AeroVironment Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

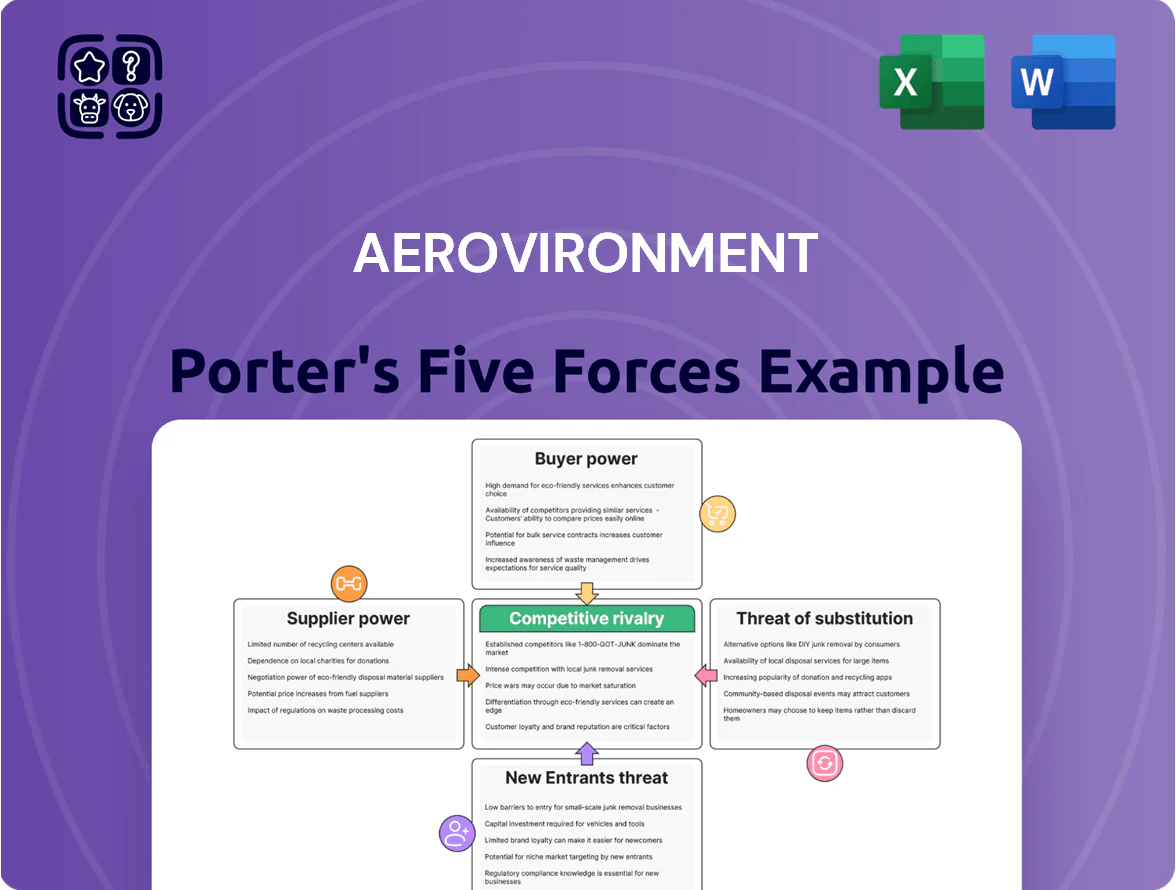

AeroVironment faces intense rivalry from larger defense contractors, specialized UAV firms, and rapid tech entrants, while supplier specialization and defense procurement cycles shape bargaining power and margins.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore AeroVironment’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Component Concentration

AeroVironment depends on a few specialized vendors for high-performance sensors, advanced optics, and proprietary carbon-fiber—suppliers that in 2025 controlled roughly 60–75% of available aerospace‑grade capacity, giving them pricing and delivery leverage.

Defense-grade specs and ITAR security mean only 2–5 suppliers can meet contracts, so supply shocks tied to 2024–25 geopolitical conflicts raised lead times by ~30% and pushed input-cost inflation ~8–12%.

Semiconductor and Microelectronics Dependency

The Switchblade’s AI and autonomy need high-end semiconductors and microelectronics, markets where chipmakers hold leverage; commercial firms and prime defense contractors bid against AeroVironment, raising component prices. In 2024 global chip shortages raised defense part lead times to 24+ weeks and lifted prices by ~12% for advanced nodes, squeezing AeroVironment’s margins and delaying robotic-production schedules. Supply-chain disruptions thus raise costs and time-to-delivery.

Niche Propulsion and Battery Technology

As demand for longer endurance and quieter UAS grows, AeroVironment relies on niche battery and electric-motor makers whose IP drives supplier power; top battery chemists hold patents enabling >20% better energy density versus legacy cells (2024 data).

Switching costs are high: redesigning airframes and certification can add 6–12 months and $2–5M per platform, so AeroVironment favors multi-year contracts to secure limited high-energy-density components and stabilize COGS.

Labor Market for Specialized Engineering

The supply of aerospace engineers and cleared software developers is a critical input for AeroVironment; US Department of Labor data shows a 6% shortage in aerospace roles vs 2024 hiring needs, tightening availability.

Established defense firms and deep‑tech startups heavily compete, pushing median total compensation for cleared engineers to about $180k–$210k in 2024, up ~8% year‑over‑year.

That scarcity acts as supplier-side pressure: AeroVironment must pay premiums, expedite hiring, and invest in retention to sustain its innovation pipeline and bid competitively on contracts.

- Cleared talent shortfall ~6% (2024)

- Median comp $180k–$210k (2024)

- Comp growth ~8% YoY

- Premiums drive higher operating and bid costs

Strict Compliance and Certification Requirements

Suppliers must meet strict DoD cybersecurity (CMMC 2.0) and AS9100 quality standards, shrinking eligible vendors to a small domestic cohort—CMMC covers over 300,000 Defense Industrial Base firms but only a fraction hold level 2+ certs.

This barrier stops AeroVironment from shifting to lower-cost international suppliers that lack US security protocols, locking procurement to certified domestic vendors.

As a result, certified suppliers sustain higher prices; for example, premium for compliant avionics parts can run 10–25% above noncompliant sources, squeezing AeroVironment’s margin.

- DoD CMMC 2.0 restricts vendor pool

- AS9100 raises entry costs

- 10–25% premium for compliant parts

- Switching to foreign suppliers largely infeasible

Supplier Power Peaks: Concentration, Long Leads, Premiums & Talent Costs Bite Margins

Suppliers hold strong leverage: 60–75% aerospace‑grade capacity concentration (2025), 2–5 qualified vendors per critical item, 24+ week lead times for advanced chips (2024), and compliant-part premiums of 10–25%; cleared talent shortfall ~6% with median comp $180k–$210k (2024), raising COGS and bid costs.

| Metric | Value (year) |

|---|---|

| Capacity concentration | 60–75% (2025) |

| Qualified suppliers per critical part | 2–5 |

| Chip lead times | 24+ weeks (2024) |

| Compliant-part premium | 10–25% |

| Cleared talent shortfall | ~6% (2024) |

| Median cleared engineer comp | $180k–$210k (2024) |

What is included in the product

Tailored exclusively for AeroVironment, this Porter's Five Forces overview uncovers key drivers of competition, supplier and buyer influence, entry barriers, substitutes, and emerging threats, with strategic insights to inform investor materials and executive decision-making.

One-sheet Porter’s Five Forces for AeroVironment—quickly spot supplier, buyer, and competitive pressures to guide UAV strategy and investment decisions.

Customers Bargaining Power

Monopsony Power of the US Government

The U.S. Department of Defense is AeroVironment’s dominant customer, creating monopsony power that shapes contract terms, pricing, and specs; in 2024 about 70% of revenue tied to major DoD programs concentrated across a few awards.

Because revenue is concentrated, the DoD can delay orders or reallocate funds during budget cycles—FY2024 shifting priorities cut some programs by mid-single digits—forcing AeroVironment to absorb timing and cash-flow risk.

This dynamic compels AeroVironment to align R&D and production to Pentagon modernization roadmaps, keeping product roadmaps and staffing flexible to meet multi-year procurement profiles.

Rigorous Procurement and Auditing Processes

Government customers use complex bidding and fixed-price or cost-plus contracts that squeeze AeroVironment’s margins—U.S. defense prime contracts saw average gross margins near 8–12% in 2024, constraining suppliers.

They retain audit rights and require cost transparency under FAR rules, reducing the company’s ability to pass on price rises or obscure overheads; audit findings can trigger price adjustments or penalties.

Bureaucratic acquisition cycles (typical 12–36 months for U.S. DoD programs) let customers shape requirements from design through deployment, increasing customer leverage over specs, timelines, and pricing.

Foreign Military Sales Restrictions

Allied governments are a growing buyer group but purchases often need U.S. State Department approval, which caps direct bargaining; in 2024 the U.S. approved $20.3 billion in foreign military sales, showing scale and control. These buyers use strategic leverage to push for discounted support, training, and offsets—contracts often include multi-year sustainment that can be 15–25% of deal value. Still, AeroVironment’s combat-proven tactical missiles, with >1,000 systems delivered by 2025, keep pricing power and limit concessions.

Shift Toward Open Architecture Requirements

- Customers: stronger leverage via open standards

- Impact: lower vendor lock-in, higher component churn

- Financials: potential short-term margin pressure, long-term service revenue gain

- Action: adopt MOSA-style interfaces, certify third-party integrations

Performance Based Contracting Trends

Performance-based logistics (customers pay for uptime) is rising in defense and commercial robotics; 2024 DOD guidance tied 30% of sustainment contracts to availability metrics, shifting repair and reliability risk to AeroVironment.

That shift increases customer bargaining power: buyers can insist on higher mean-time-between-failure targets and impose penalties—reducing AVAV’s margin if mission-readiness benchmarks (often 95%+ availability) aren’t met.

Contracts with availability pricing force AeroVironment to invest in remote diagnostics, spare pools, and predictive maintenance, raising capex and O&M while making revenue more recurring but contractually conditional.

- 2024: DOD availability-linked contracts ~30%

- Typical uptime targets ≥95%

- Penalties cut revenue if readiness shortfall occurs

- Shifts maintenance risk and increases capex/O&M

DoD monopsony drives pricing, uptime-linked sustainment shifts repair/capex risk to AVAV

The DoD is AeroVironment’s dominant buyer (~70% revenue in 2024), giving monopsony leverage to set specs, timing, and pricing; FY2024 budget shifts trimmed some programs mid-single digits and extended payment timing. Allied FMS purchases ($20.3B US approvals in 2024) add scale but need US approvals and push for discounts, sustainment, and offsets. Rising open-architecture and availability-based contracts (≈30% sustainment tied to uptime, targets ≥95% in 2024) increase buyer bargaining power and shift repair/capex risk to AVAV.

| Metric | 2024/2025 value |

|---|---|

| Revenue share from DoD | ≈70% |

| US FMS approvals (2024) | $20.3B |

| Sustainment contracts availability-linked | ≈30% |

| Typical uptime targets | ≥95% |

| Delivered systems by 2025 | >1,000 |

Same Document Delivered

AeroVironment Porter's Five Forces Analysis

This preview shows the exact AeroVironment Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or edits; the file is fully formatted, professionally written, and ready for immediate download and use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

AeroVironment faces intense rivalry from larger defense contractors, specialized UAV firms, and rapid tech entrants, while supplier specialization and defense procurement cycles shape bargaining power and margins.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore AeroVironment’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Component Concentration

AeroVironment depends on a few specialized vendors for high-performance sensors, advanced optics, and proprietary carbon-fiber—suppliers that in 2025 controlled roughly 60–75% of available aerospace‑grade capacity, giving them pricing and delivery leverage.

Defense-grade specs and ITAR security mean only 2–5 suppliers can meet contracts, so supply shocks tied to 2024–25 geopolitical conflicts raised lead times by ~30% and pushed input-cost inflation ~8–12%.

Semiconductor and Microelectronics Dependency

The Switchblade’s AI and autonomy need high-end semiconductors and microelectronics, markets where chipmakers hold leverage; commercial firms and prime defense contractors bid against AeroVironment, raising component prices. In 2024 global chip shortages raised defense part lead times to 24+ weeks and lifted prices by ~12% for advanced nodes, squeezing AeroVironment’s margins and delaying robotic-production schedules. Supply-chain disruptions thus raise costs and time-to-delivery.

Niche Propulsion and Battery Technology

As demand for longer endurance and quieter UAS grows, AeroVironment relies on niche battery and electric-motor makers whose IP drives supplier power; top battery chemists hold patents enabling >20% better energy density versus legacy cells (2024 data).

Switching costs are high: redesigning airframes and certification can add 6–12 months and $2–5M per platform, so AeroVironment favors multi-year contracts to secure limited high-energy-density components and stabilize COGS.

Labor Market for Specialized Engineering

The supply of aerospace engineers and cleared software developers is a critical input for AeroVironment; US Department of Labor data shows a 6% shortage in aerospace roles vs 2024 hiring needs, tightening availability.

Established defense firms and deep‑tech startups heavily compete, pushing median total compensation for cleared engineers to about $180k–$210k in 2024, up ~8% year‑over‑year.

That scarcity acts as supplier-side pressure: AeroVironment must pay premiums, expedite hiring, and invest in retention to sustain its innovation pipeline and bid competitively on contracts.

- Cleared talent shortfall ~6% (2024)

- Median comp $180k–$210k (2024)

- Comp growth ~8% YoY

- Premiums drive higher operating and bid costs

Strict Compliance and Certification Requirements

Suppliers must meet strict DoD cybersecurity (CMMC 2.0) and AS9100 quality standards, shrinking eligible vendors to a small domestic cohort—CMMC covers over 300,000 Defense Industrial Base firms but only a fraction hold level 2+ certs.

This barrier stops AeroVironment from shifting to lower-cost international suppliers that lack US security protocols, locking procurement to certified domestic vendors.

As a result, certified suppliers sustain higher prices; for example, premium for compliant avionics parts can run 10–25% above noncompliant sources, squeezing AeroVironment’s margin.

- DoD CMMC 2.0 restricts vendor pool

- AS9100 raises entry costs

- 10–25% premium for compliant parts

- Switching to foreign suppliers largely infeasible

Supplier Power Peaks: Concentration, Long Leads, Premiums & Talent Costs Bite Margins

Suppliers hold strong leverage: 60–75% aerospace‑grade capacity concentration (2025), 2–5 qualified vendors per critical item, 24+ week lead times for advanced chips (2024), and compliant-part premiums of 10–25%; cleared talent shortfall ~6% with median comp $180k–$210k (2024), raising COGS and bid costs.

| Metric | Value (year) |

|---|---|

| Capacity concentration | 60–75% (2025) |

| Qualified suppliers per critical part | 2–5 |

| Chip lead times | 24+ weeks (2024) |

| Compliant-part premium | 10–25% |

| Cleared talent shortfall | ~6% (2024) |

| Median cleared engineer comp | $180k–$210k (2024) |

What is included in the product

Tailored exclusively for AeroVironment, this Porter's Five Forces overview uncovers key drivers of competition, supplier and buyer influence, entry barriers, substitutes, and emerging threats, with strategic insights to inform investor materials and executive decision-making.

One-sheet Porter’s Five Forces for AeroVironment—quickly spot supplier, buyer, and competitive pressures to guide UAV strategy and investment decisions.

Customers Bargaining Power

Monopsony Power of the US Government

The U.S. Department of Defense is AeroVironment’s dominant customer, creating monopsony power that shapes contract terms, pricing, and specs; in 2024 about 70% of revenue tied to major DoD programs concentrated across a few awards.

Because revenue is concentrated, the DoD can delay orders or reallocate funds during budget cycles—FY2024 shifting priorities cut some programs by mid-single digits—forcing AeroVironment to absorb timing and cash-flow risk.

This dynamic compels AeroVironment to align R&D and production to Pentagon modernization roadmaps, keeping product roadmaps and staffing flexible to meet multi-year procurement profiles.

Rigorous Procurement and Auditing Processes

Government customers use complex bidding and fixed-price or cost-plus contracts that squeeze AeroVironment’s margins—U.S. defense prime contracts saw average gross margins near 8–12% in 2024, constraining suppliers.

They retain audit rights and require cost transparency under FAR rules, reducing the company’s ability to pass on price rises or obscure overheads; audit findings can trigger price adjustments or penalties.

Bureaucratic acquisition cycles (typical 12–36 months for U.S. DoD programs) let customers shape requirements from design through deployment, increasing customer leverage over specs, timelines, and pricing.

Foreign Military Sales Restrictions

Allied governments are a growing buyer group but purchases often need U.S. State Department approval, which caps direct bargaining; in 2024 the U.S. approved $20.3 billion in foreign military sales, showing scale and control. These buyers use strategic leverage to push for discounted support, training, and offsets—contracts often include multi-year sustainment that can be 15–25% of deal value. Still, AeroVironment’s combat-proven tactical missiles, with >1,000 systems delivered by 2025, keep pricing power and limit concessions.

Shift Toward Open Architecture Requirements

- Customers: stronger leverage via open standards

- Impact: lower vendor lock-in, higher component churn

- Financials: potential short-term margin pressure, long-term service revenue gain

- Action: adopt MOSA-style interfaces, certify third-party integrations

Performance Based Contracting Trends

Performance-based logistics (customers pay for uptime) is rising in defense and commercial robotics; 2024 DOD guidance tied 30% of sustainment contracts to availability metrics, shifting repair and reliability risk to AeroVironment.

That shift increases customer bargaining power: buyers can insist on higher mean-time-between-failure targets and impose penalties—reducing AVAV’s margin if mission-readiness benchmarks (often 95%+ availability) aren’t met.

Contracts with availability pricing force AeroVironment to invest in remote diagnostics, spare pools, and predictive maintenance, raising capex and O&M while making revenue more recurring but contractually conditional.

- 2024: DOD availability-linked contracts ~30%

- Typical uptime targets ≥95%

- Penalties cut revenue if readiness shortfall occurs

- Shifts maintenance risk and increases capex/O&M

DoD monopsony drives pricing, uptime-linked sustainment shifts repair/capex risk to AVAV

The DoD is AeroVironment’s dominant buyer (~70% revenue in 2024), giving monopsony leverage to set specs, timing, and pricing; FY2024 budget shifts trimmed some programs mid-single digits and extended payment timing. Allied FMS purchases ($20.3B US approvals in 2024) add scale but need US approvals and push for discounts, sustainment, and offsets. Rising open-architecture and availability-based contracts (≈30% sustainment tied to uptime, targets ≥95% in 2024) increase buyer bargaining power and shift repair/capex risk to AVAV.

| Metric | 2024/2025 value |

|---|---|

| Revenue share from DoD | ≈70% |

| US FMS approvals (2024) | $20.3B |

| Sustainment contracts availability-linked | ≈30% |

| Typical uptime targets | ≥95% |

| Delivered systems by 2025 | >1,000 |

Same Document Delivered

AeroVironment Porter's Five Forces Analysis

This preview shows the exact AeroVironment Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or edits; the file is fully formatted, professionally written, and ready for immediate download and use.