Aurobindo Pharma Boston Consulting Group Matrix

Visual. Strategic. Downloadable.

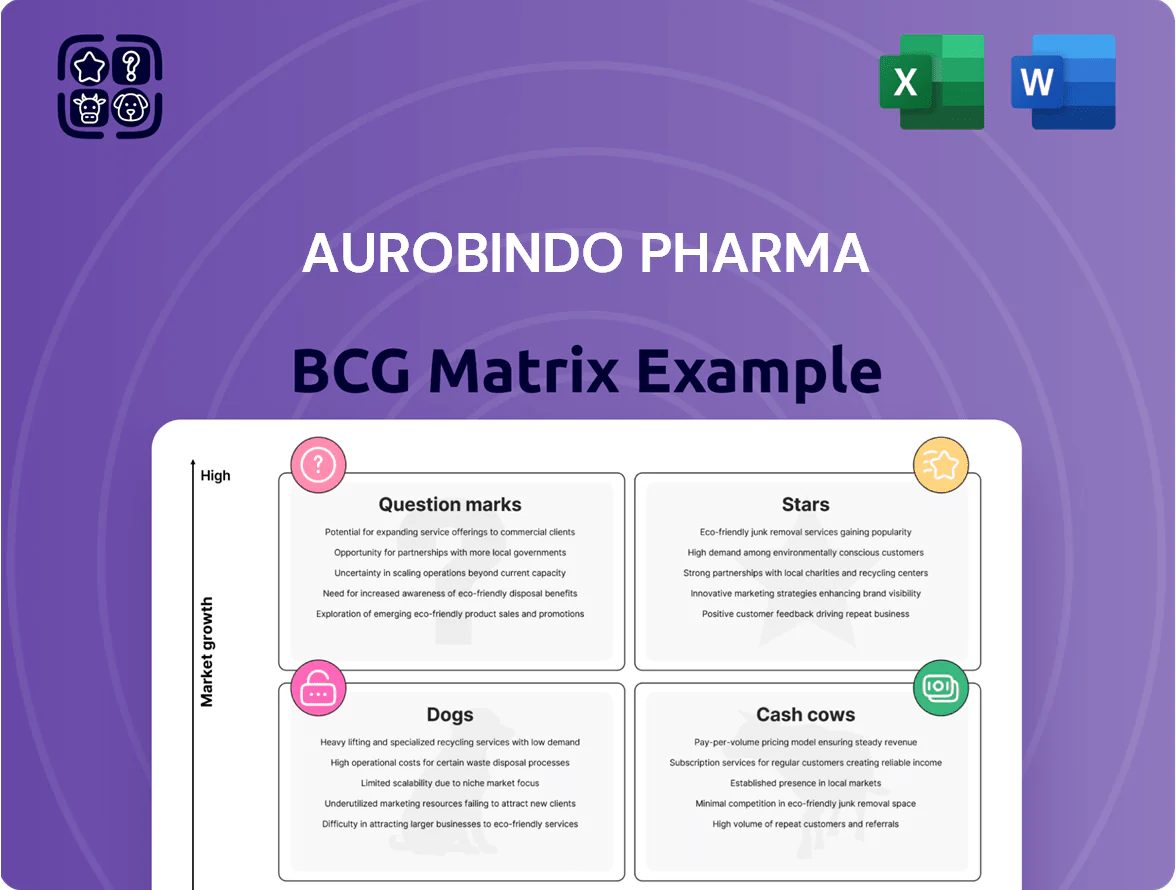

Aurobindo Pharma sits at an inflection point: high-growth generics and specialty injectables show Star potential, mature oral solids act as steady Cash Cows, while lower-margin legacy products risk being Dogs without reprioritization. This snapshot hints at resource shifts needed to fuel innovation and defend margin-heavy segments—yet the full picture matters. Purchase the complete BCG Matrix for quadrant-by-quadrant placements, data-backed recommendations, and ready-to-use Word and Excel deliverables to guide smarter allocation and strategic action.

Stars

Global Injectables Portfolio

Aurobindo’s Global Injectables are a BCG Stars unit after commissioning specialized plants in Vizag and elsewhere by late 2025, boosting sterile injectable capacity to an estimated 1.2 billion doses/year (company guidance 2025).

High barriers—complex compliance, capital intensity—and persistent US hospital shortages (2019–2024 median shortage rate ~15%) let Aurobindo grow market share, targeting a 10–12% US sterile injectables share by 2026.

With global hospital spending on injectables growing ~6–8% CAGR (2021–2025), this segment is a top revenue driver, expected to contribute 20–25% of consolidated injectable revenues in FY2026.

Biosimilars Division CuraTeQ

CuraTeQ, Aurobindo Pharma’s biosimilars arm, had multiple molecules in filing or commercial stages in regulated markets by end-2025, contributing to ~15–20% of group R&D spend and targeting >$300m peak sales per lead asset.

Given biologics market CAGR ~9% (2020–2025) and higher margin profiles, CuraTeQ sits in the BCG Stars quadrant; continued capex and OPEX support is vital for Aurobindo’s shift from generics to a specialized biopharma player.

Complex Generics and Peptides

Aurobindo’s Complex Generics, focused on respiratory and ophthalmic drugs, deliver gross margins ~28–32% vs ~18–22% for oral solids, and accounted for ~18% of FY2024 revenues (₹6,200 crore of ₹34,500 crore), marking rapid premiumization.

Peptide-based medicines reached critical mass with a pipeline of 12 peptides and two commercial launches in 2024, targeting metabolic disorders and contributing ~4% of revenues, giving a technical edge in a high-growth niche (~CAGR 9–11% through 2028).

European Market Expansion

By end-2025 Aurobindo Pharma had become a top-tier generics player in France, Germany and Portugal, with European revenues rising to about $950m, up ~28% vs 2022 on specialty conversions and price mix.

The shift to higher-margin specialty products lifted European gross margins from ~22% in 2021 to ~33% in 2025, turning the region into a high-growth engine after years of stagnation.

Europe still needs capital for marketing and distribution; Aurobindo increased regional opex by ~18% YoY in 2024–25 but captured double-digit market share gains in key ATC categories.

- 2025 Europe rev ≈ $950m; +28% since 2022

- Gross margin Europe: ~33% (2025) vs 22% (2021)

- Regional opex +18% YoY (2024–25)

- Double-digit share gains in key ATC classes

Specialty Oncology and Hormones

Specialty Oncology and Hormones: Aurobindo Pharma runs dedicated high-potency lines for oncology and hormonal APIs, a niche with complex manufacturing that limits competitors and supports high market penetration; global oncology drug spend reached about $190 billion in 2024, underpinning demand growth.

The unit requires cash for capacity expansion—Aurobindo reported capex of ~INR 1,200 crore in FY2024 partly for potent API lines—yet offers long-term leadership potential as cancer treatment volumes rise ~6–8% annually.

- Dedicated high-potent lines reduce competition

- Global oncology spend ~$190B (2024)

- FY2024 capex ~INR 1,200 crore for capacity

- Market growth ~6–8% CAGR for oncology volumes

Aurobindo surges: Injectables 1.2B doses, Europe $950M, CuraTeQ $300M+ peak

Aurobindo’s Stars: Global sterile injectables, biosimilars (CuraTeQ), complex generics, peptides and specialty oncology drive high growth and margins, backed by 2025 capacity (injectables ~1.2bn doses), Europe revenue ~$950m (2025), biosimales peak target >$300m, FY2024 capex ~INR1,200cr; continued capex/opex needed to retain market leadership.

| Unit | 2025/2024 | Key metric |

|---|---|---|

| Injectables | 2025 | 1.2bn doses |

| Europe | 2025 | $950m rev |

| CuraTeQ | 2025 | >$300m peak target |

| Capex | FY2024 | ~INR1,200cr |

What is included in the product

Comprehensive BCG Matrix of Aurobindo Pharma: identifies Stars, Cash Cows, Question Marks, and Dogs with strategic invest/hold/divest guidance and trend context.

One-page Aurobindo Pharma BCG Matrix placing products by market share and growth for quick strategic decisions.

Cash Cows

API Manufacturing and Vertical Integration

As of FY2024 Aurobindo Pharma produced APIs across 15+ plants, ranking among the top 5 global API makers and achieving ~₹6,200 crore (≈$750m) API revenue, giving a sizeable per-unit cost edge for its formulations.

This mature API unit shows low single-digit market growth but high market share in standard molecules, delivering steady operating cash flows and ~15–18% EBIT margins to fund R&D and expansion.

APIs supplied to 3rd-party firms accounted for roughly 30% of segment sales in 2024, making this the companys primary internal funding source for biosimilars and specialty drug investments.

US Oral Solids Portfolio

Aurobindo Pharma’s US oral solids portfolio dominates the mature US generic oral solids market with a catalog exceeding 500 ANDAs and ~12% market share in 2024, delivering steady revenue despite average price erosion of ~4% yearly.

High prescription volume — ~250 million scripts/year exposure — offsets low growth, keeping gross margins near 28% in FY2024 and generating free cash flow to service ~USD 650m net debt and fund R&D.

Antibiotics and Penicillins

Aurobindo Pharma is a global leader in semi-synthetic penicillins and essential antibiotics, supplying over 100 markets and recording antibiotic sales of about $650m in FY2024 (management disclosure).

The penicillin/antibiotic segment is mature with ~2–3% annual volume growth globally and high entry barriers from environmental controls and scale, limiting new competition.

Aurobindo leverages a fully integrated supply chain—captive API, fermentation and formulation—to sustain EBITDA margins near 18% in this low-growth area, milking steady cash flows for reinvestment.

Anti-Retroviral ARV Business

Aurobindo Pharma’s Anti-Retroviral (ARV) business is a cash cow: it supplies WHO, Global Fund, and national tenders for HIV/AIDS meds, leveraging scale to win price-driven contracts worldwide.

Growth has plateaued as WHO treatment protocols stabilized, but predictable demand and high volumes generated roughly $350–420M in ARV revenues in 2024, funding corporate overhead and R&D elsewhere.

Here’s the quick list:

- Global tender dominance—low margin, high volume

- Stable demand—standardized WHO protocols since 2020

- Estimated 2024 ARV revenue: $350–420M

- Funds corporate fixed costs and other pipeline bets

Cardiovascular and CNS Generics

Cardiovascular and CNS generics drive Aurobindo Pharma’s cash cow segment, supplying stable revenue from chronic therapies like antihypertensives and antiepileptics; FY2024 India and ROW generics sales contributed about $650m of the company’s $1.2bn consolidated revenue, with cardiovascular/CNS a large share.

These well‑established therapies keep high market share in retail and hospital channels, showing low churn and predictable demand, so marketing spend stays low and margins stay high; EBITDA on legacy generics ranges near 18–22% in recent quarters.

Low promotion needs let Aurobindo convert sales into free cash flow for R&D and biosimilars; capex and R&D were ~₹1,250cr in FY2024, funded largely by operating cash from these generics.

- Stable, chronic demand: high patient retention

- High market share in retail/institutional channels

- Low marketing spend → 18–22% EBITDA

- Drives free cash for R&D and M&A (₹1,250cr FY2024)

Aurobindo’s cash cows: APIs, US solids, ARVs & cardio/CNS fuel capex, R&D and debt

Aurobindo’s cash cows (FY2024): APIs (~₹6,200cr/$750M; 15+ plants; 15–18% EBIT), US oral solids (~500 ANDAs; ~12% US share; 28% gross), ARVs ($350–420M; global tenders), cardio/CNS generics (~$650M India/ROW; 18–22% EBITDA). These segments fund ₹1,250cr capex/R&D and service ~$650M net debt.

| Segment | 2024 rev | Margin |

|---|---|---|

| APIs | ₹6,200cr/$750M | 15–18% EBIT |

| US oral solids | — | 28% gross |

| ARV | $350–420M | low margin |

| Cardio/CNS | $650M | 18–22% EBITDA |

What You See Is What You Get

Aurobindo Pharma BCG Matrix

The Aurobindo Pharma BCG Matrix you're previewing is the final, fully formatted document you'll receive after purchase—no watermarks or demo content, just a professionally designed strategic analysis ready for immediate use. This preview mirrors the exact report delivered to your inbox, complete with market-backed positioning, growth-share visuals, and actionable insights for portfolio decisions. Once bought, the file is instantly downloadable, editable, and presentation-ready for stakeholders or clients.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Visual. Strategic. Downloadable.

Aurobindo Pharma sits at an inflection point: high-growth generics and specialty injectables show Star potential, mature oral solids act as steady Cash Cows, while lower-margin legacy products risk being Dogs without reprioritization. This snapshot hints at resource shifts needed to fuel innovation and defend margin-heavy segments—yet the full picture matters. Purchase the complete BCG Matrix for quadrant-by-quadrant placements, data-backed recommendations, and ready-to-use Word and Excel deliverables to guide smarter allocation and strategic action.

Stars

Global Injectables Portfolio

Aurobindo’s Global Injectables are a BCG Stars unit after commissioning specialized plants in Vizag and elsewhere by late 2025, boosting sterile injectable capacity to an estimated 1.2 billion doses/year (company guidance 2025).

High barriers—complex compliance, capital intensity—and persistent US hospital shortages (2019–2024 median shortage rate ~15%) let Aurobindo grow market share, targeting a 10–12% US sterile injectables share by 2026.

With global hospital spending on injectables growing ~6–8% CAGR (2021–2025), this segment is a top revenue driver, expected to contribute 20–25% of consolidated injectable revenues in FY2026.

Biosimilars Division CuraTeQ

CuraTeQ, Aurobindo Pharma’s biosimilars arm, had multiple molecules in filing or commercial stages in regulated markets by end-2025, contributing to ~15–20% of group R&D spend and targeting >$300m peak sales per lead asset.

Given biologics market CAGR ~9% (2020–2025) and higher margin profiles, CuraTeQ sits in the BCG Stars quadrant; continued capex and OPEX support is vital for Aurobindo’s shift from generics to a specialized biopharma player.

Complex Generics and Peptides

Aurobindo’s Complex Generics, focused on respiratory and ophthalmic drugs, deliver gross margins ~28–32% vs ~18–22% for oral solids, and accounted for ~18% of FY2024 revenues (₹6,200 crore of ₹34,500 crore), marking rapid premiumization.

Peptide-based medicines reached critical mass with a pipeline of 12 peptides and two commercial launches in 2024, targeting metabolic disorders and contributing ~4% of revenues, giving a technical edge in a high-growth niche (~CAGR 9–11% through 2028).

European Market Expansion

By end-2025 Aurobindo Pharma had become a top-tier generics player in France, Germany and Portugal, with European revenues rising to about $950m, up ~28% vs 2022 on specialty conversions and price mix.

The shift to higher-margin specialty products lifted European gross margins from ~22% in 2021 to ~33% in 2025, turning the region into a high-growth engine after years of stagnation.

Europe still needs capital for marketing and distribution; Aurobindo increased regional opex by ~18% YoY in 2024–25 but captured double-digit market share gains in key ATC categories.

- 2025 Europe rev ≈ $950m; +28% since 2022

- Gross margin Europe: ~33% (2025) vs 22% (2021)

- Regional opex +18% YoY (2024–25)

- Double-digit share gains in key ATC classes

Specialty Oncology and Hormones

Specialty Oncology and Hormones: Aurobindo Pharma runs dedicated high-potency lines for oncology and hormonal APIs, a niche with complex manufacturing that limits competitors and supports high market penetration; global oncology drug spend reached about $190 billion in 2024, underpinning demand growth.

The unit requires cash for capacity expansion—Aurobindo reported capex of ~INR 1,200 crore in FY2024 partly for potent API lines—yet offers long-term leadership potential as cancer treatment volumes rise ~6–8% annually.

- Dedicated high-potent lines reduce competition

- Global oncology spend ~$190B (2024)

- FY2024 capex ~INR 1,200 crore for capacity

- Market growth ~6–8% CAGR for oncology volumes

Aurobindo surges: Injectables 1.2B doses, Europe $950M, CuraTeQ $300M+ peak

Aurobindo’s Stars: Global sterile injectables, biosimilars (CuraTeQ), complex generics, peptides and specialty oncology drive high growth and margins, backed by 2025 capacity (injectables ~1.2bn doses), Europe revenue ~$950m (2025), biosimales peak target >$300m, FY2024 capex ~INR1,200cr; continued capex/opex needed to retain market leadership.

| Unit | 2025/2024 | Key metric |

|---|---|---|

| Injectables | 2025 | 1.2bn doses |

| Europe | 2025 | $950m rev |

| CuraTeQ | 2025 | >$300m peak target |

| Capex | FY2024 | ~INR1,200cr |

What is included in the product

Comprehensive BCG Matrix of Aurobindo Pharma: identifies Stars, Cash Cows, Question Marks, and Dogs with strategic invest/hold/divest guidance and trend context.

One-page Aurobindo Pharma BCG Matrix placing products by market share and growth for quick strategic decisions.

Cash Cows

API Manufacturing and Vertical Integration

As of FY2024 Aurobindo Pharma produced APIs across 15+ plants, ranking among the top 5 global API makers and achieving ~₹6,200 crore (≈$750m) API revenue, giving a sizeable per-unit cost edge for its formulations.

This mature API unit shows low single-digit market growth but high market share in standard molecules, delivering steady operating cash flows and ~15–18% EBIT margins to fund R&D and expansion.

APIs supplied to 3rd-party firms accounted for roughly 30% of segment sales in 2024, making this the companys primary internal funding source for biosimilars and specialty drug investments.

US Oral Solids Portfolio

Aurobindo Pharma’s US oral solids portfolio dominates the mature US generic oral solids market with a catalog exceeding 500 ANDAs and ~12% market share in 2024, delivering steady revenue despite average price erosion of ~4% yearly.

High prescription volume — ~250 million scripts/year exposure — offsets low growth, keeping gross margins near 28% in FY2024 and generating free cash flow to service ~USD 650m net debt and fund R&D.

Antibiotics and Penicillins

Aurobindo Pharma is a global leader in semi-synthetic penicillins and essential antibiotics, supplying over 100 markets and recording antibiotic sales of about $650m in FY2024 (management disclosure).

The penicillin/antibiotic segment is mature with ~2–3% annual volume growth globally and high entry barriers from environmental controls and scale, limiting new competition.

Aurobindo leverages a fully integrated supply chain—captive API, fermentation and formulation—to sustain EBITDA margins near 18% in this low-growth area, milking steady cash flows for reinvestment.

Anti-Retroviral ARV Business

Aurobindo Pharma’s Anti-Retroviral (ARV) business is a cash cow: it supplies WHO, Global Fund, and national tenders for HIV/AIDS meds, leveraging scale to win price-driven contracts worldwide.

Growth has plateaued as WHO treatment protocols stabilized, but predictable demand and high volumes generated roughly $350–420M in ARV revenues in 2024, funding corporate overhead and R&D elsewhere.

Here’s the quick list:

- Global tender dominance—low margin, high volume

- Stable demand—standardized WHO protocols since 2020

- Estimated 2024 ARV revenue: $350–420M

- Funds corporate fixed costs and other pipeline bets

Cardiovascular and CNS Generics

Cardiovascular and CNS generics drive Aurobindo Pharma’s cash cow segment, supplying stable revenue from chronic therapies like antihypertensives and antiepileptics; FY2024 India and ROW generics sales contributed about $650m of the company’s $1.2bn consolidated revenue, with cardiovascular/CNS a large share.

These well‑established therapies keep high market share in retail and hospital channels, showing low churn and predictable demand, so marketing spend stays low and margins stay high; EBITDA on legacy generics ranges near 18–22% in recent quarters.

Low promotion needs let Aurobindo convert sales into free cash flow for R&D and biosimilars; capex and R&D were ~₹1,250cr in FY2024, funded largely by operating cash from these generics.

- Stable, chronic demand: high patient retention

- High market share in retail/institutional channels

- Low marketing spend → 18–22% EBITDA

- Drives free cash for R&D and M&A (₹1,250cr FY2024)

Aurobindo’s cash cows: APIs, US solids, ARVs & cardio/CNS fuel capex, R&D and debt

Aurobindo’s cash cows (FY2024): APIs (~₹6,200cr/$750M; 15+ plants; 15–18% EBIT), US oral solids (~500 ANDAs; ~12% US share; 28% gross), ARVs ($350–420M; global tenders), cardio/CNS generics (~$650M India/ROW; 18–22% EBITDA). These segments fund ₹1,250cr capex/R&D and service ~$650M net debt.

| Segment | 2024 rev | Margin |

|---|---|---|

| APIs | ₹6,200cr/$750M | 15–18% EBIT |

| US oral solids | — | 28% gross |

| ARV | $350–420M | low margin |

| Cardio/CNS | $650M | 18–22% EBITDA |

What You See Is What You Get

Aurobindo Pharma BCG Matrix

The Aurobindo Pharma BCG Matrix you're previewing is the final, fully formatted document you'll receive after purchase—no watermarks or demo content, just a professionally designed strategic analysis ready for immediate use. This preview mirrors the exact report delivered to your inbox, complete with market-backed positioning, growth-share visuals, and actionable insights for portfolio decisions. Once bought, the file is instantly downloadable, editable, and presentation-ready for stakeholders or clients.