Autodesk PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic cycles, and rapid tech advances are shaping Autodesk's strategic outlook in our concise PESTLE snapshot—perfect for investors and strategists who need clarity fast.

Our full PESTLE delivers a deep, ready-to-use external analysis with actionable insights on regulation, sustainability, and market drivers—ideal for pitches, planning, or investment cases.

Buy the complete report now to access the detailed breakdown, editable charts, and recommendations you can apply immediately.

Political factors

Geopolitical Trade Relations

Ongoing US-China trade tensions through late 2025 have constrained Autodesk’s China sales, with FY2024 revenue exposure to APAC around 20% and China-specific cloud subscription growth slowing to mid-single digits versus global 18% CAGR. Export controls on advanced simulation and CAM tools require continuous compliance; US BIS rule changes in 2024 broadened licensing needs affecting product distribution. These dynamics risk slower revenue growth in emerging markets where local competitors, backed by preferential policies, captured roughly 5–8% share gains in 2023–24.

Government Infrastructure Mandates

National governments are increasingly mandating Building Information Modeling for public works to boost efficiency and transparency; by 2025 the EU and US infrastructure bills (combined >$2.5 trillion enacted 2021–2022) reached peak implementation, sustaining AEC software demand. Autodesk, with ~45% market share in BIM tools and placement on multiple government-approved software lists, is a primary beneficiary of these mandates.

Digitalization of Public Services

The global push for digital transformation in government agencies is driving demand for secure cloud collaboration tools; public cloud spending reached $621B in 2024, pressuring suppliers to meet stringent security standards that benefit Autodesk’s AEC cloud offerings.

Governments are prioritizing modernization of land registries and urban planning via digital twins—estimated to generate $48B in public sector value by 2026—aligning with Autodesk’s platform capabilities.

This trend creates a tailwind as Autodesk secures multi-year public-sector contracts (Autodesk reported 18% growth in AEC subscription revenue in FY2024), locking in long-term digital infrastructure revenue.

Cybersecurity Policy and Regulation

Political emphasis on national security has driven stricter cybersecurity rules for vendors to critical infrastructure; Autodesk faces compliance demands after 2024–25 executive orders requiring stronger encryption and data residency for cloud CAD platforms.

Failing to meet these standards risks exclusion from defense and utility contracts worth billions—US federal IT contracts totaled about $92B in FY2024, with critical infrastructure procurements a significant share.

- 2024–25 orders: higher encryption, data sovereignty

- Compliance required to access ~$92B federal IT market (FY2024)

- Noncompliance risks loss of defense/utility contracts

Global Tax Harmonization

- OECD Pillar Two: 15% global minimum tax for groups >EUR 750m

- Software sector ETR rose ~1–3 ppt in 2024–2025

- Digital value vs. booking shifts increase tax audit risk

- Requires transfer-pricing, capital-allocation adjustments

Autodesk Faces China Headwinds as BIM Demand and Cloud Spend Drive Growth Amid Pillar Two

US-China trade tensions and 2024 export controls slowed Autodesk’s China/cloud growth; APAC ~20% revenue exposure. Public BIM mandates and $2.5T infrastructure spending turbocharge AEC demand; Autodesk ~45% BIM share. 2024 public cloud spend $621B; federal IT market ~$92B. OECD Pillar Two 15% minimum tax for >€750M affects tax planning; software ETRs rose ~1–3 ppt (2024–25).

| Metric | Value |

|---|---|

| APAC revenue | ~20% |

| BIM market share | ~45% |

| Public cloud spend 2024 | $621B |

| Federal IT (FY2024) | $92B |

| Pillar Two rate | 15% |

What is included in the product

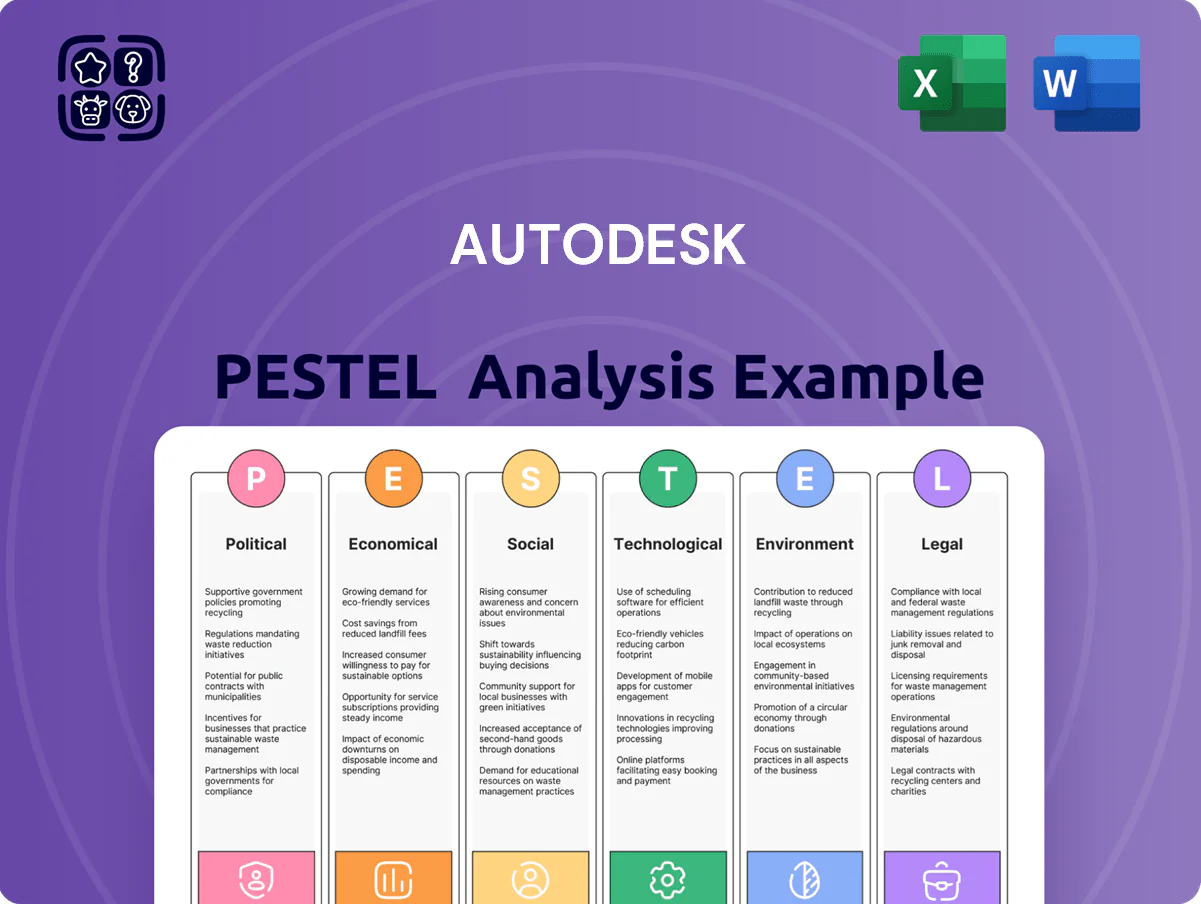

Explores how external macro-environmental factors uniquely affect Autodesk across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—each backed by current data and trends to identify threats, opportunities, and forward-looking scenarios for executives, investors, and strategists.

Condenses Autodesk's PESTLE insights into a concise, shareable summary that’s visually segmented for quick interpretation, easily dropped into presentations, and editable for region- or business-specific notes to support strategic planning and risk discussions.

Economic factors

Interest Rate Environment

Stabilization of global interest rates after early-2020s volatility supports construction and real estate cycles, with global bank rate dispersion falling to a 3-year low in 2024 and OECD average policy rates near 3.5% by mid-2025, boosting capital projects and demand for AEC software seats for firms like Autodesk.

Subscription Model Resilience

The shift to a fully subscription-based model gives Autodesk stable recurring revenue—subscription revenue hit 92% of total revenue in FY2024—helping buffer against downturns by smoothing cash flows. By end-2025 this maturation enables tighter forecasting and supports reallocation of capital, with R&D spending rising to about 17% of revenue in 2024 and planned increases into 2025. Investors favor this stability; Autodesk’s enterprise value/EBITDA multiples remained resilient at ~22x in 2024 despite macro volatility.

Inflationary Pressure on Operating Costs

Persistent inflation in technical labor markets lifted US tech wages by about 6.5% in 2024, increasing Autodesk’s software development and support costs and compressing margins on subscription services.

To protect profitability Autodesk enacted periodic price adjustments—its 2024 average subscription price rise was reported near 7%—affecting cloud and desktop offerings.

Key challenge: raising prices to offset higher operating costs without pushing users to lower-cost CAD/3D alternatives or accelerating churn in a market where price sensitivity has increased.

Currency Exchange Volatility

As a global company, Autodesk earned about 65% of revenue outside the US in FY2024, making results sensitive to USD fluctuations; a 10% USD appreciation vs EUR/JPY in 2024 trimmed reported revenue by roughly $150–200 million in currency translation effects.

Autodesk hedges foreign-currency cash flows and balance sheet exposures, using forwards and options, but long-term currency shifts still affect global pricing, competitiveness and reported ARR.

- ~65% revenue outside US (FY2024)

- 10% USD appreciation ≈ $150–200M negative translation impact (2024)

- Active hedging via forwards/options; long-term FX risk persists

Shift in Global Manufacturing Hubs

Economic shifts are driving diversification of manufacturing away from China toward Southeast Asia and Latin America, with Vietnam, Indonesia and Mexico growing manufacturing FDI by 18–25% YoY in 2024 and ASEAN manufacturing output up ~7% in 2023–24.

This migration opens demand for Autodesk manufacturing software—Fusion 360 adoption targets SMEs in these regions where digitalization spending is rising ~12% CAGR to 2026—and Autodesk is reallocating sales resources accordingly.

- ASEAN manufacturing output +7% (2023–24)

- FDI into Vietnam/Indonesia/Mexico +18–25% YoY (2024)

- Digitalization spend in manufacturing ~12% CAGR to 2026

- Autodesk expanding regional sales teams to capture SME market

Autodesk: Strong subscription cashflows weather FX headwinds as manufacturing digitalizes

Stable rates and subscription mix (92% revenue FY2024) bolster Autodesk cash flows; FX headwinds (65% international revenue; 10% USD rise ≈ $150–200M impact 2024) and 6.5% US tech wage inflation raised costs; 2024 price increases ~7% protect margins; ASEAN/Mexico manufacturing FDI +18–25% YoY (2024) fuels Fusion 360 SME demand (~12% digitalization spend CAGR to 2026).

| Metric | Value |

|---|---|

| Subscription % (FY2024) | 92% |

| Intl revenue | ~65% |

| USD 10% appreciation impact | $150–200M |

| US tech wage inflation 2024 | ~6.5% |

| Avg price increase 2024 | ~7% |

| ASEAN/Mexico FDI growth 2024 | 18–25% YoY |

| Manufacturing digitalization CAGR | ~12% to 2026 |

Same Document Delivered

Autodesk PESTLE Analysis

The preview shown here is the exact Autodesk PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or presentations.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic cycles, and rapid tech advances are shaping Autodesk's strategic outlook in our concise PESTLE snapshot—perfect for investors and strategists who need clarity fast.

Our full PESTLE delivers a deep, ready-to-use external analysis with actionable insights on regulation, sustainability, and market drivers—ideal for pitches, planning, or investment cases.

Buy the complete report now to access the detailed breakdown, editable charts, and recommendations you can apply immediately.

Political factors

Geopolitical Trade Relations

Ongoing US-China trade tensions through late 2025 have constrained Autodesk’s China sales, with FY2024 revenue exposure to APAC around 20% and China-specific cloud subscription growth slowing to mid-single digits versus global 18% CAGR. Export controls on advanced simulation and CAM tools require continuous compliance; US BIS rule changes in 2024 broadened licensing needs affecting product distribution. These dynamics risk slower revenue growth in emerging markets where local competitors, backed by preferential policies, captured roughly 5–8% share gains in 2023–24.

Government Infrastructure Mandates

National governments are increasingly mandating Building Information Modeling for public works to boost efficiency and transparency; by 2025 the EU and US infrastructure bills (combined >$2.5 trillion enacted 2021–2022) reached peak implementation, sustaining AEC software demand. Autodesk, with ~45% market share in BIM tools and placement on multiple government-approved software lists, is a primary beneficiary of these mandates.

Digitalization of Public Services

The global push for digital transformation in government agencies is driving demand for secure cloud collaboration tools; public cloud spending reached $621B in 2024, pressuring suppliers to meet stringent security standards that benefit Autodesk’s AEC cloud offerings.

Governments are prioritizing modernization of land registries and urban planning via digital twins—estimated to generate $48B in public sector value by 2026—aligning with Autodesk’s platform capabilities.

This trend creates a tailwind as Autodesk secures multi-year public-sector contracts (Autodesk reported 18% growth in AEC subscription revenue in FY2024), locking in long-term digital infrastructure revenue.

Cybersecurity Policy and Regulation

Political emphasis on national security has driven stricter cybersecurity rules for vendors to critical infrastructure; Autodesk faces compliance demands after 2024–25 executive orders requiring stronger encryption and data residency for cloud CAD platforms.

Failing to meet these standards risks exclusion from defense and utility contracts worth billions—US federal IT contracts totaled about $92B in FY2024, with critical infrastructure procurements a significant share.

- 2024–25 orders: higher encryption, data sovereignty

- Compliance required to access ~$92B federal IT market (FY2024)

- Noncompliance risks loss of defense/utility contracts

Global Tax Harmonization

- OECD Pillar Two: 15% global minimum tax for groups >EUR 750m

- Software sector ETR rose ~1–3 ppt in 2024–2025

- Digital value vs. booking shifts increase tax audit risk

- Requires transfer-pricing, capital-allocation adjustments

Autodesk Faces China Headwinds as BIM Demand and Cloud Spend Drive Growth Amid Pillar Two

US-China trade tensions and 2024 export controls slowed Autodesk’s China/cloud growth; APAC ~20% revenue exposure. Public BIM mandates and $2.5T infrastructure spending turbocharge AEC demand; Autodesk ~45% BIM share. 2024 public cloud spend $621B; federal IT market ~$92B. OECD Pillar Two 15% minimum tax for >€750M affects tax planning; software ETRs rose ~1–3 ppt (2024–25).

| Metric | Value |

|---|---|

| APAC revenue | ~20% |

| BIM market share | ~45% |

| Public cloud spend 2024 | $621B |

| Federal IT (FY2024) | $92B |

| Pillar Two rate | 15% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Autodesk across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—each backed by current data and trends to identify threats, opportunities, and forward-looking scenarios for executives, investors, and strategists.

Condenses Autodesk's PESTLE insights into a concise, shareable summary that’s visually segmented for quick interpretation, easily dropped into presentations, and editable for region- or business-specific notes to support strategic planning and risk discussions.

Economic factors

Interest Rate Environment

Stabilization of global interest rates after early-2020s volatility supports construction and real estate cycles, with global bank rate dispersion falling to a 3-year low in 2024 and OECD average policy rates near 3.5% by mid-2025, boosting capital projects and demand for AEC software seats for firms like Autodesk.

Subscription Model Resilience

The shift to a fully subscription-based model gives Autodesk stable recurring revenue—subscription revenue hit 92% of total revenue in FY2024—helping buffer against downturns by smoothing cash flows. By end-2025 this maturation enables tighter forecasting and supports reallocation of capital, with R&D spending rising to about 17% of revenue in 2024 and planned increases into 2025. Investors favor this stability; Autodesk’s enterprise value/EBITDA multiples remained resilient at ~22x in 2024 despite macro volatility.

Inflationary Pressure on Operating Costs

Persistent inflation in technical labor markets lifted US tech wages by about 6.5% in 2024, increasing Autodesk’s software development and support costs and compressing margins on subscription services.

To protect profitability Autodesk enacted periodic price adjustments—its 2024 average subscription price rise was reported near 7%—affecting cloud and desktop offerings.

Key challenge: raising prices to offset higher operating costs without pushing users to lower-cost CAD/3D alternatives or accelerating churn in a market where price sensitivity has increased.

Currency Exchange Volatility

As a global company, Autodesk earned about 65% of revenue outside the US in FY2024, making results sensitive to USD fluctuations; a 10% USD appreciation vs EUR/JPY in 2024 trimmed reported revenue by roughly $150–200 million in currency translation effects.

Autodesk hedges foreign-currency cash flows and balance sheet exposures, using forwards and options, but long-term currency shifts still affect global pricing, competitiveness and reported ARR.

- ~65% revenue outside US (FY2024)

- 10% USD appreciation ≈ $150–200M negative translation impact (2024)

- Active hedging via forwards/options; long-term FX risk persists

Shift in Global Manufacturing Hubs

Economic shifts are driving diversification of manufacturing away from China toward Southeast Asia and Latin America, with Vietnam, Indonesia and Mexico growing manufacturing FDI by 18–25% YoY in 2024 and ASEAN manufacturing output up ~7% in 2023–24.

This migration opens demand for Autodesk manufacturing software—Fusion 360 adoption targets SMEs in these regions where digitalization spending is rising ~12% CAGR to 2026—and Autodesk is reallocating sales resources accordingly.

- ASEAN manufacturing output +7% (2023–24)

- FDI into Vietnam/Indonesia/Mexico +18–25% YoY (2024)

- Digitalization spend in manufacturing ~12% CAGR to 2026

- Autodesk expanding regional sales teams to capture SME market

Autodesk: Strong subscription cashflows weather FX headwinds as manufacturing digitalizes

Stable rates and subscription mix (92% revenue FY2024) bolster Autodesk cash flows; FX headwinds (65% international revenue; 10% USD rise ≈ $150–200M impact 2024) and 6.5% US tech wage inflation raised costs; 2024 price increases ~7% protect margins; ASEAN/Mexico manufacturing FDI +18–25% YoY (2024) fuels Fusion 360 SME demand (~12% digitalization spend CAGR to 2026).

| Metric | Value |

|---|---|

| Subscription % (FY2024) | 92% |

| Intl revenue | ~65% |

| USD 10% appreciation impact | $150–200M |

| US tech wage inflation 2024 | ~6.5% |

| Avg price increase 2024 | ~7% |

| ASEAN/Mexico FDI growth 2024 | 18–25% YoY |

| Manufacturing digitalization CAGR | ~12% to 2026 |

Same Document Delivered

Autodesk PESTLE Analysis

The preview shown here is the exact Autodesk PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or presentations.