Badger Infrastructure Solutions Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

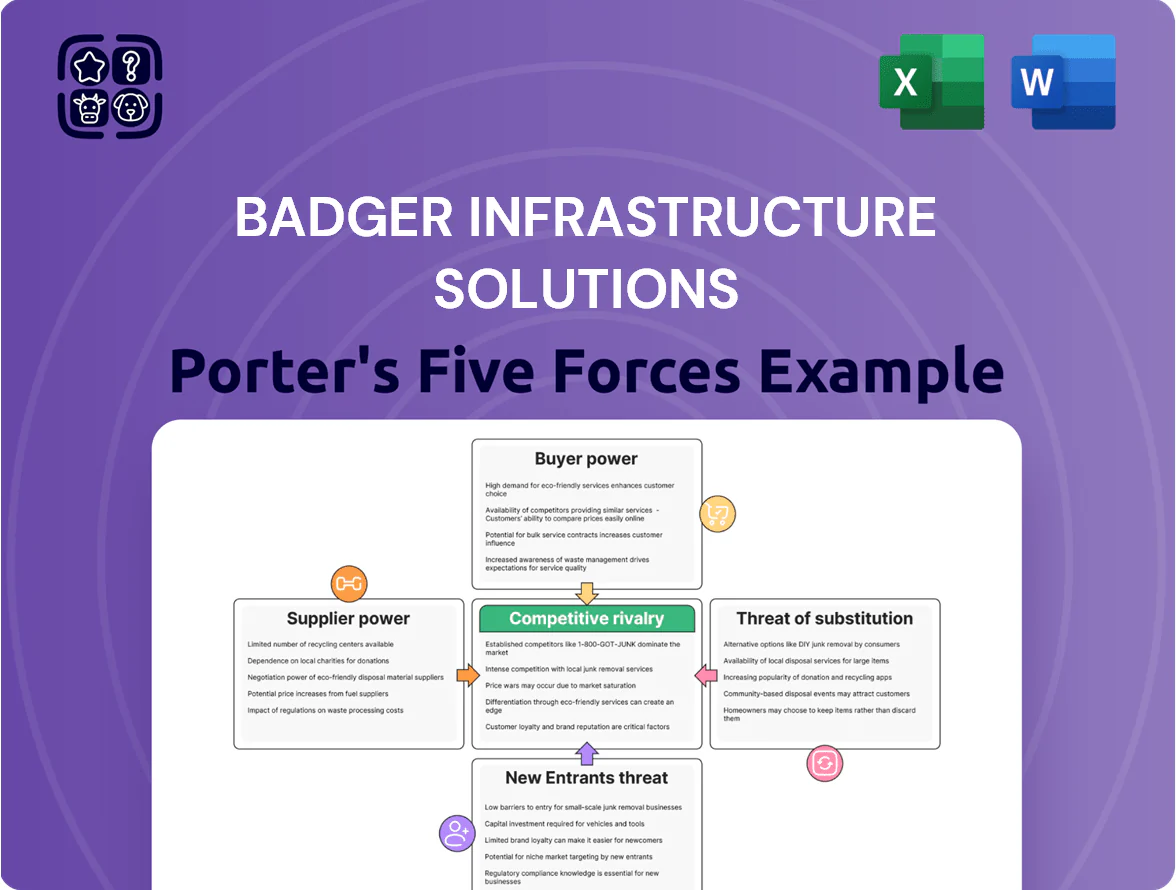

Badger Infrastructure Solutions faces moderate supplier power, high capital barriers for new entrants, and intensifying rivalry from large integrated players, while buyer negotiating strength and substitute threats remain mixed.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Badger Infrastructure Solutions’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Heavy-Duty Truck Manufacturers

The primary chassis for hydrovac units come from a handful of heavy-duty OEMs (Paccar, Daimler Truck, Volvo Group), concentrating supply and giving OEMs pricing and delivery leverage; in 2024 Class 8 truck backlogs averaged ~6–9 months, raising unit costs ~8–12% year-over-year. Badger must sustain preferred-vendor status and negotiate volume/lead-time clauses to hit fleet expansion without >10% capex overrun.

Proprietary Component Dependency

Badger makes its own hydrovac bodies but depends on third-party high-pressure pumps and vacuum blowers that account for ~22% of BOM cost; these parts are specialized and hard to substitute, raising supplier leverage.

Because only ~6 suppliers globally make compatible units, they can stretch lead times—average delivery slipped from 12 to 20 weeks in 2024—hurting Badger’s production cadence and working capital.

Volatility of Energy and Fuel Inputs

The operation of Badger Infrastructure Solutions' fleet consumes millions of liters of diesel annually—roughly 3.2 million liters in 2024—so a 20% rise in diesel prices (as seen in 2022–2023 volatility) can cut margins materially; global oil pricing (Brent crude averaged $82/barrel in 2024) is outside Badger’s control and long-term hedges are costly, leaving suppliers with leverage and forcing the company to rely on customer fuel surcharges to protect operating margins.

Availability of Specialized Labor

The pool of CDL-certified hydrovac operators with technical skills is tight; industry reports in 2024 show vacancy rates for skilled operators near 8–10% and average hourly wages rising 6% year-over-year to about $28–32 in North America.

Labor acts as a supplier of human capital—shortages push Badger Infrastructure Solutions to increase wages, hiring bonuses, and training costs, raising operating margins pressure.

Badger competes with excavation, logistics, and construction firms for the same talent, so turnover and recruitment costs are key risks to service capacity and margins.

- Skilled operator vacancy ~8–10% (2024)

- Avg wage $28–32/hr, +6% YoY (2024)

- Higher recruiting/training costs cut margins

- Competition from logistics/construction firms

Integration of Fleet Telematics and Software

As Badger Infrastructure shifts to digital dispatch and real-time fleet telematics, dependence on a few specialized software vendors increases, giving those suppliers moderate bargaining power due to high switching costs for migrating terabytes of historical GPS/telemetry data and retraining 200+ operators.

Ongoing costs—estimated $1,200–$2,500 per vehicle annually for telematics subscriptions and integrations—make vendor relationships strategically important and create lock-in unless Badger invests in open APIs or in-house platforms.

- Dependence on few vendors raises supplier power

- High switching costs: data migration, retraining

- Typical telematics spend: $1,200–$2,500/vehicle/year

- Open APIs or in-house build reduce lock-in

Suppliers Tighten Grip: Longer Lead Times, Rising Fuel, Labor & Telematics Costs

Suppliers hold moderate-to-high power: concentrated OEM chassis supply (Paccar, Daimler, Volvo) and scarce pumps/blowers raise costs and lead times (Class 8 backlogs 6–9 months; key part delivery 12→20 weeks in 2024), while fuel (Brent $82/bbl 2024) and labor tightness (skilled vacancy 8–10%; wages $28–32/hr, +6% YoY) squeeze margins; telematics vendor lock-in costs $1,200–$2,500/vehicle/year.

| Metric | 2024 |

|---|---|

| Class 8 backlog | 6–9 months |

| Key part lead time | 12→20 weeks |

| Brent crude | $82/bbl |

| Diesel use | 3.2M L |

| Skilled vacancy | 8–10% |

| Avg wage | $28–32/hr (+6% YoY) |

| Telematics spend | $1,200–$2,500/veh/yr |

What is included in the product

Tailored Porter's Five Forces assessment of Badger Infrastructure Solutions, revealing competitive intensity, customer and supplier power, entry barriers, and substitute threats to inform pricing, strategy, and market defense.

One-sheet Porter's Five Forces snapshot for Badger Infrastructure Solutions—quickly pinpoint competitive pressures and prioritize strategic moves.

Customers Bargaining Power

Concentration of Large Utility and Infrastructure Accounts

A large share of Badger Infrastructure Solutions’ revenue comes from national utilities and pipeline operators that control networks worth billions; in 2024 roughly 60–70% of sector spend flowed through the top 10 operators, giving those clients strong bargaining power via volume and long-term contracts. These buyers force competitive bids through formal procurement—RFPs and safety prequalifications—so providers compete on price, safety record, and compliance; winning margins often compress to mid-single digits on major utility projects.

Low Switching Costs for Standard Projects

Stringent Safety and Compliance Requirements

Industrial and energy clients demand impeccable safety ratings and strict environmental compliance, shrinking their vendor pool to certified operators like Badger; for example, 82% of US upstream oil firms in 2024 required ISO 45001 or equivalent for contractors.

This narrow supply raises customer power to set operational KPIs and safety clauses, and 60–70% of midstream contracts in 2023 included penalty tiers tied to compliance breaches.

Sensitivity to Municipal Budget Cycles

Municipal budgets are fixed annually and tied to tax revenues, so 68% of U.S. municipalities reported budget constraints in 2024, forcing procurement to favor the lowest qualified bidder and strengthening customer bargaining power.

Badger must price competitively within public spending limits to win multi-year maintenance contracts; for example, municipal capital outlay fell 3.2% in 2023–24 in many midwestern counties, raising price sensitivity.

- 68% of municipalities report budget limits (2024)

- Procurement often selects lowest qualified bidder

- Badger needs lean pricing to secure multi-year contracts

- Municipal capital outlay down 3.2% in 2023–24 in some regions

Threat of Customer Backward Integration

Buyers Tighten Margins — Badger Needs 70% Utilization & >10% Cost Edge

Large utilities/pipeline clients (60–70% sector spend via top 10, 2024) and strict safety/ISO 45001 rules (82% upstream, 2024) give buyers strong bargaining power; municipal budget limits (68% constrained, 2024) and low switching costs for small jobs (62% to lowest bidder under $50k, 2024) further compress margins—Badger must hit ~70% utilization and >10% cost savings vs. insourcing to retain pricing power.

| Metric | 2023–24 value |

|---|---|

| Top-10 share of sector spend | 60–70% |

| Municipal budget constrained | 68% |

| Small contracts to lowest bidder | 62% |

| ISO 45001 requirement (upstream) | 82% |

| Target utilization to compete | 70% |

| Required outsourcing cost gap | >10% |

Full Version Awaits

Badger Infrastructure Solutions Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Badger Infrastructure Solutions you'll receive upon purchase—no placeholders, no mockups, fully formatted and ready to download for immediate use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Badger Infrastructure Solutions faces moderate supplier power, high capital barriers for new entrants, and intensifying rivalry from large integrated players, while buyer negotiating strength and substitute threats remain mixed.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Badger Infrastructure Solutions’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Heavy-Duty Truck Manufacturers

The primary chassis for hydrovac units come from a handful of heavy-duty OEMs (Paccar, Daimler Truck, Volvo Group), concentrating supply and giving OEMs pricing and delivery leverage; in 2024 Class 8 truck backlogs averaged ~6–9 months, raising unit costs ~8–12% year-over-year. Badger must sustain preferred-vendor status and negotiate volume/lead-time clauses to hit fleet expansion without >10% capex overrun.

Proprietary Component Dependency

Badger makes its own hydrovac bodies but depends on third-party high-pressure pumps and vacuum blowers that account for ~22% of BOM cost; these parts are specialized and hard to substitute, raising supplier leverage.

Because only ~6 suppliers globally make compatible units, they can stretch lead times—average delivery slipped from 12 to 20 weeks in 2024—hurting Badger’s production cadence and working capital.

Volatility of Energy and Fuel Inputs

The operation of Badger Infrastructure Solutions' fleet consumes millions of liters of diesel annually—roughly 3.2 million liters in 2024—so a 20% rise in diesel prices (as seen in 2022–2023 volatility) can cut margins materially; global oil pricing (Brent crude averaged $82/barrel in 2024) is outside Badger’s control and long-term hedges are costly, leaving suppliers with leverage and forcing the company to rely on customer fuel surcharges to protect operating margins.

Availability of Specialized Labor

The pool of CDL-certified hydrovac operators with technical skills is tight; industry reports in 2024 show vacancy rates for skilled operators near 8–10% and average hourly wages rising 6% year-over-year to about $28–32 in North America.

Labor acts as a supplier of human capital—shortages push Badger Infrastructure Solutions to increase wages, hiring bonuses, and training costs, raising operating margins pressure.

Badger competes with excavation, logistics, and construction firms for the same talent, so turnover and recruitment costs are key risks to service capacity and margins.

- Skilled operator vacancy ~8–10% (2024)

- Avg wage $28–32/hr, +6% YoY (2024)

- Higher recruiting/training costs cut margins

- Competition from logistics/construction firms

Integration of Fleet Telematics and Software

As Badger Infrastructure shifts to digital dispatch and real-time fleet telematics, dependence on a few specialized software vendors increases, giving those suppliers moderate bargaining power due to high switching costs for migrating terabytes of historical GPS/telemetry data and retraining 200+ operators.

Ongoing costs—estimated $1,200–$2,500 per vehicle annually for telematics subscriptions and integrations—make vendor relationships strategically important and create lock-in unless Badger invests in open APIs or in-house platforms.

- Dependence on few vendors raises supplier power

- High switching costs: data migration, retraining

- Typical telematics spend: $1,200–$2,500/vehicle/year

- Open APIs or in-house build reduce lock-in

Suppliers Tighten Grip: Longer Lead Times, Rising Fuel, Labor & Telematics Costs

Suppliers hold moderate-to-high power: concentrated OEM chassis supply (Paccar, Daimler, Volvo) and scarce pumps/blowers raise costs and lead times (Class 8 backlogs 6–9 months; key part delivery 12→20 weeks in 2024), while fuel (Brent $82/bbl 2024) and labor tightness (skilled vacancy 8–10%; wages $28–32/hr, +6% YoY) squeeze margins; telematics vendor lock-in costs $1,200–$2,500/vehicle/year.

| Metric | 2024 |

|---|---|

| Class 8 backlog | 6–9 months |

| Key part lead time | 12→20 weeks |

| Brent crude | $82/bbl |

| Diesel use | 3.2M L |

| Skilled vacancy | 8–10% |

| Avg wage | $28–32/hr (+6% YoY) |

| Telematics spend | $1,200–$2,500/veh/yr |

What is included in the product

Tailored Porter's Five Forces assessment of Badger Infrastructure Solutions, revealing competitive intensity, customer and supplier power, entry barriers, and substitute threats to inform pricing, strategy, and market defense.

One-sheet Porter's Five Forces snapshot for Badger Infrastructure Solutions—quickly pinpoint competitive pressures and prioritize strategic moves.

Customers Bargaining Power

Concentration of Large Utility and Infrastructure Accounts

A large share of Badger Infrastructure Solutions’ revenue comes from national utilities and pipeline operators that control networks worth billions; in 2024 roughly 60–70% of sector spend flowed through the top 10 operators, giving those clients strong bargaining power via volume and long-term contracts. These buyers force competitive bids through formal procurement—RFPs and safety prequalifications—so providers compete on price, safety record, and compliance; winning margins often compress to mid-single digits on major utility projects.

Low Switching Costs for Standard Projects

Stringent Safety and Compliance Requirements

Industrial and energy clients demand impeccable safety ratings and strict environmental compliance, shrinking their vendor pool to certified operators like Badger; for example, 82% of US upstream oil firms in 2024 required ISO 45001 or equivalent for contractors.

This narrow supply raises customer power to set operational KPIs and safety clauses, and 60–70% of midstream contracts in 2023 included penalty tiers tied to compliance breaches.

Sensitivity to Municipal Budget Cycles

Municipal budgets are fixed annually and tied to tax revenues, so 68% of U.S. municipalities reported budget constraints in 2024, forcing procurement to favor the lowest qualified bidder and strengthening customer bargaining power.

Badger must price competitively within public spending limits to win multi-year maintenance contracts; for example, municipal capital outlay fell 3.2% in 2023–24 in many midwestern counties, raising price sensitivity.

- 68% of municipalities report budget limits (2024)

- Procurement often selects lowest qualified bidder

- Badger needs lean pricing to secure multi-year contracts

- Municipal capital outlay down 3.2% in 2023–24 in some regions

Threat of Customer Backward Integration

Buyers Tighten Margins — Badger Needs 70% Utilization & >10% Cost Edge

Large utilities/pipeline clients (60–70% sector spend via top 10, 2024) and strict safety/ISO 45001 rules (82% upstream, 2024) give buyers strong bargaining power; municipal budget limits (68% constrained, 2024) and low switching costs for small jobs (62% to lowest bidder under $50k, 2024) further compress margins—Badger must hit ~70% utilization and >10% cost savings vs. insourcing to retain pricing power.

| Metric | 2023–24 value |

|---|---|

| Top-10 share of sector spend | 60–70% |

| Municipal budget constrained | 68% |

| Small contracts to lowest bidder | 62% |

| ISO 45001 requirement (upstream) | 82% |

| Target utilization to compete | 70% |

| Required outsourcing cost gap | >10% |

Full Version Awaits

Badger Infrastructure Solutions Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Badger Infrastructure Solutions you'll receive upon purchase—no placeholders, no mockups, fully formatted and ready to download for immediate use.