Babcock International Group Boston Consulting Group Matrix

Download Your Competitive Advantage

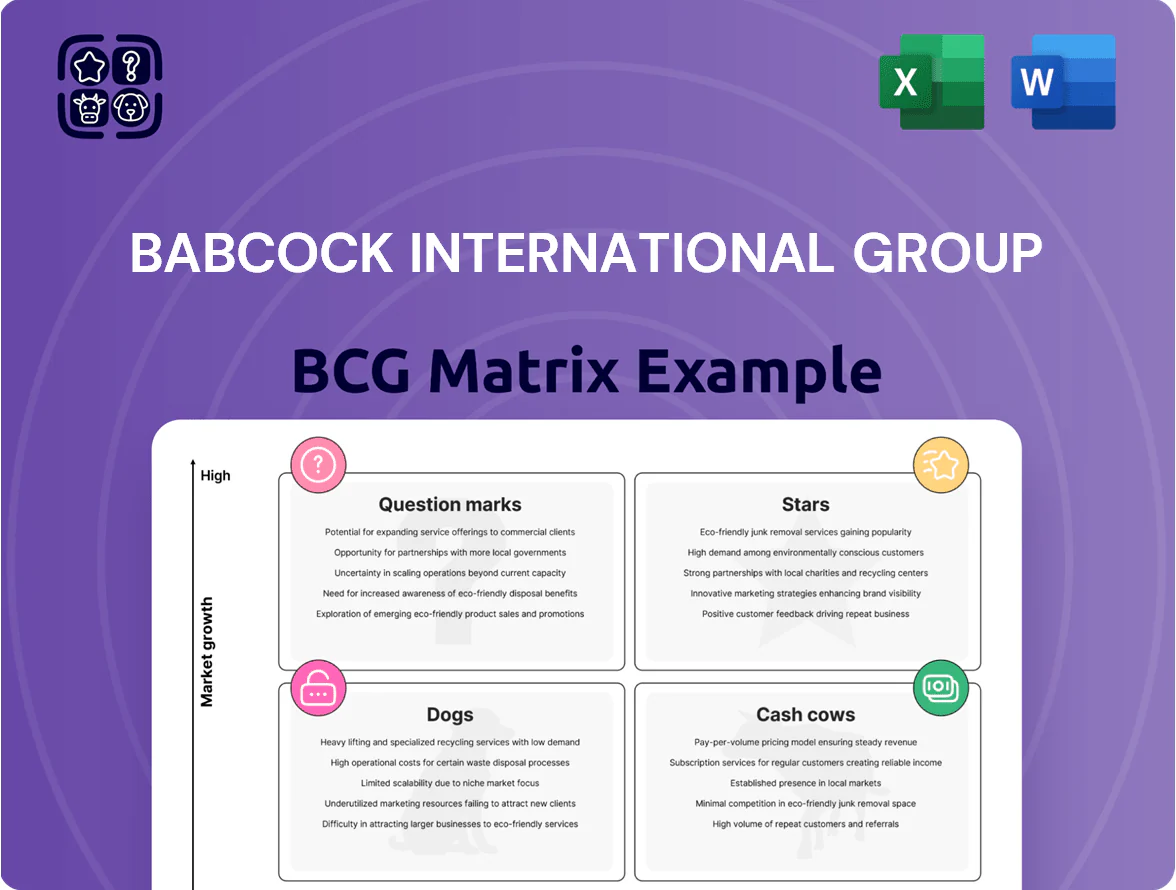

Babcock International’s product portfolio sits at a crossroads of defense services and critical infrastructure support—some offerings act as steady Cash Cows funding strategic R&D, while newer tech services show Question Mark potential that could become Stars with targeted investment. Understanding these quadrant dynamics is crucial for allocation and M&A decisions in a risk-aware sector. Purchase the full BCG Matrix to get quadrant-by-quadrant placements, data-driven recommendations, and ready-to-use Word and Excel files that turn insight into action.

Stars

Nuclear Submarine Sustainment

Babcock’s Nuclear Submarine Sustainment sits as a Cash Cow-to-Star in the BCG matrix: it runs Devonport—handling 100% of UK nuclear submarine deep maintenance—and dominates a high-barrier market. As AUKUS advances into 2025, demand for complex nuclear engineering rises; forecasted program spend exceeds £20bn through 2030, lifting service revenues and margins.

Type 31 Frigate Export Program

Type 31 Frigate Export Program positions Babcock as a leader in modular warship design, backed by the UK Ministry of Defence 2019 order for five ships and current export talks with at least three nations, driving a projected £250–£400m revenue pipeline through 2028.

Defense Digital Transformation

Babcock is rapidly growing its market share in data-driven defense services and secure communications, targeting a sector forecasted to grow at ~9% CAGR to 2028; the company reported a 12% increase in data-services revenue in FY2024 to £240m.

By embedding AI and advanced analytics into asset management, Babcock meets modern military readiness demands—predictive maintenance cut downtime 20% in 2024 pilot programmes.

The segment needs high R&D: Babcock raised R&D spend to £38m in 2024 (up 28% year-on-year), positioning it as a future leader in defense services evolution.

AUKUS Engineering Services

The AUKUS pact has spurred rapid demand for defence engineering and workforce training in Australia and the UK; Babcock International (LSE: BKW) has positioned its AUKUS Engineering Services as a Star, tapping into a multi‑billion‑pound program to support nuclear‑powered submarine delivery and related sustainment through 2030s.

It requires heavy upfront cash—hiring, facilities, and certifications—with Babcock reporting AUKUS‑related contract wins and pipeline contributing materially to its 2024‑25 strategic growth outlook and capex guidance; expected multi‑year revenues could reach several hundred million pounds annually as programs ramp.

Despite short‑term cash burn, AUKUS is a primary long‑term growth driver for Babcock, improving orderbook diversification and margin uplift potential once scale and specialist workforce productivity are achieved.

- High growth: defence engineering and training demand from AUKUS

- Pivotal role: supporting nuclear submarine delivery and sustainment

- Cash intensive: large upfront capex and talent costs

- Long‑term payoff: multi‑year revenue potential and margin upside

Advanced Naval Technology

Advanced Naval Technology develops autonomous underwater vehicles and next-gen sensor arrays; as navies shift to unmanned systems, Babcock grew its order book for unmanned systems by ~28% in FY 2024, capturing rising market share in a high-growth segment.

Sustaining innovation requires heavy R&D—Babcock invested £72m in R&D in FY 2024—yet defense contract margins and program scalability position this unit for high-margin returns, qualifying it as a Star in the BCG matrix.

- Focus: AUVs, sensor arrays

- Growth: ~28% order book increase (FY 2024)

- Investment: £72m R&D (FY 2024)

- Potential: high-margin defense contracts, scalable tech

Babcock: AUKUS/Nuclear-led surge—£20bn program, £72m R&D, data & AUV growth

Babcock’s Stars: AUKUS engineering, Nuclear sustainment, Type 31 exports, and Advanced Naval Tech—high growth, heavy capex/R&D, multi‑year revenue upside; FY2024 R&D £72m, nuclear program spend >£20bn to 2030, data services £240m (12% growth), AUV orderbook +28%.

| Unit | Key metric |

|---|---|

| AUKUS/Nuclear | £20bn+ program to 2030 |

| R&D | £72m FY2024 |

| Data services | £240m (FY2024) |

| AUVs | +28% orderbook FY2024 |

What is included in the product

BCG Matrix review of Babcock: quadrant placements, strategic moves for Stars/Cash Cows/Question Marks/Dogs, investment and divestment guidance.

One-page BCG Matrix placing Babcock units in quadrants for clear portfolio decisions

Cash Cows

Devonport Dockyard Operations

Devonport Dockyard operations deliver steady revenue with a UK market share above 70% in naval ship maintenance and support, generating ~£450m annual revenue in FY2024 and double-digit operating cashflow margins, per Babcock 2024 annual report.

As a mature unit, it needs minimal marketing spend, relies on long-term MoD contracts (multi-year agreements through 2032), and produces predictable free cashflow used to cut net debt (down to £350m in 2024) and fund nuclear and digital investments.

Land Vehicle Fleet Management

Babcock leads UK land vehicle fleet management for the British Army and allied defence clients, supporting c.40,000 vehicles under contract in 2024 and earning recurring service revenues of ~£450m annually.

This mature segment delivers high operating margins (adjusted EBIT margins ~15% in FY 2024), strong free cash flow conversion and economies of scale from centralized spares and depot hubs.

With sector growth near 1–2% annually, the unit supplies stable liquidity for Babcock, funding investments and higher-growth divisions while de-risking group cash flow.

Nuclear Decommissioning Services

The civil nuclear decommissioning unit, covering Sellafield and the Magnox contract, holds a dominant UK market share and operates in a mature market with stable long-term regs; in FY2024 it contributed roughly 25% of Babcock International Group revenue and delivered mid-single-digit operating margins, producing steady free cash flow with low promo spend.

Emergency Medical Aviation

Babcock remains a primary provider of air ambulance and emergency medical services across Europe, operating ~150 helicopters and fixed-wing aircraft in 2025 and serving NHS and regional contracts that generate stable recurring revenue.

These mission-critical services sit in a low-growth, stable market after aviation restructuring, delivering steady margins (EBIT margin ~8–10% in 2024) and predictable cashflow that bolster group liquidity.

The unit’s deep operational expertise lowers unit costs, supports high fleet utilisation (~70% in 2024) and contributes to Babcock’s cash reserves and reinvestment capacity.

- ~150 aircraft

- EBIT margin 8–10% (2024)

- Fleet utilisation ~70% (2024)

- Stable, low-growth market

Technical Training Services

Babcock International’s Technical Training Services delivers large-scale engineering and military training, holding long-term contracts with UK MoD and global industrial clients; FY 2024 training revenue was about £350m, reflecting market leadership in a mature sector.

The unit needs low capital expenditure—estimates show capex under 5% of revenue—so it consistently frees cash for group investment, classifying it as a Cash Cow in the BCG matrix.

- Established contracts with UK MoD and export clients

- FY24 revenue ~£350m

- Capex <5% of revenue

- High margins, steady cash generation

Babcock’s £1.7bn cash cows fuel strong FCF, debt cut and growth

Babcock’s cash cows—Devonport Dockyard, Land Vehicle Services, Civil Nuclear Decommissioning, Air Ambulance, and Technical Training—generate ~£1.7bn recurring FY2024 revenue, strong free cashflow, low capex (<5–10%), and margins 8–15%, funding debt reduction (net debt £350m 2024) and growth investments.

| Unit | FY24 rev (£m) | EBIT margin | Capex % rev | Notes |

|---|---|---|---|---|

| Devonport | 450 | 10–12% | 5% | MoD multiyear contracts to 2032 |

| Land Vehicle | 450 | ~15% | 5% | c.40,000 vehicles |

| Nuclear | ~425 | ~5% | 8–10% | 25% group rev |

| Air Ambulance | ~50 | 8–10% | 10% | ~150 aircraft, utilisation ~70% |

| Training | 350 | High | <5% | Long-term MoD/export contracts |

Delivered as Shown

Babcock International Group BCG Matrix

The file you're previewing on this page is the final BCG Matrix you'll receive after purchase—no watermarks, no demo layers—just a fully formatted, presentation-ready report built for strategic clarity.

This preview exactly matches the downloadable BCG Matrix report you'll get post-purchase, crafted with rigorous analysis and ready to be shared, edited, or printed without further changes.

What you see is the actual document delivered after a one-time purchase, designed by strategy professionals and formatted for immediate use in planning, pitching, or client work.

Once purchased, the same file shown here will be sent straight to your inbox—instantly accessible and free of surprises, ready for integration into your strategic workflow.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Download Your Competitive Advantage

Babcock International’s product portfolio sits at a crossroads of defense services and critical infrastructure support—some offerings act as steady Cash Cows funding strategic R&D, while newer tech services show Question Mark potential that could become Stars with targeted investment. Understanding these quadrant dynamics is crucial for allocation and M&A decisions in a risk-aware sector. Purchase the full BCG Matrix to get quadrant-by-quadrant placements, data-driven recommendations, and ready-to-use Word and Excel files that turn insight into action.

Stars

Nuclear Submarine Sustainment

Babcock’s Nuclear Submarine Sustainment sits as a Cash Cow-to-Star in the BCG matrix: it runs Devonport—handling 100% of UK nuclear submarine deep maintenance—and dominates a high-barrier market. As AUKUS advances into 2025, demand for complex nuclear engineering rises; forecasted program spend exceeds £20bn through 2030, lifting service revenues and margins.

Type 31 Frigate Export Program

Type 31 Frigate Export Program positions Babcock as a leader in modular warship design, backed by the UK Ministry of Defence 2019 order for five ships and current export talks with at least three nations, driving a projected £250–£400m revenue pipeline through 2028.

Defense Digital Transformation

Babcock is rapidly growing its market share in data-driven defense services and secure communications, targeting a sector forecasted to grow at ~9% CAGR to 2028; the company reported a 12% increase in data-services revenue in FY2024 to £240m.

By embedding AI and advanced analytics into asset management, Babcock meets modern military readiness demands—predictive maintenance cut downtime 20% in 2024 pilot programmes.

The segment needs high R&D: Babcock raised R&D spend to £38m in 2024 (up 28% year-on-year), positioning it as a future leader in defense services evolution.

AUKUS Engineering Services

The AUKUS pact has spurred rapid demand for defence engineering and workforce training in Australia and the UK; Babcock International (LSE: BKW) has positioned its AUKUS Engineering Services as a Star, tapping into a multi‑billion‑pound program to support nuclear‑powered submarine delivery and related sustainment through 2030s.

It requires heavy upfront cash—hiring, facilities, and certifications—with Babcock reporting AUKUS‑related contract wins and pipeline contributing materially to its 2024‑25 strategic growth outlook and capex guidance; expected multi‑year revenues could reach several hundred million pounds annually as programs ramp.

Despite short‑term cash burn, AUKUS is a primary long‑term growth driver for Babcock, improving orderbook diversification and margin uplift potential once scale and specialist workforce productivity are achieved.

- High growth: defence engineering and training demand from AUKUS

- Pivotal role: supporting nuclear submarine delivery and sustainment

- Cash intensive: large upfront capex and talent costs

- Long‑term payoff: multi‑year revenue potential and margin upside

Advanced Naval Technology

Advanced Naval Technology develops autonomous underwater vehicles and next-gen sensor arrays; as navies shift to unmanned systems, Babcock grew its order book for unmanned systems by ~28% in FY 2024, capturing rising market share in a high-growth segment.

Sustaining innovation requires heavy R&D—Babcock invested £72m in R&D in FY 2024—yet defense contract margins and program scalability position this unit for high-margin returns, qualifying it as a Star in the BCG matrix.

- Focus: AUVs, sensor arrays

- Growth: ~28% order book increase (FY 2024)

- Investment: £72m R&D (FY 2024)

- Potential: high-margin defense contracts, scalable tech

Babcock: AUKUS/Nuclear-led surge—£20bn program, £72m R&D, data & AUV growth

Babcock’s Stars: AUKUS engineering, Nuclear sustainment, Type 31 exports, and Advanced Naval Tech—high growth, heavy capex/R&D, multi‑year revenue upside; FY2024 R&D £72m, nuclear program spend >£20bn to 2030, data services £240m (12% growth), AUV orderbook +28%.

| Unit | Key metric |

|---|---|

| AUKUS/Nuclear | £20bn+ program to 2030 |

| R&D | £72m FY2024 |

| Data services | £240m (FY2024) |

| AUVs | +28% orderbook FY2024 |

What is included in the product

BCG Matrix review of Babcock: quadrant placements, strategic moves for Stars/Cash Cows/Question Marks/Dogs, investment and divestment guidance.

One-page BCG Matrix placing Babcock units in quadrants for clear portfolio decisions

Cash Cows

Devonport Dockyard Operations

Devonport Dockyard operations deliver steady revenue with a UK market share above 70% in naval ship maintenance and support, generating ~£450m annual revenue in FY2024 and double-digit operating cashflow margins, per Babcock 2024 annual report.

As a mature unit, it needs minimal marketing spend, relies on long-term MoD contracts (multi-year agreements through 2032), and produces predictable free cashflow used to cut net debt (down to £350m in 2024) and fund nuclear and digital investments.

Land Vehicle Fleet Management

Babcock leads UK land vehicle fleet management for the British Army and allied defence clients, supporting c.40,000 vehicles under contract in 2024 and earning recurring service revenues of ~£450m annually.

This mature segment delivers high operating margins (adjusted EBIT margins ~15% in FY 2024), strong free cash flow conversion and economies of scale from centralized spares and depot hubs.

With sector growth near 1–2% annually, the unit supplies stable liquidity for Babcock, funding investments and higher-growth divisions while de-risking group cash flow.

Nuclear Decommissioning Services

The civil nuclear decommissioning unit, covering Sellafield and the Magnox contract, holds a dominant UK market share and operates in a mature market with stable long-term regs; in FY2024 it contributed roughly 25% of Babcock International Group revenue and delivered mid-single-digit operating margins, producing steady free cash flow with low promo spend.

Emergency Medical Aviation

Babcock remains a primary provider of air ambulance and emergency medical services across Europe, operating ~150 helicopters and fixed-wing aircraft in 2025 and serving NHS and regional contracts that generate stable recurring revenue.

These mission-critical services sit in a low-growth, stable market after aviation restructuring, delivering steady margins (EBIT margin ~8–10% in 2024) and predictable cashflow that bolster group liquidity.

The unit’s deep operational expertise lowers unit costs, supports high fleet utilisation (~70% in 2024) and contributes to Babcock’s cash reserves and reinvestment capacity.

- ~150 aircraft

- EBIT margin 8–10% (2024)

- Fleet utilisation ~70% (2024)

- Stable, low-growth market

Technical Training Services

Babcock International’s Technical Training Services delivers large-scale engineering and military training, holding long-term contracts with UK MoD and global industrial clients; FY 2024 training revenue was about £350m, reflecting market leadership in a mature sector.

The unit needs low capital expenditure—estimates show capex under 5% of revenue—so it consistently frees cash for group investment, classifying it as a Cash Cow in the BCG matrix.

- Established contracts with UK MoD and export clients

- FY24 revenue ~£350m

- Capex <5% of revenue

- High margins, steady cash generation

Babcock’s £1.7bn cash cows fuel strong FCF, debt cut and growth

Babcock’s cash cows—Devonport Dockyard, Land Vehicle Services, Civil Nuclear Decommissioning, Air Ambulance, and Technical Training—generate ~£1.7bn recurring FY2024 revenue, strong free cashflow, low capex (<5–10%), and margins 8–15%, funding debt reduction (net debt £350m 2024) and growth investments.

| Unit | FY24 rev (£m) | EBIT margin | Capex % rev | Notes |

|---|---|---|---|---|

| Devonport | 450 | 10–12% | 5% | MoD multiyear contracts to 2032 |

| Land Vehicle | 450 | ~15% | 5% | c.40,000 vehicles |

| Nuclear | ~425 | ~5% | 8–10% | 25% group rev |

| Air Ambulance | ~50 | 8–10% | 10% | ~150 aircraft, utilisation ~70% |

| Training | 350 | High | <5% | Long-term MoD/export contracts |

Delivered as Shown

Babcock International Group BCG Matrix

The file you're previewing on this page is the final BCG Matrix you'll receive after purchase—no watermarks, no demo layers—just a fully formatted, presentation-ready report built for strategic clarity.

This preview exactly matches the downloadable BCG Matrix report you'll get post-purchase, crafted with rigorous analysis and ready to be shared, edited, or printed without further changes.

What you see is the actual document delivered after a one-time purchase, designed by strategy professionals and formatted for immediate use in planning, pitching, or client work.

Once purchased, the same file shown here will be sent straight to your inbox—instantly accessible and free of surprises, ready for integration into your strategic workflow.