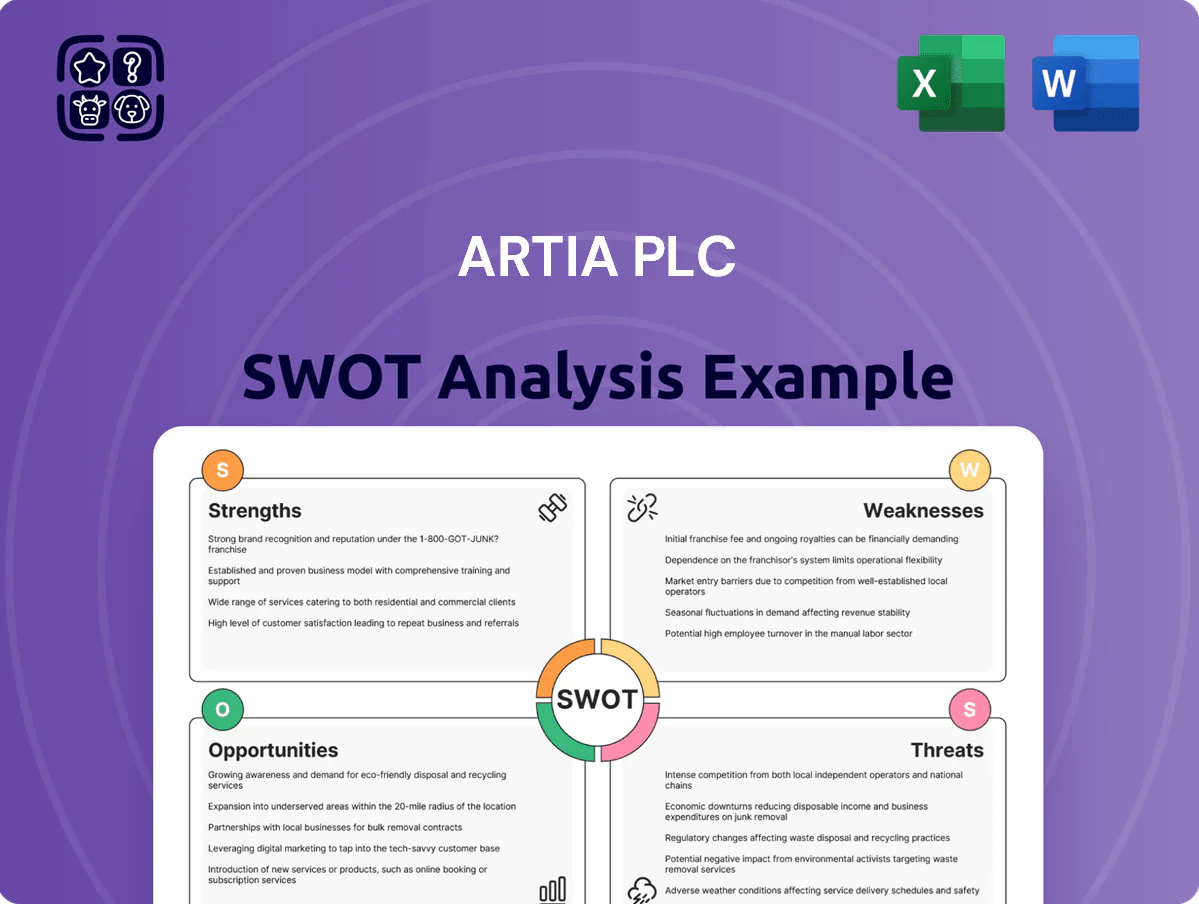

Artia PLC SWOT Analysis

Your Strategic Toolkit Starts Here

Artia PLC shows resilient niche strengths in project management software and an expanding client base, but faces competitive pressures and integration risks as it scales; strategic partnerships and product differentiation are key growth levers.

Discover the full SWOT analysis—purchase the complete, editable report (Word + Excel) for research-backed insights, financial context, and actionable strategies to support investment, planning, or pitches.

Strengths

Dominant Market Position in Finland

Atria PLC holds a leading market share in Finland’s meat and ready-to-eat segments, roughly 30–35% by value in 2025, giving a stable domestic revenue base of about EUR 900–1,000m yearly. This dominance boosts bargaining power with major Nordic retailers like Kesko and S Group, often securing favorable shelf placements and margins. By end-2025 Atria is widely recognized as a key player in national food security after capacity investments and supply-chain contracts. These factors strengthen brand reputation and resilience.

Strong Brand Equity and Trust

The Atria brand is among Northern Europe’s top-recognized food brands, with Nielsen 2024 data showing 68% spontaneous awareness in Finland and a 74% trust score in consumer safety surveys, letting Atria sustain a price premium of ~6–8% versus category average in 2024.

Ongoing marketing spend ~EUR 45m in 2024 (7% of COGS) keeps Atria top-of-mind, helping household penetration stay near 82% and positioning it as the go-to reliable protein source during demand shifts.

Highly Integrated Value Chain

Atria PLC’s farm-to-table model gives full traceability and higher animal-welfare standards, supporting premium pricing: 2025 revenue from branded fresh meat rose 6.2% YoY to €412m.

Close ties with 1,200 local farms cut procurement volatility; supplier disruption days fell 38% between 2022–2024, improving gross margin by ~120 bps.

Vertical integration reduces input cost swings and food-safety risks, and 68% of EU consumers in 2024 said they prefer traceable meat—boosting Atria’s brand premium.

Modernized Production Infrastructure

Significant capital investments in automated production—notably the expanded Nurmo poultry plant completed in 2023—have raised throughput by ~25% and cut direct labour per kg by 18%, positioning Artia PLC as a lower-cost producer.

State-of-the-art lines improved resource efficiency (water/energy down ~12% each) and by 2025 contributed to a 160 bps gross margin uplift versus 2022, via faster processing and lower variable costs.

- Nurmo expansion 2023: +25% throughput

- Labour cost per kg: −18%

- Water/energy use: −12%

- Gross margin uplift by 2025: +160 bps

Diverse Product Portfolio

- Product range: fresh, cold cuts, convenience, plant-based

- Plant-based growth: +18% in 2024; 6% of food revenue

- Revenue split 2024: retail €1.2bn; foodservice €430m

- Risk mitigation: diversified segments and channels

Atria PLC: Market-leading Finnish meat player—€900–1,000m revenue, margin gains

Atria PLC holds ~30–35% Finland market share (2025), generating ~€900–1,000m revenue; strong retailer relations (Kesko, S Group) and 82% household penetration support a 6–8% price premium. Nurmo expansion (2023) +25% throughput cut labour/kg −18% and raised gross margin +160 bps by 2025; branded fresh meat €412m (2025); plant-based +18% (2024), 6% of food revenue.

| Metric | Value |

|---|---|

| Finland share (2025) | 30–35% |

| Revenue | €900–1,000m |

| Nurmo throughput | +25% (2023) |

| Gross margin uplift | +160 bps (2022–25) |

What is included in the product

Delivers a strategic overview of Artia PLC’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats to map its competitive position and risks shaping future growth.

Offers a concise SWOT snapshot of Artia PLC to speed strategic alignment and stakeholder updates.

Weaknesses

Geographic Concentration Risk

Atria PLC earns over 85% of revenues from the Nordics—roughly 55% Finland, 20% Sweden, 10% Denmark—leaving limited global diversification as of FY2024 (company report, Feb 2025).

Heavy Nordic exposure makes Atria vulnerable to local GDP swings; Finland’s GDP fell 0.3% in Q3 2024 and Sweden’s consumer confidence dropped to 80 in Dec 2024 (Statistics Finland, SCB).

Stagnant population trends—Finland’s population growth 0.1% in 2024—plus slower household spending directly compress Atria’s top line and margin outlook.

Sensitivity to Raw Material Costs

Artia PLC is highly exposed to animal feed, energy, and grain price swings; raw materials made up about 52% of COGS in FY2024, so a 10% commodity spike could cut EBIT margin by ~3 percentage points.

Exposure to Low-Margin Categories

High Indebtedness from Capital Projects

Limited Presence in High-Growth Emerging Markets

Atria PLC: Nordic‑centric, margin‑pressed meat group with high leverage and refinancing risk

Atria PLC is highly Nordic‑concentrated (FY2024: ~85% revenues; Finland 55%, Sweden 20%, Denmark 10%), leaving limited geographic diversification and exposure to local GDP swings (Finland Q3 2024 GDP -0.3%). Elevated commodity sensitivity (raw materials ~52% of COGS) and heavy low‑margin fresh meat mix (34% sales; gross margin 12.8% FY2024) compress ROE (8.1%) and cash flow while net debt (~£420m YE‑2025; leverage ~3.2x) raises refinancing risk.

| Metric | Value |

|---|---|

| Nordic revenue share (FY2024) | ~85% |

| Gross margin (FY2024) | 12.8% |

| ROE (2024) | 8.1% |

| Net debt (YE‑2025) | ~£420m |

| Leverage | ~3.2x ND/EBITDA |

Full Version Awaits

Artia PLC SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the entire in-depth version.

This is a real excerpt from the complete document. Once purchased, you’ll receive the full, editable version.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Strategic Toolkit Starts Here

Artia PLC shows resilient niche strengths in project management software and an expanding client base, but faces competitive pressures and integration risks as it scales; strategic partnerships and product differentiation are key growth levers.

Discover the full SWOT analysis—purchase the complete, editable report (Word + Excel) for research-backed insights, financial context, and actionable strategies to support investment, planning, or pitches.

Strengths

Dominant Market Position in Finland

Atria PLC holds a leading market share in Finland’s meat and ready-to-eat segments, roughly 30–35% by value in 2025, giving a stable domestic revenue base of about EUR 900–1,000m yearly. This dominance boosts bargaining power with major Nordic retailers like Kesko and S Group, often securing favorable shelf placements and margins. By end-2025 Atria is widely recognized as a key player in national food security after capacity investments and supply-chain contracts. These factors strengthen brand reputation and resilience.

Strong Brand Equity and Trust

The Atria brand is among Northern Europe’s top-recognized food brands, with Nielsen 2024 data showing 68% spontaneous awareness in Finland and a 74% trust score in consumer safety surveys, letting Atria sustain a price premium of ~6–8% versus category average in 2024.

Ongoing marketing spend ~EUR 45m in 2024 (7% of COGS) keeps Atria top-of-mind, helping household penetration stay near 82% and positioning it as the go-to reliable protein source during demand shifts.

Highly Integrated Value Chain

Atria PLC’s farm-to-table model gives full traceability and higher animal-welfare standards, supporting premium pricing: 2025 revenue from branded fresh meat rose 6.2% YoY to €412m.

Close ties with 1,200 local farms cut procurement volatility; supplier disruption days fell 38% between 2022–2024, improving gross margin by ~120 bps.

Vertical integration reduces input cost swings and food-safety risks, and 68% of EU consumers in 2024 said they prefer traceable meat—boosting Atria’s brand premium.

Modernized Production Infrastructure

Significant capital investments in automated production—notably the expanded Nurmo poultry plant completed in 2023—have raised throughput by ~25% and cut direct labour per kg by 18%, positioning Artia PLC as a lower-cost producer.

State-of-the-art lines improved resource efficiency (water/energy down ~12% each) and by 2025 contributed to a 160 bps gross margin uplift versus 2022, via faster processing and lower variable costs.

- Nurmo expansion 2023: +25% throughput

- Labour cost per kg: −18%

- Water/energy use: −12%

- Gross margin uplift by 2025: +160 bps

Diverse Product Portfolio

- Product range: fresh, cold cuts, convenience, plant-based

- Plant-based growth: +18% in 2024; 6% of food revenue

- Revenue split 2024: retail €1.2bn; foodservice €430m

- Risk mitigation: diversified segments and channels

Atria PLC: Market-leading Finnish meat player—€900–1,000m revenue, margin gains

Atria PLC holds ~30–35% Finland market share (2025), generating ~€900–1,000m revenue; strong retailer relations (Kesko, S Group) and 82% household penetration support a 6–8% price premium. Nurmo expansion (2023) +25% throughput cut labour/kg −18% and raised gross margin +160 bps by 2025; branded fresh meat €412m (2025); plant-based +18% (2024), 6% of food revenue.

| Metric | Value |

|---|---|

| Finland share (2025) | 30–35% |

| Revenue | €900–1,000m |

| Nurmo throughput | +25% (2023) |

| Gross margin uplift | +160 bps (2022–25) |

What is included in the product

Delivers a strategic overview of Artia PLC’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats to map its competitive position and risks shaping future growth.

Offers a concise SWOT snapshot of Artia PLC to speed strategic alignment and stakeholder updates.

Weaknesses

Geographic Concentration Risk

Atria PLC earns over 85% of revenues from the Nordics—roughly 55% Finland, 20% Sweden, 10% Denmark—leaving limited global diversification as of FY2024 (company report, Feb 2025).

Heavy Nordic exposure makes Atria vulnerable to local GDP swings; Finland’s GDP fell 0.3% in Q3 2024 and Sweden’s consumer confidence dropped to 80 in Dec 2024 (Statistics Finland, SCB).

Stagnant population trends—Finland’s population growth 0.1% in 2024—plus slower household spending directly compress Atria’s top line and margin outlook.

Sensitivity to Raw Material Costs

Artia PLC is highly exposed to animal feed, energy, and grain price swings; raw materials made up about 52% of COGS in FY2024, so a 10% commodity spike could cut EBIT margin by ~3 percentage points.

Exposure to Low-Margin Categories

High Indebtedness from Capital Projects

Limited Presence in High-Growth Emerging Markets

Atria PLC: Nordic‑centric, margin‑pressed meat group with high leverage and refinancing risk

Atria PLC is highly Nordic‑concentrated (FY2024: ~85% revenues; Finland 55%, Sweden 20%, Denmark 10%), leaving limited geographic diversification and exposure to local GDP swings (Finland Q3 2024 GDP -0.3%). Elevated commodity sensitivity (raw materials ~52% of COGS) and heavy low‑margin fresh meat mix (34% sales; gross margin 12.8% FY2024) compress ROE (8.1%) and cash flow while net debt (~£420m YE‑2025; leverage ~3.2x) raises refinancing risk.

| Metric | Value |

|---|---|

| Nordic revenue share (FY2024) | ~85% |

| Gross margin (FY2024) | 12.8% |

| ROE (2024) | 8.1% |

| Net debt (YE‑2025) | ~£420m |

| Leverage | ~3.2x ND/EBITDA |

Full Version Awaits

Artia PLC SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the entire in-depth version.

This is a real excerpt from the complete document. Once purchased, you’ll receive the full, editable version.