ATN International Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

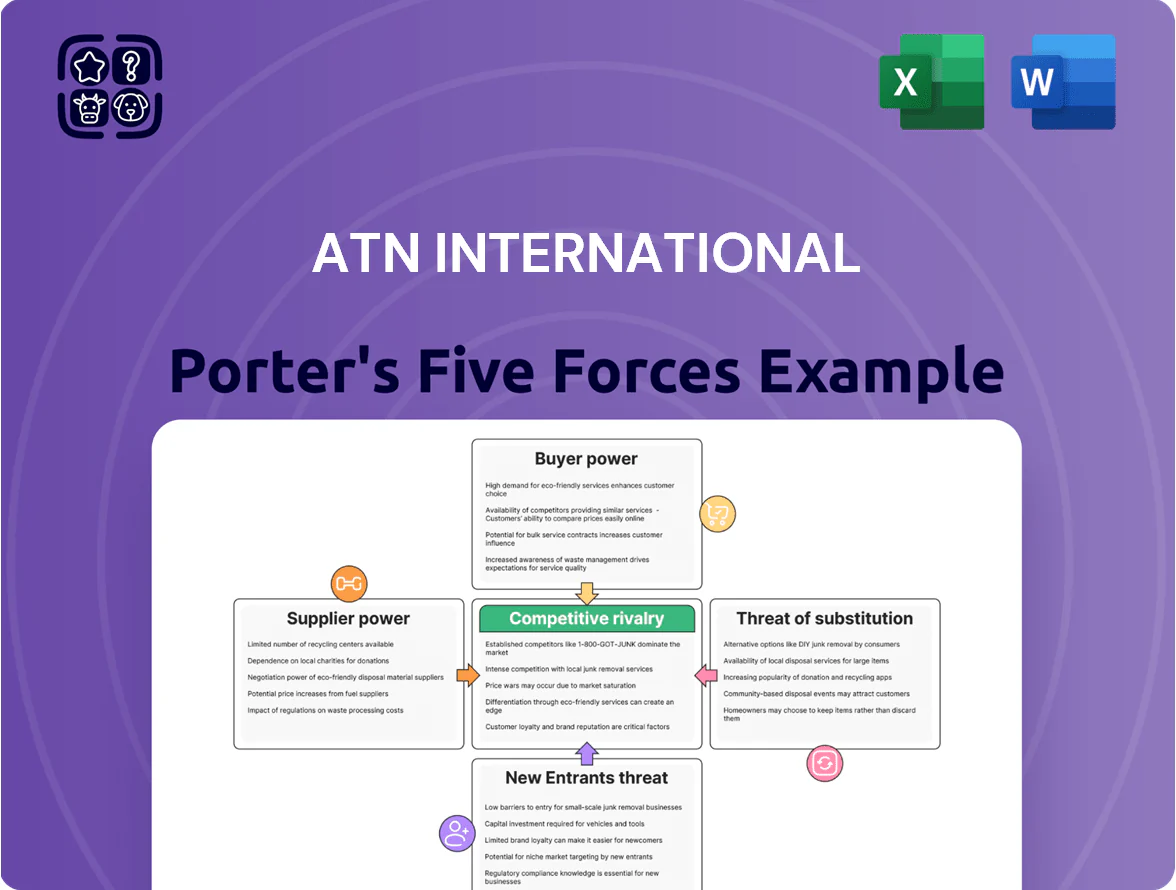

ATN International faces moderate buyer power, niche supplier relationships, and a steady threat from substitutes and new entrants due to telecom convergence and regulatory shifts; competitive rivalry is elevated by regional players and pricing pressure.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore ATN International’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Network Equipment Vendors

ATN International relies on a handful of global vendors for 5G and fiber-optic hardware, giving suppliers strong leverage because switching costs exceed millions per site and integration needs vendor-certified engineers. By Q4 2025 supply-chain lead times fell toward 8–12 weeks, but component price inflation stayed elevated—optical transceiver costs rose ~15% YoY in 2024–25—keeping procurement spend volatility high for mid-tier operators like ATN.

Limited Spectrum Availability

The government and regulators are the de facto suppliers of radio spectrum, a scarce, licensed resource; ATN International (ATNI) must win auctions or acquire licenses, which in the US averaged auction prices of about $1,000–$2,000 per MHz-pop in recent FCC auctions (2023–2024), forcing capital-intensive buys. This dependency constrains rapid scaling, since ATNI would need multi-million-dollar outlays—often tens to hundreds of millions—to secure regional bandwidth rights.

Energy Infrastructure and Solar Component Providers

ATN’s renewable segment relies heavily on photovoltaic cells and lithium-ion batteries, whose global production is concentrated in China, South Korea, and Taiwan, exposing ATN to tariffs and shipping delays; Chinese manufacturers held ~70% of PV module production in 2024 (IEA) so supplier disruption risk is high.

Rising demand for green energy pushed PV module prices up ~12% in 2024 and battery pack ASPs rose 8% Y/Y, giving suppliers stronger price leverage and squeezing ATN’s margins unless long-term contracts or vertical integration are used.

Interconnection and Roaming Partners

ATN relies on agreements with tier-one national and international carriers for roaming and data transit, giving those carriers leverage to set interconnection fees and service terms. In 2025, global wholesale roaming rates averaged $0.05–$0.12/MB, and ATN paid above-average rates on some routes due to scale limits, raising cost of goods sold and compressing margins. Larger partners can demand minimum traffic commitments or premium pricing, creating ongoing cost pressure.

- Depends on tier-one infrastructure; limited bargaining clout

- Wholesale roaming: ~$0.05–$0.12 per MB (2025 avg)

- Higher interconnect fees raise COGS and squeeze margins

- Minimum traffic clauses and premium pricing common

Specialized Technical Labor

The 2023–2025 shortage of skilled telecom and renewable-energy technicians has pushed their bargaining power up, with US vacancy rates for specialized network engineers near 6.2% in 2024 and median retention costs rising ~18% by 2025.

As AI-driven network management grows, ATN must match market pay—industry data shows top-tier engineers command total comp of $180k–$240k in 2025—to avoid poaching by Big Tech.

- Vacancy rate ~6.2% (2024)

- Retention cost +18% (2023–25)

- Top engineer comp $180k–$240k (2025)

Suppliers Hold the Cards: Soaring Spectrum, Component Costs & Talent Premiums

Suppliers exert high power: few 5G/fiber vendors, spectrum auctions costing $1k–$2k/MHz-pop (2023–24), PV makers ~70% China (2024), optical transceivers +15% YoY (2024–25), PV +12% (2024), battery ASPs +8% (2024), roaming $0.05–$0.12/MB (2025), engineer vacancy 6.2% (2024), top comp $180k–$240k (2025).

| Metric | Value |

|---|---|

| Spectrum price | $1k–$2k/MHz-pop |

| Optical transceivers | +15% YoY |

| PV share (China) | ~70% |

| Roaming rate | $0.05–$0.12/MB |

| Engineer comp | $180k–$240k |

What is included in the product

Comprehensive Porter's Five Forces for ATN International, uncovering competitive intensity, buyer/supplier leverage, entry barriers, substitute threats, and strategic levers shaping profitability and market positioning.

A concise Porter's Five Forces one-sheet for ATN International—ideal for quick strategic decisions and boardroom use.

Customers Bargaining Power

Low Switching Costs for Residential Users

Residential customers in the Caribbean and rural US face low switching costs: 68% of Caribbean mobile users and ~40% of US rural subscribers use prepaid or month-to-month plans (GSMA, 2024; FCC, 2023), enabling rapid moves for promos. That dynamic forces ATN International to spend on loyalty—2019–2024 average annual retention marketing rose ~12%—and maintain consistent QoS to curb churn, which exceeds 25% in some island markets.

Concentration of Healthcare Enterprise Clients

ATN’s managed mobile solutions heavily target healthcare, concentrating revenue: in FY2024 ATN reported wireless services revenue of $78.6M, and the healthcare-tailored unit represents a material share, so a few large hospital systems hold strong bargaining power.

These enterprise clients can insist on tailored SLAs and volume discounts; industry benchmarks show top 5 clients often drive >40% of segment spend, raising price pressure.

Loss of a single large healthcare contract could cut segment revenue by double-digit percentages; for example, a 15–25% client churn would materially dent quarterly margins and cashflow.

Price Sensitivity in Underserved Markets

A large share of ATN International’s footprint serves low-income markets where price drives choice; in 2024 roughly 60% of its sites were in territories with GDP per capita under US$8,000, making customers highly price-sensitive. This sensitivity caps ATN’s ability to pass through cost inflation—telecom ARPU (average revenue per user) in many of these markets averaged under US$10/month in 2024—so ATN must sustain tight cost control and network efficiency to keep services affordable.

Availability of Transparent Information

Government and Institutional Bargaining Power

ATN often serves government agencies and educational institutions that buy in bulk and follow strict procurement rules, letting them negotiate rates ~10–25% below retail; in 2024 ATN reported 18% revenue from institutional contracts, pressuring margins.

These buyers force competitive bidding and longer payment terms, so ATN accepts lower per-unit margins and higher contract administration costs, reducing EBITDA on those accounts.

- Bulk contracts: scale -> price cuts 10–25%

- 2024: ~18% revenue from institutions

- Competitive bidding -> lower margins

- Longer payment terms increase working capital needs

Customer pricing power and digital switch tools threaten 3–5% margin erosion

Customers wield strong price and SLA leverage: prepaid and low-ARPU consumers (≈60% in <$8k GDP/capita markets; ARPU <$10/mo in 2024) raise churn, while healthcare and institutional buyers (2024: ~18% revenue) drive volume discounts (10–25%) and longer terms, creating 3–5% margin erosion risk; digital comparison tools (47% of US small operators) increase switching.

| Metric | 2024/2025 |

|---|---|

| ARPU (selected markets) | <$10/mo |

| Markets GDP/capita <$8k | ~60% of sites |

| Institutional revenue | ~18% |

| Retention spend change (2019–24) | +12% p.a. |

| Switch tools adoption | 47% |

| Estimated margin erosion risk | 3–5% |

Preview Before You Purchase

ATN International Porter's Five Forces Analysis

This preview shows the exact ATN International Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders, no mockups.

The document displayed is the same professionally written, fully formatted file ready for download and use the moment you buy.

You're viewing the final deliverable; upon payment you'll get instant access to this identical analysis with no further setup required.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

ATN International faces moderate buyer power, niche supplier relationships, and a steady threat from substitutes and new entrants due to telecom convergence and regulatory shifts; competitive rivalry is elevated by regional players and pricing pressure.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore ATN International’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Network Equipment Vendors

ATN International relies on a handful of global vendors for 5G and fiber-optic hardware, giving suppliers strong leverage because switching costs exceed millions per site and integration needs vendor-certified engineers. By Q4 2025 supply-chain lead times fell toward 8–12 weeks, but component price inflation stayed elevated—optical transceiver costs rose ~15% YoY in 2024–25—keeping procurement spend volatility high for mid-tier operators like ATN.

Limited Spectrum Availability

The government and regulators are the de facto suppliers of radio spectrum, a scarce, licensed resource; ATN International (ATNI) must win auctions or acquire licenses, which in the US averaged auction prices of about $1,000–$2,000 per MHz-pop in recent FCC auctions (2023–2024), forcing capital-intensive buys. This dependency constrains rapid scaling, since ATNI would need multi-million-dollar outlays—often tens to hundreds of millions—to secure regional bandwidth rights.

Energy Infrastructure and Solar Component Providers

ATN’s renewable segment relies heavily on photovoltaic cells and lithium-ion batteries, whose global production is concentrated in China, South Korea, and Taiwan, exposing ATN to tariffs and shipping delays; Chinese manufacturers held ~70% of PV module production in 2024 (IEA) so supplier disruption risk is high.

Rising demand for green energy pushed PV module prices up ~12% in 2024 and battery pack ASPs rose 8% Y/Y, giving suppliers stronger price leverage and squeezing ATN’s margins unless long-term contracts or vertical integration are used.

Interconnection and Roaming Partners

ATN relies on agreements with tier-one national and international carriers for roaming and data transit, giving those carriers leverage to set interconnection fees and service terms. In 2025, global wholesale roaming rates averaged $0.05–$0.12/MB, and ATN paid above-average rates on some routes due to scale limits, raising cost of goods sold and compressing margins. Larger partners can demand minimum traffic commitments or premium pricing, creating ongoing cost pressure.

- Depends on tier-one infrastructure; limited bargaining clout

- Wholesale roaming: ~$0.05–$0.12 per MB (2025 avg)

- Higher interconnect fees raise COGS and squeeze margins

- Minimum traffic clauses and premium pricing common

Specialized Technical Labor

The 2023–2025 shortage of skilled telecom and renewable-energy technicians has pushed their bargaining power up, with US vacancy rates for specialized network engineers near 6.2% in 2024 and median retention costs rising ~18% by 2025.

As AI-driven network management grows, ATN must match market pay—industry data shows top-tier engineers command total comp of $180k–$240k in 2025—to avoid poaching by Big Tech.

- Vacancy rate ~6.2% (2024)

- Retention cost +18% (2023–25)

- Top engineer comp $180k–$240k (2025)

Suppliers Hold the Cards: Soaring Spectrum, Component Costs & Talent Premiums

Suppliers exert high power: few 5G/fiber vendors, spectrum auctions costing $1k–$2k/MHz-pop (2023–24), PV makers ~70% China (2024), optical transceivers +15% YoY (2024–25), PV +12% (2024), battery ASPs +8% (2024), roaming $0.05–$0.12/MB (2025), engineer vacancy 6.2% (2024), top comp $180k–$240k (2025).

| Metric | Value |

|---|---|

| Spectrum price | $1k–$2k/MHz-pop |

| Optical transceivers | +15% YoY |

| PV share (China) | ~70% |

| Roaming rate | $0.05–$0.12/MB |

| Engineer comp | $180k–$240k |

What is included in the product

Comprehensive Porter's Five Forces for ATN International, uncovering competitive intensity, buyer/supplier leverage, entry barriers, substitute threats, and strategic levers shaping profitability and market positioning.

A concise Porter's Five Forces one-sheet for ATN International—ideal for quick strategic decisions and boardroom use.

Customers Bargaining Power

Low Switching Costs for Residential Users

Residential customers in the Caribbean and rural US face low switching costs: 68% of Caribbean mobile users and ~40% of US rural subscribers use prepaid or month-to-month plans (GSMA, 2024; FCC, 2023), enabling rapid moves for promos. That dynamic forces ATN International to spend on loyalty—2019–2024 average annual retention marketing rose ~12%—and maintain consistent QoS to curb churn, which exceeds 25% in some island markets.

Concentration of Healthcare Enterprise Clients

ATN’s managed mobile solutions heavily target healthcare, concentrating revenue: in FY2024 ATN reported wireless services revenue of $78.6M, and the healthcare-tailored unit represents a material share, so a few large hospital systems hold strong bargaining power.

These enterprise clients can insist on tailored SLAs and volume discounts; industry benchmarks show top 5 clients often drive >40% of segment spend, raising price pressure.

Loss of a single large healthcare contract could cut segment revenue by double-digit percentages; for example, a 15–25% client churn would materially dent quarterly margins and cashflow.

Price Sensitivity in Underserved Markets

A large share of ATN International’s footprint serves low-income markets where price drives choice; in 2024 roughly 60% of its sites were in territories with GDP per capita under US$8,000, making customers highly price-sensitive. This sensitivity caps ATN’s ability to pass through cost inflation—telecom ARPU (average revenue per user) in many of these markets averaged under US$10/month in 2024—so ATN must sustain tight cost control and network efficiency to keep services affordable.

Availability of Transparent Information

Government and Institutional Bargaining Power

ATN often serves government agencies and educational institutions that buy in bulk and follow strict procurement rules, letting them negotiate rates ~10–25% below retail; in 2024 ATN reported 18% revenue from institutional contracts, pressuring margins.

These buyers force competitive bidding and longer payment terms, so ATN accepts lower per-unit margins and higher contract administration costs, reducing EBITDA on those accounts.

- Bulk contracts: scale -> price cuts 10–25%

- 2024: ~18% revenue from institutions

- Competitive bidding -> lower margins

- Longer payment terms increase working capital needs

Customer pricing power and digital switch tools threaten 3–5% margin erosion

Customers wield strong price and SLA leverage: prepaid and low-ARPU consumers (≈60% in <$8k GDP/capita markets; ARPU <$10/mo in 2024) raise churn, while healthcare and institutional buyers (2024: ~18% revenue) drive volume discounts (10–25%) and longer terms, creating 3–5% margin erosion risk; digital comparison tools (47% of US small operators) increase switching.

| Metric | 2024/2025 |

|---|---|

| ARPU (selected markets) | <$10/mo |

| Markets GDP/capita <$8k | ~60% of sites |

| Institutional revenue | ~18% |

| Retention spend change (2019–24) | +12% p.a. |

| Switch tools adoption | 47% |

| Estimated margin erosion risk | 3–5% |

Preview Before You Purchase

ATN International Porter's Five Forces Analysis

This preview shows the exact ATN International Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders, no mockups.

The document displayed is the same professionally written, fully formatted file ready for download and use the moment you buy.

You're viewing the final deliverable; upon payment you'll get instant access to this identical analysis with no further setup required.