ATS Porter's Five Forces Analysis

From Overview to Strategy Blueprint

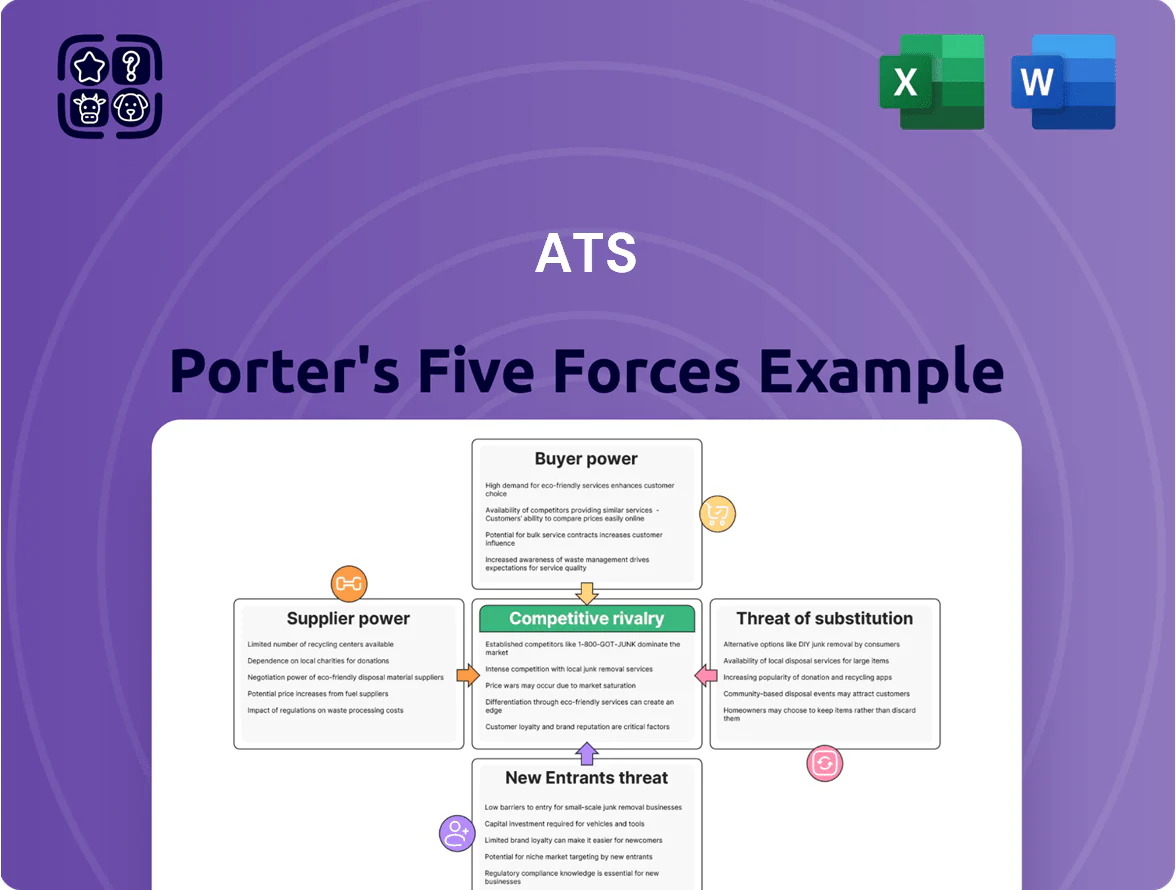

ATS faces nuanced competitive pressures—from concentrated suppliers to emerging substitutes—that shape margins and strategic choices; this snapshot highlights key dynamics but leaves deeper implications unexplored.

Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable recommendations to inform investment decisions and strategic planning.

Suppliers Bargaining Power

Specialized Component Dependency

ATS depends on a small set of specialized suppliers for high-precision sensors, robotic arms, and PLCs; industry reports show top 5 suppliers control ~60% of advanced motion components as of 2025, tightening choice.

Many parts are standardized, but custom automation needs limit qualified vendors to single digits per component, giving suppliers moderate pricing power and longer lead times (avg 18–22 weeks in 2024).

When suppliers add proprietary tech into ATS systems, they can demand 3–7% higher margins and impose stricter warranty or integration terms, raising ATS’s supplier risk.

Global Supply Chain Fragmentation

The availability of electronic components and raw materials like specialized steel depends on geopolitical stability and regional trade policies; 2024 WTO data showed 12% tariff-driven supply shifts in key Asia-Europe routes. By end-2025 ATS had diversified vendors to 48 suppliers across 6 regions, lowering single-supplier exposure to 9%, but regional monopolies for rare earths (China ~60% global output) keep supplier power high for high-performance motor inputs.

Software and AI Intellectual Property

Raw Material Price Volatility

- LME aluminum +22% (2024)

- Copper +28% (2024)

- Estimated margin hit 150–300 bps in Q3 2024

- Inflation-linked clauses common; hedging still needed

Labor Market for Technical Talent

Specialized engineering talent and skilled technicians are a vital internal supply for ATS Corporation, and shortage of high-level automation engineers at end-2025—estimated global deficit ~40,000 specialists in industrial automation—gives labor meaningful bargaining power on pay and remote/hybrid terms.

ATS competes with direct rivals and big tech for systems designers and software developers; median US automation engineer salary rose ~12% in 2024–25 to about $125,000, increasing ATS hiring costs and retention pressure.

- High scarcity: ~40,000 global shortfall

- Salary pressure: +12% (2024–25), median ~$125k US

- Competition: rivals + big tech

- Impact: higher hiring/retention costs, need for flexible work

Suppliers tighten leverage: rare-earths, metals surge & talent squeeze cut margins

Suppliers hold moderate-to-high power: top 5 control ~60% of advanced motion parts (2025), lead times averaged 18–22 weeks (2024), and rare-earths (China ~60% output) plus LME-driven metal price jumps (Al +22%, Cu +28% in 2024) squeezed margins 150–300 bps in Q3 2024; ATS diversified to 48 vendors by end-2025, cutting single-supplier exposure to ~9% but SaaS/AI platform lock-ins (enterprise AI spend $55B in 2024) and a ~40,000 engineer shortage keep supplier/labor leverage high.

| Metric | Value |

|---|---|

| Top-5 supplier share | ~60% (2025) |

| Avg lead time | 18–22 weeks (2024) |

| Vendor count | 48 (end-2025) |

| Single-supplier exposure | ~9% |

| Rare-earths (China) | ~60% global output |

| LME aluminum | +22% (2024) |

| Copper | +28% (2024) |

| Margin hit | 150–300 bps (Q3 2024) |

| Enterprise AI spend | $55B (2024) |

| Engineer shortfall | ~40,000 global (end-2025) |

What is included in the product

Concise Porter's Five Forces analysis tailored for ATS that uncovers competitive drivers, buyer and supplier influence, entry barriers, substitutes, and emerging threats to its market share, with strategic implications for pricing and profitability.

A concise, one-sheet ATS Porter’s Five Forces summary that quantifies competitive pressure and updates instantly with new hiring or technology data to speed strategic decisions.

Customers Bargaining Power

High Capital Expenditure Scrutiny

Customers in life sciences and transportation treat ATS automation systems as multi-year capital projects, often exceeding $2–10 million per installation; 2024 procurement surveys show 68% of buyers require ROI timelines under 36 months. Because of these multi-million outlays, buyers run formal RFPs, technical audits, and request uptime warranties of 99.9% or higher. This intense scrutiny gives large corporate clients strong leverage in initial contract negotiations, driving tougher pricing, longer acceptance tests, and penalty clauses. In 2025, enterprise deals accounted for roughly 74% of ATS system revenue, concentrating bargaining power.

Concentration in Regulated Industries

Switching Costs and Integration

Once an ATS automation line is embedded in a factory, switching costs—engineering rework, downtime, retraining—often exceed 20–30% of a line’s capital value, making moves to competitors prohibitively expensive; buyers thus face strong lock-in after commissioning. Customers depend on ATS for proprietary software updates, specialized spare parts and certified technicians; ATS reported 2024 recurring service revenue of €185m, highlighting ongoing reliance. Vendor lock-in cuts buyer bargaining power for price and contract terms post-installation.

Demand for Bespoke Solutions

Clients demand bespoke automation to protect their edge, so ATS differentiates but faces stronger buyer leverage to set technical milestones and KPIs; 68% of industrial buyers in 2024 said supplier customization was a top purchase criterion (Gartner, 2024).

Deep client involvement in co-design gives buyers meaningful influence over scope and final specs, increasing negotiation on price, delivery and liability.

- Customization boosts differentiation but raises buyer leverage

- 68% industrial buyers prioritize customization (Gartner 2024)

- Buyers set KPIs, milestones, and co-design scope

Performance-Linked Payment Structures

By late 2025, ~40–55% of ATS customers moved to outcome-based contracts tying payments to throughput, uptime, or yield, shifting operational risk to ATS and raising customer leverage.

These contracts make ATS financially accountable for system performance, increase buyer bargaining power, and force ongoing high-quality post-installation support to avoid penalties or price rebates.

- ~40–55% outcome-based adoption by 2025

- Payments tied to uptime/throughput/yield

- Operational risk shifts to ATS

- Higher buyer leverage via penalties/rebates

- Stronger incentive for post-install support

Enterprise buyers tighten pre-sale terms; outcome contracts shift risk to ATS—higher buyer power

Large, regulated buyers (74% enterprise revenue in 2025; pharma/medical ~42% of 2024 service sales) wield strong pre-sale leverage via RFPs, audits, 99.9% uptime demands and ROI <36 months (68% buyers, 2024); post-sale lock-in (20–30% switching cost) reduces that leverage. Outcome-based contracts (40–55% adoption by 2025) shift operational risk to ATS, raising buyer bargaining power.

| Metric | Value |

|---|---|

| Enterprise revenue share (2025) | 74% |

| Pharma/medical share (2024) | 42% |

| Buyers requiring ROI <36m (2024) | 68% |

| Switching cost (% of capex) | 20–30% |

| Outcome-based adoption (2025) | 40–55% |

Preview the Actual Deliverable

ATS Porter's Five Forces Analysis

This preview shows the exact ATS Porter's Five Forces analysis you'll receive immediately after purchase—fully written, professionally formatted, and ready for download with no placeholders.

The document displayed here is the same complete file you'll get upon payment, containing the full competitive assessment and actionable insights for immediate use.

No mockups or samples: what you see is the final deliverable and will be available to you instantly after buying.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

ATS faces nuanced competitive pressures—from concentrated suppliers to emerging substitutes—that shape margins and strategic choices; this snapshot highlights key dynamics but leaves deeper implications unexplored.

Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, visuals, and actionable recommendations to inform investment decisions and strategic planning.

Suppliers Bargaining Power

Specialized Component Dependency

ATS depends on a small set of specialized suppliers for high-precision sensors, robotic arms, and PLCs; industry reports show top 5 suppliers control ~60% of advanced motion components as of 2025, tightening choice.

Many parts are standardized, but custom automation needs limit qualified vendors to single digits per component, giving suppliers moderate pricing power and longer lead times (avg 18–22 weeks in 2024).

When suppliers add proprietary tech into ATS systems, they can demand 3–7% higher margins and impose stricter warranty or integration terms, raising ATS’s supplier risk.

Global Supply Chain Fragmentation

The availability of electronic components and raw materials like specialized steel depends on geopolitical stability and regional trade policies; 2024 WTO data showed 12% tariff-driven supply shifts in key Asia-Europe routes. By end-2025 ATS had diversified vendors to 48 suppliers across 6 regions, lowering single-supplier exposure to 9%, but regional monopolies for rare earths (China ~60% global output) keep supplier power high for high-performance motor inputs.

Software and AI Intellectual Property

Raw Material Price Volatility

- LME aluminum +22% (2024)

- Copper +28% (2024)

- Estimated margin hit 150–300 bps in Q3 2024

- Inflation-linked clauses common; hedging still needed

Labor Market for Technical Talent

Specialized engineering talent and skilled technicians are a vital internal supply for ATS Corporation, and shortage of high-level automation engineers at end-2025—estimated global deficit ~40,000 specialists in industrial automation—gives labor meaningful bargaining power on pay and remote/hybrid terms.

ATS competes with direct rivals and big tech for systems designers and software developers; median US automation engineer salary rose ~12% in 2024–25 to about $125,000, increasing ATS hiring costs and retention pressure.

- High scarcity: ~40,000 global shortfall

- Salary pressure: +12% (2024–25), median ~$125k US

- Competition: rivals + big tech

- Impact: higher hiring/retention costs, need for flexible work

Suppliers tighten leverage: rare-earths, metals surge & talent squeeze cut margins

Suppliers hold moderate-to-high power: top 5 control ~60% of advanced motion parts (2025), lead times averaged 18–22 weeks (2024), and rare-earths (China ~60% output) plus LME-driven metal price jumps (Al +22%, Cu +28% in 2024) squeezed margins 150–300 bps in Q3 2024; ATS diversified to 48 vendors by end-2025, cutting single-supplier exposure to ~9% but SaaS/AI platform lock-ins (enterprise AI spend $55B in 2024) and a ~40,000 engineer shortage keep supplier/labor leverage high.

| Metric | Value |

|---|---|

| Top-5 supplier share | ~60% (2025) |

| Avg lead time | 18–22 weeks (2024) |

| Vendor count | 48 (end-2025) |

| Single-supplier exposure | ~9% |

| Rare-earths (China) | ~60% global output |

| LME aluminum | +22% (2024) |

| Copper | +28% (2024) |

| Margin hit | 150–300 bps (Q3 2024) |

| Enterprise AI spend | $55B (2024) |

| Engineer shortfall | ~40,000 global (end-2025) |

What is included in the product

Concise Porter's Five Forces analysis tailored for ATS that uncovers competitive drivers, buyer and supplier influence, entry barriers, substitutes, and emerging threats to its market share, with strategic implications for pricing and profitability.

A concise, one-sheet ATS Porter’s Five Forces summary that quantifies competitive pressure and updates instantly with new hiring or technology data to speed strategic decisions.

Customers Bargaining Power

High Capital Expenditure Scrutiny

Customers in life sciences and transportation treat ATS automation systems as multi-year capital projects, often exceeding $2–10 million per installation; 2024 procurement surveys show 68% of buyers require ROI timelines under 36 months. Because of these multi-million outlays, buyers run formal RFPs, technical audits, and request uptime warranties of 99.9% or higher. This intense scrutiny gives large corporate clients strong leverage in initial contract negotiations, driving tougher pricing, longer acceptance tests, and penalty clauses. In 2025, enterprise deals accounted for roughly 74% of ATS system revenue, concentrating bargaining power.

Concentration in Regulated Industries

Switching Costs and Integration

Once an ATS automation line is embedded in a factory, switching costs—engineering rework, downtime, retraining—often exceed 20–30% of a line’s capital value, making moves to competitors prohibitively expensive; buyers thus face strong lock-in after commissioning. Customers depend on ATS for proprietary software updates, specialized spare parts and certified technicians; ATS reported 2024 recurring service revenue of €185m, highlighting ongoing reliance. Vendor lock-in cuts buyer bargaining power for price and contract terms post-installation.

Demand for Bespoke Solutions

Clients demand bespoke automation to protect their edge, so ATS differentiates but faces stronger buyer leverage to set technical milestones and KPIs; 68% of industrial buyers in 2024 said supplier customization was a top purchase criterion (Gartner, 2024).

Deep client involvement in co-design gives buyers meaningful influence over scope and final specs, increasing negotiation on price, delivery and liability.

- Customization boosts differentiation but raises buyer leverage

- 68% industrial buyers prioritize customization (Gartner 2024)

- Buyers set KPIs, milestones, and co-design scope

Performance-Linked Payment Structures

By late 2025, ~40–55% of ATS customers moved to outcome-based contracts tying payments to throughput, uptime, or yield, shifting operational risk to ATS and raising customer leverage.

These contracts make ATS financially accountable for system performance, increase buyer bargaining power, and force ongoing high-quality post-installation support to avoid penalties or price rebates.

- ~40–55% outcome-based adoption by 2025

- Payments tied to uptime/throughput/yield

- Operational risk shifts to ATS

- Higher buyer leverage via penalties/rebates

- Stronger incentive for post-install support

Enterprise buyers tighten pre-sale terms; outcome contracts shift risk to ATS—higher buyer power

Large, regulated buyers (74% enterprise revenue in 2025; pharma/medical ~42% of 2024 service sales) wield strong pre-sale leverage via RFPs, audits, 99.9% uptime demands and ROI <36 months (68% buyers, 2024); post-sale lock-in (20–30% switching cost) reduces that leverage. Outcome-based contracts (40–55% adoption by 2025) shift operational risk to ATS, raising buyer bargaining power.

| Metric | Value |

|---|---|

| Enterprise revenue share (2025) | 74% |

| Pharma/medical share (2024) | 42% |

| Buyers requiring ROI <36m (2024) | 68% |

| Switching cost (% of capex) | 20–30% |

| Outcome-based adoption (2025) | 40–55% |

Preview the Actual Deliverable

ATS Porter's Five Forces Analysis

This preview shows the exact ATS Porter's Five Forces analysis you'll receive immediately after purchase—fully written, professionally formatted, and ready for download with no placeholders.

The document displayed here is the same complete file you'll get upon payment, containing the full competitive assessment and actionable insights for immediate use.

No mockups or samples: what you see is the final deliverable and will be available to you instantly after buying.