Astronics SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

Astronics shows resilient aerospace niche expertise and diversified product lines, but faces cyclic defense and commercial aerospace demand and margin pressure from component costs; regulatory exposure and integration risks could temper growth. Discover the full SWOT analysis for data-driven insights, scenario impact, and an editable Word/Excel package to support investment, strategy, or M&A planning—available for purchase now.

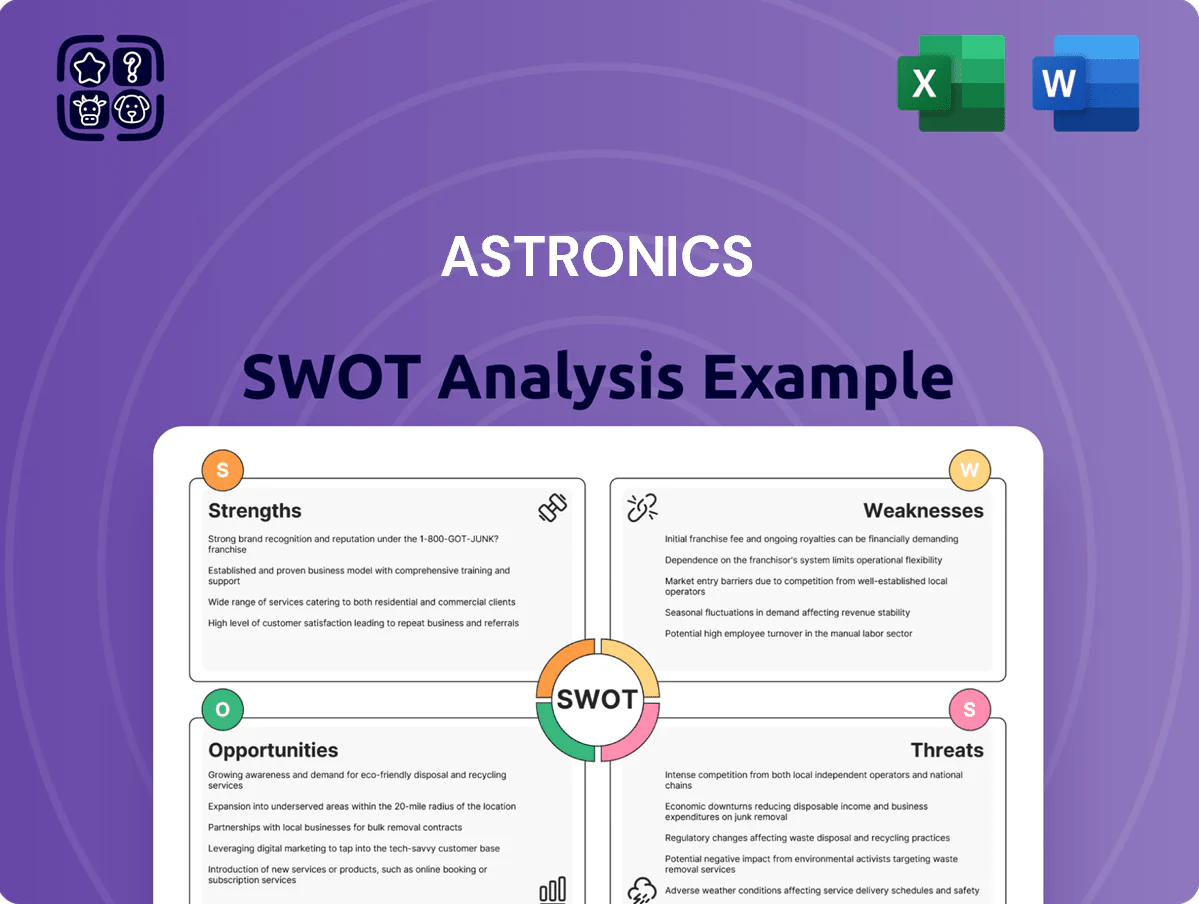

Strengths

Dominant Market Leadership in In-Seat Power

Astronics holds a commanding share of the global in-seat power market, equipping power systems on an estimated 60–70% of active narrowbody and widebody commercial jets as of 2025, which drives recurring revenue from OEMs and retrofit programs.

Their proprietary Intelligent Power Management system improves cabin energy distribution, supporting up to 120W per seat in dense layouts and reducing peak loads by ~25%, which customers cite as a key differentiation.

This market leadership produces steady aftermarket service revenue—Astronics reported 2024 connectivity and power segment sales of $220 million—and creates a strong switching moat given retrofit costs and certification timelines.

Extensive Intellectual Property and Engineering Expertise

Astronics holds a deep portfolio of patents and proprietary tech across aircraft lighting, power generation, and automated test systems, supporting 2024 revenue of $793 million and R&D spend of $42 million. Their engineering teams solve complex integration tasks that boost aircraft performance and passenger experience, evidenced by >150 issued patents and multi-year OEM programs. This technical depth keeps high barriers to entry versus smaller rivals in mission-critical aerospace niches.

Deep-Rooted Relationships with Global OEMs

Astronics maintains multi-decade contracts with OEMs like Boeing and Airbus and key defense primes, securing design-phase integration that drives life-of-airframe revenue; for example, 2024 aftermarket and OEM programs contributed roughly 68% of consolidated sales per the 2024 10-K. These ties lock in recurring production runs and spare-parts demand, backed by certifications and on-time delivery rates above industry targets, helping sustain predictable cash flow and margin stability.

Diversified Revenue Across Commercial and Defense Segments

The business mixes cyclical commercial aerospace sales with steady defense contracts; in 2024 defense orders made up ~43% of Astronics Corporation’s $640M revenue, cushioning commercial travel downturns.

Supplying automated test equipment for military electronics and specialized defense power systems helps sustain cash flow and R&D spend, supporting a 2024 R&D investment of about $18M despite market cycles.

Comprehensive Regulatory and Certification Experience

Astronics’ deep experience with FAA, EASA, and military certifications shortens avg. certification timelines, cutting time-to-market by an estimated 20–30% versus new entrants; that reduced delay risk supported 2024 product launches that helped drive company revenue of $704.6M in fiscal 2024.

This institutional know-how is critical as regulators tighten safety and environmental rules through end-2025, lowering program slip risk and protecting margins on new avionics and cabin systems.

- Proven FAA/EASA/military pathways

- 20–30% faster certification vs startups

- Supports 2024 revenue: $704.6M

- Mitigates 2025 regulatory tightening risk

Astronics: Dominant In‑Seat Power (60–70%) Driving $704M Revenue, $220M Connectivity

Astronics leads in-seat power (60–70% fleet share, 2025), drives recurring OEM/retrofit revenue, and reported 2024 consolidated revenue ≈$704.6M with strong connectivity/power sales of $220M; defense steadies results (≈43% of 2024 revenue) while R&D ($42M total, ~$18M defense-related) and >150 patents sustain high entry barriers and faster FAA/EASA certification (20–30% quicker).

| Metric | Value (2024/2025) |

|---|---|

| Total revenue | $704.6M |

| Connectivity & power sales | $220M |

| Defense share | ≈43% |

| In-seat power fleet share | 60–70% (2025) |

| R&D spend | $42M (total), $18M defense |

| Patents | >150 issued |

| Faster certification | 20–30% |

What is included in the product

Provides a clear SWOT framework for analyzing Astronics’s business strategy by mapping its operational strengths and weaknesses alongside market opportunities and risks.

Provides a concise, visual SWOT matrix for Astronics that speeds stakeholder alignment and simplifies executive decision-making.

Weaknesses

High Sensitivity to Commercial Aviation Cycles

Reliance on Major Aircraft Production Rates

Astronics' revenue swings with production at Boeing and Airbus, which accounted for roughly 45% of 2024 sales; cuts or slowdowns in narrow-body lines (A320, 737) or wide-body programs immediately reduce component shipments. Delays like the 2023 Boeing 737 production adjustments and Airbus A350 supply issues trimmed industry output by mid-single digits, amplifying Astronics' quarter-to-quarter volatility. Internal problems at either OEM can therefore hit Astronics' EBITDA and cash flow disproportionately.

Elevated Debt Levels and Interest Expenses

Despite management’s push to deleverage, Astronics Corporation carried about $218 million of long-term debt at fiscal 2024 year-end (Sept 30, 2024), and net leverage (net debt/EBITDA) stood near 2.0x, so higher interest rates would raise annual interest expense (was $18.6M in FY2024) and squeeze cash available for R&D, making disciplined cash-flow management and steady operational execution critical to restore a healthier balance sheet.

Operational Margin Pressure from Rising Costs

Astronics faces operating margin pressure as specialized-material and skilled-labor costs rose: raw material input inflation hit aerospace suppliers ~6.5% in 2024, and Astronics’ 2024 gross margin fell to 19.8% from 22.4% in 2022.

As a mid-tier supplier, Astronics has limited pricing power versus OEMs and airlines, forcing ongoing efficiency drives to avoid further margin erosion in a competitive manufacturing market.

- 2024 gross margin 19.8%

- Industry input inflation ~6.5% (2024)

- Skilled labor wage growth ~5% (2023–24)

Geographic Concentration of Manufacturing

- ~65% production capacity in limited regions (FY2024)

- Similar outages have caused ~12% revenue drops historically

- Higher disruption risk vs. geographically diversified competitors

Astronics: High OEM & Commercial Aviation Reliance, Rising Leverage & Disruption Risk

Astronics depends heavily on commercial aviation (62% of $590M 2024 revenue) and Boeing/Airbus (≈45% of sales), causing sharp revenue and earnings volatility; FY2024 net leverage ≈2.0x with $218M long-term debt and $18.6M interest expense; 2024 gross margin 19.8% (down from 22.4% in 2022); ~65% production capacity concentrated regionally, raising disruption risk.

| Metric | 2024 |

|---|---|

| Revenue | $590M |

| Commercial aviation % | 62% |

| OEM exposure | ~45% |

| Long-term debt | $218M |

| Net leverage | ~2.0x |

| Interest expense | $18.6M |

| Gross margin | 19.8% |

| Regional capacity | ~65% |

Preview Before You Purchase

Astronics SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the content shown is a real excerpt from the complete document. Once purchased, you’ll receive the full, editable version and immediate access to the entire, detailed report. You’re viewing a live preview of the actual file; the complete version becomes available after checkout.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete SWOT Report

Astronics shows resilient aerospace niche expertise and diversified product lines, but faces cyclic defense and commercial aerospace demand and margin pressure from component costs; regulatory exposure and integration risks could temper growth. Discover the full SWOT analysis for data-driven insights, scenario impact, and an editable Word/Excel package to support investment, strategy, or M&A planning—available for purchase now.

Strengths

Dominant Market Leadership in In-Seat Power

Astronics holds a commanding share of the global in-seat power market, equipping power systems on an estimated 60–70% of active narrowbody and widebody commercial jets as of 2025, which drives recurring revenue from OEMs and retrofit programs.

Their proprietary Intelligent Power Management system improves cabin energy distribution, supporting up to 120W per seat in dense layouts and reducing peak loads by ~25%, which customers cite as a key differentiation.

This market leadership produces steady aftermarket service revenue—Astronics reported 2024 connectivity and power segment sales of $220 million—and creates a strong switching moat given retrofit costs and certification timelines.

Extensive Intellectual Property and Engineering Expertise

Astronics holds a deep portfolio of patents and proprietary tech across aircraft lighting, power generation, and automated test systems, supporting 2024 revenue of $793 million and R&D spend of $42 million. Their engineering teams solve complex integration tasks that boost aircraft performance and passenger experience, evidenced by >150 issued patents and multi-year OEM programs. This technical depth keeps high barriers to entry versus smaller rivals in mission-critical aerospace niches.

Deep-Rooted Relationships with Global OEMs

Astronics maintains multi-decade contracts with OEMs like Boeing and Airbus and key defense primes, securing design-phase integration that drives life-of-airframe revenue; for example, 2024 aftermarket and OEM programs contributed roughly 68% of consolidated sales per the 2024 10-K. These ties lock in recurring production runs and spare-parts demand, backed by certifications and on-time delivery rates above industry targets, helping sustain predictable cash flow and margin stability.

Diversified Revenue Across Commercial and Defense Segments

The business mixes cyclical commercial aerospace sales with steady defense contracts; in 2024 defense orders made up ~43% of Astronics Corporation’s $640M revenue, cushioning commercial travel downturns.

Supplying automated test equipment for military electronics and specialized defense power systems helps sustain cash flow and R&D spend, supporting a 2024 R&D investment of about $18M despite market cycles.

Comprehensive Regulatory and Certification Experience

Astronics’ deep experience with FAA, EASA, and military certifications shortens avg. certification timelines, cutting time-to-market by an estimated 20–30% versus new entrants; that reduced delay risk supported 2024 product launches that helped drive company revenue of $704.6M in fiscal 2024.

This institutional know-how is critical as regulators tighten safety and environmental rules through end-2025, lowering program slip risk and protecting margins on new avionics and cabin systems.

- Proven FAA/EASA/military pathways

- 20–30% faster certification vs startups

- Supports 2024 revenue: $704.6M

- Mitigates 2025 regulatory tightening risk

Astronics: Dominant In‑Seat Power (60–70%) Driving $704M Revenue, $220M Connectivity

Astronics leads in-seat power (60–70% fleet share, 2025), drives recurring OEM/retrofit revenue, and reported 2024 consolidated revenue ≈$704.6M with strong connectivity/power sales of $220M; defense steadies results (≈43% of 2024 revenue) while R&D ($42M total, ~$18M defense-related) and >150 patents sustain high entry barriers and faster FAA/EASA certification (20–30% quicker).

| Metric | Value (2024/2025) |

|---|---|

| Total revenue | $704.6M |

| Connectivity & power sales | $220M |

| Defense share | ≈43% |

| In-seat power fleet share | 60–70% (2025) |

| R&D spend | $42M (total), $18M defense |

| Patents | >150 issued |

| Faster certification | 20–30% |

What is included in the product

Provides a clear SWOT framework for analyzing Astronics’s business strategy by mapping its operational strengths and weaknesses alongside market opportunities and risks.

Provides a concise, visual SWOT matrix for Astronics that speeds stakeholder alignment and simplifies executive decision-making.

Weaknesses

High Sensitivity to Commercial Aviation Cycles

Reliance on Major Aircraft Production Rates

Astronics' revenue swings with production at Boeing and Airbus, which accounted for roughly 45% of 2024 sales; cuts or slowdowns in narrow-body lines (A320, 737) or wide-body programs immediately reduce component shipments. Delays like the 2023 Boeing 737 production adjustments and Airbus A350 supply issues trimmed industry output by mid-single digits, amplifying Astronics' quarter-to-quarter volatility. Internal problems at either OEM can therefore hit Astronics' EBITDA and cash flow disproportionately.

Elevated Debt Levels and Interest Expenses

Despite management’s push to deleverage, Astronics Corporation carried about $218 million of long-term debt at fiscal 2024 year-end (Sept 30, 2024), and net leverage (net debt/EBITDA) stood near 2.0x, so higher interest rates would raise annual interest expense (was $18.6M in FY2024) and squeeze cash available for R&D, making disciplined cash-flow management and steady operational execution critical to restore a healthier balance sheet.

Operational Margin Pressure from Rising Costs

Astronics faces operating margin pressure as specialized-material and skilled-labor costs rose: raw material input inflation hit aerospace suppliers ~6.5% in 2024, and Astronics’ 2024 gross margin fell to 19.8% from 22.4% in 2022.

As a mid-tier supplier, Astronics has limited pricing power versus OEMs and airlines, forcing ongoing efficiency drives to avoid further margin erosion in a competitive manufacturing market.

- 2024 gross margin 19.8%

- Industry input inflation ~6.5% (2024)

- Skilled labor wage growth ~5% (2023–24)

Geographic Concentration of Manufacturing

- ~65% production capacity in limited regions (FY2024)

- Similar outages have caused ~12% revenue drops historically

- Higher disruption risk vs. geographically diversified competitors

Astronics: High OEM & Commercial Aviation Reliance, Rising Leverage & Disruption Risk

Astronics depends heavily on commercial aviation (62% of $590M 2024 revenue) and Boeing/Airbus (≈45% of sales), causing sharp revenue and earnings volatility; FY2024 net leverage ≈2.0x with $218M long-term debt and $18.6M interest expense; 2024 gross margin 19.8% (down from 22.4% in 2022); ~65% production capacity concentrated regionally, raising disruption risk.

| Metric | 2024 |

|---|---|

| Revenue | $590M |

| Commercial aviation % | 62% |

| OEM exposure | ~45% |

| Long-term debt | $218M |

| Net leverage | ~2.0x |

| Interest expense | $18.6M |

| Gross margin | 19.8% |

| Regional capacity | ~65% |

Preview Before You Purchase

Astronics SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the content shown is a real excerpt from the complete document. Once purchased, you’ll receive the full, editable version and immediate access to the entire, detailed report. You’re viewing a live preview of the actual file; the complete version becomes available after checkout.