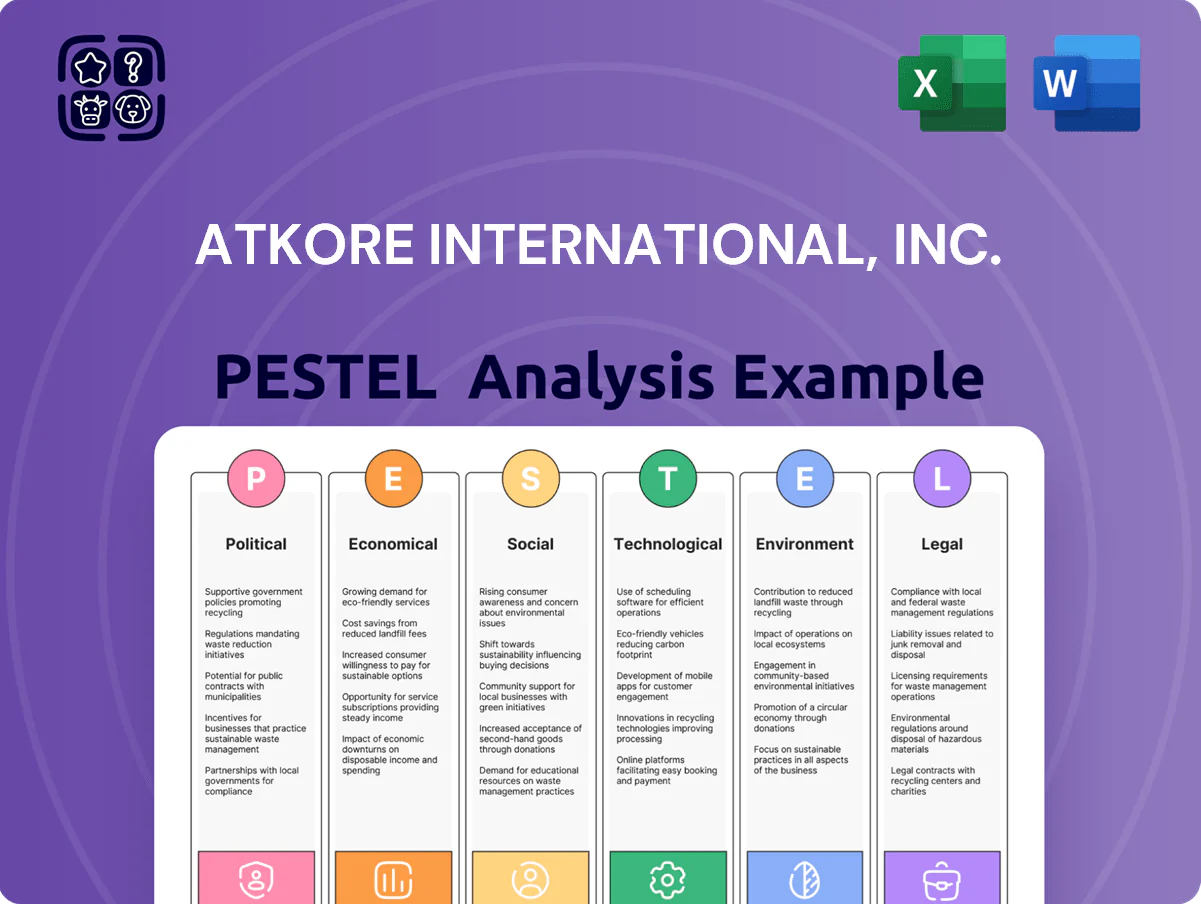

Atkore International, Inc. PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Atkore International, Inc. faces shifting regulatory, economic, and technological forces that will shape its supply chain resilience and product innovation; our concise PESTLE highlights these drivers and their strategic implications. Gain a competitive edge with the full, ready-to-use PESTLE Analysis—designed for investors and strategists—and download it now for actionable, editable insights.

Political factors

Infrastructure Spending Legislation

The Infrastructure Investment and Jobs Act disbursements continued to drive Atkore into late 2025, with federal project allocations—about $110B for grid and $65B for broadband—supporting steady demand for electrical conduits and cable management systems.

Atkore’s FY2024 U.S. infrastructure-related revenue exposure was estimated at ~20–25% of sales, and ongoing multi-year federal commitments help offset private construction cyclicality, stabilizing backlog and near-term cash flow.

Trade Policy and Tariffs

Changes in trade agreements and tariffs on imported steel and aluminum have raised Atkore's input costs; US Section 232 tariffs and 2024-25 antidumping measures increased US metal prices by roughly 15–25%, pressuring margins given Atkore's FY2024 cost of goods sold of $2.1B.

Energy Independence Initiatives

Government mandates to boost domestic energy security—such as US targets to triple solar capacity to ~300 GW by 2030—favor Atkore’s solar mounting and electrical distribution products, supporting potential revenue growth in related segments; expanded federal funding (Inflation Reduction Act, IIJA) and grid modernization spending projected at $65–$120 billion through 2030 create high-volume demand for infrastructure components; Buy American incentives and prevailing-wage requirements improve Atkore’s win rate for public utility contracts, enhancing backlog visibility and margin stability.

Taxation and Fiscal Policy

Corporate tax rates and accelerated depreciation schedules shape capex timing for Atkore’s industrial customers; faster bonus depreciation (100% through 2022, phased later) historically boosted upgrades, and current 2024 effective combined US federal-state rate ~25–27% affects ROI calculations.

Fiscal policy shifts at end-2025—projected corporate tax proposals could change Atkore’s net income by an estimated mid-single-digit percentage and alter cash available for M&A financing tied to EBITDA multiples.

Investors track tax credits for domestic manufacturing and advanced manufacturing R&D; recent Inflation Reduction Act provisions and 2024/2025 R&D credit usage materially influence valuation assumptions.

- US effective tax rate ~25–27%

- Bonus depreciation phased after 2022, affecting capex timing

- End-2025 fiscal changes could move net income mid-single-digit %

- IRA and R&D credits (2024–2025) impact valuation and M&A funding

Geopolitical Stability

While Atkore is North America–focused, 2024 metal price swings—copper up ~8% YTD and aluminum volatile amid supply disruptions—show geopolitical tensions drive input costs and logistics delays.

Instability in chokepoints like the Red Sea raised freight rates by over 30% in 2023–24, forcing Atkore to adjust pricing cadence and margins.

Political stability in secondary markets (EMEA, APAC offices) is critical to Atkore’s 5–7% international revenue growth targets and long‑term expansion.

- Geopolitical-driven metal price volatility impacts margins

- Shipping disruptions raised freight costs ~30% (2023–24)

- Frequent pricing adjustments needed to protect margins

- Stable secondary markets essential for 5–7% international growth

Infrastructure demand offsets tariff, tax and freight headwinds—FY24 revenue/backlog resilient

Federal infrastructure funding (IIJA/IRA) and Buy American rules support ~20–25% FY2024 revenue exposure and backlog; tariffs raised metal costs ~15–25%, pressuring FY2024 COGS $2.1B; US effective tax ~25–27% with end‑2025 fiscal proposals potentially shifting net income mid-single digits; shipping disruptions lifted freight >30% (2023–24), affecting margins and pricing cadence.

| Metric | Value |

|---|---|

| FY2024 infra revenue exposure | 20–25% |

| FY2024 COGS | $2.1B |

| Metal tariff impact | +15–25% |

| US effective tax rate (2024) | 25–27% |

| Freight increase (2023–24) | +30%+ |

What is included in the product

Explores how macro-environmental forces — Political, Economic, Social, Technological, Environmental, and Legal — specifically impact Atkore International, Inc., with data-driven insights and forward-looking implications for risk mitigation and strategic opportunity identification.

A concise PESTLE snapshot of Atkore International that highlights regulatory, economic, technological, environmental, and social risks and opportunities for quick inclusion in presentations or team briefings.

Economic factors

Interest Rate Environment

The late-2025 Fed funds rate near 5.25–5.50% tightened borrowing costs, contributing to a 12% year-over-year decline in U.S. housing starts in Q4 2025 and a 6% drop in nonresidential construction spending, reducing demand for Atkore’s electrical and mechanical infrastructure products.

Commodity Price Volatility

Atkore’s profitability is highly sensitive to steel, PVC and copper prices; steel surged ~18% YoY in 2024 while copper averaged $9,500/ton in 2025, pressuring gross margins. Fluctuations force sophisticated hedging—Atkore reported hedges covering roughly 60% of expected exposure in FY2024—and reliance on dynamic pricing to pass costs to customers. By late 2025, improved supply chains reduced extreme spikes, but commodity-driven inflation (core materials up ~6–8% in 2025) remains a central risk.

Labor Market Dynamics

Persistent labor shortages in construction and manufacturing slow installations of Atkore’s conduit and cable management systems, with the US construction sector facing a 2025 skilled labor gap estimated at 650,000 workers and job openings in construction averaging 500,000 in 2024, delaying revenue recognition. Rising industrial wages—average manufacturing hourly earnings up about 4.3% year-over-year in 2024—inflate operational costs, pushing Atkore toward automation investments to protect adjusted EBITDA margins (2024 adj. EBITDA margin ~13.5%). The constrained supply of skilled electricians, with apprenticeship starts down ~6% from 2019 to 2023, directly limits electrical contracting demand and therefore unit throughput for Atkore’s products.

Inflationary Pressures

Rising US core CPI averaged 3.6% in 2024, pushing steel and copper input costs up ~8–12% year-over-year and eroding end-customer purchasing power for Atkore’s electrical conduit and fittings.

Atkore’s pricing power has historically supported gross margins near 20%, but sustained inflation risks demand declines in price-sensitive construction segments; management targets a 2025 cost-reduction program to recover ~150–250 bps via lean manufacturing.

- Core CPI 2024: 3.6%

- Raw material cost rise: 8–12% YoY

- Gross margin historical: ~20%

- Targeted 2025 margin recovery: 150–250 bps

Currency Exchange Fluctuations

For Atkore, a stronger U.S. dollar versus the euro and Canadian dollar reduces price competitiveness of exported junction, conduit and cable management products; the USD appreciated about 8% vs the euro and 5% vs CAD in 2024, pressuring international margins.

Currency volatility creates translation effects—Atkore recorded a foreign exchange headwind of roughly $15–25 million in recent 2024 filings—introducing variability to reported EPS.

Economic strength in Canada and Europe matters: 2024 GDP growth was ~2.2% for Canada and ~1.3% for the euro area, directly influencing demand for construction and industrial electrical infrastructure products.

- USD appreciation (~+8% vs EUR, +5% vs CAD in 2024) hit export competitiveness

- FX translation headwind estimated $15–25M in 2024 affecting reported earnings

- Canada GDP ~2.2% and euro area ~1.3% in 2024, impacting regional demand

Inflation, FX and weaker construction squeeze margins; management eyes 150–250bp rebound

Higher U.S. rates and 2024–25 construction weakness cut demand; commodity inflation (steel +18% in 2024; core materials +6–8% in 2025) and wage inflation (~4.3% manufacturing pay in 2024) compressed margins despite hedging (~60% cover in FY2024); USD strength (~+8% vs EUR, +5% vs CAD in 2024) created ~$15–25M FX headwind; management targets 150–250 bps margin recovery in 2025.

| Metric | Value |

|---|---|

| Steel YoY 2024 | +18% |

| Core CPI 2024 | 3.6% |

| Hedge coverage FY2024 | ~60% |

| FX headwind 2024 | $15–25M |

Preview Before You Purchase

Atkore International, Inc. PESTLE Analysis

The preview shown here is the exact Atkore International, Inc. PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use; the content, layout, and insights visible here are the final file available for immediate download upon payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Atkore International, Inc. faces shifting regulatory, economic, and technological forces that will shape its supply chain resilience and product innovation; our concise PESTLE highlights these drivers and their strategic implications. Gain a competitive edge with the full, ready-to-use PESTLE Analysis—designed for investors and strategists—and download it now for actionable, editable insights.

Political factors

Infrastructure Spending Legislation

The Infrastructure Investment and Jobs Act disbursements continued to drive Atkore into late 2025, with federal project allocations—about $110B for grid and $65B for broadband—supporting steady demand for electrical conduits and cable management systems.

Atkore’s FY2024 U.S. infrastructure-related revenue exposure was estimated at ~20–25% of sales, and ongoing multi-year federal commitments help offset private construction cyclicality, stabilizing backlog and near-term cash flow.

Trade Policy and Tariffs

Changes in trade agreements and tariffs on imported steel and aluminum have raised Atkore's input costs; US Section 232 tariffs and 2024-25 antidumping measures increased US metal prices by roughly 15–25%, pressuring margins given Atkore's FY2024 cost of goods sold of $2.1B.

Energy Independence Initiatives

Government mandates to boost domestic energy security—such as US targets to triple solar capacity to ~300 GW by 2030—favor Atkore’s solar mounting and electrical distribution products, supporting potential revenue growth in related segments; expanded federal funding (Inflation Reduction Act, IIJA) and grid modernization spending projected at $65–$120 billion through 2030 create high-volume demand for infrastructure components; Buy American incentives and prevailing-wage requirements improve Atkore’s win rate for public utility contracts, enhancing backlog visibility and margin stability.

Taxation and Fiscal Policy

Corporate tax rates and accelerated depreciation schedules shape capex timing for Atkore’s industrial customers; faster bonus depreciation (100% through 2022, phased later) historically boosted upgrades, and current 2024 effective combined US federal-state rate ~25–27% affects ROI calculations.

Fiscal policy shifts at end-2025—projected corporate tax proposals could change Atkore’s net income by an estimated mid-single-digit percentage and alter cash available for M&A financing tied to EBITDA multiples.

Investors track tax credits for domestic manufacturing and advanced manufacturing R&D; recent Inflation Reduction Act provisions and 2024/2025 R&D credit usage materially influence valuation assumptions.

- US effective tax rate ~25–27%

- Bonus depreciation phased after 2022, affecting capex timing

- End-2025 fiscal changes could move net income mid-single-digit %

- IRA and R&D credits (2024–2025) impact valuation and M&A funding

Geopolitical Stability

While Atkore is North America–focused, 2024 metal price swings—copper up ~8% YTD and aluminum volatile amid supply disruptions—show geopolitical tensions drive input costs and logistics delays.

Instability in chokepoints like the Red Sea raised freight rates by over 30% in 2023–24, forcing Atkore to adjust pricing cadence and margins.

Political stability in secondary markets (EMEA, APAC offices) is critical to Atkore’s 5–7% international revenue growth targets and long‑term expansion.

- Geopolitical-driven metal price volatility impacts margins

- Shipping disruptions raised freight costs ~30% (2023–24)

- Frequent pricing adjustments needed to protect margins

- Stable secondary markets essential for 5–7% international growth

Infrastructure demand offsets tariff, tax and freight headwinds—FY24 revenue/backlog resilient

Federal infrastructure funding (IIJA/IRA) and Buy American rules support ~20–25% FY2024 revenue exposure and backlog; tariffs raised metal costs ~15–25%, pressuring FY2024 COGS $2.1B; US effective tax ~25–27% with end‑2025 fiscal proposals potentially shifting net income mid-single digits; shipping disruptions lifted freight >30% (2023–24), affecting margins and pricing cadence.

| Metric | Value |

|---|---|

| FY2024 infra revenue exposure | 20–25% |

| FY2024 COGS | $2.1B |

| Metal tariff impact | +15–25% |

| US effective tax rate (2024) | 25–27% |

| Freight increase (2023–24) | +30%+ |

What is included in the product

Explores how macro-environmental forces — Political, Economic, Social, Technological, Environmental, and Legal — specifically impact Atkore International, Inc., with data-driven insights and forward-looking implications for risk mitigation and strategic opportunity identification.

A concise PESTLE snapshot of Atkore International that highlights regulatory, economic, technological, environmental, and social risks and opportunities for quick inclusion in presentations or team briefings.

Economic factors

Interest Rate Environment

The late-2025 Fed funds rate near 5.25–5.50% tightened borrowing costs, contributing to a 12% year-over-year decline in U.S. housing starts in Q4 2025 and a 6% drop in nonresidential construction spending, reducing demand for Atkore’s electrical and mechanical infrastructure products.

Commodity Price Volatility

Atkore’s profitability is highly sensitive to steel, PVC and copper prices; steel surged ~18% YoY in 2024 while copper averaged $9,500/ton in 2025, pressuring gross margins. Fluctuations force sophisticated hedging—Atkore reported hedges covering roughly 60% of expected exposure in FY2024—and reliance on dynamic pricing to pass costs to customers. By late 2025, improved supply chains reduced extreme spikes, but commodity-driven inflation (core materials up ~6–8% in 2025) remains a central risk.

Labor Market Dynamics

Persistent labor shortages in construction and manufacturing slow installations of Atkore’s conduit and cable management systems, with the US construction sector facing a 2025 skilled labor gap estimated at 650,000 workers and job openings in construction averaging 500,000 in 2024, delaying revenue recognition. Rising industrial wages—average manufacturing hourly earnings up about 4.3% year-over-year in 2024—inflate operational costs, pushing Atkore toward automation investments to protect adjusted EBITDA margins (2024 adj. EBITDA margin ~13.5%). The constrained supply of skilled electricians, with apprenticeship starts down ~6% from 2019 to 2023, directly limits electrical contracting demand and therefore unit throughput for Atkore’s products.

Inflationary Pressures

Rising US core CPI averaged 3.6% in 2024, pushing steel and copper input costs up ~8–12% year-over-year and eroding end-customer purchasing power for Atkore’s electrical conduit and fittings.

Atkore’s pricing power has historically supported gross margins near 20%, but sustained inflation risks demand declines in price-sensitive construction segments; management targets a 2025 cost-reduction program to recover ~150–250 bps via lean manufacturing.

- Core CPI 2024: 3.6%

- Raw material cost rise: 8–12% YoY

- Gross margin historical: ~20%

- Targeted 2025 margin recovery: 150–250 bps

Currency Exchange Fluctuations

For Atkore, a stronger U.S. dollar versus the euro and Canadian dollar reduces price competitiveness of exported junction, conduit and cable management products; the USD appreciated about 8% vs the euro and 5% vs CAD in 2024, pressuring international margins.

Currency volatility creates translation effects—Atkore recorded a foreign exchange headwind of roughly $15–25 million in recent 2024 filings—introducing variability to reported EPS.

Economic strength in Canada and Europe matters: 2024 GDP growth was ~2.2% for Canada and ~1.3% for the euro area, directly influencing demand for construction and industrial electrical infrastructure products.

- USD appreciation (~+8% vs EUR, +5% vs CAD in 2024) hit export competitiveness

- FX translation headwind estimated $15–25M in 2024 affecting reported earnings

- Canada GDP ~2.2% and euro area ~1.3% in 2024, impacting regional demand

Inflation, FX and weaker construction squeeze margins; management eyes 150–250bp rebound

Higher U.S. rates and 2024–25 construction weakness cut demand; commodity inflation (steel +18% in 2024; core materials +6–8% in 2025) and wage inflation (~4.3% manufacturing pay in 2024) compressed margins despite hedging (~60% cover in FY2024); USD strength (~+8% vs EUR, +5% vs CAD in 2024) created ~$15–25M FX headwind; management targets 150–250 bps margin recovery in 2025.

| Metric | Value |

|---|---|

| Steel YoY 2024 | +18% |

| Core CPI 2024 | 3.6% |

| Hedge coverage FY2024 | ~60% |

| FX headwind 2024 | $15–25M |

Preview Before You Purchase

Atkore International, Inc. PESTLE Analysis

The preview shown here is the exact Atkore International, Inc. PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use; the content, layout, and insights visible here are the final file available for immediate download upon payment.