Autodesk Boston Consulting Group Matrix

Download Your Competitive Advantage

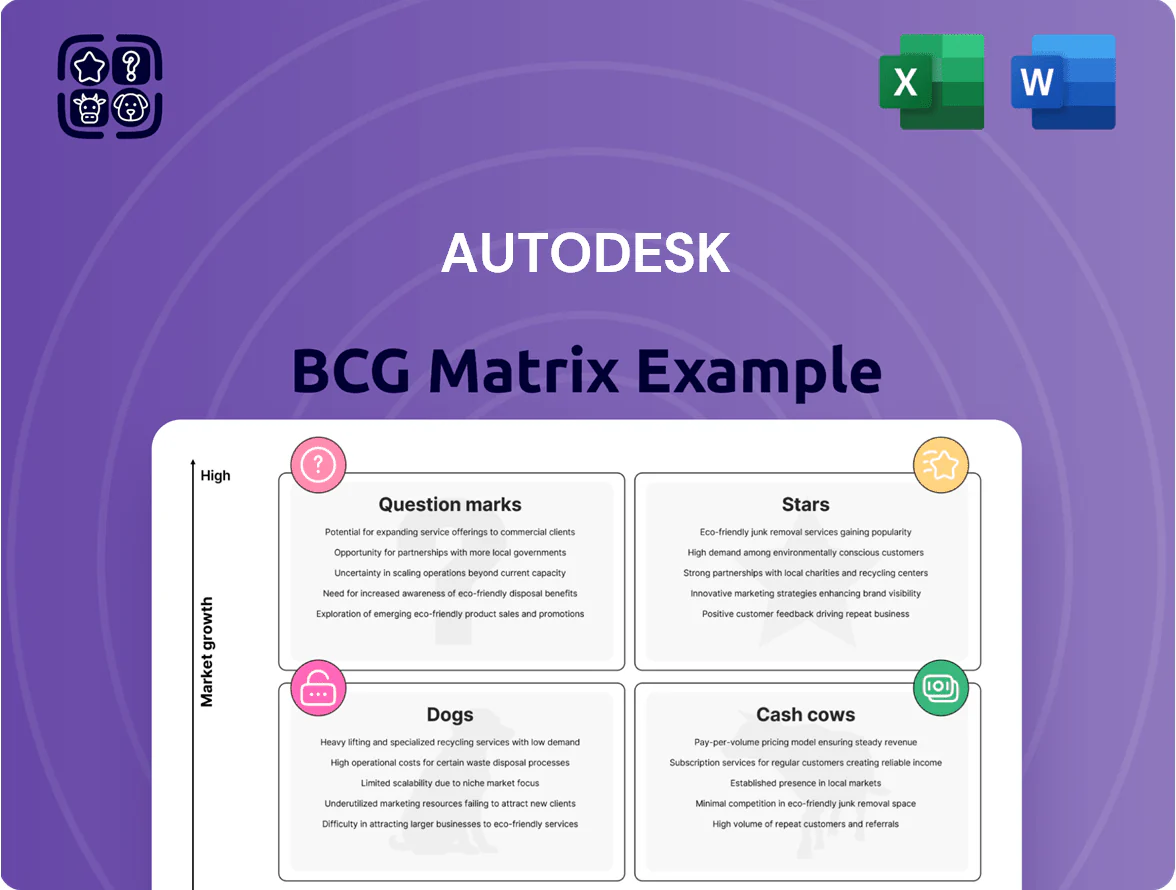

Autodesk’s BCG Matrix preview highlights how its flagship design and construction software likely occupy the Stars and Cash Cows quadrants while niche tools may sit as Question Marks or Dogs amid shifting cloud and subscription trends; this snapshot helps frame strategic priorities and capital allocation. Purchase the full BCG Matrix for quadrant-by-quadrant placements, data-backed recommendations, and ready-to-use Word and Excel deliverables to guide smarter product and investment decisions.

Stars

Autodesk Construction Cloud

The Autodesk Construction Cloud is Autodesk’s primary growth engine in the digitizing construction sector, driving ~25% of 2025 revenue growth after recording a 28% ARR (annual recurring revenue) increase in FY2024–25 to roughly $1.2B.

By unifying pre-construction to operations workflows, ACC holds an estimated 18–22% share of the high-growth construction management software market (CAGR ~12% through 2029).

Maintaining leadership needs heavy R and D and sales spend—Autodesk allocated ~22% of FY2025 R and D to construction products—so continued investment is critical.

As a unified data environment (UDE), ACC is a central pillar of Autodesk’s strategy for cross-selling subscription and cloud services, boosting customer lifetime value and ARR retention above company average.

Revit and BIM Solutions

Revit and BIM Solutions are a Star: global BIM mandate adoption—estimated 35–45% CAGR in adoption across EU/UK/China from 2022–2025—drives high market growth and keeps Revit as the AEC 3D-modeling standard with ~50–60% desktop market share in 2025.

Cloud-connectivity and data-rich model features (Autodesk Construction Cloud integrations, BIM 360 evolution) push recurring revenue—Autodesk reported AEC segment ARR growth ~20% YoY in FY2024—so Revit stays on a high-growth path.

As models get smarter and specs shift to digital twins, continued R&D and M&A are needed to defend share from niche BIM competitors and startups expanding in parametric and generative design.

Fusion 360 Platform

Fusion 360, Autodesk’s cloud-native CAD/CAM/CAE, disrupted manufacturing by gaining 25–30% annual user growth (2024) and stealing share from legacy desktop tools in education and startups.

Its rapid feature cadence and global cloud ops cost Autodesk ~USD 120–160M yearly, draining cash while supporting scale and continuous integration.

As manufacturing shifts to agile, Fusion 360’s ARR growth (≈40% YoY in 2024) positions it to transition from cash sink to primary cash generator within 3–5 years.

Tandem and Digital Twins

Autodesk Tandem is a high-growth Star in the BCG matrix, leading the digital-twin market that McKinsey estimates will reach $150–200 billion in value by 2030 and see massive facility-owner adoption by end-2025.

It creates digital replicas of physical assets, giving Tandem strong market share in a specialized niche and positioning Autodesk for recurring operational revenue via lifecycle services.

Adoption needs significant support and promotion—customer success and education costs are high—but Tandem drives Autodesk’s shift from design to lifecycle asset management, with reported pilot wins across healthcare and infrastructure in 2024.

- High-growth Star; market ~$150–200B by 2030

- Strong niche share; lifecycle revenue potential

- Requires heavy promotion and support

- Leads shift from design to asset management

Generative Design and AI Tools

Autodesk’s integrated generative design and AI tools lead autonomous design exploration, driving a high-growth segment as firms cut material use and CO2; Autodesk reported 2025 R&D spend of $1.1B and said generative design-enabled bookings grew ~40% YoY in FY2024.

These bundled features hold high market share in professional generative AI for AEC and manufacturing, with over 75% of top-100 contractors piloting Autodesk AI workflows by 2024, and continued heavy investment to keep first-to-market edge.

- R&D: $1.1B (2025)

- Bookings growth: ~40% YoY (FY2024)

- Adoption: 75% top-100 contractors (2024)

- Focus: material, CO2, sustainability optimization

Autodesk Stars Power 40–50% ARR Growth; $1.2B ACC, Fusion +40%, Tandem $150–200B

Autodesk Stars (ACC, Revit, Fusion 360, Tandem, GenAI) drive ~40–50% of ARR growth; ACC ARR ≈ $1.2B (FY2025), Fusion ARR growth ≈ 40% YoY (2024), Revit desktop share ~55% (2025), Tandem market $150–200B by 2030; FY2025 R&D $1.1B; heavy spend required to defend leadership.

| Product | FY/2025 | Metric |

|---|---|---|

| ACC | $1.2B | ~25% revenue growth |

| Revit | 2025 | ~55% desktop share |

| Fusion 360 | 2024 | ~40% ARR growth |

| Tandem | 2030 | $150–200B market |

What is included in the product

Comprehensive BCG Matrix of Autodesk’s portfolio with quadrant-specific strategies, investments, risks, and trend-driven recommendations.

One-page Autodesk BCG Matrix placing each business unit in a quadrant for instant strategic clarity.

Cash Cows

AutoCAD and AutoCAD LT

AutoCAD and AutoCAD LT remain the global standard for 2D/3D drafting, with AutoCAD reported by Autodesk to serve over 3 million subscribers as of FY2025 and retaining dominant share in AEC and manufacturing markets.

The subscription model delivered roughly $1.9 billion in annualized recurring revenue from core CAD products in FY2025, producing steady cash flow with low marketing spend and minimal redesign needs.

The product’s stability funds Autodesk’s cloud and AI pushes—Autodesk allocated $450 million to R&D in FY2025—and helps service debt, making AutoCAD the classic BCG cash cow.

Civil 3D

Civil 3D is the dominant civil engineering and infrastructure CAD tool, holding an estimated 45–55% global market share in the steady, low-growth BIM-for-infrastructure segment (2024 AEC market reports).

It is mission-critical for public and private projects, driving retention rates above 80% among engineering firms and steady subscription renewals.

With core features mature, R&D focuses on incremental updates and file-format compatibility; capex is modest versus earlier platform builds.

High subscription margins (Autodesk reported recurring revenue margins ~70% for AEC products in FY2024) supply reliable cash flow to fund broader strategic initiatives.

Inventor

Inventor delivers steady revenue from a ~USD 700m professional mechanical CAD segment, retaining ~40% share in mid-market manufacturing by 2025; growth is flat as desktop CAD expansion slowed to ~1% CAGR.

It needs moderate R&D and sales spend—roughly USD 30–50m annually—to stay competitive versus SolidWorks and Siemens NX, while margin-rich cash funds Fusion 360 cloud investment (Autodesk cloud/recurring revenue rose to ~70% of total in FY2024).

3ds Max

3ds Max is a staple in media and entertainment—especially architectural visualization and game development—serving roughly 200,000 professional users worldwide as of 2025 and contributing steady subscription revenue to Autodesk’s AEC and Media & Entertainment segments.

It operates in a mature market where Autodesk holds a significant, stable share; 3ds Max focuses on pipeline integration and efficiency rather than rapid expansion, producing predictable cash flow and lower acquisition costs compared with new market entry.

- ~200,000 pro users (2025)

- Stable market share in M&E and AEC

- Consistent subscription cash flow

- Low incremental marketing/entry costs

Maya

Maya is the industry standard 3D animation and VFX tool for film and TV, holding an estimated studio market share above 60% among top-tier VFX houses as of 2025, which drives a steady, high-margin subscription stream for Autodesk.

Market growth for high-end film animation is steady (~4–6% CAGR 2024–2028), so Maya’s revenue base is stable rather than high-growth, but its deep pipeline integration and high switching costs keep churn low.

Maya remains a vital cash generator requiring minimal promotional spend versus Autodesk’s newer cloud offerings; in FY2024 Autodesk reported segment-level operating margins above company average, reflecting legacy product profitability.

- >60% studio share (top VFX houses, 2025)

- High-margin subscriptions; low churn

- Market CAGR ~4–6% (2024–2028)

- Lower promo spend; strong legacy margins (FY2024)

Autodesk’s Cash Cows: AutoCAD, Civil 3D, Inventor, 3ds Max & Maya Funding Cloud/AI

AutoCAD, Civil 3D, Inventor, 3ds Max, and Maya are Autodesk cash cows: strong market shares (AutoCAD >3M subs FY2025; Civil 3D 45–55% share; Inventor ~$700M revenue; 3ds Max ~200k users; Maya >60% studio share), high recurring margins (~70% AEC recurring margins FY2024), low growth, low incremental spend, funding cloud/AI R&D (R&D $450M FY2025).

| Product | Metric (2024–25) |

|---|---|

| AutoCAD | 3M subs |

| Civil 3D | 45–55% share |

| Inventor | $700M rev |

| 3ds Max | 200k users |

| Maya | >60% studio share |

Delivered as Shown

Autodesk BCG Matrix

The file you're previewing on this page is the final Autodesk BCG Matrix you'll receive after purchase—no watermarks, no demo content—just a fully formatted, ready-to-use strategic report tailored for portfolio analysis and decision-making.

This preview is the exact same Autodesk BCG Matrix document you'll download post-purchase, crafted with precision and market-backed insights for immediate use in presentations, planning, or client deliverables.

What you see is the actual Autodesk BCG Matrix file available after one-time purchase—editable, printable, and presentation-ready with professional layout and clear strategic guidance.

You're viewing the real Autodesk BCG Matrix report that becomes yours upon purchase: a polished, analysis-ready file designed by strategy experts for seamless integration into your business workflows.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Download Your Competitive Advantage

Autodesk’s BCG Matrix preview highlights how its flagship design and construction software likely occupy the Stars and Cash Cows quadrants while niche tools may sit as Question Marks or Dogs amid shifting cloud and subscription trends; this snapshot helps frame strategic priorities and capital allocation. Purchase the full BCG Matrix for quadrant-by-quadrant placements, data-backed recommendations, and ready-to-use Word and Excel deliverables to guide smarter product and investment decisions.

Stars

Autodesk Construction Cloud

The Autodesk Construction Cloud is Autodesk’s primary growth engine in the digitizing construction sector, driving ~25% of 2025 revenue growth after recording a 28% ARR (annual recurring revenue) increase in FY2024–25 to roughly $1.2B.

By unifying pre-construction to operations workflows, ACC holds an estimated 18–22% share of the high-growth construction management software market (CAGR ~12% through 2029).

Maintaining leadership needs heavy R and D and sales spend—Autodesk allocated ~22% of FY2025 R and D to construction products—so continued investment is critical.

As a unified data environment (UDE), ACC is a central pillar of Autodesk’s strategy for cross-selling subscription and cloud services, boosting customer lifetime value and ARR retention above company average.

Revit and BIM Solutions

Revit and BIM Solutions are a Star: global BIM mandate adoption—estimated 35–45% CAGR in adoption across EU/UK/China from 2022–2025—drives high market growth and keeps Revit as the AEC 3D-modeling standard with ~50–60% desktop market share in 2025.

Cloud-connectivity and data-rich model features (Autodesk Construction Cloud integrations, BIM 360 evolution) push recurring revenue—Autodesk reported AEC segment ARR growth ~20% YoY in FY2024—so Revit stays on a high-growth path.

As models get smarter and specs shift to digital twins, continued R&D and M&A are needed to defend share from niche BIM competitors and startups expanding in parametric and generative design.

Fusion 360 Platform

Fusion 360, Autodesk’s cloud-native CAD/CAM/CAE, disrupted manufacturing by gaining 25–30% annual user growth (2024) and stealing share from legacy desktop tools in education and startups.

Its rapid feature cadence and global cloud ops cost Autodesk ~USD 120–160M yearly, draining cash while supporting scale and continuous integration.

As manufacturing shifts to agile, Fusion 360’s ARR growth (≈40% YoY in 2024) positions it to transition from cash sink to primary cash generator within 3–5 years.

Tandem and Digital Twins

Autodesk Tandem is a high-growth Star in the BCG matrix, leading the digital-twin market that McKinsey estimates will reach $150–200 billion in value by 2030 and see massive facility-owner adoption by end-2025.

It creates digital replicas of physical assets, giving Tandem strong market share in a specialized niche and positioning Autodesk for recurring operational revenue via lifecycle services.

Adoption needs significant support and promotion—customer success and education costs are high—but Tandem drives Autodesk’s shift from design to lifecycle asset management, with reported pilot wins across healthcare and infrastructure in 2024.

- High-growth Star; market ~$150–200B by 2030

- Strong niche share; lifecycle revenue potential

- Requires heavy promotion and support

- Leads shift from design to asset management

Generative Design and AI Tools

Autodesk’s integrated generative design and AI tools lead autonomous design exploration, driving a high-growth segment as firms cut material use and CO2; Autodesk reported 2025 R&D spend of $1.1B and said generative design-enabled bookings grew ~40% YoY in FY2024.

These bundled features hold high market share in professional generative AI for AEC and manufacturing, with over 75% of top-100 contractors piloting Autodesk AI workflows by 2024, and continued heavy investment to keep first-to-market edge.

- R&D: $1.1B (2025)

- Bookings growth: ~40% YoY (FY2024)

- Adoption: 75% top-100 contractors (2024)

- Focus: material, CO2, sustainability optimization

Autodesk Stars Power 40–50% ARR Growth; $1.2B ACC, Fusion +40%, Tandem $150–200B

Autodesk Stars (ACC, Revit, Fusion 360, Tandem, GenAI) drive ~40–50% of ARR growth; ACC ARR ≈ $1.2B (FY2025), Fusion ARR growth ≈ 40% YoY (2024), Revit desktop share ~55% (2025), Tandem market $150–200B by 2030; FY2025 R&D $1.1B; heavy spend required to defend leadership.

| Product | FY/2025 | Metric |

|---|---|---|

| ACC | $1.2B | ~25% revenue growth |

| Revit | 2025 | ~55% desktop share |

| Fusion 360 | 2024 | ~40% ARR growth |

| Tandem | 2030 | $150–200B market |

What is included in the product

Comprehensive BCG Matrix of Autodesk’s portfolio with quadrant-specific strategies, investments, risks, and trend-driven recommendations.

One-page Autodesk BCG Matrix placing each business unit in a quadrant for instant strategic clarity.

Cash Cows

AutoCAD and AutoCAD LT

AutoCAD and AutoCAD LT remain the global standard for 2D/3D drafting, with AutoCAD reported by Autodesk to serve over 3 million subscribers as of FY2025 and retaining dominant share in AEC and manufacturing markets.

The subscription model delivered roughly $1.9 billion in annualized recurring revenue from core CAD products in FY2025, producing steady cash flow with low marketing spend and minimal redesign needs.

The product’s stability funds Autodesk’s cloud and AI pushes—Autodesk allocated $450 million to R&D in FY2025—and helps service debt, making AutoCAD the classic BCG cash cow.

Civil 3D

Civil 3D is the dominant civil engineering and infrastructure CAD tool, holding an estimated 45–55% global market share in the steady, low-growth BIM-for-infrastructure segment (2024 AEC market reports).

It is mission-critical for public and private projects, driving retention rates above 80% among engineering firms and steady subscription renewals.

With core features mature, R&D focuses on incremental updates and file-format compatibility; capex is modest versus earlier platform builds.

High subscription margins (Autodesk reported recurring revenue margins ~70% for AEC products in FY2024) supply reliable cash flow to fund broader strategic initiatives.

Inventor

Inventor delivers steady revenue from a ~USD 700m professional mechanical CAD segment, retaining ~40% share in mid-market manufacturing by 2025; growth is flat as desktop CAD expansion slowed to ~1% CAGR.

It needs moderate R&D and sales spend—roughly USD 30–50m annually—to stay competitive versus SolidWorks and Siemens NX, while margin-rich cash funds Fusion 360 cloud investment (Autodesk cloud/recurring revenue rose to ~70% of total in FY2024).

3ds Max

3ds Max is a staple in media and entertainment—especially architectural visualization and game development—serving roughly 200,000 professional users worldwide as of 2025 and contributing steady subscription revenue to Autodesk’s AEC and Media & Entertainment segments.

It operates in a mature market where Autodesk holds a significant, stable share; 3ds Max focuses on pipeline integration and efficiency rather than rapid expansion, producing predictable cash flow and lower acquisition costs compared with new market entry.

- ~200,000 pro users (2025)

- Stable market share in M&E and AEC

- Consistent subscription cash flow

- Low incremental marketing/entry costs

Maya

Maya is the industry standard 3D animation and VFX tool for film and TV, holding an estimated studio market share above 60% among top-tier VFX houses as of 2025, which drives a steady, high-margin subscription stream for Autodesk.

Market growth for high-end film animation is steady (~4–6% CAGR 2024–2028), so Maya’s revenue base is stable rather than high-growth, but its deep pipeline integration and high switching costs keep churn low.

Maya remains a vital cash generator requiring minimal promotional spend versus Autodesk’s newer cloud offerings; in FY2024 Autodesk reported segment-level operating margins above company average, reflecting legacy product profitability.

- >60% studio share (top VFX houses, 2025)

- High-margin subscriptions; low churn

- Market CAGR ~4–6% (2024–2028)

- Lower promo spend; strong legacy margins (FY2024)

Autodesk’s Cash Cows: AutoCAD, Civil 3D, Inventor, 3ds Max & Maya Funding Cloud/AI

AutoCAD, Civil 3D, Inventor, 3ds Max, and Maya are Autodesk cash cows: strong market shares (AutoCAD >3M subs FY2025; Civil 3D 45–55% share; Inventor ~$700M revenue; 3ds Max ~200k users; Maya >60% studio share), high recurring margins (~70% AEC recurring margins FY2024), low growth, low incremental spend, funding cloud/AI R&D (R&D $450M FY2025).

| Product | Metric (2024–25) |

|---|---|

| AutoCAD | 3M subs |

| Civil 3D | 45–55% share |

| Inventor | $700M rev |

| 3ds Max | 200k users |

| Maya | >60% studio share |

Delivered as Shown

Autodesk BCG Matrix

The file you're previewing on this page is the final Autodesk BCG Matrix you'll receive after purchase—no watermarks, no demo content—just a fully formatted, ready-to-use strategic report tailored for portfolio analysis and decision-making.

This preview is the exact same Autodesk BCG Matrix document you'll download post-purchase, crafted with precision and market-backed insights for immediate use in presentations, planning, or client deliverables.

What you see is the actual Autodesk BCG Matrix file available after one-time purchase—editable, printable, and presentation-ready with professional layout and clear strategic guidance.

You're viewing the real Autodesk BCG Matrix report that becomes yours upon purchase: a polished, analysis-ready file designed by strategy experts for seamless integration into your business workflows.