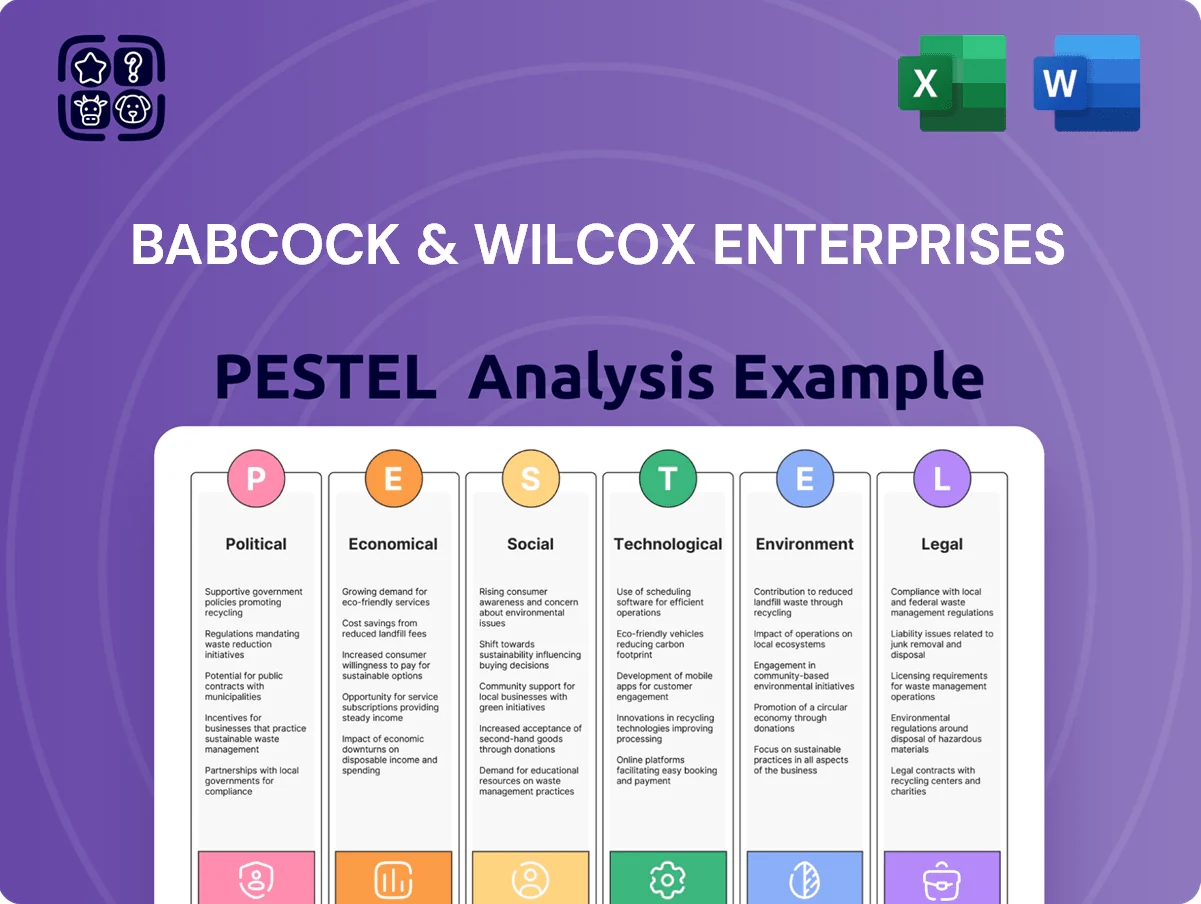

Babcock & Wilcox Enterprises PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Our PESTLE Analysis for Babcock & Wilcox Enterprises reveals how regulatory shifts, energy market dynamics, and technological innovation are reshaping the company’s risk and opportunity profile; use these concise insights to strengthen strategy and investment decisions. Purchase the full analysis to access detailed, actionable intelligence—ready for boardrooms, pitches, and financial models.

Political factors

Global Clean Energy Subsidies

The expansion of the US Inflation Reduction Act and parallel EU green deals boost Babcock & Wilcox Enterprises' renewables, with IRA tax credits covering up to 45Q-equivalent rates and EU grants co-financing ~30% of eligible projects, directly supporting carbon capture and waste-to-energy initiatives.

These policies enable higher project IRRs and helped B&W secure contracts worth $420m in cleantech backlog by Q3 2025, aligning with management targets to grow renewable revenue share above 25% by 2026.

As of late 2025, sustained political focus on the energy transition keeps a steady pipeline of subsidized projects, with US and EU public funding commitments exceeding $200bn annually for low-carbon infrastructure.

Geopolitical Supply Chain Stability

Ongoing tensions in Eastern Europe and East Asia disrupt supply of specialized steel and electronic components for power plants, with 2024 WTO data showing global steel export disruptions raised input lead times by ~18% and pushed component prices up ~12% YoY, increasing capex on international projects for Babcock & Wilcox Enterprises (BWC) and peers. Political instability risks tariffs or embargoes that can add several percentage points to project costs, forcing management to adjust pricing and extend delivery buffers to protect margins and meet utility contracts.

National Energy Security Priorities

Governments prioritizing domestic energy independence boost demand for Babcock & Wilcox Enterprises’ biomass and waste-to-energy offerings; global energy security spending hit an estimated $420 billion in 2024, supporting localized generation projects where B&W’s technologies apply.

Decarbonization Mandates

Strict political commitments to reach net-zero by 2050 drive mandatory retrofits of heavy industry; global net-zero pledges cover 74% of emissions as of 2025, increasing demand for emissions control technologies.

Babcock & Wilcox Enterprises, with its carbon capture and water/air treatment units, is a primary beneficiary—its 2024 environmental services backlog grew 18% year-over-year, reflecting mandate-driven procurement.

Ongoing legislative pressure on cement and steel sectors—responsible for ~15% of global CO2—creates a compulsory market for B&W’s scrubbers and carbon management offerings.

- Net-zero pledges: 74% of emissions covered (2025)

- B&W 2024 environmental backlog +18% YoY

- Cement/steel ≈15% of CO2, regulatory-driven demand

Trade Relations and Tariffs

Fluctuating US trade relations with China, India and Mexico can raise raw-material costs for Babcock & Wilcox Enterprises, where steel and components represent ~28% of project COGS; a 10% tariff increase could add millions to multi-year contracts.

Tariffs on imported materials directly compress margins on large infrastructure projects—B&W reported 2024 gross margin of 15.2%, sensitive to input cost shocks.

Rising protectionism may force partial supply-chain relocation to North America or Southeast Asia, increasing near-term capex but preserving long-term profitability.

- Key risk: tariff shocks boosting material costs by ~10%+

- Exposure: steel/components ~28% of COGS

- Mitigation: nearshoring raises capex but stabilizes margins

B&W rides $420M cleantech backlog and $200B green funding despite rising steel costs

US/EU green subsidies and IRA credits boost B&W’s cleantech backlog (~$420m by Q3 2025) and supported 18% YoY growth in 2024 environmental backlog; political focus funds >$200bn/yr low‑carbon projects (2025) and net‑zero pledges cover 74% of emissions. Trade tensions raised steel/component lead times ~18% and prices ~12% in 2024, with steel/components ≈28% of COGS and 2024 gross margin 15.2%.

| Metric | Value |

|---|---|

| Cleantech backlog | $420m (Q3 2025) |

| Env. backlog growth | +18% YoY (2024) |

| Low‑carbon funding | >$200bn/yr (2025) |

| Net‑zero coverage | 74% emissions (2025) |

| Steel/component share of COGS | ~28% |

| Input price/lead time moves | +12% price, +18% lead time (2024) |

| Gross margin | 15.2% (2024) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Babcock & Wilcox Enterprises across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify risks and opportunities.

A concise, PESTLE-segmented brief that highlights Babcock & Wilcox Enterprises’ regulatory, technological, and market risks for quick insertion into presentations or team discussions, easily annotated for regional or business-line specifics.

Economic factors

Interest Rate Fluctuations

The cost of capital is critical for Babcock & Wilcox Enterprises given its capital-intensive energy projects; US commercial mortgage rates rose to ~6.5%–7.0% in 2025, increasing borrowing costs for utilities and OEM customers and compressing project IRRs.

Higher interest rates through 2025 have delayed some utility-scale plant FIDs, with industry capex pauses reported and utility bond yields near 5.5% raising financing hurdles.

Any stabilization—e.g., Federal Reserve policy signaling a pause—would lower long-term infrastructure debt premiums and improve predictability for project equity returns.

Raw Material Inflation

Raw material inflation in 2024 pushed global steel and specialty alloy prices up roughly 12–18% year-over-year, raising inputs for Babcock & Wilcox Enterprises’ environmental control systems; chemicals like stainless alloy feedstocks rose ~9% in 2024 per S&P Global. The company’s price escalation clauses mitigate some risk, but abrupt spikes have compressed project margins—B&W reported a 2024 gross margin of 14.2%, down from 16.1% in 2023. Continuous monitoring of commodity markets and hedging of key inputs are essential to preserve contract profitability and project feasibility.

Green Financing Availability

Rising ESG-linked loans and green bonds—global green bond issuance hit about $560 billion in 2023 and ~$600 billion in 2024—improve Babcock & Wilcox Enterprises access to cheaper capital for sustainable tech.

Investors funneled record flows into energy-transition strategies in 2024, lowering WACC for qualifying projects and enabling more aggressive R&D funding for hydrogen and carbon capture.

Emerging Market Growth

- 200+ GW projected new capacity by 2030 in target regions

- Regional GDP growth ~4–5% (2024–25)

- High demand for cost-effective, modular energy tech

- Competitive edge requires flexible financing/local adaptation

Energy Price Volatility

Fluctuations in natural gas and coal prices affect Babcock & Wilcox Enterprises' market for biomass and waste-to-energy; US Henry Hub natural gas fell from an average $6.30/MMBtu in 2022 to about $3.50/MMBtu in 2024, reducing urgency for fuel-switching.

Higher fossil fuel prices shorten payback for renewables—when gas exceeds $5/MMBtu, project IRRs rise materially—while sustained low prices can delay industrial clients from investing in capital-intensive systems.

- 2024 US Henry Hub ~3.50/MMBtu; 2022 ~6.30/MMBtu

- Gas >5/MMBtu increases biomass project competitiveness

- Low fossil prices can postpone client transitions

Higher rates and raw-material inflation squeeze B&W margins despite greener finance

Higher 2024–25 rates raised B&W borrowing costs (US mortgage ~6.5–7.0%; utility bond ~5.5%), compressing IRRs; 2024 raw material inflation +12–18% hit margins (gross margin 14.2% vs 16.1% in 2023). Green bond issuance ~$600B (2024) improves project finance; US Henry Hub ~3.50/MMBtu (2024) vs 6.30 (2022) affects fuel-switching demand.

| Metric | 2022 | 2024 |

|---|---|---|

| US Henry Hub ($/MMBtu) | 6.30 | 3.50 |

| Green bond issuance ($bn) | 560 (2023) | 600 (2024) |

| B&W gross margin | 16.1% | 14.2% |

Full Version Awaits

Babcock & Wilcox Enterprises PESTLE Analysis

The preview shown here is the exact Babcock & Wilcox Enterprises PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and insights visible in the preview are identical to the final downloadable file you’ll get immediately after payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Our PESTLE Analysis for Babcock & Wilcox Enterprises reveals how regulatory shifts, energy market dynamics, and technological innovation are reshaping the company’s risk and opportunity profile; use these concise insights to strengthen strategy and investment decisions. Purchase the full analysis to access detailed, actionable intelligence—ready for boardrooms, pitches, and financial models.

Political factors

Global Clean Energy Subsidies

The expansion of the US Inflation Reduction Act and parallel EU green deals boost Babcock & Wilcox Enterprises' renewables, with IRA tax credits covering up to 45Q-equivalent rates and EU grants co-financing ~30% of eligible projects, directly supporting carbon capture and waste-to-energy initiatives.

These policies enable higher project IRRs and helped B&W secure contracts worth $420m in cleantech backlog by Q3 2025, aligning with management targets to grow renewable revenue share above 25% by 2026.

As of late 2025, sustained political focus on the energy transition keeps a steady pipeline of subsidized projects, with US and EU public funding commitments exceeding $200bn annually for low-carbon infrastructure.

Geopolitical Supply Chain Stability

Ongoing tensions in Eastern Europe and East Asia disrupt supply of specialized steel and electronic components for power plants, with 2024 WTO data showing global steel export disruptions raised input lead times by ~18% and pushed component prices up ~12% YoY, increasing capex on international projects for Babcock & Wilcox Enterprises (BWC) and peers. Political instability risks tariffs or embargoes that can add several percentage points to project costs, forcing management to adjust pricing and extend delivery buffers to protect margins and meet utility contracts.

National Energy Security Priorities

Governments prioritizing domestic energy independence boost demand for Babcock & Wilcox Enterprises’ biomass and waste-to-energy offerings; global energy security spending hit an estimated $420 billion in 2024, supporting localized generation projects where B&W’s technologies apply.

Decarbonization Mandates

Strict political commitments to reach net-zero by 2050 drive mandatory retrofits of heavy industry; global net-zero pledges cover 74% of emissions as of 2025, increasing demand for emissions control technologies.

Babcock & Wilcox Enterprises, with its carbon capture and water/air treatment units, is a primary beneficiary—its 2024 environmental services backlog grew 18% year-over-year, reflecting mandate-driven procurement.

Ongoing legislative pressure on cement and steel sectors—responsible for ~15% of global CO2—creates a compulsory market for B&W’s scrubbers and carbon management offerings.

- Net-zero pledges: 74% of emissions covered (2025)

- B&W 2024 environmental backlog +18% YoY

- Cement/steel ≈15% of CO2, regulatory-driven demand

Trade Relations and Tariffs

Fluctuating US trade relations with China, India and Mexico can raise raw-material costs for Babcock & Wilcox Enterprises, where steel and components represent ~28% of project COGS; a 10% tariff increase could add millions to multi-year contracts.

Tariffs on imported materials directly compress margins on large infrastructure projects—B&W reported 2024 gross margin of 15.2%, sensitive to input cost shocks.

Rising protectionism may force partial supply-chain relocation to North America or Southeast Asia, increasing near-term capex but preserving long-term profitability.

- Key risk: tariff shocks boosting material costs by ~10%+

- Exposure: steel/components ~28% of COGS

- Mitigation: nearshoring raises capex but stabilizes margins

B&W rides $420M cleantech backlog and $200B green funding despite rising steel costs

US/EU green subsidies and IRA credits boost B&W’s cleantech backlog (~$420m by Q3 2025) and supported 18% YoY growth in 2024 environmental backlog; political focus funds >$200bn/yr low‑carbon projects (2025) and net‑zero pledges cover 74% of emissions. Trade tensions raised steel/component lead times ~18% and prices ~12% in 2024, with steel/components ≈28% of COGS and 2024 gross margin 15.2%.

| Metric | Value |

|---|---|

| Cleantech backlog | $420m (Q3 2025) |

| Env. backlog growth | +18% YoY (2024) |

| Low‑carbon funding | >$200bn/yr (2025) |

| Net‑zero coverage | 74% emissions (2025) |

| Steel/component share of COGS | ~28% |

| Input price/lead time moves | +12% price, +18% lead time (2024) |

| Gross margin | 15.2% (2024) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Babcock & Wilcox Enterprises across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify risks and opportunities.

A concise, PESTLE-segmented brief that highlights Babcock & Wilcox Enterprises’ regulatory, technological, and market risks for quick insertion into presentations or team discussions, easily annotated for regional or business-line specifics.

Economic factors

Interest Rate Fluctuations

The cost of capital is critical for Babcock & Wilcox Enterprises given its capital-intensive energy projects; US commercial mortgage rates rose to ~6.5%–7.0% in 2025, increasing borrowing costs for utilities and OEM customers and compressing project IRRs.

Higher interest rates through 2025 have delayed some utility-scale plant FIDs, with industry capex pauses reported and utility bond yields near 5.5% raising financing hurdles.

Any stabilization—e.g., Federal Reserve policy signaling a pause—would lower long-term infrastructure debt premiums and improve predictability for project equity returns.

Raw Material Inflation

Raw material inflation in 2024 pushed global steel and specialty alloy prices up roughly 12–18% year-over-year, raising inputs for Babcock & Wilcox Enterprises’ environmental control systems; chemicals like stainless alloy feedstocks rose ~9% in 2024 per S&P Global. The company’s price escalation clauses mitigate some risk, but abrupt spikes have compressed project margins—B&W reported a 2024 gross margin of 14.2%, down from 16.1% in 2023. Continuous monitoring of commodity markets and hedging of key inputs are essential to preserve contract profitability and project feasibility.

Green Financing Availability

Rising ESG-linked loans and green bonds—global green bond issuance hit about $560 billion in 2023 and ~$600 billion in 2024—improve Babcock & Wilcox Enterprises access to cheaper capital for sustainable tech.

Investors funneled record flows into energy-transition strategies in 2024, lowering WACC for qualifying projects and enabling more aggressive R&D funding for hydrogen and carbon capture.

Emerging Market Growth

- 200+ GW projected new capacity by 2030 in target regions

- Regional GDP growth ~4–5% (2024–25)

- High demand for cost-effective, modular energy tech

- Competitive edge requires flexible financing/local adaptation

Energy Price Volatility

Fluctuations in natural gas and coal prices affect Babcock & Wilcox Enterprises' market for biomass and waste-to-energy; US Henry Hub natural gas fell from an average $6.30/MMBtu in 2022 to about $3.50/MMBtu in 2024, reducing urgency for fuel-switching.

Higher fossil fuel prices shorten payback for renewables—when gas exceeds $5/MMBtu, project IRRs rise materially—while sustained low prices can delay industrial clients from investing in capital-intensive systems.

- 2024 US Henry Hub ~3.50/MMBtu; 2022 ~6.30/MMBtu

- Gas >5/MMBtu increases biomass project competitiveness

- Low fossil prices can postpone client transitions

Higher rates and raw-material inflation squeeze B&W margins despite greener finance

Higher 2024–25 rates raised B&W borrowing costs (US mortgage ~6.5–7.0%; utility bond ~5.5%), compressing IRRs; 2024 raw material inflation +12–18% hit margins (gross margin 14.2% vs 16.1% in 2023). Green bond issuance ~$600B (2024) improves project finance; US Henry Hub ~3.50/MMBtu (2024) vs 6.30 (2022) affects fuel-switching demand.

| Metric | 2022 | 2024 |

|---|---|---|

| US Henry Hub ($/MMBtu) | 6.30 | 3.50 |

| Green bond issuance ($bn) | 560 (2023) | 600 (2024) |

| B&W gross margin | 16.1% | 14.2% |

Full Version Awaits

Babcock & Wilcox Enterprises PESTLE Analysis

The preview shown here is the exact Babcock & Wilcox Enterprises PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and insights visible in the preview are identical to the final downloadable file you’ll get immediately after payment.