AT&T PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Navigate AT&T’s future with our concise PESTLE snapshot—unpacking regulatory pressure, shifting consumer behavior, tech disruption, and macroeconomic headwinds that will shape strategy and valuation; perfect for investors and strategists who need quick, actionable context. Purchase the full PESTLE to access the complete, editable report with deep-dive insights and data-driven recommendations.

Political factors

Government Infrastructure Funding and BEAD Program

The BEAD program remains a pivotal political driver for AT&T in late 2025; AT&T has secured or competed for projects supported by BEAD’s $42.45 billion federal fund aimed at closing the rural broadband gap, enabling the company to offset substantial fiber build costs.

Spectrum Allocation and FCC Policy Shifting

Political shifts at the FCC reshape spectrum auction rules for 5G/6G; recent 2024 FCC proposals targeting mid-band reallocations could affect AT&T’s access to ~100 MHz blocks crucial for nationwide capacity.

AT&T maintains active lobbying—spending $31.2M in 2023–2024 on telecom policy—to defend incumbent-favorable licensing versus moves toward unlicensed/shared use.

Regulatory alignment determines long-term wireless throughput: restricted licensed allocations would preserve AT&T’s ability to scale cumulative network speeds and ARPU tied to premium 5G services.

National Security and Global Supply Chain Restrictions

Ongoing political tensions over international tech providers force AT&T to follow strict national security mandates; in 2024 the US expanded entity lists impacting telecom suppliers and prompted AT&T to certify supply-chain compliance for $15+ billion in federal and state contracts. AT&T must avoid restricted foreign components—especially from China—driving a shift to domestic or allied sourcing. This pivot raised procurement unit costs by an estimated 8–12% in 2023–24, squeezing margins on network upgrades.

Net Neutrality and Regulatory Oversight

The political see-saw over net neutrality keeps AT&T in an uncertain regulatory environment, with potential for reinstated strictures on traffic prioritization and paid prioritization bans under a different administration in late 2025; such shifts could affect AT&T’s 2024 wireless revenue of $111.3 billion and broadband monetization strategies.

Stricter rules would force greater pricing transparency and limit differential treatment of traffic, constraining AT&T’s ability to bundle enterprise services and prioritize low-latency applications across its 2025 nationwide 5G network footprint.

Regulatory outcomes determine how much control AT&T retains over network architecture and monetization levers, influencing capital allocation across the company’s $24.9 billion 2024 capital expenditures and future fiber investments.

- Net neutrality uncertainty may restrict paid prioritization and affect enterprise bundling revenues.

- Policy shifts impact pricing transparency requirements and competitive positioning in 5G/fiber markets.

- Regulatory limits influence capital deployment: AT&T spent $24.9B CAPEX in 2024 and reported $111.3B wireless revenue.

Public-Private Partnerships for Public Safety

The FirstNet contract, valued at roughly $6.5 billion over 25 years, anchors AT&T’s strategic political ties to the U.S. government and secures predictable revenue and infrastructure influence.

Maintaining the dedicated public-safety network—serving over 2.7 million public safety users—gives AT&T leverage in federal infrastructure talks but requires meeting strict KPIs tied to funding and renewal.

Failure to meet federal performance benchmarks risks penalties and jeopardizes expansions of FirstNet amid increased federal scrutiny of network resilience and cybersecurity.

- FirstNet contract ~$6.5B/25 years

- 2.7M+ public-safety users

- Renewal contingent on strict federal KPIs

- Noncompliance risks penalties and lost expansion

AT&T's Future Hinges on $42B BEAD, FCC Mid‑Band, FirstNet & Rising Costs

Political drivers for AT&T include BEAD funding access (~$42.45B federal BEAD program), 2024 FCC mid‑band spectrum proposals (impacting ~100 MHz blocks), lobbying spend $31.2M (2023–24), FirstNet contract ~$6.5B/25 yrs serving 2.7M+ users, supply‑chain compliance raising procurement costs ~8–12% (2023–24), net‑neutrality uncertainty affecting pricing and ARPU tied to $111.3B 2024 wireless revenue and $24.9B 2024 CAPEX.

| Item | Value/Year |

|---|---|

| BEAD fund | $42.45B |

| FCC mid‑band impact | ~100 MHz blocks |

| Lobbying | $31.2M (2023–24) |

| FirstNet | $6.5B/25 yrs; 2.7M+ users |

| Procurement cost rise | +8–12% (2023–24) |

| Wireless revenue | $111.3B (2024) |

| CAPEX | $24.9B (2024) |

What is included in the product

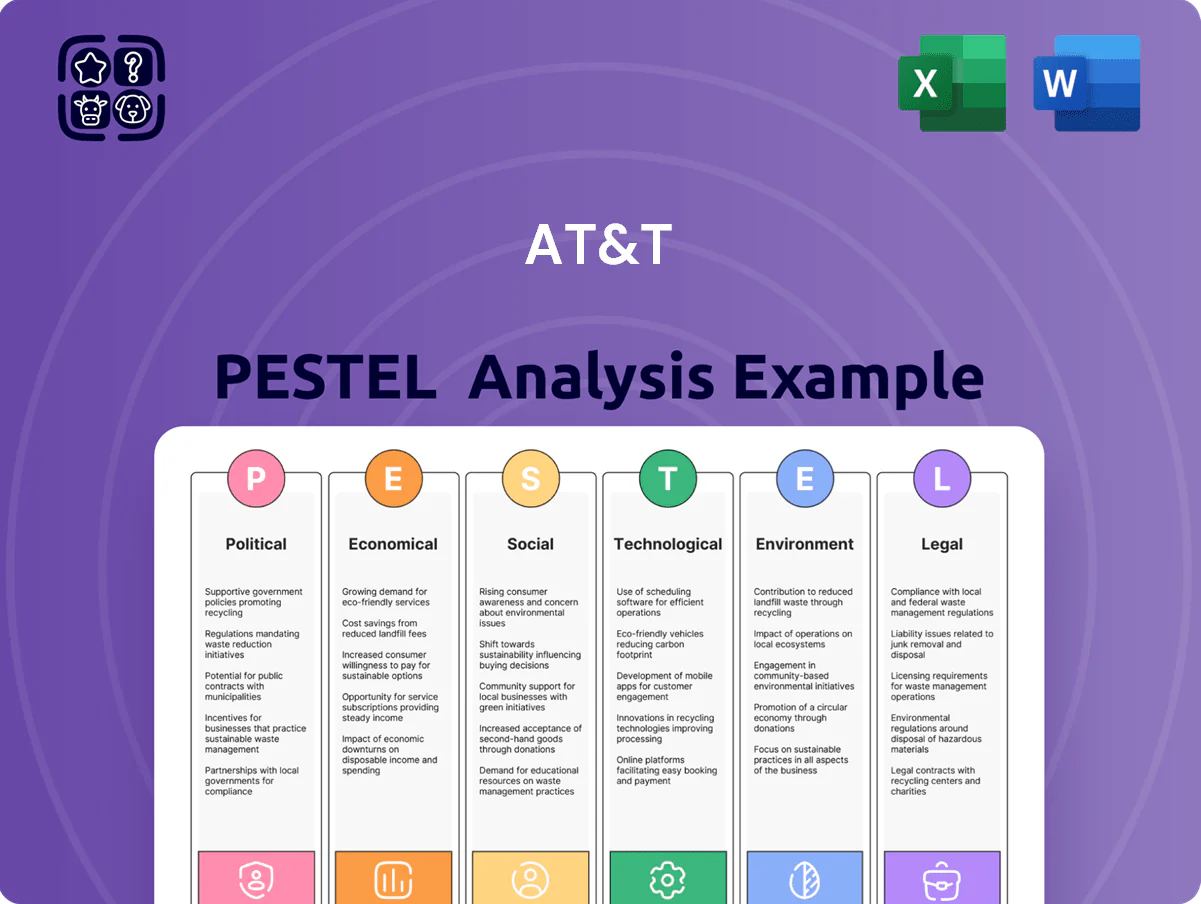

Explores how external macro-environmental factors uniquely affect AT&T across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities for executives, investors, and strategists.

A concise, shareable AT&T PESTLE snapshot organized by category for quick reference in meetings, presentations, or strategy sessions—editable for region- or business‑line–specific notes and usable across PowerPoint, Excel, and tablets.

Economic factors

Interest Rate Environment and Debt Servicing

As of end-2025, AT&T’s substantial leverage—net debt roughly $120 billion in 2024—makes it highly rate-sensitive; a 100bps rise since 2023 raises annual interest expense materially and increases refinancing costs for remaining maturities and new fiber capex. Higher rates elevate WACC and pressure free cash flow, complicating dividend coverage (2024 dividend yield ~6%) and funding of multi‑year fiber expansion unless central bank guidance stabilizes.

Inflationary Pressures on Operational Expenses

Persistent U.S. inflation, with CPI averaging about 3.4% in 2024 and energy price volatility up to ±10% year-over-year, raises AT&T’s labor, network hardware and data-center energy costs; AT&T reported $30.9B in capex in 2024, intensifying pressure on margins.

Passing increases risks churn in a saturated wireless market where postpaid ARPU rose only 1.6% in 2024, so AT&T must weigh customer elasticity before raising prices.

Economic swings forced AT&T to pursue $3–5B annual efficiency targets (announced 2024–25) and tighter opex controls to protect EBITDA margins near mid-30% levels.

Consumer Spending Power and Subscription Resilience

Consumer spending power directs plan choice: in Q4 2025 US real disposable personal income rose 1.2% YoY, supporting demand for premium unlimited plans, but 2024 recession fears pushed downgrades to prepaid options by about 3% industry-wide. Wireless service retention proved resilient—AT&T reported total wireless revenue of $36.2B in 2025, with device upgrades slowing as handset sales fell ~6% YoY. AT&T tracks consumer confidence indexes and adjusted promotions and equipment-installment plans, offering longer-term 0% financing to sustain ARPU and reduce churn.

Capital Expenditure for 5G and Fiber Integration

AT&T faces multi-billion dollar annual capital expenditure to shift from copper to a fiber-first, 5G-integrated network—CapEx guidance was about $21–23 billion for 2024 with continued heavy spend into 2025 to expand fiber and 5G coverage.

Management must show clear ROI to shareholders while vying for limited capital against competitors like Verizon and Charter; private funding and asset sales (e.g., past divestitures) influence pace.

Transition speed depends on availability of private capital, project IRRs, and the economic viability of new market entrants driving competitive pressure.

- AT&T 2024 CapEx ~ $21–23B; continued multi-year spend expected

- ROI expectations pressure deployment pace amid competing capital needs

- Private capital/access to funding and new entrants’ economics dictate transition speed

Competitive Pricing and Market Saturation

The U.S. wireless market’s ~87% smartphone penetration and four-player structure limit AT&T’s organic growth, driving FY2025 focus on bundling wireless with fiber to boost ARPU (wireless+wireline ARPU rose to about $175 in 2024 vs $162 in 2022).

Aggressive bundling aims to offset saturated net adds (postpaid phone net adds at ~+1.2M in 2024) while making churn (postpaid phone churn 0.77% in Q4 2024) critical to stability and margins.

- Market saturation: ~87% smartphone penetration

- ARPU focus: ~$175 combined ARPU (2024)

- Growth constrained: ~+1.2M postpaid net adds (2024)

- Churn critical: 0.77% postpaid phone churn (Q4 2024)

AT&T: High $120B Debt, Rate-Sensitive; Efficiency & CapEx Key to Sustaining 6% Yield

High leverage (net debt ~$120B in 2024) makes AT&T rate-sensitive; 100bps hikes raise interest expense and WACC, pressuring FCF and dividend (~6% yield 2024). CPI ~3.4% in 2024 and ±10% energy swings lift labor, hardware, and energy costs against $30.9B capex (2024) and $21–23B guidance; ARPU constraints (postpaid ARPU +1.6% 2024) limit pricing power, so efficiency targets $3–5B/yr sustain margins.

| Metric | Value (Year) |

|---|---|

| Net debt | $120B (2024) |

| CapEx | $30.9B (2024) |

| CapEx guidance | $21–23B (2024) |

| Dividend yield | ~6% (2024) |

| CPI | ~3.4% (2024) |

| Postpaid ARPU growth | +1.6% (2024) |

| Efficiency target | $3–5B/yr (2024–25) |

Preview the Actual Deliverable

AT&T PESTLE Analysis

The preview shown here is the exact AT&T PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Navigate AT&T’s future with our concise PESTLE snapshot—unpacking regulatory pressure, shifting consumer behavior, tech disruption, and macroeconomic headwinds that will shape strategy and valuation; perfect for investors and strategists who need quick, actionable context. Purchase the full PESTLE to access the complete, editable report with deep-dive insights and data-driven recommendations.

Political factors

Government Infrastructure Funding and BEAD Program

The BEAD program remains a pivotal political driver for AT&T in late 2025; AT&T has secured or competed for projects supported by BEAD’s $42.45 billion federal fund aimed at closing the rural broadband gap, enabling the company to offset substantial fiber build costs.

Spectrum Allocation and FCC Policy Shifting

Political shifts at the FCC reshape spectrum auction rules for 5G/6G; recent 2024 FCC proposals targeting mid-band reallocations could affect AT&T’s access to ~100 MHz blocks crucial for nationwide capacity.

AT&T maintains active lobbying—spending $31.2M in 2023–2024 on telecom policy—to defend incumbent-favorable licensing versus moves toward unlicensed/shared use.

Regulatory alignment determines long-term wireless throughput: restricted licensed allocations would preserve AT&T’s ability to scale cumulative network speeds and ARPU tied to premium 5G services.

National Security and Global Supply Chain Restrictions

Ongoing political tensions over international tech providers force AT&T to follow strict national security mandates; in 2024 the US expanded entity lists impacting telecom suppliers and prompted AT&T to certify supply-chain compliance for $15+ billion in federal and state contracts. AT&T must avoid restricted foreign components—especially from China—driving a shift to domestic or allied sourcing. This pivot raised procurement unit costs by an estimated 8–12% in 2023–24, squeezing margins on network upgrades.

Net Neutrality and Regulatory Oversight

The political see-saw over net neutrality keeps AT&T in an uncertain regulatory environment, with potential for reinstated strictures on traffic prioritization and paid prioritization bans under a different administration in late 2025; such shifts could affect AT&T’s 2024 wireless revenue of $111.3 billion and broadband monetization strategies.

Stricter rules would force greater pricing transparency and limit differential treatment of traffic, constraining AT&T’s ability to bundle enterprise services and prioritize low-latency applications across its 2025 nationwide 5G network footprint.

Regulatory outcomes determine how much control AT&T retains over network architecture and monetization levers, influencing capital allocation across the company’s $24.9 billion 2024 capital expenditures and future fiber investments.

- Net neutrality uncertainty may restrict paid prioritization and affect enterprise bundling revenues.

- Policy shifts impact pricing transparency requirements and competitive positioning in 5G/fiber markets.

- Regulatory limits influence capital deployment: AT&T spent $24.9B CAPEX in 2024 and reported $111.3B wireless revenue.

Public-Private Partnerships for Public Safety

The FirstNet contract, valued at roughly $6.5 billion over 25 years, anchors AT&T’s strategic political ties to the U.S. government and secures predictable revenue and infrastructure influence.

Maintaining the dedicated public-safety network—serving over 2.7 million public safety users—gives AT&T leverage in federal infrastructure talks but requires meeting strict KPIs tied to funding and renewal.

Failure to meet federal performance benchmarks risks penalties and jeopardizes expansions of FirstNet amid increased federal scrutiny of network resilience and cybersecurity.

- FirstNet contract ~$6.5B/25 years

- 2.7M+ public-safety users

- Renewal contingent on strict federal KPIs

- Noncompliance risks penalties and lost expansion

AT&T's Future Hinges on $42B BEAD, FCC Mid‑Band, FirstNet & Rising Costs

Political drivers for AT&T include BEAD funding access (~$42.45B federal BEAD program), 2024 FCC mid‑band spectrum proposals (impacting ~100 MHz blocks), lobbying spend $31.2M (2023–24), FirstNet contract ~$6.5B/25 yrs serving 2.7M+ users, supply‑chain compliance raising procurement costs ~8–12% (2023–24), net‑neutrality uncertainty affecting pricing and ARPU tied to $111.3B 2024 wireless revenue and $24.9B 2024 CAPEX.

| Item | Value/Year |

|---|---|

| BEAD fund | $42.45B |

| FCC mid‑band impact | ~100 MHz blocks |

| Lobbying | $31.2M (2023–24) |

| FirstNet | $6.5B/25 yrs; 2.7M+ users |

| Procurement cost rise | +8–12% (2023–24) |

| Wireless revenue | $111.3B (2024) |

| CAPEX | $24.9B (2024) |

What is included in the product

Explores how external macro-environmental factors uniquely affect AT&T across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities for executives, investors, and strategists.

A concise, shareable AT&T PESTLE snapshot organized by category for quick reference in meetings, presentations, or strategy sessions—editable for region- or business‑line–specific notes and usable across PowerPoint, Excel, and tablets.

Economic factors

Interest Rate Environment and Debt Servicing

As of end-2025, AT&T’s substantial leverage—net debt roughly $120 billion in 2024—makes it highly rate-sensitive; a 100bps rise since 2023 raises annual interest expense materially and increases refinancing costs for remaining maturities and new fiber capex. Higher rates elevate WACC and pressure free cash flow, complicating dividend coverage (2024 dividend yield ~6%) and funding of multi‑year fiber expansion unless central bank guidance stabilizes.

Inflationary Pressures on Operational Expenses

Persistent U.S. inflation, with CPI averaging about 3.4% in 2024 and energy price volatility up to ±10% year-over-year, raises AT&T’s labor, network hardware and data-center energy costs; AT&T reported $30.9B in capex in 2024, intensifying pressure on margins.

Passing increases risks churn in a saturated wireless market where postpaid ARPU rose only 1.6% in 2024, so AT&T must weigh customer elasticity before raising prices.

Economic swings forced AT&T to pursue $3–5B annual efficiency targets (announced 2024–25) and tighter opex controls to protect EBITDA margins near mid-30% levels.

Consumer Spending Power and Subscription Resilience

Consumer spending power directs plan choice: in Q4 2025 US real disposable personal income rose 1.2% YoY, supporting demand for premium unlimited plans, but 2024 recession fears pushed downgrades to prepaid options by about 3% industry-wide. Wireless service retention proved resilient—AT&T reported total wireless revenue of $36.2B in 2025, with device upgrades slowing as handset sales fell ~6% YoY. AT&T tracks consumer confidence indexes and adjusted promotions and equipment-installment plans, offering longer-term 0% financing to sustain ARPU and reduce churn.

Capital Expenditure for 5G and Fiber Integration

AT&T faces multi-billion dollar annual capital expenditure to shift from copper to a fiber-first, 5G-integrated network—CapEx guidance was about $21–23 billion for 2024 with continued heavy spend into 2025 to expand fiber and 5G coverage.

Management must show clear ROI to shareholders while vying for limited capital against competitors like Verizon and Charter; private funding and asset sales (e.g., past divestitures) influence pace.

Transition speed depends on availability of private capital, project IRRs, and the economic viability of new market entrants driving competitive pressure.

- AT&T 2024 CapEx ~ $21–23B; continued multi-year spend expected

- ROI expectations pressure deployment pace amid competing capital needs

- Private capital/access to funding and new entrants’ economics dictate transition speed

Competitive Pricing and Market Saturation

The U.S. wireless market’s ~87% smartphone penetration and four-player structure limit AT&T’s organic growth, driving FY2025 focus on bundling wireless with fiber to boost ARPU (wireless+wireline ARPU rose to about $175 in 2024 vs $162 in 2022).

Aggressive bundling aims to offset saturated net adds (postpaid phone net adds at ~+1.2M in 2024) while making churn (postpaid phone churn 0.77% in Q4 2024) critical to stability and margins.

- Market saturation: ~87% smartphone penetration

- ARPU focus: ~$175 combined ARPU (2024)

- Growth constrained: ~+1.2M postpaid net adds (2024)

- Churn critical: 0.77% postpaid phone churn (Q4 2024)

AT&T: High $120B Debt, Rate-Sensitive; Efficiency & CapEx Key to Sustaining 6% Yield

High leverage (net debt ~$120B in 2024) makes AT&T rate-sensitive; 100bps hikes raise interest expense and WACC, pressuring FCF and dividend (~6% yield 2024). CPI ~3.4% in 2024 and ±10% energy swings lift labor, hardware, and energy costs against $30.9B capex (2024) and $21–23B guidance; ARPU constraints (postpaid ARPU +1.6% 2024) limit pricing power, so efficiency targets $3–5B/yr sustain margins.

| Metric | Value (Year) |

|---|---|

| Net debt | $120B (2024) |

| CapEx | $30.9B (2024) |

| CapEx guidance | $21–23B (2024) |

| Dividend yield | ~6% (2024) |

| CPI | ~3.4% (2024) |

| Postpaid ARPU growth | +1.6% (2024) |

| Efficiency target | $3–5B/yr (2024–25) |

Preview the Actual Deliverable

AT&T PESTLE Analysis

The preview shown here is the exact AT&T PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.