AviChina Industry & Technology Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

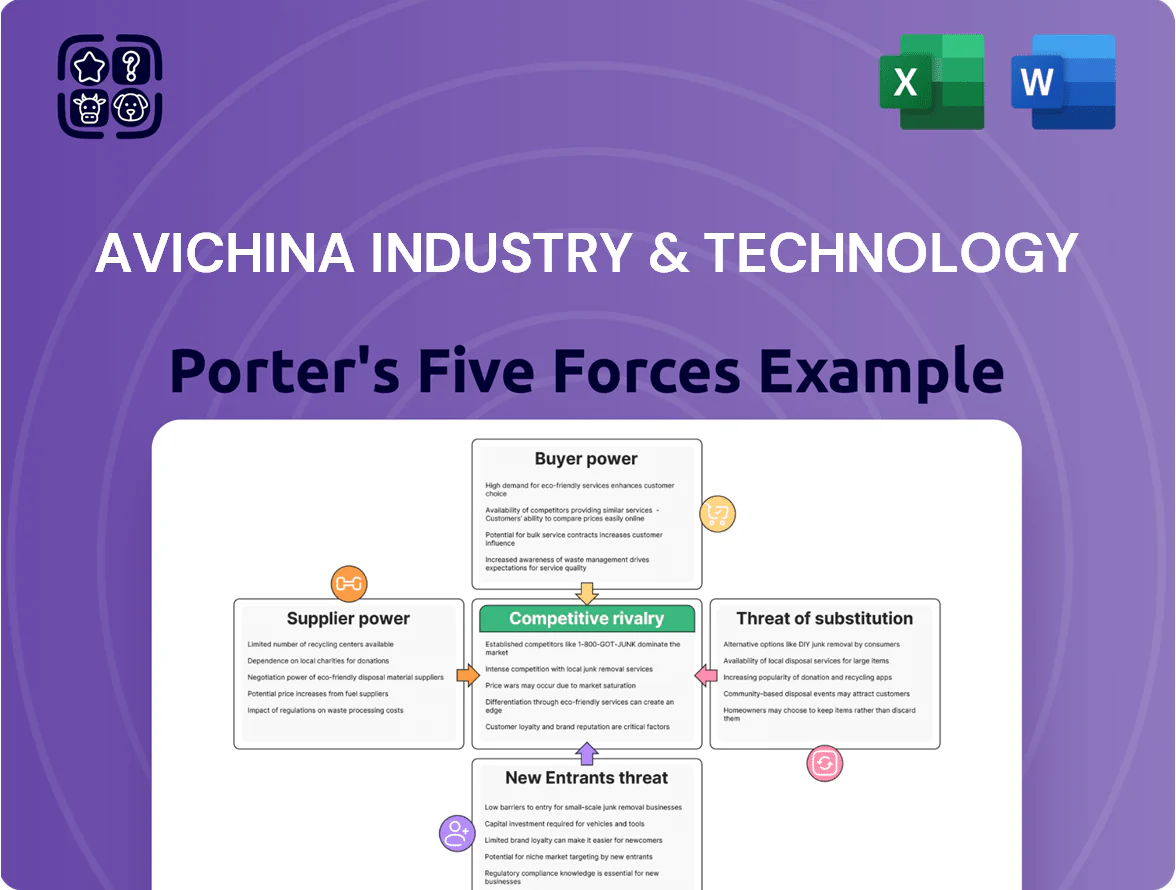

AviChina faces intense supplier and buyer dynamics, moderate threat from new entrants due to high capital and regulatory barriers, strong rivalry among aerospace peers, and evolving substitute risks from international OEMs and tech shifts—impacting margins and strategic choices.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore AviChina Industry & Technology’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Raw Material Dependency

The production of helicopters and components needs titanium alloys, carbon-fiber composites and aerospace-grade aluminum, materials supplied by few certified firms; this scarcity gives suppliers leverage over AviChina’s input costs and timelines.

By late 2025 China’s domestic-sourcing push concentrated supply among state-backed material groups—e.g., China Metallurgical Group and AVIC subsidiary partners—raising bargaining power as they control ~60–70% of certified titanium and composite capacity.

Critical Propulsion and Engine Systems

Despite AviChina's vertical integration, dependence on high-performance engine suppliers remains acute; only 4–6 global turboshaft OEMs serve military-grade helicopters, concentrating pricing power and delivery control.

Engine IP and 7–10 year R&D cycles raise switching costs; in 2024 engine components accounted for ~18% of AviChina's COGS, so supplier delays can shift project margins by 150–300 basis points.

Concentration within the AVIC Ecosystem

High-End Avionics and Electronic Components

The rise of digital cockpits and fly-by-wire control raises supplier power: top avionics firms (Honeywell, Collins Aerospace) and specialist Chinese players command pricing and certification leverage over AviChina for flight-critical modules.

Post-2022 supply shifts increased reliance on domestic semiconductors and IMUs; China’s automotive-grade chip output grew 28% in 2024 but high-reliability aerospace capacity lags, keeping supplier leverage high.

Immediate alternatives are scarce—long certification cycles (2–5 years) and limited qualified suppliers sustain high bargaining power for advanced electronics providers.

- Flight-critical suppliers hold pricing/certification leverage

- China semiconductor output +28% in 2024, aerospace capacity still limited

- Certification 2–5 years → few substitute vendors

Technological Switching Costs

Integrating a new supplier into an existing aircraft platform requires months-to-years of testing and certs from CAAC and EASA, driving switching costs that deter frequent changes and mute AviChina’s price leverage.

High switching costs let incumbent suppliers push harder at renewals; for example, supplier consolidation can raise component margins by 200–400 bps, and a single major avionics recertification can cost >$10m and 12–24 months.

- Months–years recertification time

- >$10m typical major recert cost

- 200–400 bps higher supplier margins

Supplier leverage pins costs: concentrated materials, few engine OEMs, chip supply bottleneck

Suppliers hold high leverage: certified titanium/composite capacity concentrated (60–70% domestic, 2025), 4–6 global turboshaft OEMs, engines = ~18% of COGS (2024), recertification 12–24 months >$10m; intra-AVIC sourcing ~60–75% (2024) stabilizes delivery but limits price leverage; aerospace-grade semiconductor capacity lags despite +28% auto-chip output (2024), keeping avionics/IMU power high.

| Metric | Value |

|---|---|

| Domestic certified titanium/composites | 60–70% (2025) |

| Engine suppliers | 4–6 global OEMs |

| Engines share of COGS | ~18% (2024) |

| Intra-AVIC procurement | 60–75% (2024) |

| Auto-chip output growth | +28% (2024) |

| Recertification cost/time | >$10m / 12–24 months |

What is included in the product

Tailored exclusively for AviChina Industry & Technology, this Porter's Five Forces overview uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats that shape the company’s pricing, profitability, and strategic positioning.

A concise AviChina Porter's Five Forces one-sheet that highlights supplier, buyer, rivalry, entrant, and substitute pressures—ideal for quick strategic decisions and slide-ready summaries.

Customers Bargaining Power

Monopsonistic Military Procurement

AviChina earns roughly 60–70% of revenue from the People’s Liberation Army and state defense agencies, creating a monopsonistic buyer that pressures prices, specs, and delivery dates; in 2024 state contracts accounted for about CNY 22.5 billion of its CNY 34 billion revenue, giving the buyer near-total control of demand and forcing AviChina to accept tighter margins and bespoke design timelines.

State-Owned Enterprise Influence

State-owned airlines and GA operators in China, like Air China and China Eastern (both government-influenced), bundle procurement: in 2024 they accounted for ~65% of domestic airframe/helicopter demand, giving strong collective bargaining power.

They secure concessional financing—China Development Bank-backed deals cut funding costs by ~150–250 bps in recent widebody/rotor contracts—pressuring suppliers on price and margins.

Aligned with Made in China industrial policy, they demand localized MRO, parts sourcing, and tech transfer; AviChina faces requirements for >40% local content and joint venture tech-sharing clauses in major 2023–25 contracts.

Low-Altitude Economy Commercial Buyers

By end-2025 the low-altitude economy added ~40% more commercial buyers—logistics and emergency services—raising order volume but lowering margins; these buyers are highly price-sensitive and benchmark AviChina against global rivals such as Bell and Airbus, whose rotorcraft unit prices run 15–30% higher on comparable specs. This pressure pushed AviChina to adopt competitive pricing and enhanced after-sales packages, with service contracts now representing ~22% of related revenue.

Availability of Global Alternatives

For civil aviation products, customers can pick global OEMs like Airbus (2024 deliveries: 642 aircraft) and Boeing (2024 deliveries: 289), so Chinese offerings must match safety and performance to win orders.

Foreign giants active in China give buyers leverage to benchmark prices and terms, limiting AviChina Industry & Technology’s pricing power in the non-military sector.

- Airbus/Boeing deliveries used as benchmarks

- Global alternatives raise buyer leverage

- Limits AviChina pricing in civil market

High Information Transparency

Financial analysts and institutional buyers in aviation use public performance metrics and ICAO safety benchmarks; 2024 data shows 72% of procurement decisions weigh lifecycle cost over upfront price, pressuring suppliers like AviChina.

This transparency shifts purchase drivers to fuel burn, MTBUR (mean time between unscheduled removals) and resale value, so AviChina must meet tight specs and justify margins against OEM peers.

- 72% lifecycle-cost focus (2024 buyer survey)

- ICAO/FAA standards drive technical thresholds

- MTBUR and fuel burn now key KPIs

- Price premium only if efficiency >5%

Buyers Command Pricing: 66% State Revenue, >40% Local Content, 72% Lifecycle Focus

Buyers hold strong leverage: state defense customers made ~66% of 2024 revenue (CNY22.5bn/34bn), force >40% local content and tech transfer, and drive pricing; civil buyers benchmark Airbus/Boeing (2024 deliveries: 642/289), pushing lifecycle-cost focus (72% of decisions) and limiting price premium to >5% efficiency gains.

| Metric | Value (2024) |

|---|---|

| State revenue share | 66% (CNY22.5bn) |

| Lifecycle-cost weight | 72% |

| Airbus/Boeing deliveries | 642 / 289 |

| Local content req | >40% |

Preview the Actual Deliverable

AviChina Industry & Technology Porter's Five Forces Analysis

This preview shows the exact AviChina Industry & Technology Porter’s Five Forces analysis you’ll receive immediately after purchase—no surprises, no placeholders. The document displayed here is fully formatted and ready for download the moment you buy, containing the same comprehensive assessment of competitive rivalry, supplier and buyer power, threats of entry and substitution, and strategic implications. You’re previewing the final version; once payment is complete, you’ll get instant access to this exact file for immediate use. No mockups or samples—this is the deliverable.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

AviChina faces intense supplier and buyer dynamics, moderate threat from new entrants due to high capital and regulatory barriers, strong rivalry among aerospace peers, and evolving substitute risks from international OEMs and tech shifts—impacting margins and strategic choices.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore AviChina Industry & Technology’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Raw Material Dependency

The production of helicopters and components needs titanium alloys, carbon-fiber composites and aerospace-grade aluminum, materials supplied by few certified firms; this scarcity gives suppliers leverage over AviChina’s input costs and timelines.

By late 2025 China’s domestic-sourcing push concentrated supply among state-backed material groups—e.g., China Metallurgical Group and AVIC subsidiary partners—raising bargaining power as they control ~60–70% of certified titanium and composite capacity.

Critical Propulsion and Engine Systems

Despite AviChina's vertical integration, dependence on high-performance engine suppliers remains acute; only 4–6 global turboshaft OEMs serve military-grade helicopters, concentrating pricing power and delivery control.

Engine IP and 7–10 year R&D cycles raise switching costs; in 2024 engine components accounted for ~18% of AviChina's COGS, so supplier delays can shift project margins by 150–300 basis points.

Concentration within the AVIC Ecosystem

High-End Avionics and Electronic Components

The rise of digital cockpits and fly-by-wire control raises supplier power: top avionics firms (Honeywell, Collins Aerospace) and specialist Chinese players command pricing and certification leverage over AviChina for flight-critical modules.

Post-2022 supply shifts increased reliance on domestic semiconductors and IMUs; China’s automotive-grade chip output grew 28% in 2024 but high-reliability aerospace capacity lags, keeping supplier leverage high.

Immediate alternatives are scarce—long certification cycles (2–5 years) and limited qualified suppliers sustain high bargaining power for advanced electronics providers.

- Flight-critical suppliers hold pricing/certification leverage

- China semiconductor output +28% in 2024, aerospace capacity still limited

- Certification 2–5 years → few substitute vendors

Technological Switching Costs

Integrating a new supplier into an existing aircraft platform requires months-to-years of testing and certs from CAAC and EASA, driving switching costs that deter frequent changes and mute AviChina’s price leverage.

High switching costs let incumbent suppliers push harder at renewals; for example, supplier consolidation can raise component margins by 200–400 bps, and a single major avionics recertification can cost >$10m and 12–24 months.

- Months–years recertification time

- >$10m typical major recert cost

- 200–400 bps higher supplier margins

Supplier leverage pins costs: concentrated materials, few engine OEMs, chip supply bottleneck

Suppliers hold high leverage: certified titanium/composite capacity concentrated (60–70% domestic, 2025), 4–6 global turboshaft OEMs, engines = ~18% of COGS (2024), recertification 12–24 months >$10m; intra-AVIC sourcing ~60–75% (2024) stabilizes delivery but limits price leverage; aerospace-grade semiconductor capacity lags despite +28% auto-chip output (2024), keeping avionics/IMU power high.

| Metric | Value |

|---|---|

| Domestic certified titanium/composites | 60–70% (2025) |

| Engine suppliers | 4–6 global OEMs |

| Engines share of COGS | ~18% (2024) |

| Intra-AVIC procurement | 60–75% (2024) |

| Auto-chip output growth | +28% (2024) |

| Recertification cost/time | >$10m / 12–24 months |

What is included in the product

Tailored exclusively for AviChina Industry & Technology, this Porter's Five Forces overview uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats that shape the company’s pricing, profitability, and strategic positioning.

A concise AviChina Porter's Five Forces one-sheet that highlights supplier, buyer, rivalry, entrant, and substitute pressures—ideal for quick strategic decisions and slide-ready summaries.

Customers Bargaining Power

Monopsonistic Military Procurement

AviChina earns roughly 60–70% of revenue from the People’s Liberation Army and state defense agencies, creating a monopsonistic buyer that pressures prices, specs, and delivery dates; in 2024 state contracts accounted for about CNY 22.5 billion of its CNY 34 billion revenue, giving the buyer near-total control of demand and forcing AviChina to accept tighter margins and bespoke design timelines.

State-Owned Enterprise Influence

State-owned airlines and GA operators in China, like Air China and China Eastern (both government-influenced), bundle procurement: in 2024 they accounted for ~65% of domestic airframe/helicopter demand, giving strong collective bargaining power.

They secure concessional financing—China Development Bank-backed deals cut funding costs by ~150–250 bps in recent widebody/rotor contracts—pressuring suppliers on price and margins.

Aligned with Made in China industrial policy, they demand localized MRO, parts sourcing, and tech transfer; AviChina faces requirements for >40% local content and joint venture tech-sharing clauses in major 2023–25 contracts.

Low-Altitude Economy Commercial Buyers

By end-2025 the low-altitude economy added ~40% more commercial buyers—logistics and emergency services—raising order volume but lowering margins; these buyers are highly price-sensitive and benchmark AviChina against global rivals such as Bell and Airbus, whose rotorcraft unit prices run 15–30% higher on comparable specs. This pressure pushed AviChina to adopt competitive pricing and enhanced after-sales packages, with service contracts now representing ~22% of related revenue.

Availability of Global Alternatives

For civil aviation products, customers can pick global OEMs like Airbus (2024 deliveries: 642 aircraft) and Boeing (2024 deliveries: 289), so Chinese offerings must match safety and performance to win orders.

Foreign giants active in China give buyers leverage to benchmark prices and terms, limiting AviChina Industry & Technology’s pricing power in the non-military sector.

- Airbus/Boeing deliveries used as benchmarks

- Global alternatives raise buyer leverage

- Limits AviChina pricing in civil market

High Information Transparency

Financial analysts and institutional buyers in aviation use public performance metrics and ICAO safety benchmarks; 2024 data shows 72% of procurement decisions weigh lifecycle cost over upfront price, pressuring suppliers like AviChina.

This transparency shifts purchase drivers to fuel burn, MTBUR (mean time between unscheduled removals) and resale value, so AviChina must meet tight specs and justify margins against OEM peers.

- 72% lifecycle-cost focus (2024 buyer survey)

- ICAO/FAA standards drive technical thresholds

- MTBUR and fuel burn now key KPIs

- Price premium only if efficiency >5%

Buyers Command Pricing: 66% State Revenue, >40% Local Content, 72% Lifecycle Focus

Buyers hold strong leverage: state defense customers made ~66% of 2024 revenue (CNY22.5bn/34bn), force >40% local content and tech transfer, and drive pricing; civil buyers benchmark Airbus/Boeing (2024 deliveries: 642/289), pushing lifecycle-cost focus (72% of decisions) and limiting price premium to >5% efficiency gains.

| Metric | Value (2024) |

|---|---|

| State revenue share | 66% (CNY22.5bn) |

| Lifecycle-cost weight | 72% |

| Airbus/Boeing deliveries | 642 / 289 |

| Local content req | >40% |

Preview the Actual Deliverable

AviChina Industry & Technology Porter's Five Forces Analysis

This preview shows the exact AviChina Industry & Technology Porter’s Five Forces analysis you’ll receive immediately after purchase—no surprises, no placeholders. The document displayed here is fully formatted and ready for download the moment you buy, containing the same comprehensive assessment of competitive rivalry, supplier and buyer power, threats of entry and substitution, and strategic implications. You’re previewing the final version; once payment is complete, you’ll get instant access to this exact file for immediate use. No mockups or samples—this is the deliverable.