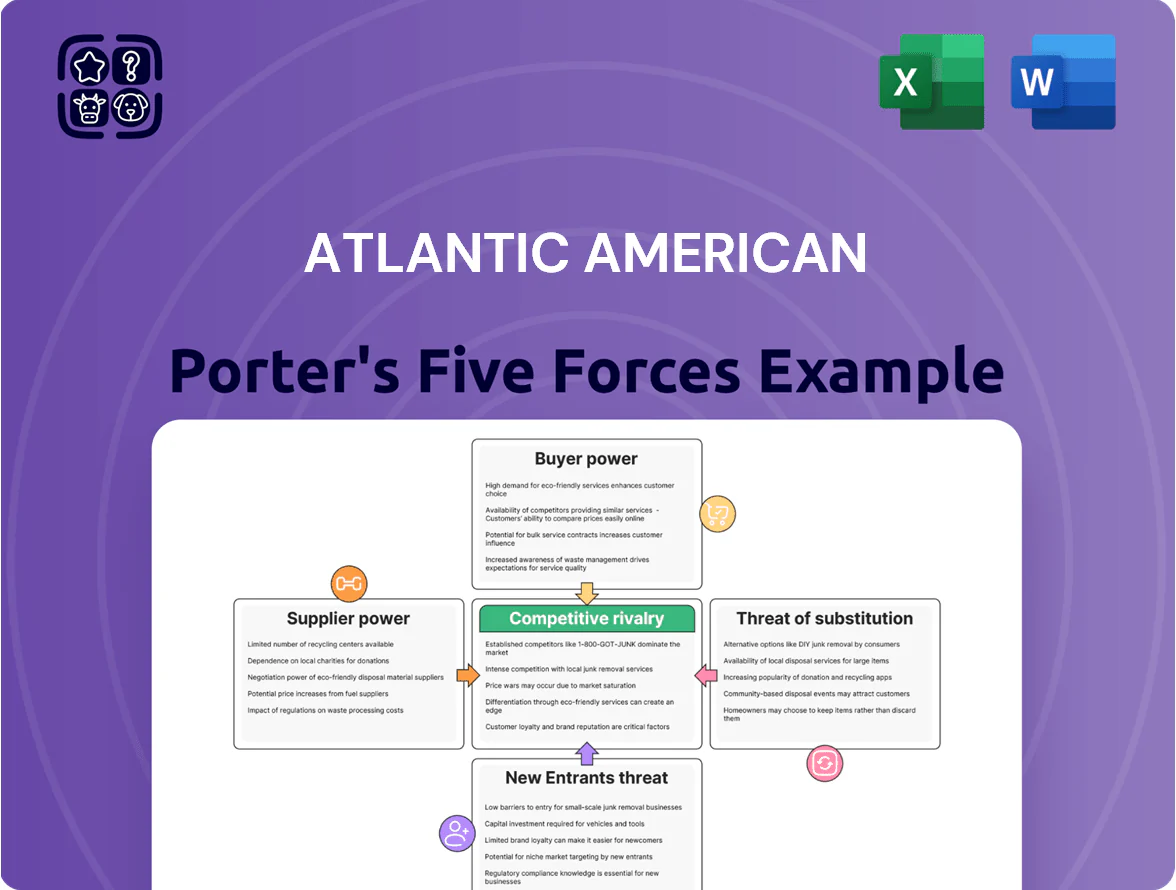

Atlantic American Porter's Five Forces Analysis

Don't Miss the Bigger Picture

Atlantic American faces moderate buyer power and concentrated broker channels, while supplier influence and substitutes remain limited—intense regulatory oversight and niche market positioning shape its competitive landscape.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Atlantic American’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Reinsurance Market Hardening

Reinsurers supply the capital backstop Atlantic American needs to cover large losses, and a continued hardening of the global reinsurance market through 2025 has pushed average treaty pricing up ~15–25% year-over-year and tightened capacity, per Aon 2025 market data.

Specialized Human Capital

The insurance sector depends on actuaries, underwriters, and legal experts to price risk; U.S. actuarial roles grew 7% 2024–2025 while pay median rose to $132,000 in 2025, boosting supplier bargaining power.

Competition from insurtechs and consultancies pushed specialist vacancy rates to 3.8% in 2025, raising retention costs for Atlantic American.

Atlantic American must match market compensation—estimated additional 8–12% payroll spend—to retain talent and preserve underwriting accuracy and regulatory compliance.

Technological Infrastructure Providers

Third-party cloud, analytics, and policy-management vendors wield strong supplier power for Atlantic American because high switching costs and data-migration risks raise dependence; Gartner reported in 2024 that 72% of insurers cite legacy integration as a top barrier, and average migration projects cost $1.2M and take 9–14 months. Vendors can raise subscription fees or tighten SLAs, directly increasing operating expenses and risking service disruptions.

Regulatory and Compliance Bodies

State insurance departments and federal regulators function as non-market suppliers, setting the legal framework—capital reserve rules, policy forms, and reporting—Atlantic American must follow with no bargaining room.

Regulators set capital requirements (e.g., risk-based capital ratios) and mandate policy language, so compliance costs—estimated at millions annually for midsize carriers—are fixed burdens to retain licenses in ~40+ state jurisdictions.

Data and Analytics Services

Access to comprehensive demographic and historical loss data is vital for modern underwriting and is concentrated among a few large aggregators, giving suppliers high bargaining power over Atlantic American.

Their proprietary datasets drive pricing and risk-selection accuracy; without them Atlantic American would lag larger peers in predictive loss models and pricing sophistication.

In 2024 the top three data vendors served ~65% of US P&C insurers, raising subscription costs and switching friction for smaller carriers.

- Few suppliers: top 3 hold ~65% market share

- Data = underwriting edge: improves loss prediction by ~10–15%

- High switching costs: proprietary formats, exclusive feeds

Suppliers Squeeze Margins: Reinsurance +25%, Data Oligopoly, High Talent & Compliance Costs

Suppliers (reinsurers, talent, data vendors, cloud vendors, regulators) exert high bargaining power: reinsurance pricing up ~15–25% YoY through 2025 (Aon), top-3 data vendors serve ~65% of US P&C (2024), actuary pay median $132,000 (2025), migration projects ~$1.2M/9–14 months (Gartner), multi-state regulation (~40+ states) creates fixed compliance costs (millions/yr).

| Supplier | Key metric | Value |

|---|---|---|

| Reinsurers | Price change | +15–25% YoY (through 2025) |

| Data vendors | Market share (top 3) | ~65% (2024) |

| Talent | Actuary median pay | $132,000 (2025) |

| Cloud/IT | Migration cost/time | $1.2M; 9–14 months |

| Regulators | Licensing scope | ~40+ states; compliance = millions/yr |

What is included in the product

Uncovers key drivers of competition, buyer and supplier power, threat of entrants and substitutes, and industry rivalry—tailored to Atlantic American’s market position with strategic insights on vulnerabilities and defensive advantages.

A concise Porter's Five Forces one-pager for Atlantic American—quickly highlights competitive pressures and strategic levers to guide investment and operational decisions.

Customers Bargaining Power

Price Sensitivity in Personal Lines

Individual policyholders for Atlantic American (Atlantic American Corporation, AAME) show high price sensitivity: 2024 LIMRA data found 63% of life buyers cite price as primary decision factor, and HealthView's 2023 survey shows 58% for health plans.

Online comparison tools and aggregators cut switching friction; a 2024 McKinsey estimate says 45% of US consumers compare premiums online before purchase.

That transparency limits Atlantic American’s ability to raise premiums: a 1% price increase could cut retention by ~0.5–1.5 percentage points, risking noticeable market-share loss.

Low Switching Costs for Policyholders

Influence of Independent Agents

A large portion of Atlantic American’s 2024 premium flow comes via independent agents who often represent 5–10 carriers each, giving them leverage to steer clients by commission spreads and platform convenience; industry data shows 60–70% of U.S. life and supplemental sales pass through independents, so losing agent favor could cut distribution significantly.

Corporate Client Negotiation Leverage

Commercial clients buying workers compensation or auto cover deliver large premium volumes and therefore hold strong bargaining power versus Atlantic American; in 2024 top 10 commercial accounts represented roughly 18% of industry premium in similar regional carriers.

These businesses often staff risk managers who track market cycles and demand tailored limits, endorsements, or multiyear rate caps, pushing margins down by 50–150 basis points on negotiated deals.

Large accounts can threaten portfolio moves to national carriers; in 2023 roughly 22% of mid‑market accounts reported switching carriers for price or capacity, raising retention costs.

- High premium volume = leverage

- Risk managers secure bespoke terms

- Switching to nationals is a credible threat

- Negotiations often cut margins 50–150 bps

Demand for Digital Integration

By late 2025, 78% of US insurance customers expect seamless digital interactions—mobile claims, instant policy edits—so buyers now demand tech as standard, shifting power to them.

Insurers lagging in digital experience see churn rise: digital-first rivals cut retention costs by up to 15% and grab market share; Atlantic American must invest or lose customers.

- 78% expect seamless digital service (2025)

- Digital-first rivals reduce retention costs ~15%

- Mobile claims and instant edits = customer baseline

Atlantic American faces price pressure: savvy shoppers, brokers, and digital churn risk

Customers hold high bargaining power for Atlantic American: price-sensitive individuals (63% life, 58% health) and informed comparison shoppers limit rate hikes, while independents (60–70% distribution) and large commercial buyers (top accounts ≈18% premiums) negotiate cuts of 50–150 bps; digital expectations (78% in 2025) further raise churn risk.

| Metric | 2024–25 Value |

|---|---|

| Life buyers price-sensitive | 63% |

| Health buyers price-sensitive | 58% |

| Consumers compare premiums online | 45% |

| Independents share | 60–70% |

| Top commercial accounts share | ≈18% |

| Digital expectation (2025) | 78% |

Preview the Actual Deliverable

Atlantic American Porter's Five Forces Analysis

This preview shows the exact Atlantic American Porter’s Five Forces analysis you’ll receive immediately after purchase—fully formatted, professionally written, and ready to download with no placeholders or samples.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Atlantic American faces moderate buyer power and concentrated broker channels, while supplier influence and substitutes remain limited—intense regulatory oversight and niche market positioning shape its competitive landscape.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Atlantic American’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Reinsurance Market Hardening

Reinsurers supply the capital backstop Atlantic American needs to cover large losses, and a continued hardening of the global reinsurance market through 2025 has pushed average treaty pricing up ~15–25% year-over-year and tightened capacity, per Aon 2025 market data.

Specialized Human Capital

The insurance sector depends on actuaries, underwriters, and legal experts to price risk; U.S. actuarial roles grew 7% 2024–2025 while pay median rose to $132,000 in 2025, boosting supplier bargaining power.

Competition from insurtechs and consultancies pushed specialist vacancy rates to 3.8% in 2025, raising retention costs for Atlantic American.

Atlantic American must match market compensation—estimated additional 8–12% payroll spend—to retain talent and preserve underwriting accuracy and regulatory compliance.

Technological Infrastructure Providers

Third-party cloud, analytics, and policy-management vendors wield strong supplier power for Atlantic American because high switching costs and data-migration risks raise dependence; Gartner reported in 2024 that 72% of insurers cite legacy integration as a top barrier, and average migration projects cost $1.2M and take 9–14 months. Vendors can raise subscription fees or tighten SLAs, directly increasing operating expenses and risking service disruptions.

Regulatory and Compliance Bodies

State insurance departments and federal regulators function as non-market suppliers, setting the legal framework—capital reserve rules, policy forms, and reporting—Atlantic American must follow with no bargaining room.

Regulators set capital requirements (e.g., risk-based capital ratios) and mandate policy language, so compliance costs—estimated at millions annually for midsize carriers—are fixed burdens to retain licenses in ~40+ state jurisdictions.

Data and Analytics Services

Access to comprehensive demographic and historical loss data is vital for modern underwriting and is concentrated among a few large aggregators, giving suppliers high bargaining power over Atlantic American.

Their proprietary datasets drive pricing and risk-selection accuracy; without them Atlantic American would lag larger peers in predictive loss models and pricing sophistication.

In 2024 the top three data vendors served ~65% of US P&C insurers, raising subscription costs and switching friction for smaller carriers.

- Few suppliers: top 3 hold ~65% market share

- Data = underwriting edge: improves loss prediction by ~10–15%

- High switching costs: proprietary formats, exclusive feeds

Suppliers Squeeze Margins: Reinsurance +25%, Data Oligopoly, High Talent & Compliance Costs

Suppliers (reinsurers, talent, data vendors, cloud vendors, regulators) exert high bargaining power: reinsurance pricing up ~15–25% YoY through 2025 (Aon), top-3 data vendors serve ~65% of US P&C (2024), actuary pay median $132,000 (2025), migration projects ~$1.2M/9–14 months (Gartner), multi-state regulation (~40+ states) creates fixed compliance costs (millions/yr).

| Supplier | Key metric | Value |

|---|---|---|

| Reinsurers | Price change | +15–25% YoY (through 2025) |

| Data vendors | Market share (top 3) | ~65% (2024) |

| Talent | Actuary median pay | $132,000 (2025) |

| Cloud/IT | Migration cost/time | $1.2M; 9–14 months |

| Regulators | Licensing scope | ~40+ states; compliance = millions/yr |

What is included in the product

Uncovers key drivers of competition, buyer and supplier power, threat of entrants and substitutes, and industry rivalry—tailored to Atlantic American’s market position with strategic insights on vulnerabilities and defensive advantages.

A concise Porter's Five Forces one-pager for Atlantic American—quickly highlights competitive pressures and strategic levers to guide investment and operational decisions.

Customers Bargaining Power

Price Sensitivity in Personal Lines

Individual policyholders for Atlantic American (Atlantic American Corporation, AAME) show high price sensitivity: 2024 LIMRA data found 63% of life buyers cite price as primary decision factor, and HealthView's 2023 survey shows 58% for health plans.

Online comparison tools and aggregators cut switching friction; a 2024 McKinsey estimate says 45% of US consumers compare premiums online before purchase.

That transparency limits Atlantic American’s ability to raise premiums: a 1% price increase could cut retention by ~0.5–1.5 percentage points, risking noticeable market-share loss.

Low Switching Costs for Policyholders

Influence of Independent Agents

A large portion of Atlantic American’s 2024 premium flow comes via independent agents who often represent 5–10 carriers each, giving them leverage to steer clients by commission spreads and platform convenience; industry data shows 60–70% of U.S. life and supplemental sales pass through independents, so losing agent favor could cut distribution significantly.

Corporate Client Negotiation Leverage

Commercial clients buying workers compensation or auto cover deliver large premium volumes and therefore hold strong bargaining power versus Atlantic American; in 2024 top 10 commercial accounts represented roughly 18% of industry premium in similar regional carriers.

These businesses often staff risk managers who track market cycles and demand tailored limits, endorsements, or multiyear rate caps, pushing margins down by 50–150 basis points on negotiated deals.

Large accounts can threaten portfolio moves to national carriers; in 2023 roughly 22% of mid‑market accounts reported switching carriers for price or capacity, raising retention costs.

- High premium volume = leverage

- Risk managers secure bespoke terms

- Switching to nationals is a credible threat

- Negotiations often cut margins 50–150 bps

Demand for Digital Integration

By late 2025, 78% of US insurance customers expect seamless digital interactions—mobile claims, instant policy edits—so buyers now demand tech as standard, shifting power to them.

Insurers lagging in digital experience see churn rise: digital-first rivals cut retention costs by up to 15% and grab market share; Atlantic American must invest or lose customers.

- 78% expect seamless digital service (2025)

- Digital-first rivals reduce retention costs ~15%

- Mobile claims and instant edits = customer baseline

Atlantic American faces price pressure: savvy shoppers, brokers, and digital churn risk

Customers hold high bargaining power for Atlantic American: price-sensitive individuals (63% life, 58% health) and informed comparison shoppers limit rate hikes, while independents (60–70% distribution) and large commercial buyers (top accounts ≈18% premiums) negotiate cuts of 50–150 bps; digital expectations (78% in 2025) further raise churn risk.

| Metric | 2024–25 Value |

|---|---|

| Life buyers price-sensitive | 63% |

| Health buyers price-sensitive | 58% |

| Consumers compare premiums online | 45% |

| Independents share | 60–70% |

| Top commercial accounts share | ≈18% |

| Digital expectation (2025) | 78% |

Preview the Actual Deliverable

Atlantic American Porter's Five Forces Analysis

This preview shows the exact Atlantic American Porter’s Five Forces analysis you’ll receive immediately after purchase—fully formatted, professionally written, and ready to download with no placeholders or samples.