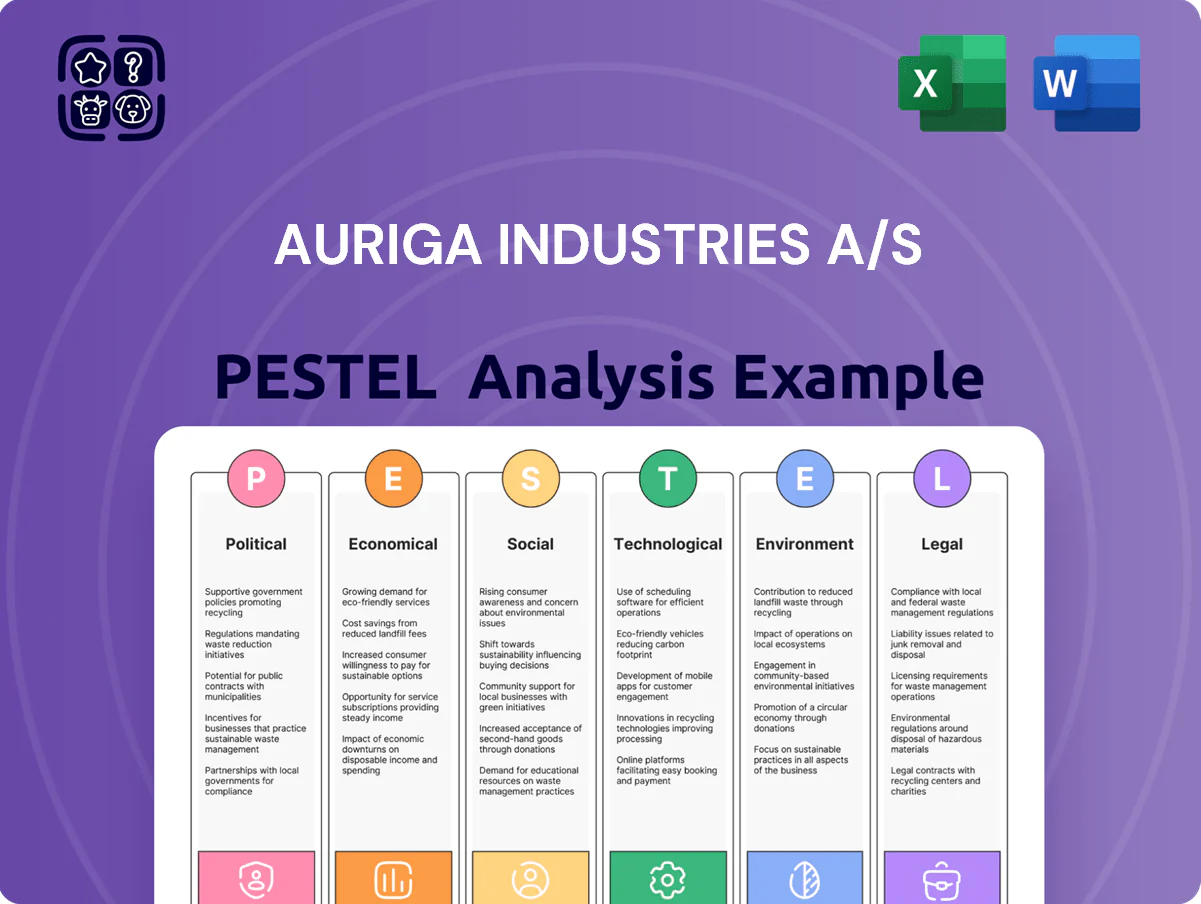

Auriga Industries A/S PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Gain a strategic advantage with our PESTLE Analysis of Auriga Industries A/S—uncover how political shifts, economic trends, social dynamics, technological change, legal developments, and environmental pressures are reshaping the company’s prospects; download the full version now for actionable insights, editable formats, and data-driven guidance to inform investments, strategy, and competitive positioning.

Political factors

Global Trade Protectionism

Global trade protectionism—seen in 2023–2025 with global tariff spikes (WTO reports showing average applied tariffs rising from 3.2% in 2020 to ~4.1% by 2024)—threatens Auriga Industries A/S’s export-heavy agricultural chemicals distribution, risking margin compression on crop protection lines that generated ~62% of group sales in 2024.

Agricultural Subsidy Reforms

Food Security Sovereignty

National governments are prioritizing food sovereignty, with 2024 FAO data showing 68% of low- and middle-income countries adopting state-backed local production programs; this boosts demand for inputs that raise yields. Auriga Industries A/S can target these markets—agrochemicals/seeds demand grew 5.6% CAGR 2020–24—positioning its subsidiaries as partners in national food security strategies to capture fiscal-backed procurement and subsidy flows.

Geopolitical Supply Chain Risks

Political instability in regions supplying phosphate and potash increases Auriga Industries A/S supply-chain risk; Russia and Belarus account for about 40% of global potash exports (2024), raising vulnerability to disruptions and price volatility.

Conflicts or sanctions can trigger sudden shortages and price spikes in chemical precursors—global fertilizer prices surged ~28% in 2022–23 during supply shocks—impacting margins and working capital.

Diversifying suppliers and holding strategic reserves (3–6 months of key inputs) are recommended mitigation steps to stabilize costs and ensure production continuity.

- 40% of potash from Russia/Belarus (2024)

- Fertilizer prices rose ~28% in 2022–23

- Maintain 3–6 months of strategic reserves

- Diversify supplier base across regions

Regulatory Harmonization Efforts

Monitoring negotiations (EU Farm to Fork, US trade talks) is vital: a 2025 EC impact study estimated harmonization could expand addressable market by 12–18% for approved crop solutions, guiding CAPEX and trial scheduling.

- Harmonization can simplify market access or increase compliance costs

- Approval times 9–24 months across major blocs affect launch timing

- 2024 WTO: 62% of SPS measures more trade-restrictive

- 2025 EC study: potential 12–18% addressable market growth

Policy shocks raise input costs, shift demand to low-toxicity products—12–18% market lift

Political risks: rising trade protectionism (average tariffs ~4.1% by 2024) and sanctions on potash exporters (Russia/Belarus ~40% of global supply) heighten input-cost volatility; EU CAP reallocation (~30% to eco-schemes 2023–27) shifts demand to low-toxicity products; harmonization could expand addressable market 12–18% but raises compliance costs; approval times 9–24 months impact launch timing.

| Metric | Value |

|---|---|

| Avg applied tariffs (2024) | ~4.1% |

| Potash share Russia/Belarus (2024) | ~40% |

| CAP eco-scheme reallocation | ~30% (2023–27) |

| Market expansion (EC 2025) | 12–18% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Auriga Industries A/S across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and region-specific implications to identify threats and opportunities for executives, investors, and strategists.

A concise, visually segmented PESTLE snapshot of Auriga Industries A/S that’s easily dropped into presentations or shared across teams to streamline strategic discussions and highlight external risks and market positioning.

Economic factors

Input Cost Volatility

Fluctuating energy and raw chemical prices compress manufacturing margins for crop protection products; EU industrial gas prices averaged €80–€120/MWh in 2024 versus €40–€60/MWh pre-2021, raising input costs materially. High natural gas spikes lift production costs for nitrogen-based nutrition—feedstock ammonia costs rose ~45% in 2024, squeezing margins. Auriga must deploy hedging and dynamic pricing; robust commodity hedges and pass-through clauses can mitigate volatility and protect profitability.

Interest Rate Environments

Central bank tightening in 2024–25 pushed policy rates to ~4.5% in the EU and 5.25% in the US, raising Auriga Industries A/S’s weighted average cost of capital for R&D and capex and increasing hurdle rates for new projects.

Higher rates elevate debt servicing costs for holding-company expansion: a €100m acquisition financed at 5% vs 2% adds ~€3m/year in interest expense.

The 2025 landscape requires disciplined leverage: target net-debt/EBITDA ≤2.0 and IRR thresholds increased by ~250–350bps versus pre-2022 norms when appraising investments.

Emerging Market Growth

Economic expansion in developing markets—IMF projects 2024 growth of 4.3% for emerging and developing economies—accelerates farm modernization, raising demand for advanced inputs and precision solutions that Auriga Industries A/S can supply.

Rising middle classes in Asia and Africa, forecasted to add ~1.3 billion people by 2030, shift diets toward higher-value crops, increasing need for intensive crop management and specialty agrochemicals.

By focusing on high-growth regions like Southeast Asia and Sub-Saharan Africa, where agricultural investment is growing over 6% CAGR in 2023–25, Auriga can capture significant market share and revenue upside.

Commodity Price Fluctuations

- Low commodity prices → reduced premium product spend

- High prices (eg 2024–25 rally) → higher adoption of inputs

- Price volatility raises demand for cost-effective solutions

Currency Exchange Risks

Auriga Industries A/S faces FX volatility between DKK, EUR and USD; 2025 saw EUR/DKK fluctuate within a 0.5% band while USD/DKK moved ~6% year-on-year, risking margin compression on exports and translating into weaker repatriated profits.

Rapid devaluations in markets like Turkey (lira down ~20% in 2024) can erode pricing competitiveness; hedging using forwards and options and shifting production locally reduces economic exposure.

- 2024–25 USD/DKK ~6% Y/Y swing

- EUR/DKK low volatility ~0.5% in 2025

- Hedging + local manufacturing mitigate profit erosion

Inflation, rates and FX squeeze margins—hedge, localise production, keep net-debt/EBITDA ≤2.0

Energy and feedstock cost inflation (EU gas €80–€120/MWh in 2024) and higher policy rates (~4.5% EU, 5.25% US) raise WACC and capex hurdles; commodity price swings (corn $4.50, wheat $6.50, soy $13.00 in 2025) and FX volatility (USD/DKK ~6% Y/Y in 2025) drive demand shifts and margin risk; hedging, local production and net-debt/EBITDA ≤2.0 mitigate exposure.

| Metric | 2024–25 |

|---|---|

| EU gas | €80–€120/MWh |

| Policy rates | EU 4.5% / US 5.25% |

| Commodities | Corn $4.50, Wheat $6.50, Soy $13.00 |

| FX USD/DKK | ~6% Y/Y |

| Leverage target | Net-debt/EBITDA ≤2.0 |

Preview Before You Purchase

Auriga Industries A/S PESTLE Analysis

The preview shown here is the exact Auriga Industries A/S PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or investor review.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Gain a strategic advantage with our PESTLE Analysis of Auriga Industries A/S—uncover how political shifts, economic trends, social dynamics, technological change, legal developments, and environmental pressures are reshaping the company’s prospects; download the full version now for actionable insights, editable formats, and data-driven guidance to inform investments, strategy, and competitive positioning.

Political factors

Global Trade Protectionism

Global trade protectionism—seen in 2023–2025 with global tariff spikes (WTO reports showing average applied tariffs rising from 3.2% in 2020 to ~4.1% by 2024)—threatens Auriga Industries A/S’s export-heavy agricultural chemicals distribution, risking margin compression on crop protection lines that generated ~62% of group sales in 2024.

Agricultural Subsidy Reforms

Food Security Sovereignty

National governments are prioritizing food sovereignty, with 2024 FAO data showing 68% of low- and middle-income countries adopting state-backed local production programs; this boosts demand for inputs that raise yields. Auriga Industries A/S can target these markets—agrochemicals/seeds demand grew 5.6% CAGR 2020–24—positioning its subsidiaries as partners in national food security strategies to capture fiscal-backed procurement and subsidy flows.

Geopolitical Supply Chain Risks

Political instability in regions supplying phosphate and potash increases Auriga Industries A/S supply-chain risk; Russia and Belarus account for about 40% of global potash exports (2024), raising vulnerability to disruptions and price volatility.

Conflicts or sanctions can trigger sudden shortages and price spikes in chemical precursors—global fertilizer prices surged ~28% in 2022–23 during supply shocks—impacting margins and working capital.

Diversifying suppliers and holding strategic reserves (3–6 months of key inputs) are recommended mitigation steps to stabilize costs and ensure production continuity.

- 40% of potash from Russia/Belarus (2024)

- Fertilizer prices rose ~28% in 2022–23

- Maintain 3–6 months of strategic reserves

- Diversify supplier base across regions

Regulatory Harmonization Efforts

Monitoring negotiations (EU Farm to Fork, US trade talks) is vital: a 2025 EC impact study estimated harmonization could expand addressable market by 12–18% for approved crop solutions, guiding CAPEX and trial scheduling.

- Harmonization can simplify market access or increase compliance costs

- Approval times 9–24 months across major blocs affect launch timing

- 2024 WTO: 62% of SPS measures more trade-restrictive

- 2025 EC study: potential 12–18% addressable market growth

Policy shocks raise input costs, shift demand to low-toxicity products—12–18% market lift

Political risks: rising trade protectionism (average tariffs ~4.1% by 2024) and sanctions on potash exporters (Russia/Belarus ~40% of global supply) heighten input-cost volatility; EU CAP reallocation (~30% to eco-schemes 2023–27) shifts demand to low-toxicity products; harmonization could expand addressable market 12–18% but raises compliance costs; approval times 9–24 months impact launch timing.

| Metric | Value |

|---|---|

| Avg applied tariffs (2024) | ~4.1% |

| Potash share Russia/Belarus (2024) | ~40% |

| CAP eco-scheme reallocation | ~30% (2023–27) |

| Market expansion (EC 2025) | 12–18% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Auriga Industries A/S across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and region-specific implications to identify threats and opportunities for executives, investors, and strategists.

A concise, visually segmented PESTLE snapshot of Auriga Industries A/S that’s easily dropped into presentations or shared across teams to streamline strategic discussions and highlight external risks and market positioning.

Economic factors

Input Cost Volatility

Fluctuating energy and raw chemical prices compress manufacturing margins for crop protection products; EU industrial gas prices averaged €80–€120/MWh in 2024 versus €40–€60/MWh pre-2021, raising input costs materially. High natural gas spikes lift production costs for nitrogen-based nutrition—feedstock ammonia costs rose ~45% in 2024, squeezing margins. Auriga must deploy hedging and dynamic pricing; robust commodity hedges and pass-through clauses can mitigate volatility and protect profitability.

Interest Rate Environments

Central bank tightening in 2024–25 pushed policy rates to ~4.5% in the EU and 5.25% in the US, raising Auriga Industries A/S’s weighted average cost of capital for R&D and capex and increasing hurdle rates for new projects.

Higher rates elevate debt servicing costs for holding-company expansion: a €100m acquisition financed at 5% vs 2% adds ~€3m/year in interest expense.

The 2025 landscape requires disciplined leverage: target net-debt/EBITDA ≤2.0 and IRR thresholds increased by ~250–350bps versus pre-2022 norms when appraising investments.

Emerging Market Growth

Economic expansion in developing markets—IMF projects 2024 growth of 4.3% for emerging and developing economies—accelerates farm modernization, raising demand for advanced inputs and precision solutions that Auriga Industries A/S can supply.

Rising middle classes in Asia and Africa, forecasted to add ~1.3 billion people by 2030, shift diets toward higher-value crops, increasing need for intensive crop management and specialty agrochemicals.

By focusing on high-growth regions like Southeast Asia and Sub-Saharan Africa, where agricultural investment is growing over 6% CAGR in 2023–25, Auriga can capture significant market share and revenue upside.

Commodity Price Fluctuations

- Low commodity prices → reduced premium product spend

- High prices (eg 2024–25 rally) → higher adoption of inputs

- Price volatility raises demand for cost-effective solutions

Currency Exchange Risks

Auriga Industries A/S faces FX volatility between DKK, EUR and USD; 2025 saw EUR/DKK fluctuate within a 0.5% band while USD/DKK moved ~6% year-on-year, risking margin compression on exports and translating into weaker repatriated profits.

Rapid devaluations in markets like Turkey (lira down ~20% in 2024) can erode pricing competitiveness; hedging using forwards and options and shifting production locally reduces economic exposure.

- 2024–25 USD/DKK ~6% Y/Y swing

- EUR/DKK low volatility ~0.5% in 2025

- Hedging + local manufacturing mitigate profit erosion

Inflation, rates and FX squeeze margins—hedge, localise production, keep net-debt/EBITDA ≤2.0

Energy and feedstock cost inflation (EU gas €80–€120/MWh in 2024) and higher policy rates (~4.5% EU, 5.25% US) raise WACC and capex hurdles; commodity price swings (corn $4.50, wheat $6.50, soy $13.00 in 2025) and FX volatility (USD/DKK ~6% Y/Y in 2025) drive demand shifts and margin risk; hedging, local production and net-debt/EBITDA ≤2.0 mitigate exposure.

| Metric | 2024–25 |

|---|---|

| EU gas | €80–€120/MWh |

| Policy rates | EU 4.5% / US 5.25% |

| Commodities | Corn $4.50, Wheat $6.50, Soy $13.00 |

| FX USD/DKK | ~6% Y/Y |

| Leverage target | Net-debt/EBITDA ≤2.0 |

Preview Before You Purchase

Auriga Industries A/S PESTLE Analysis

The preview shown here is the exact Auriga Industries A/S PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or investor review.