Aurora Porter's Five Forces Analysis

Don't Miss the Bigger Picture

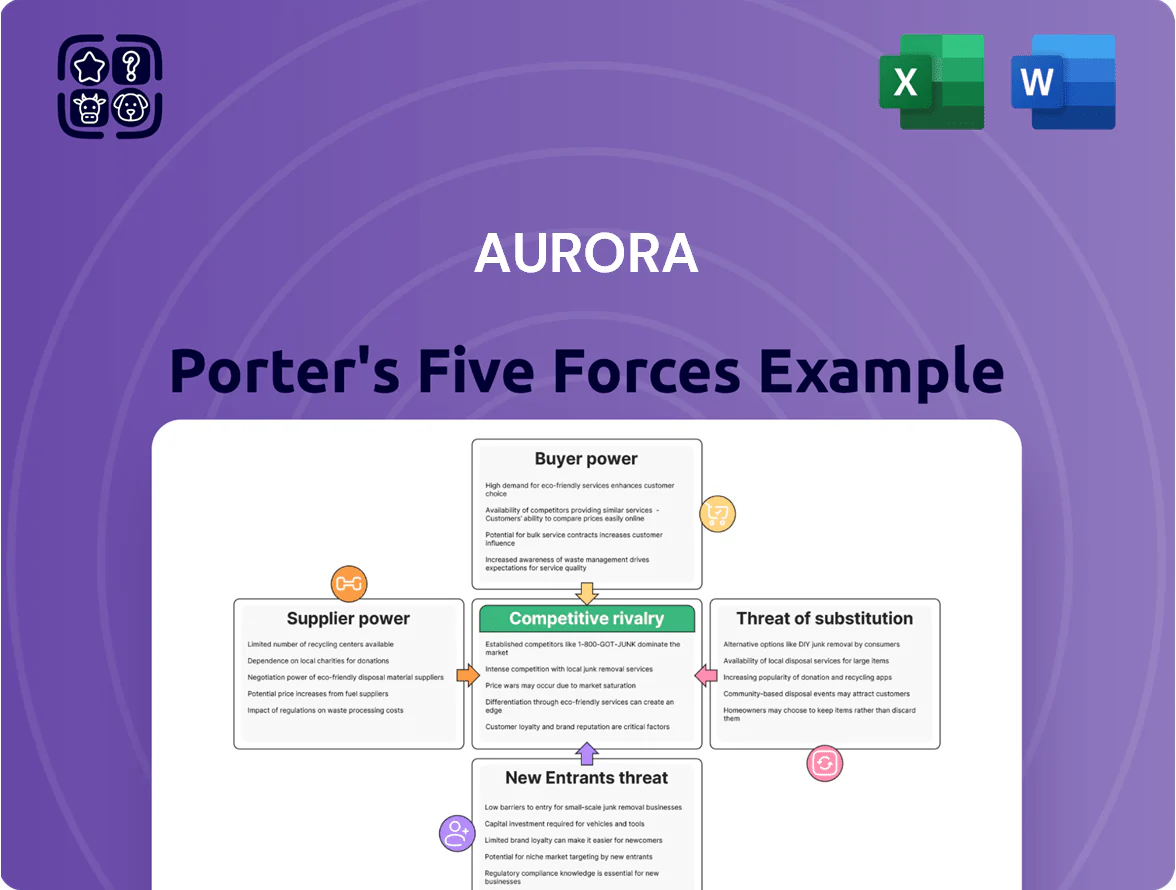

Aurora’s Porter's Five Forces snapshot highlights competitive intensity, supplier and buyer leverage, substitute threats, and entry barriers shaping its market position.

This preview teases force-by-force ratings and strategic implications; the full Porter's Five Forces Analysis delivers detailed data, visuals, and actionable recommendations tailored to Aurora.

Unlock the complete report to translate these insights into investment decisions, competitive strategies, or investor-ready presentations.

Suppliers Bargaining Power

Specialized Cultivation Technology Providers

Aurora depends on advanced lighting, irrigation, and climate-control systems to sustain yields of ~650–900 g/m2 per annum in its high-tech facilities; vendors for these systems therefore hold moderate supplier power because their equipment directly affects product quality and OPEX. Multiple global suppliers exist, yet replacing integrated systems in a 100,000 sq ft facility typically costs $3–8 million and requires 6–12 months downtime, raising switching barriers. Aurora’s 2024 capex of CAD 120–160 million for facility upgrades shows exposure to vendor pricing and lead times.

Energy and Utility Corporations

Energy use drives cannabis cultivation—indoor grows consume 2,500–5,000 kWh per kg of flower; electricity is a non-differentiable, market-priced input, so utility providers wield high bargaining power and Aurora cannot meaningfully hedge rates; in 2024 Aurora Cannabis reported energy and facility costs representing roughly 8–12% of COGS, making volatile wholesale electricity prices and regulated rates a fixed margin risk.

Genetics and Seed Breeders

Access to unique, high-potency cannabis genetics is critical for Aurora to stand out in medical and recreational markets; elite breeders now command royalties or upfront fees, with reported licensing deals averaging 5–12% royalties or CAD 0.5–2.0 per gram in 2024 industry reports. As IP protection tightens, genetics suppliers gain leverage—Aurora faces margin pressure if it must pay premiums or buy proprietary clones outright.

Regulatory Compliance and Testing Labs

Third-party labs must test Aurora’s products for safety, potency, and contaminants before sale; in 2024, 62% of US cannabis recalls cited lab-testing failures, showing labs’ gatekeeper role.

Certified facilities are few in key states—e.g., California had 120 licensed labs in 2024—so capacity limits give suppliers leverage over timing and price.

Any testing bottleneck or a 10–20% fee hike raises Aurora’s COGS and delays launches, cutting quarterly revenue and speed-to-market.

- Mandatory testing creates supplier power

- Limited certified labs: capacity risk

- 2024: 62% recalls linked to lab failures

- 10–20% cost rise → higher COGS, launch delays

Packaging and Raw Material Vendors

Suppliers of child-resistant packaging face strict US and EU regulations, shrinking the vendor pool and giving these suppliers modest leverage despite commoditized inputs; industry reports show ~60% of compliant packaging capacity concentrated in five firms as of 2025.

Aurora offsets risk by diversifying vendors, keeping single-supplier exposure under 20% per SKU and negotiating multi-year contracts to cap price volatility tied to compliance costs.

- ~60% compliant capacity held by five firms (2025)

- Single-supplier exposure kept <20% per SKU

- Raw materials commoditized, lower leverage

- Multi-year contracts reduce price swings

Supplier Risks: High-Cost Downtime, Energy & Royalties Concentration

Suppliers hold mixed power: critical systems (replacement cost CAD 3–8M, 6–12 months downtime) and utilities (2,500–5,000 kWh/kg; 8–12% of COGS in 2024) are high leverage, genetics demand 5–12% royalties (2024) and labs concentrate risk (California 120 labs in 2024; 62% recalls linked to lab failures), while packaging ~60% capacity rests with five firms (2025); Aurora keeps single-supplier exposure <20% per SKU.

| Metric | 2024–25 |

|---|---|

| Facility replacement cost | CAD 3–8M |

| Downtime | 6–12 months |

| Energy use | 2,500–5,000 kWh/kg |

| Energy % of COGS | 8–12% |

| Genetics royalties | 5–12% |

| CA labs (2024) | 120 |

| Recalls linked to labs | 62% |

| Packaging capacity top5 (2025) | ~60% |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Aurora, evaluating supplier and buyer power, substitute threats, rivalry intensity, and barriers that protect or expose its market position.

A concise Aurora Porter's Five Forces one-sheet that highlights competitive pressures and relief strategies—ideal for rapid decision-making and slide-ready presentations.

Customers Bargaining Power

Provincial Wholesale Distribution Boards

In Canada’s recreational market provincial wholesale distribution boards (e.g., Ontario Cannabis Store, Alberta Gaming, Liquor and Cannabis Commission) hold immense bargaining power, controlling ~70–90% of retail supply channels and dictating price, shelf placement, and product listings.

Aurora acts largely as a price-taker to these bodies, facing mandated margins and frequent requisitions for discounts or returns that compress wholesale ASPs; in 2024 Aurora reported retail channel ASPs ~20% below direct-store prices.

These boards can demand volume rebates and delist products, meaning losing shelf space can cut provincial sales by a majority share quickly; Aurora’s provincial channel revenue concentration was ~55% of Canadian revenue in FY2024.

Medical Patient Price Sensitivity

Medical cannabis patients show high price sensitivity and readily switch licensed producers; in Canada a 2024 Health Canada survey found 42% of medical users chose suppliers mainly for lower prices, so Aurora faces churn risk if prices lag market.

Entry of new producers raised SKU variety 28% in 2023–24 and pushed average medical flower price down ~12% to CA$6.50/g in 2024, increasing patient choice.

Aurora must sustain service levels and consistent quality—repeat-patient share falls sharply if on-time delivery or potency consistency drops; in 2024 industry retention averaged 60%, so small declines cost material revenue.

Retail Consumer Brand Loyalty

Adult-use consumers are more savvy and choose from 1,000+ SKUs in Canada’s legal market; brand loyalty rising—Aurora reports repeat-purchase rates near 42% in 2024—but many buyers still pick higher THC or lower price, with 61% citing potency/price as top factors in a 2023 survey; Aurora must therefore innovate product formats and keep gross margins tight, often pricing within 5–10% of category lows to retain share.

International Health Systems and Insurers

In markets like Germany, large government health insurers and pharmacy chains negotiate bulk medical cannabis prices, often pushing discounts of 15–40% for reimbursement inclusion; Aurora must concede margins to win these contracts.

Securing reimbursement access is vital: Germany accounted for €261m in medical cannabis imports in 2024, so exclusion limits Aurora’s international revenue growth despite margin pressure.

- Payors: government insurers + pharmacy chains

- Discounts: typically 15–40% for reimbursement

- 2024 Germany market: €261m imports

- Impact: necessary contracts but lower margins

Transparency and Information Access

The digital cannabis market lets customers compare prices, reviews, and lab results instantly, raising transparency and shifting power to buyers.

Both retail and medical buyers use data—88% of Canadian cannabis shoppers research products online (2024), and 62% cite lab reports as purchase drivers—forcing Aurora to justify price and quality vs cheaper rivals.

Result: persistent margin pressure and higher marketing spend to prove value.

- 88% of Canadian shoppers research online (2024)

- 62% use lab reports to decide

- Price comparisons compress margins

- Aurora must show measurable quality to compete

Provincial Channels Squeeze Aurora: Lower ASPs, Rising Marketing & Margin Pressure

Provincial wholesale boards control ~70–90% of retail supply, forcing Aurora to be price-taker; provincial channels were ~55% of Canadian revenue in FY2024, and retail ASPs ran ~20% below D2C in 2024. Germany reimbursement discounts 15–40%; 2024 German imports €261m. Digital shoppers: 88% research online; 62% use lab reports. Result: sustained margin pressure and higher marketing spend.

| Metric | Value (2024) |

|---|---|

| Provincial channel share | ~55% |

| Provincial control | 70–90% |

| Retail vs D2C ASP | ~20% lower |

| Germany imports | €261m |

| German discounts | 15–40% |

| Online research | 88% |

| Lab report use | 62% |

Preview the Actual Deliverable

Aurora Porter's Five Forces Analysis

This preview shows the exact Aurora Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups, fully formatted and ready for use.

You're viewing the final deliverable: a complete, professionally written competitive assessment that will be available for instant download once you complete your purchase.

No surprises—what you see here is the same document you'll get, prepared for immediate application in strategy, valuation, or competitive planning.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Aurora’s Porter's Five Forces snapshot highlights competitive intensity, supplier and buyer leverage, substitute threats, and entry barriers shaping its market position.

This preview teases force-by-force ratings and strategic implications; the full Porter's Five Forces Analysis delivers detailed data, visuals, and actionable recommendations tailored to Aurora.

Unlock the complete report to translate these insights into investment decisions, competitive strategies, or investor-ready presentations.

Suppliers Bargaining Power

Specialized Cultivation Technology Providers

Aurora depends on advanced lighting, irrigation, and climate-control systems to sustain yields of ~650–900 g/m2 per annum in its high-tech facilities; vendors for these systems therefore hold moderate supplier power because their equipment directly affects product quality and OPEX. Multiple global suppliers exist, yet replacing integrated systems in a 100,000 sq ft facility typically costs $3–8 million and requires 6–12 months downtime, raising switching barriers. Aurora’s 2024 capex of CAD 120–160 million for facility upgrades shows exposure to vendor pricing and lead times.

Energy and Utility Corporations

Energy use drives cannabis cultivation—indoor grows consume 2,500–5,000 kWh per kg of flower; electricity is a non-differentiable, market-priced input, so utility providers wield high bargaining power and Aurora cannot meaningfully hedge rates; in 2024 Aurora Cannabis reported energy and facility costs representing roughly 8–12% of COGS, making volatile wholesale electricity prices and regulated rates a fixed margin risk.

Genetics and Seed Breeders

Access to unique, high-potency cannabis genetics is critical for Aurora to stand out in medical and recreational markets; elite breeders now command royalties or upfront fees, with reported licensing deals averaging 5–12% royalties or CAD 0.5–2.0 per gram in 2024 industry reports. As IP protection tightens, genetics suppliers gain leverage—Aurora faces margin pressure if it must pay premiums or buy proprietary clones outright.

Regulatory Compliance and Testing Labs

Third-party labs must test Aurora’s products for safety, potency, and contaminants before sale; in 2024, 62% of US cannabis recalls cited lab-testing failures, showing labs’ gatekeeper role.

Certified facilities are few in key states—e.g., California had 120 licensed labs in 2024—so capacity limits give suppliers leverage over timing and price.

Any testing bottleneck or a 10–20% fee hike raises Aurora’s COGS and delays launches, cutting quarterly revenue and speed-to-market.

- Mandatory testing creates supplier power

- Limited certified labs: capacity risk

- 2024: 62% recalls linked to lab failures

- 10–20% cost rise → higher COGS, launch delays

Packaging and Raw Material Vendors

Suppliers of child-resistant packaging face strict US and EU regulations, shrinking the vendor pool and giving these suppliers modest leverage despite commoditized inputs; industry reports show ~60% of compliant packaging capacity concentrated in five firms as of 2025.

Aurora offsets risk by diversifying vendors, keeping single-supplier exposure under 20% per SKU and negotiating multi-year contracts to cap price volatility tied to compliance costs.

- ~60% compliant capacity held by five firms (2025)

- Single-supplier exposure kept <20% per SKU

- Raw materials commoditized, lower leverage

- Multi-year contracts reduce price swings

Supplier Risks: High-Cost Downtime, Energy & Royalties Concentration

Suppliers hold mixed power: critical systems (replacement cost CAD 3–8M, 6–12 months downtime) and utilities (2,500–5,000 kWh/kg; 8–12% of COGS in 2024) are high leverage, genetics demand 5–12% royalties (2024) and labs concentrate risk (California 120 labs in 2024; 62% recalls linked to lab failures), while packaging ~60% capacity rests with five firms (2025); Aurora keeps single-supplier exposure <20% per SKU.

| Metric | 2024–25 |

|---|---|

| Facility replacement cost | CAD 3–8M |

| Downtime | 6–12 months |

| Energy use | 2,500–5,000 kWh/kg |

| Energy % of COGS | 8–12% |

| Genetics royalties | 5–12% |

| CA labs (2024) | 120 |

| Recalls linked to labs | 62% |

| Packaging capacity top5 (2025) | ~60% |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Aurora, evaluating supplier and buyer power, substitute threats, rivalry intensity, and barriers that protect or expose its market position.

A concise Aurora Porter's Five Forces one-sheet that highlights competitive pressures and relief strategies—ideal for rapid decision-making and slide-ready presentations.

Customers Bargaining Power

Provincial Wholesale Distribution Boards

In Canada’s recreational market provincial wholesale distribution boards (e.g., Ontario Cannabis Store, Alberta Gaming, Liquor and Cannabis Commission) hold immense bargaining power, controlling ~70–90% of retail supply channels and dictating price, shelf placement, and product listings.

Aurora acts largely as a price-taker to these bodies, facing mandated margins and frequent requisitions for discounts or returns that compress wholesale ASPs; in 2024 Aurora reported retail channel ASPs ~20% below direct-store prices.

These boards can demand volume rebates and delist products, meaning losing shelf space can cut provincial sales by a majority share quickly; Aurora’s provincial channel revenue concentration was ~55% of Canadian revenue in FY2024.

Medical Patient Price Sensitivity

Medical cannabis patients show high price sensitivity and readily switch licensed producers; in Canada a 2024 Health Canada survey found 42% of medical users chose suppliers mainly for lower prices, so Aurora faces churn risk if prices lag market.

Entry of new producers raised SKU variety 28% in 2023–24 and pushed average medical flower price down ~12% to CA$6.50/g in 2024, increasing patient choice.

Aurora must sustain service levels and consistent quality—repeat-patient share falls sharply if on-time delivery or potency consistency drops; in 2024 industry retention averaged 60%, so small declines cost material revenue.

Retail Consumer Brand Loyalty

Adult-use consumers are more savvy and choose from 1,000+ SKUs in Canada’s legal market; brand loyalty rising—Aurora reports repeat-purchase rates near 42% in 2024—but many buyers still pick higher THC or lower price, with 61% citing potency/price as top factors in a 2023 survey; Aurora must therefore innovate product formats and keep gross margins tight, often pricing within 5–10% of category lows to retain share.

International Health Systems and Insurers

In markets like Germany, large government health insurers and pharmacy chains negotiate bulk medical cannabis prices, often pushing discounts of 15–40% for reimbursement inclusion; Aurora must concede margins to win these contracts.

Securing reimbursement access is vital: Germany accounted for €261m in medical cannabis imports in 2024, so exclusion limits Aurora’s international revenue growth despite margin pressure.

- Payors: government insurers + pharmacy chains

- Discounts: typically 15–40% for reimbursement

- 2024 Germany market: €261m imports

- Impact: necessary contracts but lower margins

Transparency and Information Access

The digital cannabis market lets customers compare prices, reviews, and lab results instantly, raising transparency and shifting power to buyers.

Both retail and medical buyers use data—88% of Canadian cannabis shoppers research products online (2024), and 62% cite lab reports as purchase drivers—forcing Aurora to justify price and quality vs cheaper rivals.

Result: persistent margin pressure and higher marketing spend to prove value.

- 88% of Canadian shoppers research online (2024)

- 62% use lab reports to decide

- Price comparisons compress margins

- Aurora must show measurable quality to compete

Provincial Channels Squeeze Aurora: Lower ASPs, Rising Marketing & Margin Pressure

Provincial wholesale boards control ~70–90% of retail supply, forcing Aurora to be price-taker; provincial channels were ~55% of Canadian revenue in FY2024, and retail ASPs ran ~20% below D2C in 2024. Germany reimbursement discounts 15–40%; 2024 German imports €261m. Digital shoppers: 88% research online; 62% use lab reports. Result: sustained margin pressure and higher marketing spend.

| Metric | Value (2024) |

|---|---|

| Provincial channel share | ~55% |

| Provincial control | 70–90% |

| Retail vs D2C ASP | ~20% lower |

| Germany imports | €261m |

| German discounts | 15–40% |

| Online research | 88% |

| Lab report use | 62% |

Preview the Actual Deliverable

Aurora Porter's Five Forces Analysis

This preview shows the exact Aurora Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups, fully formatted and ready for use.

You're viewing the final deliverable: a complete, professionally written competitive assessment that will be available for instant download once you complete your purchase.

No surprises—what you see here is the same document you'll get, prepared for immediate application in strategy, valuation, or competitive planning.