Attijariwafa Bank Boston Consulting Group Matrix

Download Your Competitive Advantage

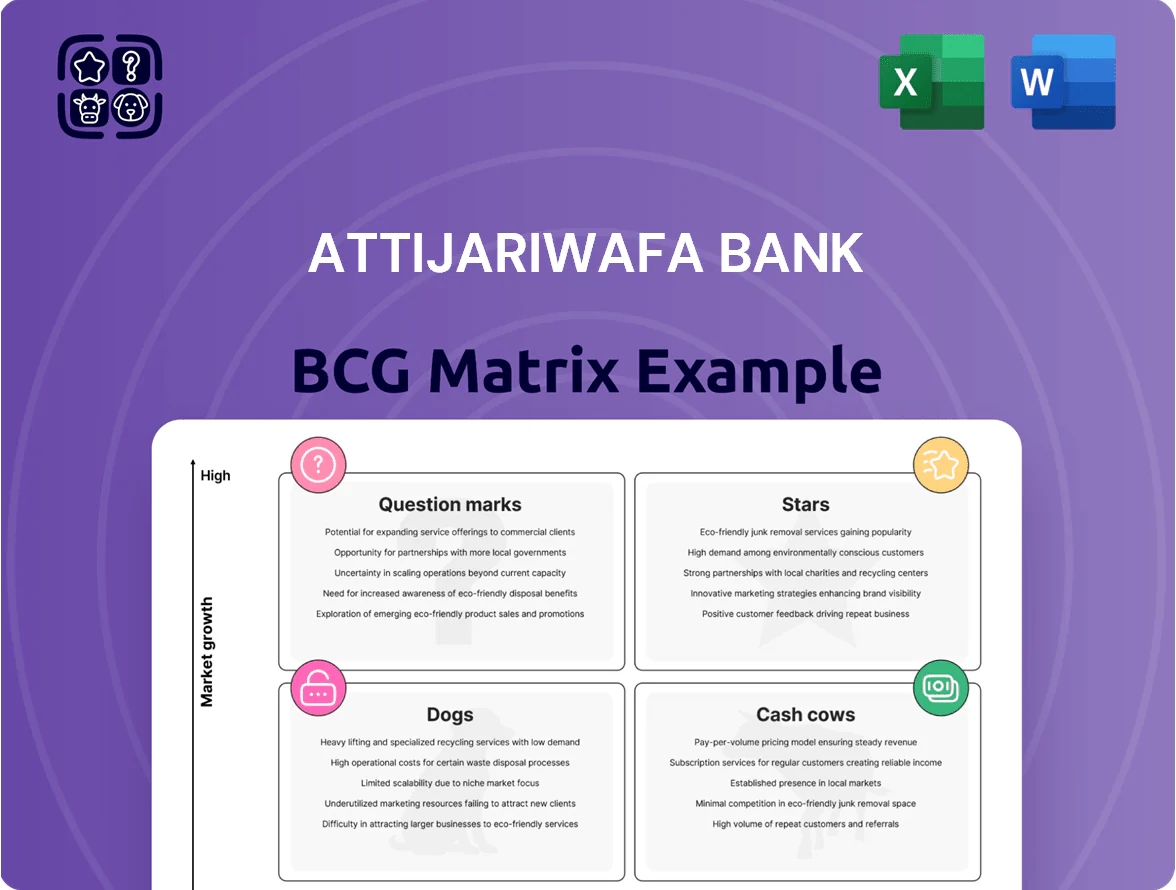

Attijariwafa Bank’s BCG Matrix preview highlights its core banking segments and competitive dynamics—showing where retail banking, corporate finance, and digital services may fall among Stars, Cash Cows, Question Marks, or Dogs as market growth and relative share shift. This snapshot teases strategic implications for capital allocation and portfolio pruning but doesn’t give the quadrant-level detail you need to act. Purchase the full BCG Matrix report for a complete, data-backed breakdown, quadrant mappings, and actionable recommendations in Word and Excel to guide investment and strategic decisions.

Stars

Digital Banking and Fintech Integration

Attijariwafa Bank’s digital arm L'Bankalik has been aggressively scaled to capture Morocco’s tech-savvy youth and unbanked segments, reaching an estimated 2.4 million users and ~35% market share of Moroccan digital banking by end-2025.

The unit benefits from Africa’s double-digit mobile finance growth—mobile money transaction value in Morocco rose ~28% YoY in 2024—and L'Bankalik posted 18% annual user growth in 2025.

The BCG position is a Star: high relative market share and rapid market growth, prompting reinvestment of about MAD 1.2 billion (2023–25) to sustain tech leadership and fend off neo-banks.

Sub-Saharan African Expansion (WAEMU & CEMAC)

Attijariwafa Bank’s subsidiaries in WAEMU and CEMAC are high-growth engines, with pooled loans up ~18% y/y to €6.2bn in 2024 and market share gains in key countries (e.g., Senegal +210bp, Cameroon +160bp). These markets show credit penetration below 25% of GDP versus North Africa’s 60%, signaling large untapped demand for retail and trade finance.

Green Finance and ESG-Linked Lending

Attijariwafa Bank dominates Morocco’s renewable financing, leading arrangments for solar and wind projects that account for over 60% of project financing in 2024, backing 1.2 GW of capacity and committing roughly MAD 9.5bn (≈USD 930m) in green loans.

Corporate and Investment Banking (CIB) in Emerging Markets

Attijariwafa Bank’s Corporate and Investment Banking (CIB) is a regional Star, leading South-South cross-border M&A and infrastructure advisory with ~25% market share in Francophone Africa deals in 2024 and advising on projects totalling $6.1bn in 2023–24.

Demand for structured finance and syndication is rising with African industrial investment up 14% YoY; the CIB needs senior deal teams and deep liquidity but can secure dominant market leadership.

- ~25% share in Francophone Africa M&A (2024)

- $6.1bn advised in infra deals (2023–24)

- Industrial investment +14% YoY

- Requires senior bankers, syndication lines, capital buffer

Wealth Management and Private Banking

Wealth Management and Private Banking targets a rising HNWI base in North and West Africa, where HNWIs grew ~8% annually to ~95,000 people in 2024, marking high market growth and a strong competitive position for Attijariwafa Bank.

Attijariwafa leverages its 4,000-branch regional network and 2024 AUM growth of ~14% to deliver bespoke investment products that often outperform local peers on returns and client retention.

Continued investment in specialized digital platforms and ties with global partners (Europe, MENA) is essential to meet evolving affluent-client needs and sustain double-digit AUM growth.

- HNWI count ~95,000 in 2024, +8% YoY

- AUM growth ~14% in 2024

- 4,000 regional branches

- Priority: digital platforms + international partnerships

High-growth leaders: L'Bankalik, CIB, Renewables & Wealth drive scale and returns

Stars: L'Bankalik, CIB, renewables financing and Wealth Management are high-share, high-growth units—L'Bankalik 2.4M users (~35% digital share, 18% user growth 2025); CIB ~25% Francophone M&A share (2024), $6.1bn advised (2023–24); renewables 1.2GW, MAD 9.5bn green loans (2024); AUM +14%, HNWI ~95,000 (+8% 2024).

| Unit | Key metric | 2024–25 |

|---|---|---|

| L'Bankalik | Users / digital share | 2.4M / ~35% |

| CIB | M&A share / advised | ~25% / $6.1bn |

| Renewables | Capacity / green loans | 1.2GW / MAD 9.5bn |

| Wealth | AUM growth / HNWI | +14% / 95,000 |

What is included in the product

BCG analysis of Attijariwafa Bank: quadrant-by-quadrant strategic guidance highlighting Stars, Cash Cows, Question Marks, Dogs with investment and divestment recommendations.

One-page Attijariwafa Bank BCG Matrix placing each business unit in a quadrant for swift portfolio prioritization.

Cash Cows

Moroccan Retail Banking

Moroccan retail banking is Attijariwafa Bank’s foundational cash cow, holding ~30% market share in a mature domestic market with GDP growth 1.5% in 2024 and banking penetration ~70%. It delivers steady high-volume net interest margin cash flow—group domestic deposits totaled €24.5bn in 2024—requiring low capex and marketing spend.

Group liquidity from Moroccan deposits funds expansion in West Africa and MENA stars and supports steady dividends: Attijariwafa paid €0.28 per share in 2024, while ~40% of FY2024 operating cash flow originated domestically.

Consumer Credit (Wafasalaf)

Wafasalaf leads Morocco’s consumer lending with ~40% market share in 2024 and loan book ~MAD 18.2bn (≈USD 1.7bn), in a mature market growing ~2% annually.

High operational efficiency (cost/income ~38% in 2024) and strong brand yield net margins near 18%, needing low capex.

It reliably funds Attijariwafa Bank’s digital bets, contributing ~12% of group net income in 2024.

Leasing and Factoring Services (Wafabail)

As market leader, Wafabail (Attijariwafa Bank’s leasing and factoring arm) serves 8,200+ corporate clients and posted 2024 net revenue of MAD 1.1bn, leveraging deep credit processes and high client loyalty.

Morocco’s traditional leasing market grew 3.8% in 2024 and is mature, producing stable cash inflows and low volatility—Wafabail’s NPL ratio stood at 2.7% in 2024.

These predictable cash flows funded MAD 4.6bn of group corporate debt service in 2024 and bolster Attijariwafa’s CET1 ratio, supporting balance-sheet strength.

Bancassurance (Wafa Assurance)

Bancassurance via Wafa Assurance posts ~35% bancassurance penetration in Morocco and Wafa holds ~28% market share in premiums (2024), making it a dominant, mature cash cow with slowing life/non-life growth under 3% annually; it requires minimal capex and funds group ROE, contributing ~150 bps to Attijariwafa Bank’s 2024 return on equity.

- High bancassurance reach: ~35% penetration (2024)

- Market share: ~28% of Moroccan insurance premiums (2024)

- Growth: ≈<3% YoY in traditional segments (2024)

- ROE support: ~150 basis points contribution (2024)

- Low reinvestment need; steady cash generation

Trade Finance for Established Corporates

Attijariwafa Bank handles trade finance for Morocco’s top industrials and exporters, covering an estimated 35–40% market share in export-linked credit lines as of 2025 and processing roughly MAD 120 billion annually in documentary credits and guarantees.

This is a mature, high-barrier segment—long-standing client relationships, regulatory know-how, and correspondent networks—delivering stable fee revenue (about MAD 1.1 billion in 2024) that funds acquisitions and strategic investments.

- Stable fee income: ~MAD 1.1bn (2024)

- Annual trade flows: ~MAD 120bn (2025)

- Market share: 35–40% (export-linked)

- High barriers: compliance, networks, client tenure

- Provides acquisition dry powder

Attijariwafa cash cows: retail, Wafasalaf, Wafabail & assurance fuel 40% of 2024 cash flow

Attijariwafa’s Moroccan retail banking, Wafasalaf, Wafabail and Wafa Assurance are cash cows: combined domestic deposits €24.5bn (2024), Wafasalaf loans MAD 18.2bn (≈USD1.7bn, 2024), Wafabail rev MAD1.1bn (2024), bancassurance premium share 28% with ~35% penetration (2024); together funded €0.28/share dividend and ~40% of FY2024 operating cash flow.

| Metric | 2024 |

|---|---|

| Deposits | €24.5bn |

| Wafasalaf loans | MAD18.2bn |

| Wafabail rev | MAD1.1bn |

| Bancassurance share | 28% |

Preview = Final Product

Attijariwafa Bank BCG Matrix

The file you're previewing is the exact Attijariwafa Bank BCG Matrix report you'll receive after purchase—no watermarks, no placeholders, just the fully formatted, analysis-ready document crafted for strategic clarity and professional presentation.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Download Your Competitive Advantage

Attijariwafa Bank’s BCG Matrix preview highlights its core banking segments and competitive dynamics—showing where retail banking, corporate finance, and digital services may fall among Stars, Cash Cows, Question Marks, or Dogs as market growth and relative share shift. This snapshot teases strategic implications for capital allocation and portfolio pruning but doesn’t give the quadrant-level detail you need to act. Purchase the full BCG Matrix report for a complete, data-backed breakdown, quadrant mappings, and actionable recommendations in Word and Excel to guide investment and strategic decisions.

Stars

Digital Banking and Fintech Integration

Attijariwafa Bank’s digital arm L'Bankalik has been aggressively scaled to capture Morocco’s tech-savvy youth and unbanked segments, reaching an estimated 2.4 million users and ~35% market share of Moroccan digital banking by end-2025.

The unit benefits from Africa’s double-digit mobile finance growth—mobile money transaction value in Morocco rose ~28% YoY in 2024—and L'Bankalik posted 18% annual user growth in 2025.

The BCG position is a Star: high relative market share and rapid market growth, prompting reinvestment of about MAD 1.2 billion (2023–25) to sustain tech leadership and fend off neo-banks.

Sub-Saharan African Expansion (WAEMU & CEMAC)

Attijariwafa Bank’s subsidiaries in WAEMU and CEMAC are high-growth engines, with pooled loans up ~18% y/y to €6.2bn in 2024 and market share gains in key countries (e.g., Senegal +210bp, Cameroon +160bp). These markets show credit penetration below 25% of GDP versus North Africa’s 60%, signaling large untapped demand for retail and trade finance.

Green Finance and ESG-Linked Lending

Attijariwafa Bank dominates Morocco’s renewable financing, leading arrangments for solar and wind projects that account for over 60% of project financing in 2024, backing 1.2 GW of capacity and committing roughly MAD 9.5bn (≈USD 930m) in green loans.

Corporate and Investment Banking (CIB) in Emerging Markets

Attijariwafa Bank’s Corporate and Investment Banking (CIB) is a regional Star, leading South-South cross-border M&A and infrastructure advisory with ~25% market share in Francophone Africa deals in 2024 and advising on projects totalling $6.1bn in 2023–24.

Demand for structured finance and syndication is rising with African industrial investment up 14% YoY; the CIB needs senior deal teams and deep liquidity but can secure dominant market leadership.

- ~25% share in Francophone Africa M&A (2024)

- $6.1bn advised in infra deals (2023–24)

- Industrial investment +14% YoY

- Requires senior bankers, syndication lines, capital buffer

Wealth Management and Private Banking

Wealth Management and Private Banking targets a rising HNWI base in North and West Africa, where HNWIs grew ~8% annually to ~95,000 people in 2024, marking high market growth and a strong competitive position for Attijariwafa Bank.

Attijariwafa leverages its 4,000-branch regional network and 2024 AUM growth of ~14% to deliver bespoke investment products that often outperform local peers on returns and client retention.

Continued investment in specialized digital platforms and ties with global partners (Europe, MENA) is essential to meet evolving affluent-client needs and sustain double-digit AUM growth.

- HNWI count ~95,000 in 2024, +8% YoY

- AUM growth ~14% in 2024

- 4,000 regional branches

- Priority: digital platforms + international partnerships

High-growth leaders: L'Bankalik, CIB, Renewables & Wealth drive scale and returns

Stars: L'Bankalik, CIB, renewables financing and Wealth Management are high-share, high-growth units—L'Bankalik 2.4M users (~35% digital share, 18% user growth 2025); CIB ~25% Francophone M&A share (2024), $6.1bn advised (2023–24); renewables 1.2GW, MAD 9.5bn green loans (2024); AUM +14%, HNWI ~95,000 (+8% 2024).

| Unit | Key metric | 2024–25 |

|---|---|---|

| L'Bankalik | Users / digital share | 2.4M / ~35% |

| CIB | M&A share / advised | ~25% / $6.1bn |

| Renewables | Capacity / green loans | 1.2GW / MAD 9.5bn |

| Wealth | AUM growth / HNWI | +14% / 95,000 |

What is included in the product

BCG analysis of Attijariwafa Bank: quadrant-by-quadrant strategic guidance highlighting Stars, Cash Cows, Question Marks, Dogs with investment and divestment recommendations.

One-page Attijariwafa Bank BCG Matrix placing each business unit in a quadrant for swift portfolio prioritization.

Cash Cows

Moroccan Retail Banking

Moroccan retail banking is Attijariwafa Bank’s foundational cash cow, holding ~30% market share in a mature domestic market with GDP growth 1.5% in 2024 and banking penetration ~70%. It delivers steady high-volume net interest margin cash flow—group domestic deposits totaled €24.5bn in 2024—requiring low capex and marketing spend.

Group liquidity from Moroccan deposits funds expansion in West Africa and MENA stars and supports steady dividends: Attijariwafa paid €0.28 per share in 2024, while ~40% of FY2024 operating cash flow originated domestically.

Consumer Credit (Wafasalaf)

Wafasalaf leads Morocco’s consumer lending with ~40% market share in 2024 and loan book ~MAD 18.2bn (≈USD 1.7bn), in a mature market growing ~2% annually.

High operational efficiency (cost/income ~38% in 2024) and strong brand yield net margins near 18%, needing low capex.

It reliably funds Attijariwafa Bank’s digital bets, contributing ~12% of group net income in 2024.

Leasing and Factoring Services (Wafabail)

As market leader, Wafabail (Attijariwafa Bank’s leasing and factoring arm) serves 8,200+ corporate clients and posted 2024 net revenue of MAD 1.1bn, leveraging deep credit processes and high client loyalty.

Morocco’s traditional leasing market grew 3.8% in 2024 and is mature, producing stable cash inflows and low volatility—Wafabail’s NPL ratio stood at 2.7% in 2024.

These predictable cash flows funded MAD 4.6bn of group corporate debt service in 2024 and bolster Attijariwafa’s CET1 ratio, supporting balance-sheet strength.

Bancassurance (Wafa Assurance)

Bancassurance via Wafa Assurance posts ~35% bancassurance penetration in Morocco and Wafa holds ~28% market share in premiums (2024), making it a dominant, mature cash cow with slowing life/non-life growth under 3% annually; it requires minimal capex and funds group ROE, contributing ~150 bps to Attijariwafa Bank’s 2024 return on equity.

- High bancassurance reach: ~35% penetration (2024)

- Market share: ~28% of Moroccan insurance premiums (2024)

- Growth: ≈<3% YoY in traditional segments (2024)

- ROE support: ~150 basis points contribution (2024)

- Low reinvestment need; steady cash generation

Trade Finance for Established Corporates

Attijariwafa Bank handles trade finance for Morocco’s top industrials and exporters, covering an estimated 35–40% market share in export-linked credit lines as of 2025 and processing roughly MAD 120 billion annually in documentary credits and guarantees.

This is a mature, high-barrier segment—long-standing client relationships, regulatory know-how, and correspondent networks—delivering stable fee revenue (about MAD 1.1 billion in 2024) that funds acquisitions and strategic investments.

- Stable fee income: ~MAD 1.1bn (2024)

- Annual trade flows: ~MAD 120bn (2025)

- Market share: 35–40% (export-linked)

- High barriers: compliance, networks, client tenure

- Provides acquisition dry powder

Attijariwafa cash cows: retail, Wafasalaf, Wafabail & assurance fuel 40% of 2024 cash flow

Attijariwafa’s Moroccan retail banking, Wafasalaf, Wafabail and Wafa Assurance are cash cows: combined domestic deposits €24.5bn (2024), Wafasalaf loans MAD 18.2bn (≈USD1.7bn, 2024), Wafabail rev MAD1.1bn (2024), bancassurance premium share 28% with ~35% penetration (2024); together funded €0.28/share dividend and ~40% of FY2024 operating cash flow.

| Metric | 2024 |

|---|---|

| Deposits | €24.5bn |

| Wafasalaf loans | MAD18.2bn |

| Wafabail rev | MAD1.1bn |

| Bancassurance share | 28% |

Preview = Final Product

Attijariwafa Bank BCG Matrix

The file you're previewing is the exact Attijariwafa Bank BCG Matrix report you'll receive after purchase—no watermarks, no placeholders, just the fully formatted, analysis-ready document crafted for strategic clarity and professional presentation.