Axon Enterprise Boston Consulting Group Matrix

Actionable Strategy Starts Here

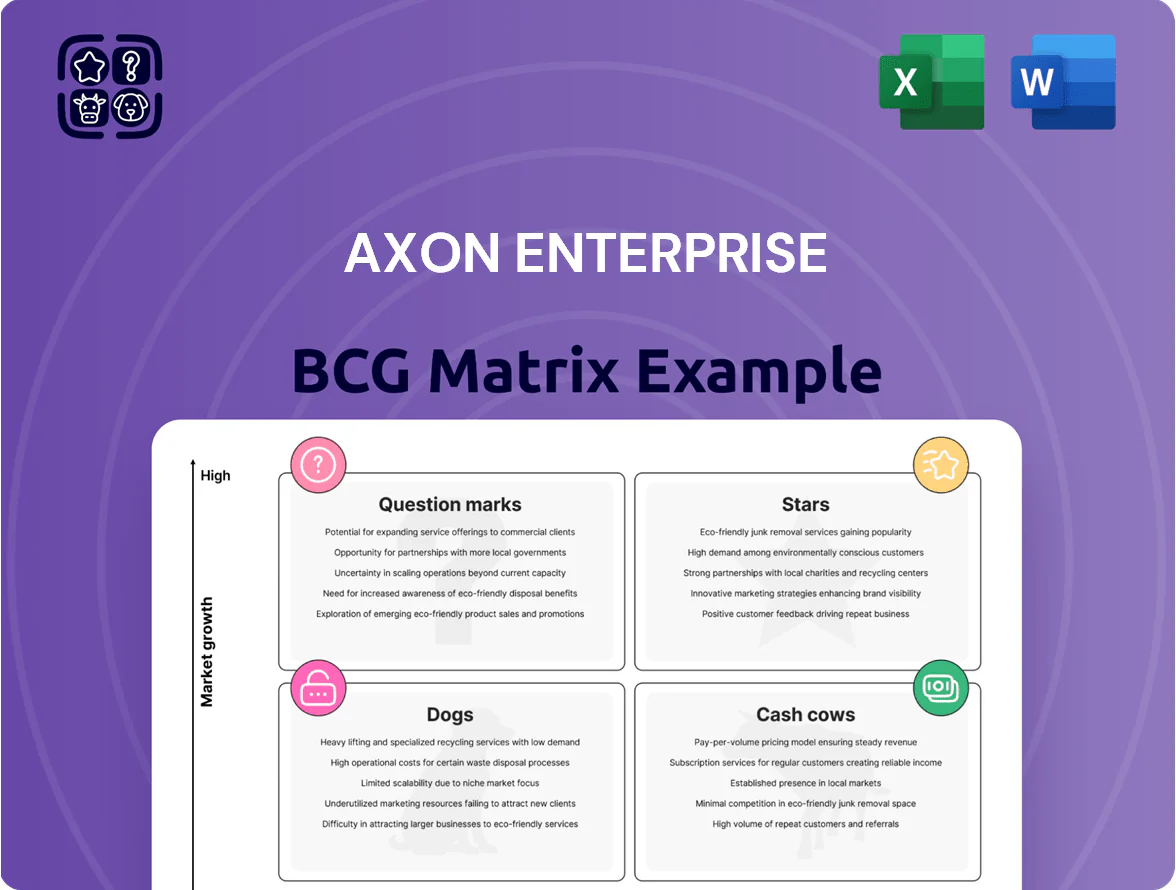

Axon Enterprise’s brief BCG Matrix preview highlights its high-growth body-camera and software segments as Stars, stable TASER legacy units as Cash Cows, and emerging services as Question Marks needing capital for scale; a few minor hardware lines appear as Dogs. This snapshot points to strategic priorities—invest in cloud and AI-enabled evidence management, milk TASER cash flow to fund innovation, and reassess low-return hardware. Dive deeper into this company’s BCG Matrix and gain a clear view of where its products stand—Stars, Cash Cows, Dogs, or Question Marks. Purchase the full version for a complete breakdown and strategic insights you can act on.

Stars

Axon Cloud Services and Evidence.com

As of late 2025, Axon Cloud (Evidence.com) is Axon Enterprise’s star: high market share in digital evidence management with estimated SaaS ARR of about $820 million in FY2025, up ~22% year-over-year, driving most company growth.

The segment benefits from a global shift to public-safety SaaS, yielding gross margins near 70% and recurring revenue stability; cloud bookings rose ~28% in 2025.

Axon’s continuous integration of AI analytics (real-time tagging, redaction) keeps it ahead as the global digital evidence market projects a 14% CAGR through 2030, expanding addressable market.

Axon Body 4 and Next-Gen Wearables

Axon’s Body 4 and next-gen wearables sit in the Stars quadrant: global bodycam market set to reach $7.2B by 2026 (MarketsandMarkets), and Axon held ~55% US market share in 2024 per company filings, driving strong unit growth.

High demand for real-time comms and upgraded sensors pushes Axon to spend ~15% of revenue on R&D and ~10% on sales/marketing in FY2024, fitting a capital‑intensive Star profile.

Fleet 3 and In-Car Video Systems

Axon Fleet 3, combining in-car video with AI ALPR, holds about 40% of US patrol vehicle installs and drove Axon’s 2025 wearable & vehicle segment revenue growth of ~28% year-over-year, per company filings; agencies are replacing legacy kits with cloud-connected systems at a CAGR near 15% through 2028. Still, maintaining this high-margin position needs continuous R&D and capex to fend off emerging competitors and protect recurring software revenue.

Draft One AI Transcription

Draft One AI Transcription is a Star: since its 2024 launch it captured ~22% of US mid-to-large police agency report automation within 12 months by converting body-cam audio to draft narratives, cutting report time by ~60% and saving agencies ~$1.2M annual labor per 100-officer force.

Its use of generative AI aligns with Axon’s high-growth ecosystem, with projected ARR contribution of $55–75M by end-2025 as adoption expands across 600+ agencies, keeping it in the high market growth, high market share quadrant.

- Launched 2024; ~22% market share (mid-large agencies)

- Reduces report time ~60%; ~$1.2M saved per 100 officers

- 600+ agency adopters; ARR est. $55–75M by 2025

International Expansion Units

Axon’s push into Tier 1 Europe and Asia-Pacific produced double-digit ARR growth and ~18% regional market-share gains by Q4 2025, marking these segments as Stars in the BCG matrix because rapid growth and rising share need heavy local investment.

These markets demand significant sales, service, and compliance capex—Axon spent $220M on international expansion in FY2024–25—yet projected revenue upside to $1.2B by 2028 justifies the spend.

- Double-digit ARR growth (2025)

- ~18% regional market-share gain (Q4 2025)

- $220M expansion capex (FY2024–25)

- $1.2B revenue potential by 2028

Axon’s Growth Engines: Cloud ARR $820M, Bodycams 55% US, Draft One AI $55–75M

Axon’s Stars: Axon Cloud (Evidence.com) ARR ~$820M (FY2025), ~70% gross margin; Body 4/wearables ~55% US share (2024), fleet installs ~40% US; Draft One AI ~22% mid-large agency share, ARR $55–75M (2025); Intl expansion spent $220M (FY2024–25), ARR upside $1.2B by 2028.

| Asset | Key metric | 2025 figure |

|---|---|---|

| Axon Cloud | ARR | $820M |

| Bodycams/Fleet | US share | 55%/40% |

| Draft One AI | ARR | $55–75M |

| Intl | Expansion spend | $220M |

What is included in the product

BCG Matrix analysis of Axon’s products with strategic recommendations for Stars, Cash Cows, Question Marks, and Dogs.

One-page Axon Enterprise BCG Matrix positioning business units by growth and market share for quick executive decisions.

Cash Cows

TASER 10 Platform

The TASER 10 platform dominates the conducted-energy device market with ~60% US law-enforcement share (2024), facing minimal direct competition, and has reached maturity. It drives strong cash flow: Axon reported 2024 device revenue of $1.2B and gross margins >55%, plus recurring cartridge program revenue of ~$420M. With a stable non-lethal weapons market, Axon can milk TASER 10 to fund higher-risk R&D and M&A.

Legacy TASER Cartridges and Accessories

Sales of legacy TASER cartridges and accessories generate steady, high-margin cash: Axon reported consumables and accessories revenue of about $380 million in FY2024, driven by an installed base of hundreds of thousands of officers and >60% gross margins, making this a low-growth, predictable cash cow.

Axon Evidence Legacy Storage Plans

Axon Evidence legacy storage plans act as a stable Cash Cow: as of FY2024 Axon reported recurring cloud revenue exceeding $200M, with legacy storage contracts delivering high gross margins and low churn while newer AI features drive growth.

Professional Services and Training

Axon’s Professional Services and Training are cash cows: TASER certification and software-implementation training generated steady, recurring revenue—Axon reported services revenue of $226 million in FY2024 (about 14% of total revenue), reflecting mature, policy-driven demand that’s resilient across cycles.

Infrastructure is in place, so marginal costs stay low and gross margins for services exceed product margins; predictable contracts and agency mandates make scaling profitable with minimal incremental investment.

- Services revenue: $226M in FY2024

- ~14% of Axon total revenue (2024)

- High gross margin vs hardware

- Policy-mandated demand stabilizes cash flow

Axon Signal Vehicle Integration

Axon Signal Vehicle Integration — which auto-activates in-car cameras on vehicle triggers — is a mature, high-penetration product in North America, installed in an estimated 65–75% of US police fleet deployments by 2025 and generating steady recurring revenue for Axon Enterprise (AXON) via hardware sales and cloud storage fees.

As a standard fleet feature, it needs little promotion, delivers predictable margins (hardware gross margin ~40% in 2024), and increases retention by tying agencies to Axon Evidence cloud and Taser/Body camera ecosystems, reinforcing platform stickiness and lifetime value.

- Market penetration: ~65–75% US fleets (2025)

- Hardware GM: ~40% (2024)

- Drives recurring cloud/storage revenue

- Increases customer retention and ecosystem lock-in

Axon: High‑margin TASER 10 + consumables and recurring cloud drive predictable cash growth

Axon’s TASER 10, consumables, legacy Evidence storage, services, and Signal vehicle integration together generate high-margin, predictable cash: FY2024 device revenue $1.2B, consumables ~$380–420M, services $226M (14% of revenue), cloud recurring >$200M, device GM >55%, consumables GM >60%, vehicle hardware GM ~40%, US fleet penetration 65–75% (2025).

| Line | 2024/2025 |

|---|---|

| TASER 10 revenue | $1.2B (2024) |

| Consumables | $380–420M (2024) |

| Services | $226M (2024) |

| Cloud recurring | >$200M (2024) |

| Device GM | >55% (2024) |

| Consumables GM | >60% (2024) |

| Vehicle penetration | 65–75% US fleets (2025) |

| Vehicle hardware GM | ~40% (2024) |

What You’re Viewing Is Included

Axon Enterprise BCG Matrix

The file you're previewing on this page is the final Axon Enterprise BCG Matrix you'll receive after purchase—no watermarks, no demo content; just a fully formatted, analysis-ready report tailored for strategic clarity and professional presentation.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Actionable Strategy Starts Here

Axon Enterprise’s brief BCG Matrix preview highlights its high-growth body-camera and software segments as Stars, stable TASER legacy units as Cash Cows, and emerging services as Question Marks needing capital for scale; a few minor hardware lines appear as Dogs. This snapshot points to strategic priorities—invest in cloud and AI-enabled evidence management, milk TASER cash flow to fund innovation, and reassess low-return hardware. Dive deeper into this company’s BCG Matrix and gain a clear view of where its products stand—Stars, Cash Cows, Dogs, or Question Marks. Purchase the full version for a complete breakdown and strategic insights you can act on.

Stars

Axon Cloud Services and Evidence.com

As of late 2025, Axon Cloud (Evidence.com) is Axon Enterprise’s star: high market share in digital evidence management with estimated SaaS ARR of about $820 million in FY2025, up ~22% year-over-year, driving most company growth.

The segment benefits from a global shift to public-safety SaaS, yielding gross margins near 70% and recurring revenue stability; cloud bookings rose ~28% in 2025.

Axon’s continuous integration of AI analytics (real-time tagging, redaction) keeps it ahead as the global digital evidence market projects a 14% CAGR through 2030, expanding addressable market.

Axon Body 4 and Next-Gen Wearables

Axon’s Body 4 and next-gen wearables sit in the Stars quadrant: global bodycam market set to reach $7.2B by 2026 (MarketsandMarkets), and Axon held ~55% US market share in 2024 per company filings, driving strong unit growth.

High demand for real-time comms and upgraded sensors pushes Axon to spend ~15% of revenue on R&D and ~10% on sales/marketing in FY2024, fitting a capital‑intensive Star profile.

Fleet 3 and In-Car Video Systems

Axon Fleet 3, combining in-car video with AI ALPR, holds about 40% of US patrol vehicle installs and drove Axon’s 2025 wearable & vehicle segment revenue growth of ~28% year-over-year, per company filings; agencies are replacing legacy kits with cloud-connected systems at a CAGR near 15% through 2028. Still, maintaining this high-margin position needs continuous R&D and capex to fend off emerging competitors and protect recurring software revenue.

Draft One AI Transcription

Draft One AI Transcription is a Star: since its 2024 launch it captured ~22% of US mid-to-large police agency report automation within 12 months by converting body-cam audio to draft narratives, cutting report time by ~60% and saving agencies ~$1.2M annual labor per 100-officer force.

Its use of generative AI aligns with Axon’s high-growth ecosystem, with projected ARR contribution of $55–75M by end-2025 as adoption expands across 600+ agencies, keeping it in the high market growth, high market share quadrant.

- Launched 2024; ~22% market share (mid-large agencies)

- Reduces report time ~60%; ~$1.2M saved per 100 officers

- 600+ agency adopters; ARR est. $55–75M by 2025

International Expansion Units

Axon’s push into Tier 1 Europe and Asia-Pacific produced double-digit ARR growth and ~18% regional market-share gains by Q4 2025, marking these segments as Stars in the BCG matrix because rapid growth and rising share need heavy local investment.

These markets demand significant sales, service, and compliance capex—Axon spent $220M on international expansion in FY2024–25—yet projected revenue upside to $1.2B by 2028 justifies the spend.

- Double-digit ARR growth (2025)

- ~18% regional market-share gain (Q4 2025)

- $220M expansion capex (FY2024–25)

- $1.2B revenue potential by 2028

Axon’s Growth Engines: Cloud ARR $820M, Bodycams 55% US, Draft One AI $55–75M

Axon’s Stars: Axon Cloud (Evidence.com) ARR ~$820M (FY2025), ~70% gross margin; Body 4/wearables ~55% US share (2024), fleet installs ~40% US; Draft One AI ~22% mid-large agency share, ARR $55–75M (2025); Intl expansion spent $220M (FY2024–25), ARR upside $1.2B by 2028.

| Asset | Key metric | 2025 figure |

|---|---|---|

| Axon Cloud | ARR | $820M |

| Bodycams/Fleet | US share | 55%/40% |

| Draft One AI | ARR | $55–75M |

| Intl | Expansion spend | $220M |

What is included in the product

BCG Matrix analysis of Axon’s products with strategic recommendations for Stars, Cash Cows, Question Marks, and Dogs.

One-page Axon Enterprise BCG Matrix positioning business units by growth and market share for quick executive decisions.

Cash Cows

TASER 10 Platform

The TASER 10 platform dominates the conducted-energy device market with ~60% US law-enforcement share (2024), facing minimal direct competition, and has reached maturity. It drives strong cash flow: Axon reported 2024 device revenue of $1.2B and gross margins >55%, plus recurring cartridge program revenue of ~$420M. With a stable non-lethal weapons market, Axon can milk TASER 10 to fund higher-risk R&D and M&A.

Legacy TASER Cartridges and Accessories

Sales of legacy TASER cartridges and accessories generate steady, high-margin cash: Axon reported consumables and accessories revenue of about $380 million in FY2024, driven by an installed base of hundreds of thousands of officers and >60% gross margins, making this a low-growth, predictable cash cow.

Axon Evidence Legacy Storage Plans

Axon Evidence legacy storage plans act as a stable Cash Cow: as of FY2024 Axon reported recurring cloud revenue exceeding $200M, with legacy storage contracts delivering high gross margins and low churn while newer AI features drive growth.

Professional Services and Training

Axon’s Professional Services and Training are cash cows: TASER certification and software-implementation training generated steady, recurring revenue—Axon reported services revenue of $226 million in FY2024 (about 14% of total revenue), reflecting mature, policy-driven demand that’s resilient across cycles.

Infrastructure is in place, so marginal costs stay low and gross margins for services exceed product margins; predictable contracts and agency mandates make scaling profitable with minimal incremental investment.

- Services revenue: $226M in FY2024

- ~14% of Axon total revenue (2024)

- High gross margin vs hardware

- Policy-mandated demand stabilizes cash flow

Axon Signal Vehicle Integration

Axon Signal Vehicle Integration — which auto-activates in-car cameras on vehicle triggers — is a mature, high-penetration product in North America, installed in an estimated 65–75% of US police fleet deployments by 2025 and generating steady recurring revenue for Axon Enterprise (AXON) via hardware sales and cloud storage fees.

As a standard fleet feature, it needs little promotion, delivers predictable margins (hardware gross margin ~40% in 2024), and increases retention by tying agencies to Axon Evidence cloud and Taser/Body camera ecosystems, reinforcing platform stickiness and lifetime value.

- Market penetration: ~65–75% US fleets (2025)

- Hardware GM: ~40% (2024)

- Drives recurring cloud/storage revenue

- Increases customer retention and ecosystem lock-in

Axon: High‑margin TASER 10 + consumables and recurring cloud drive predictable cash growth

Axon’s TASER 10, consumables, legacy Evidence storage, services, and Signal vehicle integration together generate high-margin, predictable cash: FY2024 device revenue $1.2B, consumables ~$380–420M, services $226M (14% of revenue), cloud recurring >$200M, device GM >55%, consumables GM >60%, vehicle hardware GM ~40%, US fleet penetration 65–75% (2025).

| Line | 2024/2025 |

|---|---|

| TASER 10 revenue | $1.2B (2024) |

| Consumables | $380–420M (2024) |

| Services | $226M (2024) |

| Cloud recurring | >$200M (2024) |

| Device GM | >55% (2024) |

| Consumables GM | >60% (2024) |

| Vehicle penetration | 65–75% US fleets (2025) |

| Vehicle hardware GM | ~40% (2024) |

What You’re Viewing Is Included

Axon Enterprise BCG Matrix

The file you're previewing on this page is the final Axon Enterprise BCG Matrix you'll receive after purchase—no watermarks, no demo content; just a fully formatted, analysis-ready report tailored for strategic clarity and professional presentation.