Autodistribution SWOT Analysis

Your Strategic Toolkit Starts Here

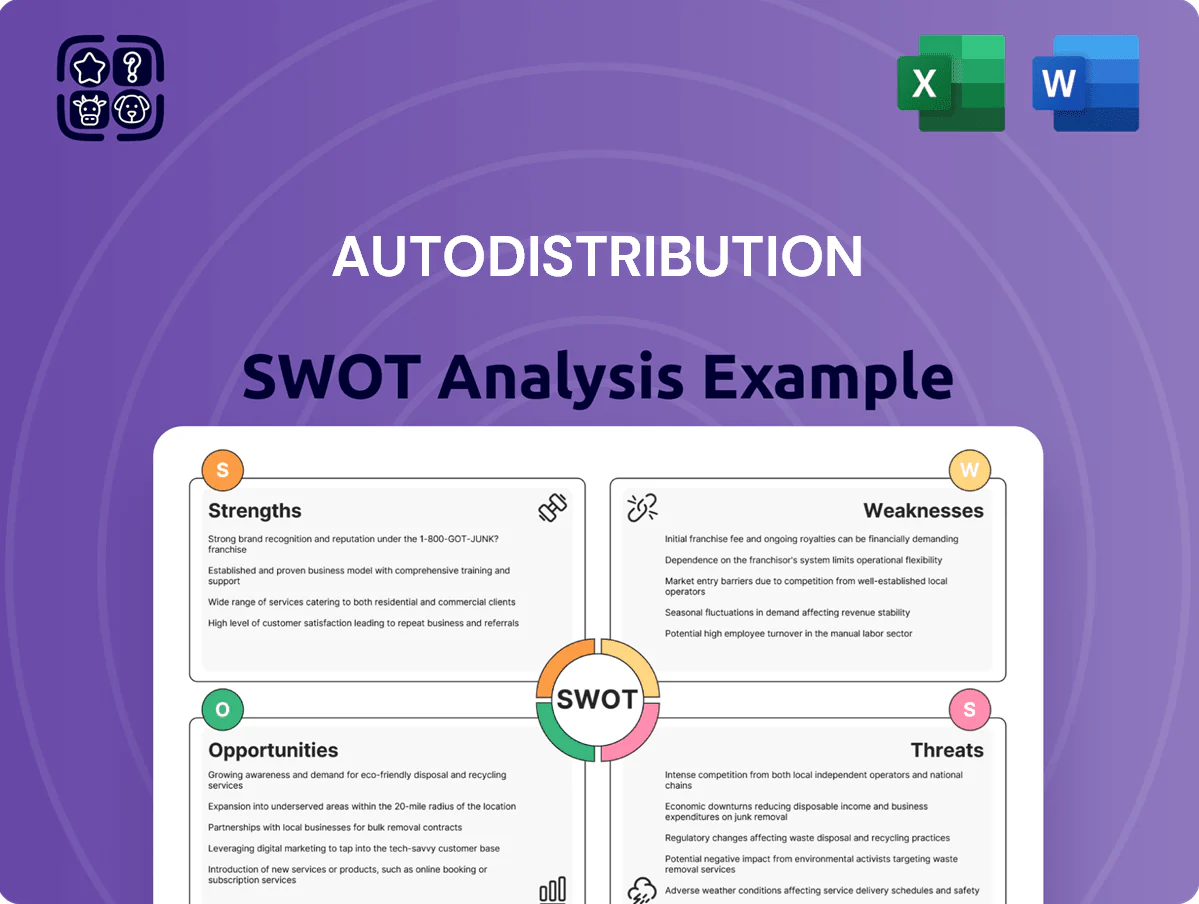

Autodistribution’s SWOT highlights its wide dealer network and digital rollout as key strengths, balanced by inventory tightness and competitive pressure; opportunities include EV parts expansion while regulatory shifts pose risks. Discover the full strategic picture—purchase the complete SWOT analysis for a research-backed, editable report and Excel matrix to support investment, planning, or pitch-ready work.

Strengths

Dominant Market Position in France

Autodistribution leads the French independent aftermarket with ~28% market share in 2024, giving strong brand recognition and a wide garage network that creates a durable competitive moat.

Scale yields superior bargaining power—group purchasing reduced component costs by ~3.5% in 2023 versus peers—boosting margins and supplier access.

Integration into Parts Holding Europe (completed 2025) expands pan‑European procurement, aggregating €1.8bn+ in purchasing volume for better terms.

Robust Logistics and Distribution Network

Autodistribution runs a high-frequency logistics network with multiple daily deliveries to >12,000 partner workshops across France and Iberia, cutting average part lead time to 6 hours in metro areas (2024 internal ops data).

That rapid fulfillment trims vehicle downtime—key for professional workshops—supporting a 14% faster repair cycle versus national averages, boosting workshop throughput and repeat orders.

Over 180 regional warehouses stock long-tail SKUs, keeping fill rates above 97% for niche parts and reducing emergency sourcing costs for customers.

Integrated Digital Service Ecosystem

Autodistribution’s Autossimo platform links distributor and repairer systems, cutting parts-identification time by up to 40% and raising order accuracy to ~98% (2025 internal data), which lowers workshop downtime and parts returns.

Integrated repair data and automated ordering boost workshop productivity—clients report 12–18% higher throughput—and create digital stickiness that reduced churn to 6% vs. 11% industry average in 2024, making displacement costly for rivals.

Strong Multi-Brand Technical Training

The AD Institute trains over 25,000 technicians annually, keeping independent mechanics current on ADAS and hybrid systems and reducing repair turnaround by ~18% (AD internal 2024 data).

This ongoing education builds long-term loyalty—network members report a 12% higher parts share retention—and lets AD handle complex diagnostics, not just parts sales.

Positioning as a knowledge provider expands AD’s value-chain role and supports aftermarket revenue growth; training-linked service upsells raised per-bay revenue by ~9% in 2024.

- 25,000+ technicians trained/year

- 18% faster repair turnaround

- 12% higher parts share retention

- 9% service revenue uplift

Diversified Private Label Portfolio

Autodistribution’s private label Isotech delivered ~18% gross margin improvement vs sourced OEM lines in 2024, letting the group capture higher per-unit profits while pricing ~20–35% below premium parts for price-sensitive owners of older cars.

These private labels carry certified warranties and meet key quality standards (e.g., ISO/TS), so they serve customers seeking value without sacrificing reliability; they complement premium brands to cover vehicles from 0–20+ years.

- Higher margins: +18% (2024)

- Price gap: 20–35% below premium

- Target: owners of 8–20+ year vehicles

- Quality: certified warranties, ISO standards

Autodistribution: 28% of French IAM, 97% fill, 6hr lead time—faster repairs, higher margins

Autodistribution dominates the French IAM with ~28% share (2024), 12,000+ workshops served, 97% fill rates on 180+ warehouses, and 6‑hour metro lead time—driving 14% faster repair cycles, 12–18% workshop throughput gains, and churn at 6% vs 11% industry (2024); Isotech raised gross margins ~18% and prices 20–35% below premium (2024).

| Metric | Value |

|---|---|

| Market share (FR, 2024) | ~28% |

| Workshops served | >12,000 |

| Fill rate | 97% |

| Metro lead time | 6 hrs |

| Repair cycle improvement | +14% |

| Workshop throughput | +12–18% |

| Churn | 6% (vs 11%) |

| Isotech margin uplift | +18% |

What is included in the product

Delivers a concise SWOT overview of Autodistribution’s internal capabilities and external market forces, highlighting core strengths, operational weaknesses, growth opportunities, and potential threats shaping its competitive position.

Delivers a concise Autodistribution SWOT matrix for rapid strategy alignment, enabling stakeholders to visualize strengths, weaknesses, opportunities, and threats at a glance.

Weaknesses

High Exposure to French Market

Despite expansion, Autodistribution still earns about 62% of 2024 revenue in France (estimated €2.1bn of ~€3.4bn total), leaving results highly tied to the French auto market; a local GDP drop or sector-specific slowdown would hit earnings quickly. This concentration raises exposure to French labor strikes—recalls in 2023 cut distribution weeks—and to national regulatory shifts like 2024 emissions rules. Diversification into Spain, Italy and Benelux is progressing, but core financials remain France-dependent.

Significant Fixed Operational Overhead

Maintaining Autodistribution’s 420 local branches and 28 regional warehouses drives heavy fixed costs—estimated at €320m in rent and €210m in payroll in 2024—squeezing margins when demand falls 5–10% seasonally. Energy and labor inflation (2021–24 wage growth ~9%, eurozone industrial gas up 45% peak) can cut operating margin by 150–250 basis points. Balancing service-level expectations and cost control is an ongoing tightrope.

Complexity of Multi-Brand Integration

Legacy Reliance on ICE Components

- High % inventory tied to ICE, declining demand

- EV parts demand 40–60% lower per vehicle

- Estimated €150–250M capex to realign supply chain

- Risk of stranded stock and margin compression

High Leverage from Strategic Acquisitions

The group's aggressive acquisition push left net debt at €1.12 billion at year-end 2024, constraining cash flow and reducing strategic flexibility during downturns.

Servicing that debt demands steady EBITDA—Autodistribution reported 2024 adjusted EBITDA of €185 million—so sudden sales drops or higher rates would tighten liquidity.

Tighter credit or rates up 200bps would raise interest expense materially and could delay tech investments or bolt-on deals.

- Net debt €1.12B (YE 2024)

- Adjusted EBITDA €185M (2024)

- High sensitivity to +200bps rate moves

France-heavy dealer faces margin squeeze, €1.12bn net debt and costly EV transition

Heavy France concentration (~62% revenue; ~€2.1bn/€3.4bn in 2024) and exposure to strikes/regulation; high fixed costs (€320m rent, €210m payroll est. 2024) compress margins; complex M&A estate (450 entities, 12–18m IT projects) raises integration costs; ICE-heavy inventory risks stranded stock as BEV share hits ~14% (2024) — transition may need €150–250m capex while net debt €1.12bn vs EBITDA €185m tightens flexibility.

| Metric | Value |

|---|---|

| France revenue % | 62% (~€2.1bn) |

| Net debt (YE 2024) | €1.12bn |

| Adj. EBITDA (2024) | €185m |

| Estimated fixed costs (2024) | €530m |

| BEV global share (2024) | ~14% |

| Transition capex est. | €150–250m |

Full Version Awaits

Autodistribution SWOT Analysis

This is the actual Autodistribution SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality; the preview below is taken directly from the full report and the complete, editable version is unlocked after checkout.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Strategic Toolkit Starts Here

Autodistribution’s SWOT highlights its wide dealer network and digital rollout as key strengths, balanced by inventory tightness and competitive pressure; opportunities include EV parts expansion while regulatory shifts pose risks. Discover the full strategic picture—purchase the complete SWOT analysis for a research-backed, editable report and Excel matrix to support investment, planning, or pitch-ready work.

Strengths

Dominant Market Position in France

Autodistribution leads the French independent aftermarket with ~28% market share in 2024, giving strong brand recognition and a wide garage network that creates a durable competitive moat.

Scale yields superior bargaining power—group purchasing reduced component costs by ~3.5% in 2023 versus peers—boosting margins and supplier access.

Integration into Parts Holding Europe (completed 2025) expands pan‑European procurement, aggregating €1.8bn+ in purchasing volume for better terms.

Robust Logistics and Distribution Network

Autodistribution runs a high-frequency logistics network with multiple daily deliveries to >12,000 partner workshops across France and Iberia, cutting average part lead time to 6 hours in metro areas (2024 internal ops data).

That rapid fulfillment trims vehicle downtime—key for professional workshops—supporting a 14% faster repair cycle versus national averages, boosting workshop throughput and repeat orders.

Over 180 regional warehouses stock long-tail SKUs, keeping fill rates above 97% for niche parts and reducing emergency sourcing costs for customers.

Integrated Digital Service Ecosystem

Autodistribution’s Autossimo platform links distributor and repairer systems, cutting parts-identification time by up to 40% and raising order accuracy to ~98% (2025 internal data), which lowers workshop downtime and parts returns.

Integrated repair data and automated ordering boost workshop productivity—clients report 12–18% higher throughput—and create digital stickiness that reduced churn to 6% vs. 11% industry average in 2024, making displacement costly for rivals.

Strong Multi-Brand Technical Training

The AD Institute trains over 25,000 technicians annually, keeping independent mechanics current on ADAS and hybrid systems and reducing repair turnaround by ~18% (AD internal 2024 data).

This ongoing education builds long-term loyalty—network members report a 12% higher parts share retention—and lets AD handle complex diagnostics, not just parts sales.

Positioning as a knowledge provider expands AD’s value-chain role and supports aftermarket revenue growth; training-linked service upsells raised per-bay revenue by ~9% in 2024.

- 25,000+ technicians trained/year

- 18% faster repair turnaround

- 12% higher parts share retention

- 9% service revenue uplift

Diversified Private Label Portfolio

Autodistribution’s private label Isotech delivered ~18% gross margin improvement vs sourced OEM lines in 2024, letting the group capture higher per-unit profits while pricing ~20–35% below premium parts for price-sensitive owners of older cars.

These private labels carry certified warranties and meet key quality standards (e.g., ISO/TS), so they serve customers seeking value without sacrificing reliability; they complement premium brands to cover vehicles from 0–20+ years.

- Higher margins: +18% (2024)

- Price gap: 20–35% below premium

- Target: owners of 8–20+ year vehicles

- Quality: certified warranties, ISO standards

Autodistribution: 28% of French IAM, 97% fill, 6hr lead time—faster repairs, higher margins

Autodistribution dominates the French IAM with ~28% share (2024), 12,000+ workshops served, 97% fill rates on 180+ warehouses, and 6‑hour metro lead time—driving 14% faster repair cycles, 12–18% workshop throughput gains, and churn at 6% vs 11% industry (2024); Isotech raised gross margins ~18% and prices 20–35% below premium (2024).

| Metric | Value |

|---|---|

| Market share (FR, 2024) | ~28% |

| Workshops served | >12,000 |

| Fill rate | 97% |

| Metro lead time | 6 hrs |

| Repair cycle improvement | +14% |

| Workshop throughput | +12–18% |

| Churn | 6% (vs 11%) |

| Isotech margin uplift | +18% |

What is included in the product

Delivers a concise SWOT overview of Autodistribution’s internal capabilities and external market forces, highlighting core strengths, operational weaknesses, growth opportunities, and potential threats shaping its competitive position.

Delivers a concise Autodistribution SWOT matrix for rapid strategy alignment, enabling stakeholders to visualize strengths, weaknesses, opportunities, and threats at a glance.

Weaknesses

High Exposure to French Market

Despite expansion, Autodistribution still earns about 62% of 2024 revenue in France (estimated €2.1bn of ~€3.4bn total), leaving results highly tied to the French auto market; a local GDP drop or sector-specific slowdown would hit earnings quickly. This concentration raises exposure to French labor strikes—recalls in 2023 cut distribution weeks—and to national regulatory shifts like 2024 emissions rules. Diversification into Spain, Italy and Benelux is progressing, but core financials remain France-dependent.

Significant Fixed Operational Overhead

Maintaining Autodistribution’s 420 local branches and 28 regional warehouses drives heavy fixed costs—estimated at €320m in rent and €210m in payroll in 2024—squeezing margins when demand falls 5–10% seasonally. Energy and labor inflation (2021–24 wage growth ~9%, eurozone industrial gas up 45% peak) can cut operating margin by 150–250 basis points. Balancing service-level expectations and cost control is an ongoing tightrope.

Complexity of Multi-Brand Integration

Legacy Reliance on ICE Components

- High % inventory tied to ICE, declining demand

- EV parts demand 40–60% lower per vehicle

- Estimated €150–250M capex to realign supply chain

- Risk of stranded stock and margin compression

High Leverage from Strategic Acquisitions

The group's aggressive acquisition push left net debt at €1.12 billion at year-end 2024, constraining cash flow and reducing strategic flexibility during downturns.

Servicing that debt demands steady EBITDA—Autodistribution reported 2024 adjusted EBITDA of €185 million—so sudden sales drops or higher rates would tighten liquidity.

Tighter credit or rates up 200bps would raise interest expense materially and could delay tech investments or bolt-on deals.

- Net debt €1.12B (YE 2024)

- Adjusted EBITDA €185M (2024)

- High sensitivity to +200bps rate moves

France-heavy dealer faces margin squeeze, €1.12bn net debt and costly EV transition

Heavy France concentration (~62% revenue; ~€2.1bn/€3.4bn in 2024) and exposure to strikes/regulation; high fixed costs (€320m rent, €210m payroll est. 2024) compress margins; complex M&A estate (450 entities, 12–18m IT projects) raises integration costs; ICE-heavy inventory risks stranded stock as BEV share hits ~14% (2024) — transition may need €150–250m capex while net debt €1.12bn vs EBITDA €185m tightens flexibility.

| Metric | Value |

|---|---|

| France revenue % | 62% (~€2.1bn) |

| Net debt (YE 2024) | €1.12bn |

| Adj. EBITDA (2024) | €185m |

| Estimated fixed costs (2024) | €530m |

| BEV global share (2024) | ~14% |

| Transition capex est. | €150–250m |

Full Version Awaits

Autodistribution SWOT Analysis

This is the actual Autodistribution SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality; the preview below is taken directly from the full report and the complete, editable version is unlocked after checkout.