Axon Enterprise Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

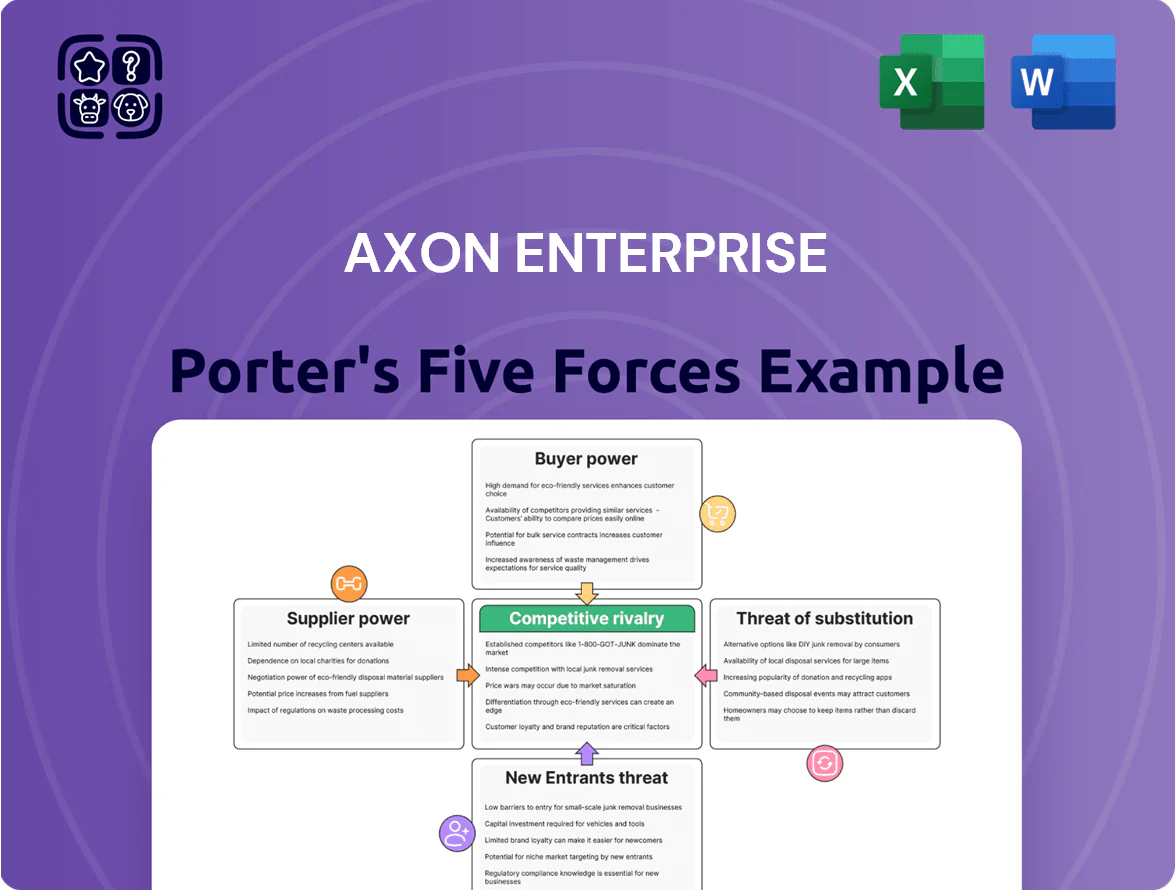

Axon Enterprise faces strong buyer scrutiny, moderate supplier leverage, and regulatory-plus-tech-driven substitution risks that shape its defensive moat and growth runway—while scale and recurring contracts temper newcomer threats.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Axon Enterprise’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Component Dependency

Axon depends on specialized sensors, high-performance optics, and proprietary circuitry for TASERs and body cameras, creating supplier power over key components; in 2024 Axon reported gross margin pressure from component costs, with R&D and component spend contributing to 33% of COGS in FY2024.

Software and Cloud Infrastructure Costs

Axon’s Evidence.com runs largely on Microsoft Azure, raising supplier power as Azure, AWS, and Google Cloud control >60% of global cloud IaaS/SaaS market (Gartner 2024) and set pricing/terms; migrating Axon’s sensitive public-safety data would cost hundreds of millions and disrupt contracts—Azure enterprise egress and rehosting fees plus compliance work are material.

Raw Material Price Volatility

Axon’s hardware manufacturing uses metals, plastics and lithium for batteries, so it is exposed to commodity swings—lithium carbonate jumped ~45% in 2023–24 and copper rose ~30% YTD 2025, pressuring COGS. Despite scale (2024 revenue $1.5B in devices and software-linked hardware), Axon is a price taker for base materials. Semiconductor and battery supply disruptions in 2021–24 caused multi-week delays, raising production costs and squeezing gross margin by ~150–250 bps in peak months.

Sole-Source Proprietary Inputs

Suppliers holding patents on advanced TASER tech or AI camera components can gain outsized leverage if their tech becomes an industry standard Axon lacks; in 2025 third-party IP disputes drove 12% higher procurement costs for similar hardware in public-safety supply chains.

Axon reduces this risk through vertical integration and R&D—Axon reported R&D spend of $163.7M in FY2024, up 18% year-over-year—so it builds alternate suppliers and in-house IP to limit supplier bargaining power.

- Third-party IP can raise costs ~12%

- Industry standardization shifts leverage to IP holders

- Axon R&D = $163.7M in FY2024

- Vertical integration and internal IP lessen supplier power

Labor Market for Specialized Engineering

The supply of senior software engineers, AI researchers, and hardware designers is a key human-capital supplier for Axon Enterprise and carries strong bargaining power.

By late 2025, U.S. tech median total compensation for senior ML engineers rose ~18% year-over-year to ~$300k and defense-grade cloud specialists command premiums 20–35% above market rates, tightening Axon’s hiring costs and time-to-fill.

Higher wages, low unemployment in specialized roles (sub-2% in AI fields per 2024 NSF estimates), and demand from Big Tech and defense contractors increase turnover risk and supplier leverage.

- Senior ML pay ≈ $300k (2025 median)

- Defense/cloud premium 20–35%

- AI role unemployment <2% (2024 NSF)

- Hiring costs and time-to-fill up, raising R&D margins pressure

Axon faces rising supplier power: components, cloud, lithium & top ML talent squeeze margins

Axon faces moderate-to-high supplier power from specialized components, cloud providers, commodities, IP holders, and scarce engineering talent; FY2024 R&D $163.7M, device/software revenue ~$1.5B, component/COS share 33%, lithium ↑45% (2023–24), cloud market >60% (Gartner 2024), senior ML pay ≈$300k (2025).

| Metric | Value |

|---|---|

| R&D FY2024 | $163.7M |

| Device/software rev | $1.5B |

| COGS from components/R&D | 33% |

| Lithium price change | +45% (2023–24) |

| Cloud IaaS share | >60% (Gartner 2024) |

| Senior ML median pay | ≈$300k (2025) |

What is included in the product

Comprehensive Porter's Five Forces for Axon Enterprise, revealing competitive intensity, buyer/supplier power, substitution risks, and entry barriers with strategic insights and industry-backed commentary.

Axon Enterprise Porter's Five Forces—one-sheet clarity highlighting competitive threats and bargaining power so executives can act fast to mitigate risk and prioritize strategic investments.

Customers Bargaining Power

High Switching Costs and Ecosystem Lock-in

Once a law enforcement agency adopts Axon’s ecosystem—Evidence.com cloud, Tasers, and integrated body cameras—the switching cost is high: 2024 Axon reported ~224,000 connected devices and over 6.2 petabytes of evidence stored, making data migration and validation expensive and slow.

Officer retraining and replacing hardware (Axon’s average body-cam unit cost ~$700 in 2024) add capital and operational burden, creating sticky demand and lowering buyer bargaining power.

This lock-in lets Axon keep pricing power—despite public-sector procurement rules—reflected in 2024 gross margin of ~64% and recurring subscription revenue rising to 48% of total revenue.

Fragmented Customer Base

The customer base is highly fragmented—thousands of local, state, and federal agencies buy Axon Enterprise products, so no single buyer dominates; in 2024 Axon reported over 18,000 public safety agency customers. While large agencies (for example NYPD, which spent roughly $25–40m annually on body cameras and TASERs in major procurement cycles) hold some leverage, most agencies lack volume to demand steep discounts. Fragmentation prevents coordinated buyer pressure across the industry.

Budgetary Constraints and Procurement Cycles

Public safety agencies run on tight taxpayer budgets and long RFP cycles, letting buyers delay purchases or demand multi-year price freezes—e.g., US state/local CAPEX fell 3.1% in 2024, raising procurement caution. During downturns agencies push for cost predictability, upping buyer leverage. Axon’s shift to multi-year subscription bundles (over 60% recurring revenue in FY2024) reduces that leverage by locking in predictable cash flow and extending contract terms.

Product Essentiality and Mandates

Increasing federal and state mandates for body-worn cameras (BWC) and transparency—California AB 748 updates and DOJ funding boosts in 2024—have turned Axon’s cameras and evidence cloud into operational must-haves, shrinking buyer exit options.

When use is legally required, agencies trade price for compliance; Axon’s ~50–60% US BWC market share in 2024 makes it the perceived gold standard, strengthening customer bargaining disadvantage.

Emphasis on Total Cost of Ownership

Axon’s pricing power: 224K devices, 6.2PB, ~60% BWC share & 64% margins

Customers have limited bargaining power: high switching costs (224,000 connected devices, 6.2 PB stored in 2024) plus Axon’s ~50–60% US BWC share and 64% gross margin let Axon keep pricing power despite fragmented agencies (18,000+ customers) and budget pressure (state/local CAPEX -3.1% in 2024); mandates and DOJ funding raise demand and reduce exit options.

| Metric | 2024 Value |

|---|---|

| Connected devices | ~224,000 |

| Evidence stored | 6.2 PB |

| US BWC share | 50–60% |

| Public safety customers | 18,000+ |

| Gross margin | ~64% |

| Recurring revenue | 48–60% (FY2024) |

| State/local CAPEX change | -3.1% |

What You See Is What You Get

Axon Enterprise Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Axon Enterprise you'll receive after purchase—no placeholders or mockups, fully formatted and ready for immediate download and use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Axon Enterprise faces strong buyer scrutiny, moderate supplier leverage, and regulatory-plus-tech-driven substitution risks that shape its defensive moat and growth runway—while scale and recurring contracts temper newcomer threats.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Axon Enterprise’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Component Dependency

Axon depends on specialized sensors, high-performance optics, and proprietary circuitry for TASERs and body cameras, creating supplier power over key components; in 2024 Axon reported gross margin pressure from component costs, with R&D and component spend contributing to 33% of COGS in FY2024.

Software and Cloud Infrastructure Costs

Axon’s Evidence.com runs largely on Microsoft Azure, raising supplier power as Azure, AWS, and Google Cloud control >60% of global cloud IaaS/SaaS market (Gartner 2024) and set pricing/terms; migrating Axon’s sensitive public-safety data would cost hundreds of millions and disrupt contracts—Azure enterprise egress and rehosting fees plus compliance work are material.

Raw Material Price Volatility

Axon’s hardware manufacturing uses metals, plastics and lithium for batteries, so it is exposed to commodity swings—lithium carbonate jumped ~45% in 2023–24 and copper rose ~30% YTD 2025, pressuring COGS. Despite scale (2024 revenue $1.5B in devices and software-linked hardware), Axon is a price taker for base materials. Semiconductor and battery supply disruptions in 2021–24 caused multi-week delays, raising production costs and squeezing gross margin by ~150–250 bps in peak months.

Sole-Source Proprietary Inputs

Suppliers holding patents on advanced TASER tech or AI camera components can gain outsized leverage if their tech becomes an industry standard Axon lacks; in 2025 third-party IP disputes drove 12% higher procurement costs for similar hardware in public-safety supply chains.

Axon reduces this risk through vertical integration and R&D—Axon reported R&D spend of $163.7M in FY2024, up 18% year-over-year—so it builds alternate suppliers and in-house IP to limit supplier bargaining power.

- Third-party IP can raise costs ~12%

- Industry standardization shifts leverage to IP holders

- Axon R&D = $163.7M in FY2024

- Vertical integration and internal IP lessen supplier power

Labor Market for Specialized Engineering

The supply of senior software engineers, AI researchers, and hardware designers is a key human-capital supplier for Axon Enterprise and carries strong bargaining power.

By late 2025, U.S. tech median total compensation for senior ML engineers rose ~18% year-over-year to ~$300k and defense-grade cloud specialists command premiums 20–35% above market rates, tightening Axon’s hiring costs and time-to-fill.

Higher wages, low unemployment in specialized roles (sub-2% in AI fields per 2024 NSF estimates), and demand from Big Tech and defense contractors increase turnover risk and supplier leverage.

- Senior ML pay ≈ $300k (2025 median)

- Defense/cloud premium 20–35%

- AI role unemployment <2% (2024 NSF)

- Hiring costs and time-to-fill up, raising R&D margins pressure

Axon faces rising supplier power: components, cloud, lithium & top ML talent squeeze margins

Axon faces moderate-to-high supplier power from specialized components, cloud providers, commodities, IP holders, and scarce engineering talent; FY2024 R&D $163.7M, device/software revenue ~$1.5B, component/COS share 33%, lithium ↑45% (2023–24), cloud market >60% (Gartner 2024), senior ML pay ≈$300k (2025).

| Metric | Value |

|---|---|

| R&D FY2024 | $163.7M |

| Device/software rev | $1.5B |

| COGS from components/R&D | 33% |

| Lithium price change | +45% (2023–24) |

| Cloud IaaS share | >60% (Gartner 2024) |

| Senior ML median pay | ≈$300k (2025) |

What is included in the product

Comprehensive Porter's Five Forces for Axon Enterprise, revealing competitive intensity, buyer/supplier power, substitution risks, and entry barriers with strategic insights and industry-backed commentary.

Axon Enterprise Porter's Five Forces—one-sheet clarity highlighting competitive threats and bargaining power so executives can act fast to mitigate risk and prioritize strategic investments.

Customers Bargaining Power

High Switching Costs and Ecosystem Lock-in

Once a law enforcement agency adopts Axon’s ecosystem—Evidence.com cloud, Tasers, and integrated body cameras—the switching cost is high: 2024 Axon reported ~224,000 connected devices and over 6.2 petabytes of evidence stored, making data migration and validation expensive and slow.

Officer retraining and replacing hardware (Axon’s average body-cam unit cost ~$700 in 2024) add capital and operational burden, creating sticky demand and lowering buyer bargaining power.

This lock-in lets Axon keep pricing power—despite public-sector procurement rules—reflected in 2024 gross margin of ~64% and recurring subscription revenue rising to 48% of total revenue.

Fragmented Customer Base

The customer base is highly fragmented—thousands of local, state, and federal agencies buy Axon Enterprise products, so no single buyer dominates; in 2024 Axon reported over 18,000 public safety agency customers. While large agencies (for example NYPD, which spent roughly $25–40m annually on body cameras and TASERs in major procurement cycles) hold some leverage, most agencies lack volume to demand steep discounts. Fragmentation prevents coordinated buyer pressure across the industry.

Budgetary Constraints and Procurement Cycles

Public safety agencies run on tight taxpayer budgets and long RFP cycles, letting buyers delay purchases or demand multi-year price freezes—e.g., US state/local CAPEX fell 3.1% in 2024, raising procurement caution. During downturns agencies push for cost predictability, upping buyer leverage. Axon’s shift to multi-year subscription bundles (over 60% recurring revenue in FY2024) reduces that leverage by locking in predictable cash flow and extending contract terms.

Product Essentiality and Mandates

Increasing federal and state mandates for body-worn cameras (BWC) and transparency—California AB 748 updates and DOJ funding boosts in 2024—have turned Axon’s cameras and evidence cloud into operational must-haves, shrinking buyer exit options.

When use is legally required, agencies trade price for compliance; Axon’s ~50–60% US BWC market share in 2024 makes it the perceived gold standard, strengthening customer bargaining disadvantage.

Emphasis on Total Cost of Ownership

Axon’s pricing power: 224K devices, 6.2PB, ~60% BWC share & 64% margins

Customers have limited bargaining power: high switching costs (224,000 connected devices, 6.2 PB stored in 2024) plus Axon’s ~50–60% US BWC share and 64% gross margin let Axon keep pricing power despite fragmented agencies (18,000+ customers) and budget pressure (state/local CAPEX -3.1% in 2024); mandates and DOJ funding raise demand and reduce exit options.

| Metric | 2024 Value |

|---|---|

| Connected devices | ~224,000 |

| Evidence stored | 6.2 PB |

| US BWC share | 50–60% |

| Public safety customers | 18,000+ |

| Gross margin | ~64% |

| Recurring revenue | 48–60% (FY2024) |

| State/local CAPEX change | -3.1% |

What You See Is What You Get

Axon Enterprise Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Axon Enterprise you'll receive after purchase—no placeholders or mockups, fully formatted and ready for immediate download and use.