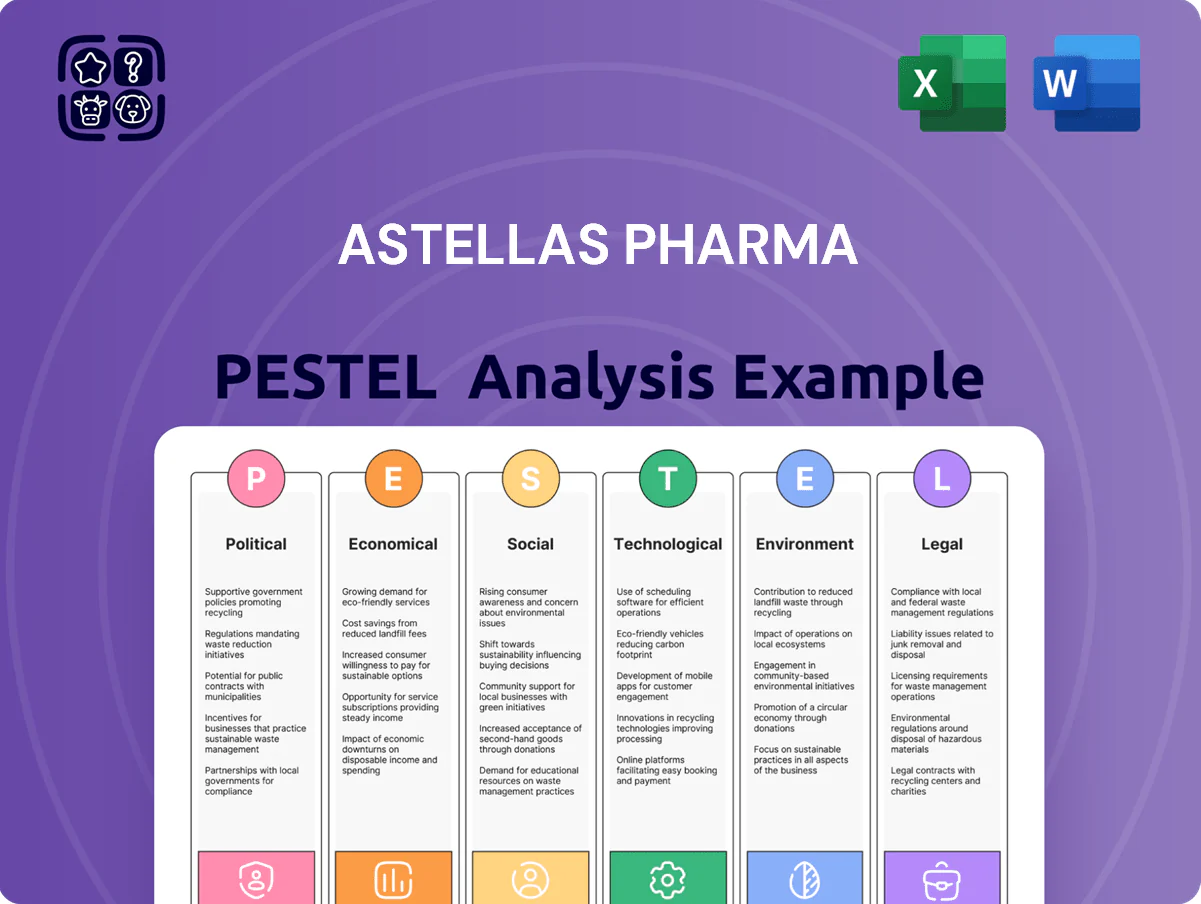

Astellas Pharma PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, regulatory pressures, and rapid biopharma innovation are reshaping Astellas Pharma’s strategy and risk profile—our concise PESTLE highlights the critical external drivers you need to know; purchase the full analysis for detailed, actionable insights and ready-to-use slides to inform your next investment or strategic move.

Political factors

Global drug pricing regulations

Astellas faces rising government-led price controls across the US and EU; Medicare drug-price negotiations under the US Inflation Reduction Act could cut list prices for top-selling therapies, with CMS targeting savings projected at $100+ billion through 2031 for Medicare Part D/Medicare drug spending.

European reference pricing and national cost-effectiveness thresholds (e.g., UK NICE) pressure launch prices and reimbursement, compressing margins on blockbusters that generated ¥1.1 trillion in FY2024 revenue. Decision-makers must track legislative shifts closely as they directly alter long-term revenue forecasts and R&D reinvestment plans.

Geopolitical trade tensions

As a Japanese multinational, Astellas faces heightened risk from US-China trade tensions that in 2024 saw tariffs and export controls impacting pharma intermediates; disruptions helped push global supply‑chain costs up ~8% year‑on‑year in pharmaceutics. Trade barriers and logistics delays can constrain distribution of specialized therapies and sourcing of API precursors, affecting margins given Astellas' ¥2.1 trillion 2024 revenue. Strategic planning therefore emphasizes diversified suppliers across Japan, EU, and Southeast Asia to reduce geopolitical concentration risk.

Government healthcare funding levels

Regulatory harmonization efforts

Regulatory cooperation among FDA, EMA and PMDA—illustrated by the 2024 ICMRA alignment and rising reliance pathways—can shorten multinational approvals; Astellas benefits as cross-agency reliance can cut development timelines and lower per-market regulatory costs.

For Astellas, faster approvals enhance ROI on the Focus Area portfolio: in 2024 Astellas reported ¥1.54 trillion revenue, so even modest 3–6 month accelerations materially improve NPV and earlier global launch revenues.

Investors should monitor policy shifts and pilot reliance programs that enable synchronized submissions and rolling reviews, which directly support quicker scaling into US, EU and Japan markets.

- ICMRA/2024 alignment boosts cross-border reliance

- 3–6 month approval acceleration materially raises NPV

- Astellas 2024 revenue: ¥1.54 trillion—sensitive to launch timing

Intellectual property protection advocacy

Political stability in patent regimes and adherence to treaties like TRIPS are vital for safeguarding Astellas’ R&D outlays—Astellas spent ¥269.8 billion on R&D in FY2024, making strong IP protection crucial to recoup investment.

Weakening IP rights in key emerging markets risks earlier generic entry and revenue erosion from flagship drugs, threatening patent-protected sales that comprised a significant portion of Astellas’ ¥1.60 trillion FY2024 revenue.

Astellas actively lobbies and partners with industry groups to strengthen global IP frameworks, supporting policies that preserve exclusivity periods and incentives for biotech innovation.

- R&D spend FY2024: ¥269.8 billion

- Revenue FY2024: ¥1.60 trillion

- Risk: premature generics from weaker IP regimes

- Action: policy advocacy for robust global IP protections

Astellas faces pricing, supply and policy swings—R&D-heavy 2024; approvals may speed

Astellas faces drug-price controls (US IRA negotiations, EU reference pricing) that can cut revenue; FY2024 revenue ¥1.54–1.60T and R&D ¥269.8B heighten sensitivity to pricing and IP policy. US-China trade tensions and ~8% higher supply costs in 2024 raise sourcing risk. Regulatory reliance (ICMRA 2024) may accelerate approvals 3–6 months, improving NPV and launch timing.

| Metric | 2024 |

|---|---|

| Revenue | ¥1.54–1.60T |

| R&D | ¥269.8B |

| Supply‑chain cost rise | ~8% |

What is included in the product

Explores how macro-environmental factors specifically impact Astellas Pharma across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends highlighting regulatory shifts, reimbursement pressures, R&D innovation, sustainability risks, and market dynamics.

A concise, neatly segmented PESTLE summary for Astellas Pharma that’s easily dropped into presentations or shared across teams to streamline risk discussions and strategic planning.

Economic factors

Currency exchange rate fluctuations

Astellas reports in Japanese yen while roughly 60% of 2024 revenue is from USD and EUR markets, exposing results to FX swings; a 1% JPY appreciation vs USD trimmed FY2024 operating profit by an estimated ¥6–8 billion. Strong fluctuations have produced quarter-to-quarter EPS variance and can erode foreign-market pricing competitiveness, particularly in the US and EU. Analysts should incorporate the company’s cross-currency hedging (noted hedged volumes ~40–50% in 2024) when modeling net income and valuation.

High research and development costs

The shift to cell and gene therapies forces Astellas to absorb R&D costs often exceeding $1 billion per program, raising project-level failure risk and capex needs; industry median phase III attrition remains ~50%, amplifying expected losses.

Higher upfront spending in 2024–25 depressed Astellas’ short-term liquidity and pressured EBITDA margins, with R&D expense rising to ¥434.9 billion in FY2024 (approx $3.0bn), up from ¥384.6bn in FY2022.

Long-term value hinges on R&D productivity: breakeven requires more efficient clinical translation and higher peak sales per asset to justify stage-gate investments in complex modalities.

Inflationary impact on operational costs

Rising energy prices (global industrial electricity up ~18% in 2023–24) and higher costs for specialized biopharma labor (wage inflation ~6–8% in 2024) plus a >10% rise in key lab consumables since 2022 push Astellas' OPEX upward.

Although Astellas holds pricing power for oncology and transplant drugs, government payer price controls and rebates mean rapid inflation can erode margins if price adjustments lag.

Maintaining 2024 operating margin targets therefore requires intensified operational excellence, procurement optimization, and cost-reduction programs to offset input-cost inflation.

Interest rate environment

The prevailing interest rate environment affects Astellas Pharma’s cost of debt, with Japan’s policy rate at -0.1% (BoJ) and US Fed funds at 5.25–5.50% (Feb 2025), influencing cross-border borrowing costs for acquisitions and capex.

Higher global rates push Astellas toward conservative M&A and capital projects, raising weighted average borrowing costs and potentially delaying deals.

Strategists must track central bank guidance to forecast financing costs and available investment capacity.

- BoJ rate -0.1% (2025)

- US Fed 5.25–5.50% (Feb 2025)

- Higher rates → tighter M&A, slower capex

Emerging market growth potential

Emerging market growth in Southeast Asia and Latin America—projected GDP growth of ~4.5–5.0% in 2024–25 and middle-class expansion to ~1.8 billion by 2030—offers Astellas volume upside, especially in generics and chronic therapies, but average per-capita health spending remains low (e.g., Mexico ~$1,100, Indonesia ~$120 in 2023), pressuring revenue per unit.

Astellas must balance volume penetration with value-based pricing and risk management amid currency volatility, political risk, and lower reimbursement levels, targeting portfolio segmentation and tiered pricing to protect margins.

- Regional GDP growth ~4.5–5.0% (2024–25)

- Middle class ~1.8B by 2030

- Per-capita health spend: Mexico ~$1,100; Indonesia ~$120 (2023)

- Need for tiered pricing, portfolio segmentation, and risk hedging

JPY swings, rising R&D and costs squeeze margins; FX, rates cap M&A/capex

FX exposure (60% revenue USD/EUR) and ~40–50% hedged volumes in 2024 make JPY moves material (1% JPY↑ vs USD ≈ ¥6–8bn OP impact); R&D rose to ¥434.9bn (FY2024) driving margin pressure amid >50% phase‑III attrition; rising input costs (energy +18% 2023–24, wages +6–8% 2024) and higher global rates (BoJ -0.1% 2025, US 5.25–5.50% Feb 2025) constrain M&A and capex.

| Metric | Value |

|---|---|

| FY2024 R&D | ¥434.9bn (~$3.0bn) |

| FX exposure USD/EUR | ~60% |

| Hedged volumes 2024 | ~40–50% |

| Energy increase | ~18% (2023–24) |

| Wage inflation 2024 | ~6–8% |

| BoJ policy rate | -0.1% (2025) |

| US Fed funds | 5.25–5.50% (Feb 2025) |

Preview Before You Purchase

Astellas Pharma PESTLE Analysis

The preview shown here is the exact Astellas Pharma PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or investment decisions.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, regulatory pressures, and rapid biopharma innovation are reshaping Astellas Pharma’s strategy and risk profile—our concise PESTLE highlights the critical external drivers you need to know; purchase the full analysis for detailed, actionable insights and ready-to-use slides to inform your next investment or strategic move.

Political factors

Global drug pricing regulations

Astellas faces rising government-led price controls across the US and EU; Medicare drug-price negotiations under the US Inflation Reduction Act could cut list prices for top-selling therapies, with CMS targeting savings projected at $100+ billion through 2031 for Medicare Part D/Medicare drug spending.

European reference pricing and national cost-effectiveness thresholds (e.g., UK NICE) pressure launch prices and reimbursement, compressing margins on blockbusters that generated ¥1.1 trillion in FY2024 revenue. Decision-makers must track legislative shifts closely as they directly alter long-term revenue forecasts and R&D reinvestment plans.

Geopolitical trade tensions

As a Japanese multinational, Astellas faces heightened risk from US-China trade tensions that in 2024 saw tariffs and export controls impacting pharma intermediates; disruptions helped push global supply‑chain costs up ~8% year‑on‑year in pharmaceutics. Trade barriers and logistics delays can constrain distribution of specialized therapies and sourcing of API precursors, affecting margins given Astellas' ¥2.1 trillion 2024 revenue. Strategic planning therefore emphasizes diversified suppliers across Japan, EU, and Southeast Asia to reduce geopolitical concentration risk.

Government healthcare funding levels

Regulatory harmonization efforts

Regulatory cooperation among FDA, EMA and PMDA—illustrated by the 2024 ICMRA alignment and rising reliance pathways—can shorten multinational approvals; Astellas benefits as cross-agency reliance can cut development timelines and lower per-market regulatory costs.

For Astellas, faster approvals enhance ROI on the Focus Area portfolio: in 2024 Astellas reported ¥1.54 trillion revenue, so even modest 3–6 month accelerations materially improve NPV and earlier global launch revenues.

Investors should monitor policy shifts and pilot reliance programs that enable synchronized submissions and rolling reviews, which directly support quicker scaling into US, EU and Japan markets.

- ICMRA/2024 alignment boosts cross-border reliance

- 3–6 month approval acceleration materially raises NPV

- Astellas 2024 revenue: ¥1.54 trillion—sensitive to launch timing

Intellectual property protection advocacy

Political stability in patent regimes and adherence to treaties like TRIPS are vital for safeguarding Astellas’ R&D outlays—Astellas spent ¥269.8 billion on R&D in FY2024, making strong IP protection crucial to recoup investment.

Weakening IP rights in key emerging markets risks earlier generic entry and revenue erosion from flagship drugs, threatening patent-protected sales that comprised a significant portion of Astellas’ ¥1.60 trillion FY2024 revenue.

Astellas actively lobbies and partners with industry groups to strengthen global IP frameworks, supporting policies that preserve exclusivity periods and incentives for biotech innovation.

- R&D spend FY2024: ¥269.8 billion

- Revenue FY2024: ¥1.60 trillion

- Risk: premature generics from weaker IP regimes

- Action: policy advocacy for robust global IP protections

Astellas faces pricing, supply and policy swings—R&D-heavy 2024; approvals may speed

Astellas faces drug-price controls (US IRA negotiations, EU reference pricing) that can cut revenue; FY2024 revenue ¥1.54–1.60T and R&D ¥269.8B heighten sensitivity to pricing and IP policy. US-China trade tensions and ~8% higher supply costs in 2024 raise sourcing risk. Regulatory reliance (ICMRA 2024) may accelerate approvals 3–6 months, improving NPV and launch timing.

| Metric | 2024 |

|---|---|

| Revenue | ¥1.54–1.60T |

| R&D | ¥269.8B |

| Supply‑chain cost rise | ~8% |

What is included in the product

Explores how macro-environmental factors specifically impact Astellas Pharma across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends highlighting regulatory shifts, reimbursement pressures, R&D innovation, sustainability risks, and market dynamics.

A concise, neatly segmented PESTLE summary for Astellas Pharma that’s easily dropped into presentations or shared across teams to streamline risk discussions and strategic planning.

Economic factors

Currency exchange rate fluctuations

Astellas reports in Japanese yen while roughly 60% of 2024 revenue is from USD and EUR markets, exposing results to FX swings; a 1% JPY appreciation vs USD trimmed FY2024 operating profit by an estimated ¥6–8 billion. Strong fluctuations have produced quarter-to-quarter EPS variance and can erode foreign-market pricing competitiveness, particularly in the US and EU. Analysts should incorporate the company’s cross-currency hedging (noted hedged volumes ~40–50% in 2024) when modeling net income and valuation.

High research and development costs

The shift to cell and gene therapies forces Astellas to absorb R&D costs often exceeding $1 billion per program, raising project-level failure risk and capex needs; industry median phase III attrition remains ~50%, amplifying expected losses.

Higher upfront spending in 2024–25 depressed Astellas’ short-term liquidity and pressured EBITDA margins, with R&D expense rising to ¥434.9 billion in FY2024 (approx $3.0bn), up from ¥384.6bn in FY2022.

Long-term value hinges on R&D productivity: breakeven requires more efficient clinical translation and higher peak sales per asset to justify stage-gate investments in complex modalities.

Inflationary impact on operational costs

Rising energy prices (global industrial electricity up ~18% in 2023–24) and higher costs for specialized biopharma labor (wage inflation ~6–8% in 2024) plus a >10% rise in key lab consumables since 2022 push Astellas' OPEX upward.

Although Astellas holds pricing power for oncology and transplant drugs, government payer price controls and rebates mean rapid inflation can erode margins if price adjustments lag.

Maintaining 2024 operating margin targets therefore requires intensified operational excellence, procurement optimization, and cost-reduction programs to offset input-cost inflation.

Interest rate environment

The prevailing interest rate environment affects Astellas Pharma’s cost of debt, with Japan’s policy rate at -0.1% (BoJ) and US Fed funds at 5.25–5.50% (Feb 2025), influencing cross-border borrowing costs for acquisitions and capex.

Higher global rates push Astellas toward conservative M&A and capital projects, raising weighted average borrowing costs and potentially delaying deals.

Strategists must track central bank guidance to forecast financing costs and available investment capacity.

- BoJ rate -0.1% (2025)

- US Fed 5.25–5.50% (Feb 2025)

- Higher rates → tighter M&A, slower capex

Emerging market growth potential

Emerging market growth in Southeast Asia and Latin America—projected GDP growth of ~4.5–5.0% in 2024–25 and middle-class expansion to ~1.8 billion by 2030—offers Astellas volume upside, especially in generics and chronic therapies, but average per-capita health spending remains low (e.g., Mexico ~$1,100, Indonesia ~$120 in 2023), pressuring revenue per unit.

Astellas must balance volume penetration with value-based pricing and risk management amid currency volatility, political risk, and lower reimbursement levels, targeting portfolio segmentation and tiered pricing to protect margins.

- Regional GDP growth ~4.5–5.0% (2024–25)

- Middle class ~1.8B by 2030

- Per-capita health spend: Mexico ~$1,100; Indonesia ~$120 (2023)

- Need for tiered pricing, portfolio segmentation, and risk hedging

JPY swings, rising R&D and costs squeeze margins; FX, rates cap M&A/capex

FX exposure (60% revenue USD/EUR) and ~40–50% hedged volumes in 2024 make JPY moves material (1% JPY↑ vs USD ≈ ¥6–8bn OP impact); R&D rose to ¥434.9bn (FY2024) driving margin pressure amid >50% phase‑III attrition; rising input costs (energy +18% 2023–24, wages +6–8% 2024) and higher global rates (BoJ -0.1% 2025, US 5.25–5.50% Feb 2025) constrain M&A and capex.

| Metric | Value |

|---|---|

| FY2024 R&D | ¥434.9bn (~$3.0bn) |

| FX exposure USD/EUR | ~60% |

| Hedged volumes 2024 | ~40–50% |

| Energy increase | ~18% (2023–24) |

| Wage inflation 2024 | ~6–8% |

| BoJ policy rate | -0.1% (2025) |

| US Fed funds | 5.25–5.50% (Feb 2025) |

Preview Before You Purchase

Astellas Pharma PESTLE Analysis

The preview shown here is the exact Astellas Pharma PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or investment decisions.