Azenta Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

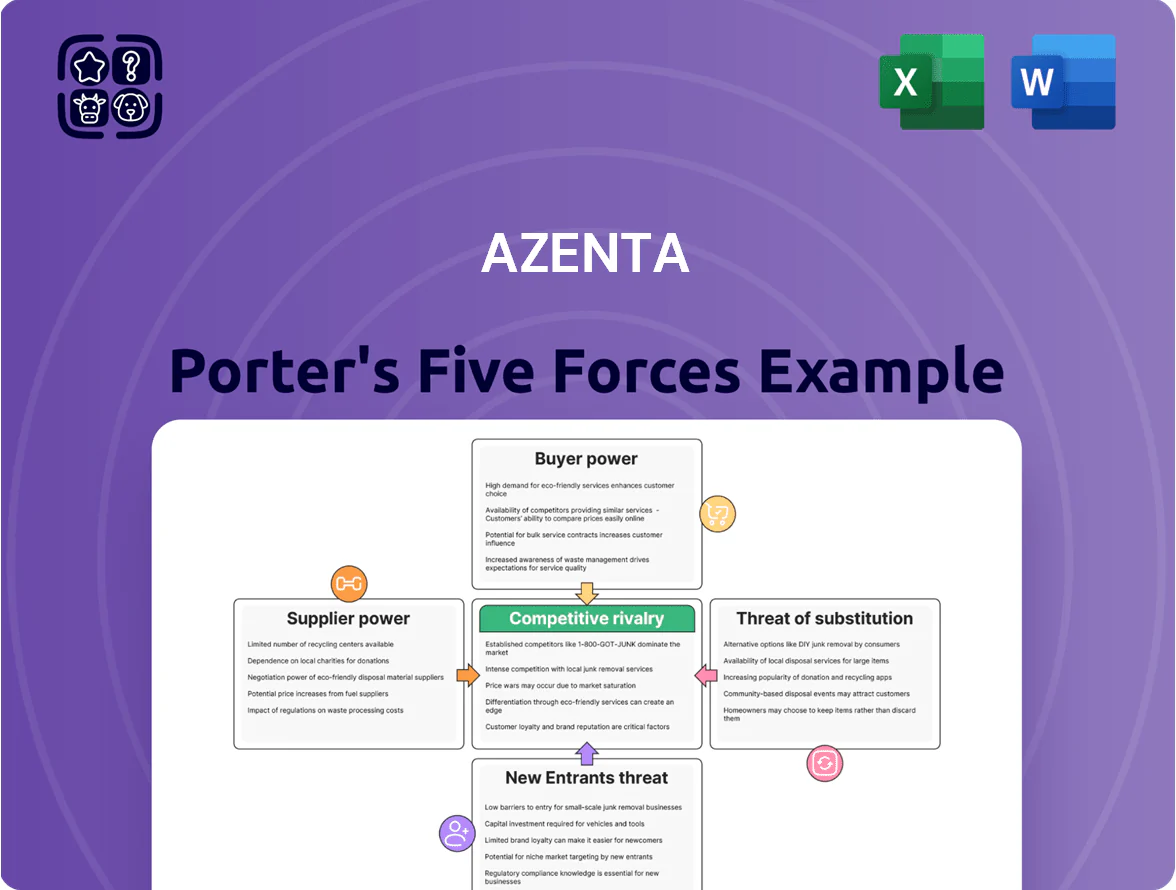

Azenta faces moderate supplier power and high buyer scrutiny in a niche life-sciences tools market where specialization raises entry barriers but innovation and M&A keep competitive pressure intense; substitutes and regulatory shifts add episodic threats that shape pricing and R&D choices. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Azenta’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Component Dependency

Azenta depends on niche suppliers for precision actuators and custom optics used in its automated storage and robotic arms, with fewer than five global vendors able to meet biotech tolerances; in 2024 supplier concentration contributed to a 6–9% input-cost sensitivity for instrument margins. Any single-vendor disruption or a 10–15% price rise can delay shipments by 6–12 weeks and cut gross margin by ~150–300 basis points.

Reagent and Chemical Consumables

The genomic services division depends on high-purity reagents and chemical consumables supplied mainly by a few large life-science firms (Thermo Fisher, Merck, Agilent), giving suppliers strong bargaining power; these inputs represent roughly 12–18% of lab operating costs and are critical for sequencing accuracy, so Azenta has limited room to push prices down. The specialized chemistries create high switching costs—revalidation can take weeks and cost tens of thousands—locking Azenta into supplier relationships.

Highly Skilled Technical Labor

The supply of specialized labor—robotics engineers and genomic scientists—is a critical input for Azenta’s service-led model, and as of 2025 demand outstrips supply: US biotech job openings grew 12% year-over-year in 2024 and median genomic scientist pay rose to about $120,000 in 2024, giving these workers strong bargaining power over compensation; Azenta must match or exceed market packages (total comp uplifts of 15–25% vs. 2022) to avoid talent loss to Big Pharma and tech firms.

Logistics and Cold Chain Providers

Maintaining biological sample integrity needs advanced cold-chain logistics and specialized transport; Azenta relies on external providers for ultra-low temperature shipping across borders, where losses can cost millions per batch. In 2024, certified biological shippers numbered only a few dozen globally, giving these firms moderate pricing leverage over Azenta’s sample-management margins, though long-term contracts and vertical investments limit rate volatility.

- Few dozen certified shippers globally (2024)

- Ultra-low temp transport critical—losses can cost millions

- Suppliers hold moderate pricing leverage

- Azenta offsets risk via long-term contracts and investments

Technological Infrastructure and Software

Azenta relies on third-party cloud and enterprise software to process >100PB of genomic and cold-storage data; AWS, Microsoft Azure, and Google Cloud account for ~60% of global cloud revenue in 2024, giving them leverage via multi-year contracts and complex migrations.

These suppliers can raise subscription fees or mandate security upgrades, squeezing Azenta’s margins—cloud costs for data-intensive biotech can reach 10–20% of OPEX; a single 10% fee hike would add millions annually.

Supplier power: hardware, reagents, talent & cloud drive 30–50% lab cost pressure

Suppliers hold moderate-to-strong power:

specialized hardware vendors (<5) drive 6–9% input-cost sensitivity; reagent suppliers (Thermo Fisher, Merck, Agilent) account for ~12–18% lab costs; talent pay rose ~12% in 2024 to $120k median; certified ultra-low shippers only few dozen (2024); cloud vendors (AWS/Azure/GCP) = ~60% market, cloud = 10–20% OPEX.

| Category | Metric (2024) |

|---|---|

| Hardware vendors | <5 vendors; 6–9% cost sensitivity |

| Reagents | 12–18% lab costs |

| Talent | Median $120k; +12% YoY |

| Shippers | Few dozen certified |

| Cloud | 60% market; 10–20% OPEX |

What is included in the product

Tailored Porter's Five Forces analysis for Azenta that uncovers competitive drivers, supplier and buyer power, threats from substitutes and new entrants, and identifies disruptive forces and strategic levers to protect market share.

Clear one-sheet Porter's Five Forces for Azenta—quickly assess supplier/customer power, rivalry, entry threat, and substitutes to guide strategic moves and investment decisions.

Customers Bargaining Power

Concentration of Large Pharmaceutical Clients

A sizable share of Azenta’s revenue comes from a handful of pharma/biotech giants—about 45% of 2024 revenue was concentrated in top 10 customers—giving these buyers strong bargaining power to demand volume discounts and bespoke SLAs. Those clients can push pricing down or require costly customizations; Azenta must therefore balance competitive contracts to retain anchor accounts while protecting margins (gross margin 2024: ~34%).

High Switching Costs for Integrated Systems

Once a lab integrates Azenta’s automated storage and inventory systems, switching costs—software retraining, hardware replacement, and workflow revalidation—can exceed $250k and 6–12 months, sharply lowering immediate customer bargaining power.

Proprietary firmware and LIMS (lab information management systems) integrations create technological lock-in, making customers dependent on Azenta for upgrades and support.

Still, initial sales remain buyer-driven: procurement cycles average 9 months with >30% of contracts won through competitive RFPs and price concessions.

Budget Constraints in Academic Research

Academic and government labs, which accounted for about 38% of life-science consumables spending in 2024, face fixed grant budgets and are highly price-sensitive, pushing Azenta to match lower-cost manual workflows or local providers to stretch funds.

Demand for Comprehensive Data Solutions

Modern customers demand integrated solutions pairing physical sample storage with digital genomic data and analytics, a trend led by genomics market growth to $34.8B in 2024 and 12.6% CAGR (2024–2030).

This gives buyers leverage to push Azenta to expand beyond storage into end-to-end services; losing that could drive customers to full-service CROs, which captured ~18% of life-science outsourcing spend in 2024.

- Customers force bundled offerings

- Genomics market $34.8B (2024)

- CROs ~18% outsourcing share (2024)

Availability of Alternative Service Providers

Customers in genomics can choose among Illumina, Thermo Fisher, BGI and Novogene, raising price and turnaround pressure; sequencing revenue is highly commoditized with unit costs falling ~15–25% annually through 2024, so switching is low-friction.

Azenta’s sample-management services are stickier but face churn risk: Azenta reported 2024 revenue $1.02bn, up 8%—forcing continual quality, SOP, and TAT (turnaround time) improvements to retain clients.

- Multiple top competitors: Illumina, Thermo Fisher, BGI, Novogene

- Sequencing unit-cost decline ~15–25%/yr to 2024

- Azenta 2024 revenue $1.02bn, +8% YoY

- Sample management more specialized, lower switch rate

Top‑10 buyers squeeze Azenta margins despite lock‑in; genomics market stays buyer‑driven

Large pharma buyers (top 10 = ~45% of 2024 revenue) exert high bargaining power via volume discounts and bespoke SLAs, pressuring Azenta’s ~34% gross margin; switching costs (≥$250k, 6–12 months) and LIMS lock‑in lower short‑term leverage. Academic/government price sensitivity and competing sequencers (Illumina, Thermo Fisher, BGI) plus CROs (18% outsourcing share, 2024) keep procurement buyer-driven.

| Metric | Value (2024) |

|---|---|

| Top‑10 customer share | ≈45% |

| Gross margin | ≈34% |

| Switching cost / time | ≥$250k / 6–12m |

| Azenta revenue | $1.02bn (+8%) |

| Genomics market | $34.8B |

| CRO share | ≈18% |

Full Version Awaits

Azenta Porter's Five Forces Analysis

This preview shows the exact Azenta Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples—fully formatted, professionally written, and ready for download and use the moment you buy.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Azenta faces moderate supplier power and high buyer scrutiny in a niche life-sciences tools market where specialization raises entry barriers but innovation and M&A keep competitive pressure intense; substitutes and regulatory shifts add episodic threats that shape pricing and R&D choices. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Azenta’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Component Dependency

Azenta depends on niche suppliers for precision actuators and custom optics used in its automated storage and robotic arms, with fewer than five global vendors able to meet biotech tolerances; in 2024 supplier concentration contributed to a 6–9% input-cost sensitivity for instrument margins. Any single-vendor disruption or a 10–15% price rise can delay shipments by 6–12 weeks and cut gross margin by ~150–300 basis points.

Reagent and Chemical Consumables

The genomic services division depends on high-purity reagents and chemical consumables supplied mainly by a few large life-science firms (Thermo Fisher, Merck, Agilent), giving suppliers strong bargaining power; these inputs represent roughly 12–18% of lab operating costs and are critical for sequencing accuracy, so Azenta has limited room to push prices down. The specialized chemistries create high switching costs—revalidation can take weeks and cost tens of thousands—locking Azenta into supplier relationships.

Highly Skilled Technical Labor

The supply of specialized labor—robotics engineers and genomic scientists—is a critical input for Azenta’s service-led model, and as of 2025 demand outstrips supply: US biotech job openings grew 12% year-over-year in 2024 and median genomic scientist pay rose to about $120,000 in 2024, giving these workers strong bargaining power over compensation; Azenta must match or exceed market packages (total comp uplifts of 15–25% vs. 2022) to avoid talent loss to Big Pharma and tech firms.

Logistics and Cold Chain Providers

Maintaining biological sample integrity needs advanced cold-chain logistics and specialized transport; Azenta relies on external providers for ultra-low temperature shipping across borders, where losses can cost millions per batch. In 2024, certified biological shippers numbered only a few dozen globally, giving these firms moderate pricing leverage over Azenta’s sample-management margins, though long-term contracts and vertical investments limit rate volatility.

- Few dozen certified shippers globally (2024)

- Ultra-low temp transport critical—losses can cost millions

- Suppliers hold moderate pricing leverage

- Azenta offsets risk via long-term contracts and investments

Technological Infrastructure and Software

Azenta relies on third-party cloud and enterprise software to process >100PB of genomic and cold-storage data; AWS, Microsoft Azure, and Google Cloud account for ~60% of global cloud revenue in 2024, giving them leverage via multi-year contracts and complex migrations.

These suppliers can raise subscription fees or mandate security upgrades, squeezing Azenta’s margins—cloud costs for data-intensive biotech can reach 10–20% of OPEX; a single 10% fee hike would add millions annually.

Supplier power: hardware, reagents, talent & cloud drive 30–50% lab cost pressure

Suppliers hold moderate-to-strong power:

specialized hardware vendors (<5) drive 6–9% input-cost sensitivity; reagent suppliers (Thermo Fisher, Merck, Agilent) account for ~12–18% lab costs; talent pay rose ~12% in 2024 to $120k median; certified ultra-low shippers only few dozen (2024); cloud vendors (AWS/Azure/GCP) = ~60% market, cloud = 10–20% OPEX.

| Category | Metric (2024) |

|---|---|

| Hardware vendors | <5 vendors; 6–9% cost sensitivity |

| Reagents | 12–18% lab costs |

| Talent | Median $120k; +12% YoY |

| Shippers | Few dozen certified |

| Cloud | 60% market; 10–20% OPEX |

What is included in the product

Tailored Porter's Five Forces analysis for Azenta that uncovers competitive drivers, supplier and buyer power, threats from substitutes and new entrants, and identifies disruptive forces and strategic levers to protect market share.

Clear one-sheet Porter's Five Forces for Azenta—quickly assess supplier/customer power, rivalry, entry threat, and substitutes to guide strategic moves and investment decisions.

Customers Bargaining Power

Concentration of Large Pharmaceutical Clients

A sizable share of Azenta’s revenue comes from a handful of pharma/biotech giants—about 45% of 2024 revenue was concentrated in top 10 customers—giving these buyers strong bargaining power to demand volume discounts and bespoke SLAs. Those clients can push pricing down or require costly customizations; Azenta must therefore balance competitive contracts to retain anchor accounts while protecting margins (gross margin 2024: ~34%).

High Switching Costs for Integrated Systems

Once a lab integrates Azenta’s automated storage and inventory systems, switching costs—software retraining, hardware replacement, and workflow revalidation—can exceed $250k and 6–12 months, sharply lowering immediate customer bargaining power.

Proprietary firmware and LIMS (lab information management systems) integrations create technological lock-in, making customers dependent on Azenta for upgrades and support.

Still, initial sales remain buyer-driven: procurement cycles average 9 months with >30% of contracts won through competitive RFPs and price concessions.

Budget Constraints in Academic Research

Academic and government labs, which accounted for about 38% of life-science consumables spending in 2024, face fixed grant budgets and are highly price-sensitive, pushing Azenta to match lower-cost manual workflows or local providers to stretch funds.

Demand for Comprehensive Data Solutions

Modern customers demand integrated solutions pairing physical sample storage with digital genomic data and analytics, a trend led by genomics market growth to $34.8B in 2024 and 12.6% CAGR (2024–2030).

This gives buyers leverage to push Azenta to expand beyond storage into end-to-end services; losing that could drive customers to full-service CROs, which captured ~18% of life-science outsourcing spend in 2024.

- Customers force bundled offerings

- Genomics market $34.8B (2024)

- CROs ~18% outsourcing share (2024)

Availability of Alternative Service Providers

Customers in genomics can choose among Illumina, Thermo Fisher, BGI and Novogene, raising price and turnaround pressure; sequencing revenue is highly commoditized with unit costs falling ~15–25% annually through 2024, so switching is low-friction.

Azenta’s sample-management services are stickier but face churn risk: Azenta reported 2024 revenue $1.02bn, up 8%—forcing continual quality, SOP, and TAT (turnaround time) improvements to retain clients.

- Multiple top competitors: Illumina, Thermo Fisher, BGI, Novogene

- Sequencing unit-cost decline ~15–25%/yr to 2024

- Azenta 2024 revenue $1.02bn, +8% YoY

- Sample management more specialized, lower switch rate

Top‑10 buyers squeeze Azenta margins despite lock‑in; genomics market stays buyer‑driven

Large pharma buyers (top 10 = ~45% of 2024 revenue) exert high bargaining power via volume discounts and bespoke SLAs, pressuring Azenta’s ~34% gross margin; switching costs (≥$250k, 6–12 months) and LIMS lock‑in lower short‑term leverage. Academic/government price sensitivity and competing sequencers (Illumina, Thermo Fisher, BGI) plus CROs (18% outsourcing share, 2024) keep procurement buyer-driven.

| Metric | Value (2024) |

|---|---|

| Top‑10 customer share | ≈45% |

| Gross margin | ≈34% |

| Switching cost / time | ≥$250k / 6–12m |

| Azenta revenue | $1.02bn (+8%) |

| Genomics market | $34.8B |

| CRO share | ≈18% |

Full Version Awaits

Azenta Porter's Five Forces Analysis

This preview shows the exact Azenta Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples—fully formatted, professionally written, and ready for download and use the moment you buy.