Auric Group Porter's Five Forces Analysis

Don't Miss the Bigger Picture

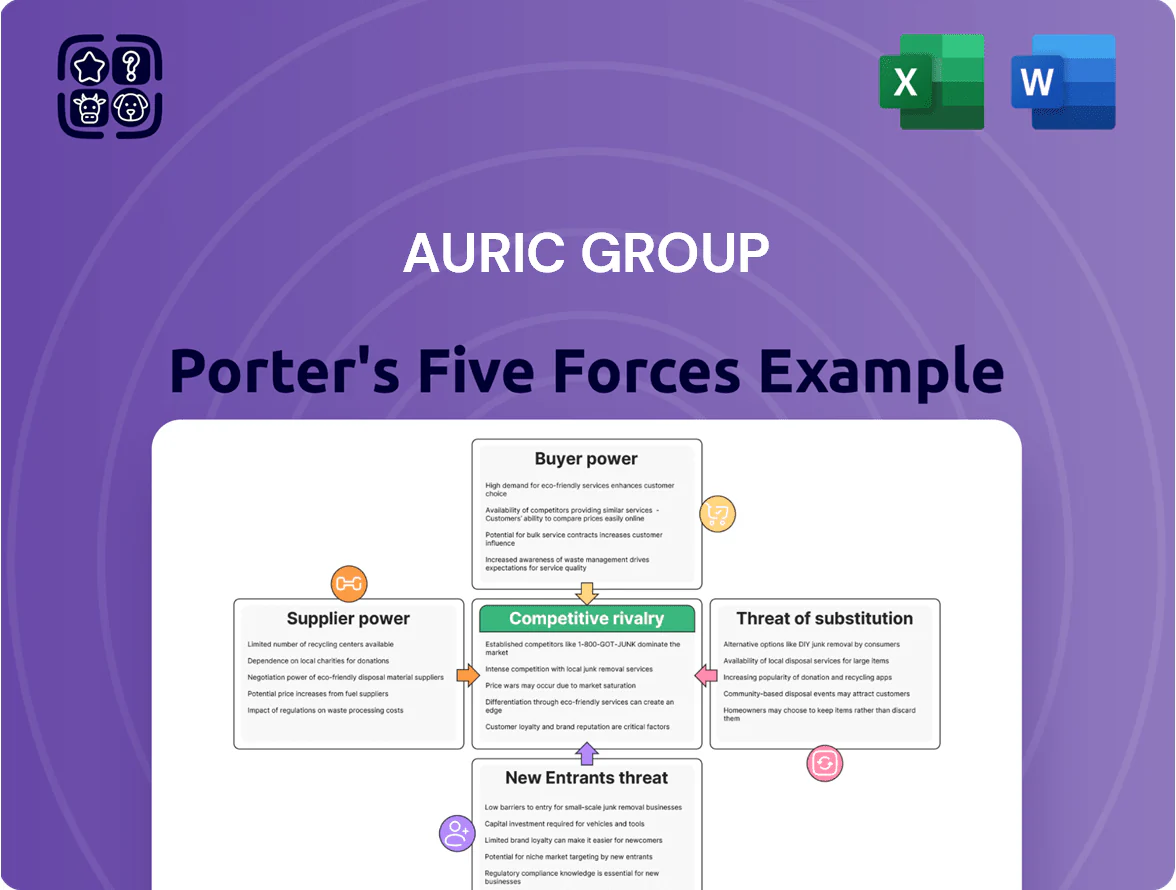

Auric Group faces moderate supplier power and rising buyer sophistication, while new entrants are deterred by capital and brand barriers, and substitutes pose niche threats—creating a dynamic competitive landscape that demands strategic clarity.

Suppliers Bargaining Power

Raw Material Commodity Fluctuations

Portfolio companies face margin pressure from swings in prices for coffee, spices and botanical extracts; coffee bean costs rose 28% year-over-year to Q3 2025, squeezing COGS.

Suppliers of rare organic extracts command premium pricing and stricter terms after 2024–25 supply shocks, raising procurement risk.

Auric must diversify vendors across Latin America, Africa and SE Asia; adding 3–5 alternative suppliers per key ingredient can cut price volatility exposure by ~15–20%.

Supplier Consolidation in Specialized Segments

In wellness and lifestyle, roughly 12 certified global suppliers control high-end organic ingredients, letting them set prices and stricter credit terms that squeeze smaller brands’ margins.

Auric Group offsets this by pooling demand across 18 subsidiaries, negotiating 15–25% better volume discounts and extending supplier credit from 30 to 60 days on average in 2025.

Impact of Sustainability and ESG Standards

Suppliers with ESG (environmental, social, governance) certifications command higher leverage as consumer demand for ethical brands rose 42% globally between 2019–2024, per McKinsey; Auric Group’s portfolio needs these certifications to protect brand integrity, so compliant vendors often charge 5–15% price premiums, keeping supplier power high.

Logistics and Packaging Provider Influence

Labor Market Constraints in Production

Suppliers of manufacturing and co-packing face rising labor costs—wages up ~6–8% in Southeast Asia in 2024—and skilled staff shortages, pushing service fees higher and extending lead times by 10–25% for new product launches.

Auric Group flags these trends to portfolio companies, adjusts contract terms, and diversifies co-packers to protect margins and time-to-market.

- Wage growth 6–8% (2024, regional average)

- Lead-time increases 10–25%

- Higher service fees passed to investors

Auric combats soaring input costs with pooled buying, long-term contracts & $5–10M CAPEX

Suppliers exert high bargaining power: coffee bean costs +28% YoY to Q3 2025 and eco-materials +18% in 2025, niche organic extract premiums 5–15%, wage inflation 6–8% (2024) and lead-times +10–25% raise COGS and launch risk; Auric offsets via pooled buying (18 subsidiaries) to secure 15–25% volume discounts and supplier credit extension to 60 days, and should sign 3–5 year contracts or invest $5–10m in packaging CAPEX.

| Metric | Value |

|---|---|

| Coffee cost change | +28% YoY to Q3 2025 |

| Eco-materials | +18% (2025) |

| Organic extract premium | 5–15% |

| Wage growth (SE Asia) | 6–8% (2024) |

| Lead-time impact | +10–25% |

| Volume discount (pooled) | 15–25% |

| Packaging CAPEX | $5–10m |

What is included in the product

Tailored Porter's Five Forces analysis for Auric Group, uncovering competitive drivers, supplier and buyer influence, entry barriers, substitutes, and emerging threats to its market position, with strategic insights for investors and executives.

A concise Porter's Five Forces snapshot tailored to Auric Group—instant clarity on competitive pressures for faster strategic choices.

Customers Bargaining Power

Retailer Dominance in Distribution Channels

Major supermarket chains and wellness retailers command shelf space and reach, forcing Auric Group brands to accept discounts, slotting fees and co-op marketing that can cut gross margins by 5–12 percentage points; India’s top 5 grocery chains control ~60% of modern retail, amplifying this leverage. Maintaining and scaling Direct-to-Consumer sales—Auric reported DTC growth of ~28% in FY2024—helps reclaim pricing power and improves blended margins.

Low Switching Costs for Modern Consumers

Low switching costs in food, beverage and lifestyle mean consumers can move brands with near-zero financial or functional pain, so Auric Group must spend to keep them; Auric’s 2024 marketing spend rose ~18% year-on-year to ₹1.2 billion to fight churn.

Increased Price Sensitivity and Information Access

With 76% of UAE shoppers using price-comparison tools and 58% consulting digital reviews before buying (2024 Kantar), customers spot cheaper alternatives and wait for promos, forcing downward price pressure on premium wellness brands.

Auric Group counters this by emphasizing distinct product science, exclusive ingredients, and emotional storytelling; premium SKUs saw a 12% NPD uplift in 2024, showing value over price.

Influence of Digital Influencers and Community

Customers now follow niche influencers and social communities more than TV ads; 82% of Gen Z and 70% of millennials say influencer content guides purchases (Morning Consult, 2024), shifting power to organized online groups.

These communities can make or break reputation via viral trends and aggregated feedback, causing rapid demand swings and reputational risk.

Auric Group engages influencers and forums directly, converting members into advocates and cutting general market bargaining pressure; influencer-driven sales grew 18% for Auric in 2024.

- 82% Gen Z, 70% millennials follow influencer guidance

- Viral trends can flip demand in days

- Auric’s influencer-driven sales +18% in 2024

- Direct engagement lowers broad buyer leverage

Demand for Transparency and Ethical Sourcing

Modern consumers demand transparency on origins and ethics; 73% of global shoppers (2024 Deloitte survey) say they would switch brands for better social proof, raising churn risk for opaque labels.

If Auric Group fails to disclose sourcing across brands, customers can migrate to rivals offering traceability, pressuring margins and marketing spend to rebuild trust.

Auric must keep rigorous, audited standards across its portfolio to protect long-term brand equity and repeat sales; 58% of buyers pay a premium for certified products (2023 IRI data).

- 73% would switch for transparency (Deloitte 2024)

- 58% pay premium for certified goods (IRI 2023)

- Audit traceability across portfolio to reduce churn

Consumers wield pricing power: modern retail 60%, traceability premium fuels DTC gains

Customers hold strong price and transparency leverage: India’s top-5 grocery chains control ~60% modern retail, cutting gross margins 5–12 ppt; Auric’s DTC grew ~28% in FY2024, reclaiming margin. Low switching costs and influencer-led communities (82% Gen Z follow influencers) drive promo sensitivity; Auric’s influencer sales +18% in 2024. Traceability demand: 73% switch for transparency; 58% pay premiums for certified goods.

| Metric | Value (2024) |

|---|---|

| Top-5 grocery share (India) | ~60% |

| Auric DTC growth | ~28% |

| Influencer-driven sales | +18% |

| Gen Z influencer following | 82% |

| Switch for transparency | 73% |

| Pay premium for certified | 58% |

What You See Is What You Get

Auric Group Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Auric Group you'll receive immediately after purchase—no placeholders or samples, fully formatted and ready to download and use the moment you buy.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Auric Group faces moderate supplier power and rising buyer sophistication, while new entrants are deterred by capital and brand barriers, and substitutes pose niche threats—creating a dynamic competitive landscape that demands strategic clarity.

Suppliers Bargaining Power

Raw Material Commodity Fluctuations

Portfolio companies face margin pressure from swings in prices for coffee, spices and botanical extracts; coffee bean costs rose 28% year-over-year to Q3 2025, squeezing COGS.

Suppliers of rare organic extracts command premium pricing and stricter terms after 2024–25 supply shocks, raising procurement risk.

Auric must diversify vendors across Latin America, Africa and SE Asia; adding 3–5 alternative suppliers per key ingredient can cut price volatility exposure by ~15–20%.

Supplier Consolidation in Specialized Segments

In wellness and lifestyle, roughly 12 certified global suppliers control high-end organic ingredients, letting them set prices and stricter credit terms that squeeze smaller brands’ margins.

Auric Group offsets this by pooling demand across 18 subsidiaries, negotiating 15–25% better volume discounts and extending supplier credit from 30 to 60 days on average in 2025.

Impact of Sustainability and ESG Standards

Suppliers with ESG (environmental, social, governance) certifications command higher leverage as consumer demand for ethical brands rose 42% globally between 2019–2024, per McKinsey; Auric Group’s portfolio needs these certifications to protect brand integrity, so compliant vendors often charge 5–15% price premiums, keeping supplier power high.

Logistics and Packaging Provider Influence

Labor Market Constraints in Production

Suppliers of manufacturing and co-packing face rising labor costs—wages up ~6–8% in Southeast Asia in 2024—and skilled staff shortages, pushing service fees higher and extending lead times by 10–25% for new product launches.

Auric Group flags these trends to portfolio companies, adjusts contract terms, and diversifies co-packers to protect margins and time-to-market.

- Wage growth 6–8% (2024, regional average)

- Lead-time increases 10–25%

- Higher service fees passed to investors

Auric combats soaring input costs with pooled buying, long-term contracts & $5–10M CAPEX

Suppliers exert high bargaining power: coffee bean costs +28% YoY to Q3 2025 and eco-materials +18% in 2025, niche organic extract premiums 5–15%, wage inflation 6–8% (2024) and lead-times +10–25% raise COGS and launch risk; Auric offsets via pooled buying (18 subsidiaries) to secure 15–25% volume discounts and supplier credit extension to 60 days, and should sign 3–5 year contracts or invest $5–10m in packaging CAPEX.

| Metric | Value |

|---|---|

| Coffee cost change | +28% YoY to Q3 2025 |

| Eco-materials | +18% (2025) |

| Organic extract premium | 5–15% |

| Wage growth (SE Asia) | 6–8% (2024) |

| Lead-time impact | +10–25% |

| Volume discount (pooled) | 15–25% |

| Packaging CAPEX | $5–10m |

What is included in the product

Tailored Porter's Five Forces analysis for Auric Group, uncovering competitive drivers, supplier and buyer influence, entry barriers, substitutes, and emerging threats to its market position, with strategic insights for investors and executives.

A concise Porter's Five Forces snapshot tailored to Auric Group—instant clarity on competitive pressures for faster strategic choices.

Customers Bargaining Power

Retailer Dominance in Distribution Channels

Major supermarket chains and wellness retailers command shelf space and reach, forcing Auric Group brands to accept discounts, slotting fees and co-op marketing that can cut gross margins by 5–12 percentage points; India’s top 5 grocery chains control ~60% of modern retail, amplifying this leverage. Maintaining and scaling Direct-to-Consumer sales—Auric reported DTC growth of ~28% in FY2024—helps reclaim pricing power and improves blended margins.

Low Switching Costs for Modern Consumers

Low switching costs in food, beverage and lifestyle mean consumers can move brands with near-zero financial or functional pain, so Auric Group must spend to keep them; Auric’s 2024 marketing spend rose ~18% year-on-year to ₹1.2 billion to fight churn.

Increased Price Sensitivity and Information Access

With 76% of UAE shoppers using price-comparison tools and 58% consulting digital reviews before buying (2024 Kantar), customers spot cheaper alternatives and wait for promos, forcing downward price pressure on premium wellness brands.

Auric Group counters this by emphasizing distinct product science, exclusive ingredients, and emotional storytelling; premium SKUs saw a 12% NPD uplift in 2024, showing value over price.

Influence of Digital Influencers and Community

Customers now follow niche influencers and social communities more than TV ads; 82% of Gen Z and 70% of millennials say influencer content guides purchases (Morning Consult, 2024), shifting power to organized online groups.

These communities can make or break reputation via viral trends and aggregated feedback, causing rapid demand swings and reputational risk.

Auric Group engages influencers and forums directly, converting members into advocates and cutting general market bargaining pressure; influencer-driven sales grew 18% for Auric in 2024.

- 82% Gen Z, 70% millennials follow influencer guidance

- Viral trends can flip demand in days

- Auric’s influencer-driven sales +18% in 2024

- Direct engagement lowers broad buyer leverage

Demand for Transparency and Ethical Sourcing

Modern consumers demand transparency on origins and ethics; 73% of global shoppers (2024 Deloitte survey) say they would switch brands for better social proof, raising churn risk for opaque labels.

If Auric Group fails to disclose sourcing across brands, customers can migrate to rivals offering traceability, pressuring margins and marketing spend to rebuild trust.

Auric must keep rigorous, audited standards across its portfolio to protect long-term brand equity and repeat sales; 58% of buyers pay a premium for certified products (2023 IRI data).

- 73% would switch for transparency (Deloitte 2024)

- 58% pay premium for certified goods (IRI 2023)

- Audit traceability across portfolio to reduce churn

Consumers wield pricing power: modern retail 60%, traceability premium fuels DTC gains

Customers hold strong price and transparency leverage: India’s top-5 grocery chains control ~60% modern retail, cutting gross margins 5–12 ppt; Auric’s DTC grew ~28% in FY2024, reclaiming margin. Low switching costs and influencer-led communities (82% Gen Z follow influencers) drive promo sensitivity; Auric’s influencer sales +18% in 2024. Traceability demand: 73% switch for transparency; 58% pay premiums for certified goods.

| Metric | Value (2024) |

|---|---|

| Top-5 grocery share (India) | ~60% |

| Auric DTC growth | ~28% |

| Influencer-driven sales | +18% |

| Gen Z influencer following | 82% |

| Switch for transparency | 73% |

| Pay premium for certified | 58% |

What You See Is What You Get

Auric Group Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Auric Group you'll receive immediately after purchase—no placeholders or samples, fully formatted and ready to download and use the moment you buy.