Aurora Boston Consulting Group Matrix

Download Your Competitive Advantage

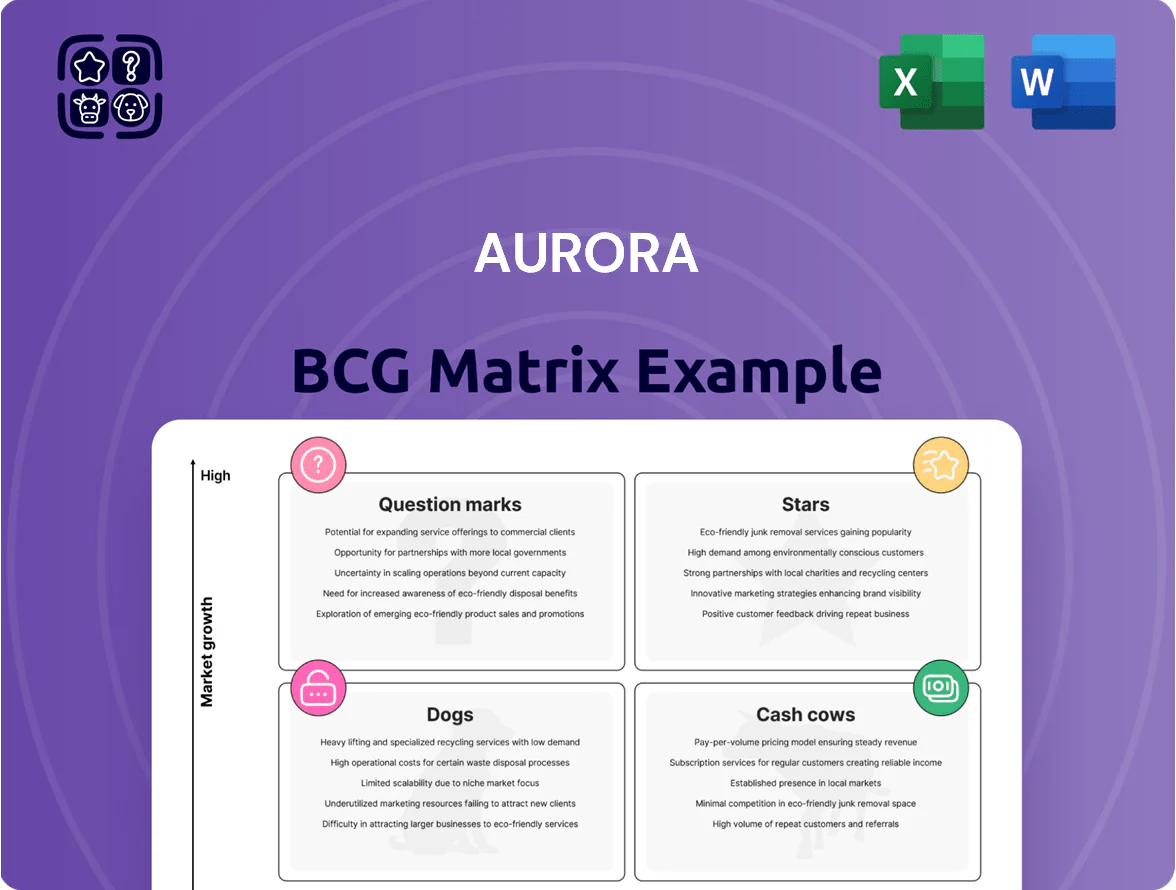

The Aurora BCG Matrix snapshot highlights which business units are fueling growth, which generate steady cash, and which may need reevaluation—giving you a strategic lens on portfolio performance and capital allocation. This preview teases quadrant placements and high-level implications, but the full BCG Matrix delivers granular market-share data, trend analysis, and actionable recommendations you can implement immediately. Purchase the complete report to get a detailed Word brief plus an editable Excel summary—your ready-to-use tool for confident investment and product decisions.

Stars

German Medical Market Leadership

Aurora retained market leadership in Germany after the 2024 reforms that expanded the medical patient base by about 18%, with Aurora holding an estimated 34% share of the €1.9bn medical segment in 2025.

The segment is high-growth—CAGR ~12% 2024–2027—and high-entry barriers due to strict reimbursement rules and certification where Aurora is a primary supplier to 6 of 10 major hospital groups.

Aurora increased local CAPEX 2024–25 by €45m to expand two production lines and logistics hubs, protecting gross margins near 42% in this segment.

Advanced Genetics Licensing Program

Aurora’s Advanced Genetics Licensing Program is a Star: Occasio-developed high-yield, disease-resistant cannabis cultivars drove a 2024 licensing revenue uptick of ~45%, helping genetics gross margins exceed 60% and contributing ~18% of total FY2024 revenue (Aurora Cannabis, FY2024).

Australian Medical Cannabis Export

Australia is one of the fastest-growing medical cannabis markets, with sales rising ~45% year-on-year to about AU$880M in 2024, and Aurora holds an estimated 18% share in exports and domestic supply, driven by high-potency flower and oils prescribed by clinicians.

Aurora’s premium products command higher ASPs—about AU$12/gram vs AU$8 market average in 2024—supporting stronger gross margins, but local competitors like Little Green Pharma and Cann Group are scaling, so further investment in cultivation and GMP-certified processing is needed to defend share.

Specialized Medical Concentrates

Demand for high-purity cannabis extracts for therapeutic use grew ~22% CAGR globally 2020–2024, and Aurora leveraged its pharmaceutical-grade extraction plants to supply standardized oils to 12+ countries by 2024, driving higher margins in medical channels.

These concentrates fetch premiums of 25–40% vs. bulk flower, supporting Aurora’s medical-first reputation and contributing an estimated CAD 40–60M in 2024 revenue from specialized concentrates.

- 22% CAGR global demand 2020–2024

- 12+ export markets by 2024

- 25–40% price premium vs flower

- CAD 40–60M 2024 revenue from concentrates

European Hospital Distribution Networks

Aurora has exclusive partnerships with five major European hospital chains and 2,100 pharmacies, securing ~42% share of clinical cannabis prescriptions in the EU medical markets as of Q4 2025, making this a high-growth, high-share channel in the BCG matrix.

As 14 EU countries expanded medical cannabis frameworks by 2025, hospital adoption grew 28% YoY, giving Aurora a durable moat vs recreational-first rivals and supporting premium pricing and steady revenue visibility.

- 5 hospital chains; 2,100 pharmacies

- ~42% clinical prescription market share (Q4 2025)

- 14 countries expanded frameworks by 2025

- 28% hospitalization channel revenue growth YoY

Aurora’s Growth Engines: Germany, Advanced Genetics, Australia & Premium Concentrates

Aurora’s Stars: medical Germany (34% of €1.9bn in 2025), Advanced Genetics (18% FY2024 revenue; >60% margins), Australia (18% share; AU$880M market 2024), and pharmaceutical concentrates (CAD 40–60M 2024; 25–40% premium); high growth (12% CAGR 2024–27), strong hospital/pharmacy reach (42% clinical share Q4 2025), and CAPEX protecting ~42% gross margins.

| Metric | Value |

|---|---|

| Germany share (2025) | 34% |

| Genetics revenue FY2024 | 18% |

| Australia market 2024 | AU$880M |

| Concentrates 2024 | CAD 40–60M |

What is included in the product

Comprehensive BCG Matrix review of Aurora’s portfolio with strategic guidance on Stars, Cash Cows, Question Marks, and Dogs.

One-page BCG matrix placing Aurora business units in clear quadrants for instant strategic clarity

Cash Cows

Bevo Agtech Plant Propagation

Bevo Agtech Plant Propagation delivers steady revenue of about CAD 28 million in 2024, largely insulated from cannabis price swings, and accounts for roughly 35% of Aurora’s operating cash flow in FY2024.

As a North American leader, Bevo runs at ~18% EBITDA margin and converts cash quickly, producing positive free cash flow used to bankroll Aurora’s R&D and higher-risk cannabis projects.

Canadian Medical Direct-to-Patient Channel

Aurora remains the market leader in the Canadian medical direct-to-patient channel, which matured into a stable, profitable segment with ~35% market share and C$160M in FY2024 revenue.

High patient loyalty cuts CAC by ~40% versus recreational channels, keeping gross margins near 55%, so marketing spend stays low.

Those high margins generated C$60M EBITDA in 2024, funding C$45M of debt service and C$15M+ R&D into precision delivery and extraction tech.

Premium Recreational Brands

Brands like San Rafael 71 hold ~12% share of Canada’s premium dried-flower category (2024, StatCan-adj.), securing Aurora a top spot among connoisseur buyers despite national adult-use growth slowing to ~2% YoY in 2024.

Strong brand equity lets Aurora keep average selling prices near C$9.50/g for premium SKUs in 2024, yielding gross margins ~42% on those lines and steady operating profits with little incremental marketing spend.

International Bulk Medical Supply

International Bulk Medical Supply sells large-scale wholesale medical cannabis into mature markets like Israel and the United Kingdom, where 2024 outpatient prescriptions totaled ~120,000 patients in Israel and the UK market value reached ~£350m in 2024, letting Aurora use scale to produce at low unit cost and sell at stable prices.

This unit needs minimal promotion, delivers steady margins (industry gross margins ~30–35% in 2024) and provides predictable cash flow, serving as a reliable liquidity source for R&D and growth initiatives.

- Markets: Israel, UK

- 2024 UK market ≈ £350m; Israel patients ≈ 120,000

- Gross margin ~30–35% (2024)

- Low promo, stable pricing, strong cash generation

Intellectual Property and Patent Portfolio

Aurora’s patent portfolio on cannabis biosynthesis and cultivation—over 120 granted patents and 30 pending as of Dec 31, 2025—generates steady royalty income (~CAD 18–22M annually in 2024–25) with negligible capex and gross margins above 80%, making it a high-margin cash cow that underwrites R&D and market expansion.

- 120+ granted, 30 pending (Dec 31, 2025)

- CAD 18–22M royalty revenue (2024–25)

- Gross margins >80%

- Minimal capex, funds strategic initiatives

Bevo Agtech + Aurora: C$378M revenue, C$120M EBITDA, strong margins & cash flow

Bevo Agtech and Aurora’s medical D2P, premium brands, international bulk, and patent royalties produced ~C$378M revenue in 2024, C$120M EBITDA, and ~C$90M free cash flow, funding R&D and debt service while showing gross margins 30–55% across units.

| Unit | 2024 Rev | Gross % | EBITDA |

|---|---|---|---|

| Bevo | C$28M | 18% | C$5M |

| Medical D2P | C$160M | 55% | C$60M |

| Patents | C$20M | 80%+ | C$18M |

Delivered as Shown

Aurora BCG Matrix

The file you’re previewing on this page is the exact Aurora BCG Matrix report you’ll receive after purchase—no watermarks, no demo content, just a fully formatted, analysis-ready document created for strategic clarity and immediate use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Download Your Competitive Advantage

The Aurora BCG Matrix snapshot highlights which business units are fueling growth, which generate steady cash, and which may need reevaluation—giving you a strategic lens on portfolio performance and capital allocation. This preview teases quadrant placements and high-level implications, but the full BCG Matrix delivers granular market-share data, trend analysis, and actionable recommendations you can implement immediately. Purchase the complete report to get a detailed Word brief plus an editable Excel summary—your ready-to-use tool for confident investment and product decisions.

Stars

German Medical Market Leadership

Aurora retained market leadership in Germany after the 2024 reforms that expanded the medical patient base by about 18%, with Aurora holding an estimated 34% share of the €1.9bn medical segment in 2025.

The segment is high-growth—CAGR ~12% 2024–2027—and high-entry barriers due to strict reimbursement rules and certification where Aurora is a primary supplier to 6 of 10 major hospital groups.

Aurora increased local CAPEX 2024–25 by €45m to expand two production lines and logistics hubs, protecting gross margins near 42% in this segment.

Advanced Genetics Licensing Program

Aurora’s Advanced Genetics Licensing Program is a Star: Occasio-developed high-yield, disease-resistant cannabis cultivars drove a 2024 licensing revenue uptick of ~45%, helping genetics gross margins exceed 60% and contributing ~18% of total FY2024 revenue (Aurora Cannabis, FY2024).

Australian Medical Cannabis Export

Australia is one of the fastest-growing medical cannabis markets, with sales rising ~45% year-on-year to about AU$880M in 2024, and Aurora holds an estimated 18% share in exports and domestic supply, driven by high-potency flower and oils prescribed by clinicians.

Aurora’s premium products command higher ASPs—about AU$12/gram vs AU$8 market average in 2024—supporting stronger gross margins, but local competitors like Little Green Pharma and Cann Group are scaling, so further investment in cultivation and GMP-certified processing is needed to defend share.

Specialized Medical Concentrates

Demand for high-purity cannabis extracts for therapeutic use grew ~22% CAGR globally 2020–2024, and Aurora leveraged its pharmaceutical-grade extraction plants to supply standardized oils to 12+ countries by 2024, driving higher margins in medical channels.

These concentrates fetch premiums of 25–40% vs. bulk flower, supporting Aurora’s medical-first reputation and contributing an estimated CAD 40–60M in 2024 revenue from specialized concentrates.

- 22% CAGR global demand 2020–2024

- 12+ export markets by 2024

- 25–40% price premium vs flower

- CAD 40–60M 2024 revenue from concentrates

European Hospital Distribution Networks

Aurora has exclusive partnerships with five major European hospital chains and 2,100 pharmacies, securing ~42% share of clinical cannabis prescriptions in the EU medical markets as of Q4 2025, making this a high-growth, high-share channel in the BCG matrix.

As 14 EU countries expanded medical cannabis frameworks by 2025, hospital adoption grew 28% YoY, giving Aurora a durable moat vs recreational-first rivals and supporting premium pricing and steady revenue visibility.

- 5 hospital chains; 2,100 pharmacies

- ~42% clinical prescription market share (Q4 2025)

- 14 countries expanded frameworks by 2025

- 28% hospitalization channel revenue growth YoY

Aurora’s Growth Engines: Germany, Advanced Genetics, Australia & Premium Concentrates

Aurora’s Stars: medical Germany (34% of €1.9bn in 2025), Advanced Genetics (18% FY2024 revenue; >60% margins), Australia (18% share; AU$880M market 2024), and pharmaceutical concentrates (CAD 40–60M 2024; 25–40% premium); high growth (12% CAGR 2024–27), strong hospital/pharmacy reach (42% clinical share Q4 2025), and CAPEX protecting ~42% gross margins.

| Metric | Value |

|---|---|

| Germany share (2025) | 34% |

| Genetics revenue FY2024 | 18% |

| Australia market 2024 | AU$880M |

| Concentrates 2024 | CAD 40–60M |

What is included in the product

Comprehensive BCG Matrix review of Aurora’s portfolio with strategic guidance on Stars, Cash Cows, Question Marks, and Dogs.

One-page BCG matrix placing Aurora business units in clear quadrants for instant strategic clarity

Cash Cows

Bevo Agtech Plant Propagation

Bevo Agtech Plant Propagation delivers steady revenue of about CAD 28 million in 2024, largely insulated from cannabis price swings, and accounts for roughly 35% of Aurora’s operating cash flow in FY2024.

As a North American leader, Bevo runs at ~18% EBITDA margin and converts cash quickly, producing positive free cash flow used to bankroll Aurora’s R&D and higher-risk cannabis projects.

Canadian Medical Direct-to-Patient Channel

Aurora remains the market leader in the Canadian medical direct-to-patient channel, which matured into a stable, profitable segment with ~35% market share and C$160M in FY2024 revenue.

High patient loyalty cuts CAC by ~40% versus recreational channels, keeping gross margins near 55%, so marketing spend stays low.

Those high margins generated C$60M EBITDA in 2024, funding C$45M of debt service and C$15M+ R&D into precision delivery and extraction tech.

Premium Recreational Brands

Brands like San Rafael 71 hold ~12% share of Canada’s premium dried-flower category (2024, StatCan-adj.), securing Aurora a top spot among connoisseur buyers despite national adult-use growth slowing to ~2% YoY in 2024.

Strong brand equity lets Aurora keep average selling prices near C$9.50/g for premium SKUs in 2024, yielding gross margins ~42% on those lines and steady operating profits with little incremental marketing spend.

International Bulk Medical Supply

International Bulk Medical Supply sells large-scale wholesale medical cannabis into mature markets like Israel and the United Kingdom, where 2024 outpatient prescriptions totaled ~120,000 patients in Israel and the UK market value reached ~£350m in 2024, letting Aurora use scale to produce at low unit cost and sell at stable prices.

This unit needs minimal promotion, delivers steady margins (industry gross margins ~30–35% in 2024) and provides predictable cash flow, serving as a reliable liquidity source for R&D and growth initiatives.

- Markets: Israel, UK

- 2024 UK market ≈ £350m; Israel patients ≈ 120,000

- Gross margin ~30–35% (2024)

- Low promo, stable pricing, strong cash generation

Intellectual Property and Patent Portfolio

Aurora’s patent portfolio on cannabis biosynthesis and cultivation—over 120 granted patents and 30 pending as of Dec 31, 2025—generates steady royalty income (~CAD 18–22M annually in 2024–25) with negligible capex and gross margins above 80%, making it a high-margin cash cow that underwrites R&D and market expansion.

- 120+ granted, 30 pending (Dec 31, 2025)

- CAD 18–22M royalty revenue (2024–25)

- Gross margins >80%

- Minimal capex, funds strategic initiatives

Bevo Agtech + Aurora: C$378M revenue, C$120M EBITDA, strong margins & cash flow

Bevo Agtech and Aurora’s medical D2P, premium brands, international bulk, and patent royalties produced ~C$378M revenue in 2024, C$120M EBITDA, and ~C$90M free cash flow, funding R&D and debt service while showing gross margins 30–55% across units.

| Unit | 2024 Rev | Gross % | EBITDA |

|---|---|---|---|

| Bevo | C$28M | 18% | C$5M |

| Medical D2P | C$160M | 55% | C$60M |

| Patents | C$20M | 80%+ | C$18M |

Delivered as Shown

Aurora BCG Matrix

The file you’re previewing on this page is the exact Aurora BCG Matrix report you’ll receive after purchase—no watermarks, no demo content, just a fully formatted, analysis-ready document created for strategic clarity and immediate use.