tighten yields 15–40 bps (2025). Assured Guaranty earned $1.1B premiums (2024), making placement and pricing critical.

| Metric | 2024–25 |

|---|---|

| Public pension AUM | $5.6T |

| Global underwritings | $8.3T |

| Muni yield (2024) | ~3.5% |

| Assured premiums | $1.1B |

| Wrap yield impact | 15–40 bps (2025) |

What You See Is What You Get

Assured Guaranty Porter's Five Forces Analysis

This preview shows the exact Assured Guaranty Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders, no mockups, fully formatted and ready for use.

You're viewing the actual deliverable: a professionally written, download-ready file that becomes instantly accessible once your purchase is complete.