Badger Infrastructure Solutions PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Discover how political shifts, infrastructure spending cycles, and emerging technologies are reshaping Badger Infrastructure Solutions’ outlook—our concise PESTLE highlights key external risks and opportunities to inform smarter strategy and investment decisions. Purchase the full analysis for a complete, actionable breakdown you can use in pitches, due diligence, or strategic planning.

Political factors

Federal infrastructure investment and funding

The continued rollout of North American infrastructure bills—over US 1.2 trillion committed since 2021 and US 110B+ for grid and broadband through 2025—generates steady hydrovac demand; Badger Infrastructure Solutions benefits as safe-excavation is mandated for grid modernization and rural broadband builds. These multi-year federal commitments underpin multi-year service contracts with major utilities, supporting revenue predictability and backlog growth.

Cross-border trade and regulatory relations

As Badger operates across Canada and the US, North American trade policy directly affects costs; 2024 steel tariffs (up to 25% on certain imports) could raise fleet component costs by an estimated 3–7% of manufacturing spend, per industry averages. Maintaining status under USMCA and customs facilitation is vital to avoid delays that, in 2025, could add $1,200–$2,500 per cross-border truck move in logistics costs.

Energy transition and permitting policies

Political shifts to renewables drive demand for new underground infrastructure: North American transmission capacity investment needs are estimated at US$500–800bn by 2030, boosting opportunities for Badger in cable and trenching works; however, federal/provincial permitting delays—average approval times rose 15% in Canada (2023–24)—create timeline volatility and potential cost overruns; Badger must manage differing regulatory hurdles between oil/gas pipelines and green-energy transmission projects.

Labor union influence and public sector contracts

The political strength of labor unions in construction and utilities raises baseline wage and safety standards; unionized projects can push labor costs up 8–15% versus nonunion work per recent sector studies (2023–2025).

Government-funded contracts often mandate specific labor agreements and prevailing wages, affecting Badger Infrastructure Solutions’ bid pricing and margins on projects worth over $50M annually.

Active engagement with policymakers and unions helps Badger anticipate changes in public procurement rules and prevailing wage laws, reducing bid risk and compliance costs.

- Union influence can increase labor costs 8–15%

- Public contracts represent projects >$50M annually

- Proactive stakeholder engagement lowers bid and compliance risk

Municipal zoning and urban development priorities

Local urban densification and smart city projects increased trenchless work demand by 18% in 2024, driving need for non-destructive excavation in congested corridors.

City councils mandating hydrovac over mechanical digging to protect fiber and water networks—cited in 2023 ordinances across 42 US municipalities—favor Badger’s service model.

Ordinances prioritizing minimal public service disruption reduce project delays and cost overruns, supporting Badger’s revenue stability and higher margin bids.

- 2024 demand +18%

- 42 municipalities with hydrovac mandates (2023)

- Lower delays = improved margins

Infrastructure surge boosts hydrovac demand amid higher steel, labor costs and permitting delays

Federal infrastructure bills (US$1.2T+ since 2021; US$110B+ for grid/broadband to 2025) and US transmission needs (US$500–800B by 2030) drive hydrovac demand; 2024 steel tariffs (up to 25%) may raise component costs ~3–7%. Unionized projects increase labor costs 8–15% and public contracts (>US$50M) impose prevailing wages; 2023–24 permitting delays rose ~15%, affecting timelines.

| Metric | Value |

|---|---|

| Federal infrastructure committed | US$1.2T+ |

| Grid/broadband funding | US$110B+ |

| Transmission need by 2030 | US$500–800B |

| Steel tariffs (2024) | up to 25% |

| Labor cost uplift (union) | 8–15% |

| Permitting delay increase (2023–24) | ~15% |

What is included in the product

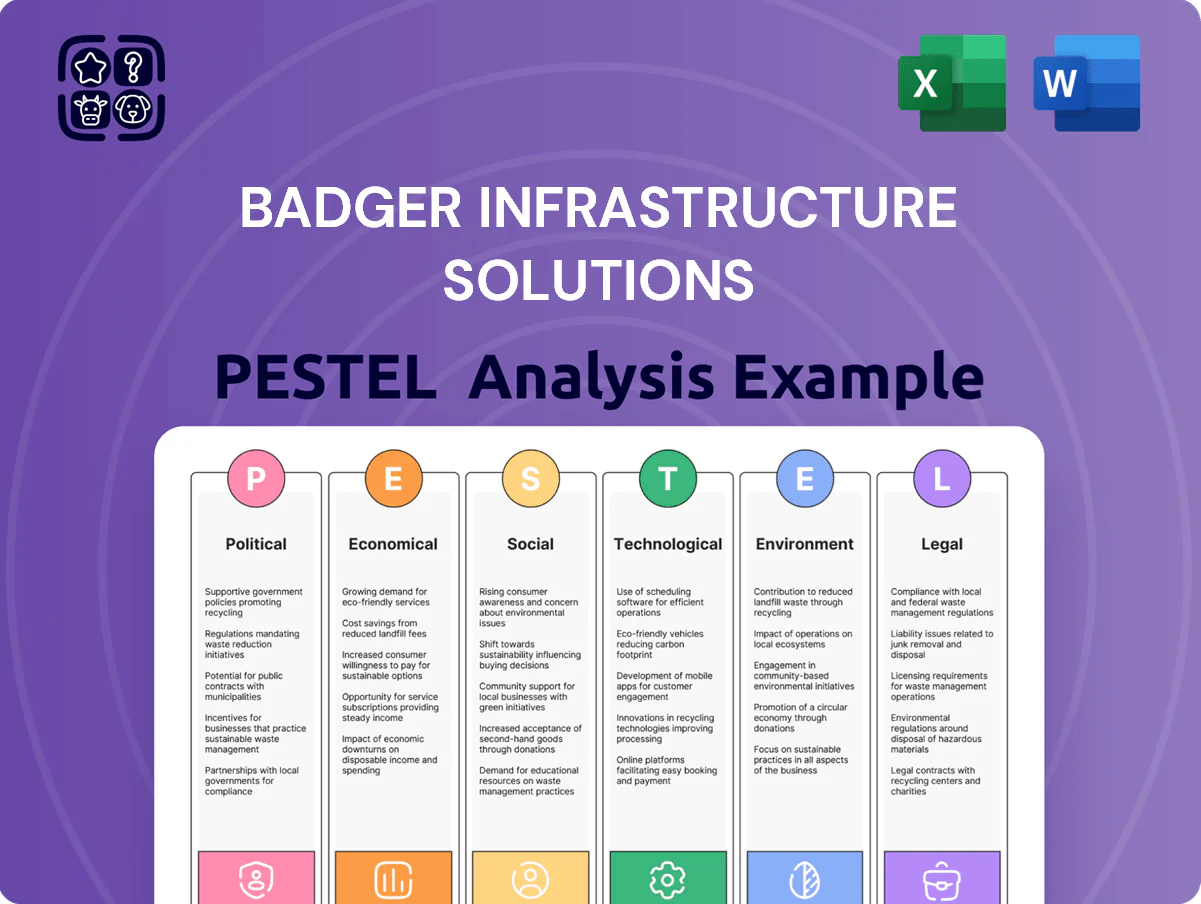

Explores how macro-environmental factors uniquely affect Badger Infrastructure Solutions across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section tied to current regional and industry trends to identify risks and opportunities.

A concise, visually segmented PESTLE summary tailored for Badger Infrastructure Solutions that eases meeting prep, supports quick risk discussions, and can be dropped into presentations or shared across teams for fast alignment.

Economic factors

Interest rate environment and capital expenditure

The cost of borrowing remains critical for Badger as it finances its proprietary fleet; with US 10-year Treasury yields averaging ~4.2% in 2024 and banks pricing prime/commercial loans near 7–9%, interest expense has pressured margins on capital-intensive equipment purchases.

High rates through 2025 raised weighted average cost of capital for fleet upgrades, increasing annual financing costs by an estimated $20–40m versus a low-rate scenario.

Any stabilization—markets pricing Fed funds nearer 4.5% by late 2025—could prompt utilities to accelerate deferred maintenance, supporting demand for Badger’s rental and service offerings.

Labor market shortages and wage inflation

The specialized nature of hydrovac operations demands skilled operators to handle complex machinery and safety protocols, and US Bureau of Labor Statistics data through 2024 shows heavy equipment operator employment up 1.8% while construction vacancies remained historically high, tightening supply. Wage inflation pressures the sector—average hourly wages for heavy equipment operators rose about 6.5% YoY in 2023–24—raising recruitment costs. Badger must invest in training, apprenticeships, and retention programs to offset a shrinking qualified labor pool and limit overtime and contractor premiums that can erode margins.

Energy and fuel price volatility

Badger’s hydrovac fleet consumes large diesel volumes, making margins tied to oil: Brent averaged about 82 USD/bbl in 2024, and diesel retail rose ~14% YOY in the US through Q3 2024, pressuring operating margins.

Fuel surcharges mitigate some risk, but rapid spikes—like the 2022 crude jump where diesel rack prices rose 40% in months—can compress margins short-term.

Badger is exploring alternative fuels and electrification pilots; industry estimates suggest switching to lower-carbon fuels could cut fuel cost volatility exposure by 20–30% over a decade.

Utility and industrial capital spending cycles

The financial health of major utilities and industrial firms drives Badger Infrastructure Solutions’ workload; for example, US electric utilities invested about $136 billion in T&D in 2023 and projected 3–4% annual growth through 2025, boosting potential contracts.

In downturns clients delay non-essential maintenance—industrial capex fell 8% in 2023—but emergency repairs remain steady, typically 15–25% of service revenue.

Strong telecom and power sector forecasts, with global power capex rising to ~$540 billion in 2024, generally increase demand for Badger’s services.

- Utilities T&D spend: $136B (US, 2023); 3–4% growth to 2025

- Industrial capex drop: −8% (2023) but emergency work = 15–25% revenue

- Global power capex: ~$540B (2024) → higher service demand

Inflationary pressure on parts and manufacturing

Inflation raised commodity and component costs 6.2% year-over-year in 2024, pushing prices for hydraulic systems, high-pressure pumps, and truck chassis up 7–10%, pressuring margins on Badger’s proprietary hydrovac units.

Disciplined pricing and a 3–5% productivity target in manufacturing are required to offset input-cost inflation and preserve gross margins.

Efficient supply-chain management—leveraging longer-term supplier contracts and inventory hedging—remains essential to economic viability of the internal manufacturing division.

- 2024 U.S. core PCE +4.1% YoY; parts/components +7–10%

- Target 3–5% productivity gains to offset inflation

- Long-term contracts and hedging reduce input volatility

Rising rates, diesel spikes and wages squeeze margins; T&D demand offsets weaker industrial capex

Rising borrowing costs (US 10y ~4.2% in 2024; bank loans ~7–9%) and diesel volatility (Brent ~$82/bbl, diesel +14% YTD 2024) pressure margins; wage inflation for heavy equipment operators rose ~6.5% YoY. Utilities T&D spend ($136B US, 2023; +3–4% to 2025) supports demand but industrial capex down −8% (2023). Productivity gains (3–5%) and supply contracts/hedging are required to protect margins.

| Metric | 2023–24 |

|---|---|

| US 10y yield | ~4.2% |

| Bank loan rates | 7–9% |

| Brent | $82/bbl (2024) |

| Diesel change | +14% YTD 2024 |

| Heavy operator wage | +6.5% YoY |

| US utilities T&D | $136B (2023) |

| Industrial capex | −8% (2023) |

What You See Is What You Get

Badger Infrastructure Solutions PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This Badger Infrastructure Solutions PESTLE analysis provides actionable insights on political, economic, social, technological, legal, and environmental factors relevant to strategic decision-making. The layout, content, and structure visible here are exactly what you’ll download immediately after buying. No placeholders or surprises—this is the final, professionally structured file.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Discover how political shifts, infrastructure spending cycles, and emerging technologies are reshaping Badger Infrastructure Solutions’ outlook—our concise PESTLE highlights key external risks and opportunities to inform smarter strategy and investment decisions. Purchase the full analysis for a complete, actionable breakdown you can use in pitches, due diligence, or strategic planning.

Political factors

Federal infrastructure investment and funding

The continued rollout of North American infrastructure bills—over US 1.2 trillion committed since 2021 and US 110B+ for grid and broadband through 2025—generates steady hydrovac demand; Badger Infrastructure Solutions benefits as safe-excavation is mandated for grid modernization and rural broadband builds. These multi-year federal commitments underpin multi-year service contracts with major utilities, supporting revenue predictability and backlog growth.

Cross-border trade and regulatory relations

As Badger operates across Canada and the US, North American trade policy directly affects costs; 2024 steel tariffs (up to 25% on certain imports) could raise fleet component costs by an estimated 3–7% of manufacturing spend, per industry averages. Maintaining status under USMCA and customs facilitation is vital to avoid delays that, in 2025, could add $1,200–$2,500 per cross-border truck move in logistics costs.

Energy transition and permitting policies

Political shifts to renewables drive demand for new underground infrastructure: North American transmission capacity investment needs are estimated at US$500–800bn by 2030, boosting opportunities for Badger in cable and trenching works; however, federal/provincial permitting delays—average approval times rose 15% in Canada (2023–24)—create timeline volatility and potential cost overruns; Badger must manage differing regulatory hurdles between oil/gas pipelines and green-energy transmission projects.

Labor union influence and public sector contracts

The political strength of labor unions in construction and utilities raises baseline wage and safety standards; unionized projects can push labor costs up 8–15% versus nonunion work per recent sector studies (2023–2025).

Government-funded contracts often mandate specific labor agreements and prevailing wages, affecting Badger Infrastructure Solutions’ bid pricing and margins on projects worth over $50M annually.

Active engagement with policymakers and unions helps Badger anticipate changes in public procurement rules and prevailing wage laws, reducing bid risk and compliance costs.

- Union influence can increase labor costs 8–15%

- Public contracts represent projects >$50M annually

- Proactive stakeholder engagement lowers bid and compliance risk

Municipal zoning and urban development priorities

Local urban densification and smart city projects increased trenchless work demand by 18% in 2024, driving need for non-destructive excavation in congested corridors.

City councils mandating hydrovac over mechanical digging to protect fiber and water networks—cited in 2023 ordinances across 42 US municipalities—favor Badger’s service model.

Ordinances prioritizing minimal public service disruption reduce project delays and cost overruns, supporting Badger’s revenue stability and higher margin bids.

- 2024 demand +18%

- 42 municipalities with hydrovac mandates (2023)

- Lower delays = improved margins

Infrastructure surge boosts hydrovac demand amid higher steel, labor costs and permitting delays

Federal infrastructure bills (US$1.2T+ since 2021; US$110B+ for grid/broadband to 2025) and US transmission needs (US$500–800B by 2030) drive hydrovac demand; 2024 steel tariffs (up to 25%) may raise component costs ~3–7%. Unionized projects increase labor costs 8–15% and public contracts (>US$50M) impose prevailing wages; 2023–24 permitting delays rose ~15%, affecting timelines.

| Metric | Value |

|---|---|

| Federal infrastructure committed | US$1.2T+ |

| Grid/broadband funding | US$110B+ |

| Transmission need by 2030 | US$500–800B |

| Steel tariffs (2024) | up to 25% |

| Labor cost uplift (union) | 8–15% |

| Permitting delay increase (2023–24) | ~15% |

What is included in the product

Explores how macro-environmental factors uniquely affect Badger Infrastructure Solutions across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section tied to current regional and industry trends to identify risks and opportunities.

A concise, visually segmented PESTLE summary tailored for Badger Infrastructure Solutions that eases meeting prep, supports quick risk discussions, and can be dropped into presentations or shared across teams for fast alignment.

Economic factors

Interest rate environment and capital expenditure

The cost of borrowing remains critical for Badger as it finances its proprietary fleet; with US 10-year Treasury yields averaging ~4.2% in 2024 and banks pricing prime/commercial loans near 7–9%, interest expense has pressured margins on capital-intensive equipment purchases.

High rates through 2025 raised weighted average cost of capital for fleet upgrades, increasing annual financing costs by an estimated $20–40m versus a low-rate scenario.

Any stabilization—markets pricing Fed funds nearer 4.5% by late 2025—could prompt utilities to accelerate deferred maintenance, supporting demand for Badger’s rental and service offerings.

Labor market shortages and wage inflation

The specialized nature of hydrovac operations demands skilled operators to handle complex machinery and safety protocols, and US Bureau of Labor Statistics data through 2024 shows heavy equipment operator employment up 1.8% while construction vacancies remained historically high, tightening supply. Wage inflation pressures the sector—average hourly wages for heavy equipment operators rose about 6.5% YoY in 2023–24—raising recruitment costs. Badger must invest in training, apprenticeships, and retention programs to offset a shrinking qualified labor pool and limit overtime and contractor premiums that can erode margins.

Energy and fuel price volatility

Badger’s hydrovac fleet consumes large diesel volumes, making margins tied to oil: Brent averaged about 82 USD/bbl in 2024, and diesel retail rose ~14% YOY in the US through Q3 2024, pressuring operating margins.

Fuel surcharges mitigate some risk, but rapid spikes—like the 2022 crude jump where diesel rack prices rose 40% in months—can compress margins short-term.

Badger is exploring alternative fuels and electrification pilots; industry estimates suggest switching to lower-carbon fuels could cut fuel cost volatility exposure by 20–30% over a decade.

Utility and industrial capital spending cycles

The financial health of major utilities and industrial firms drives Badger Infrastructure Solutions’ workload; for example, US electric utilities invested about $136 billion in T&D in 2023 and projected 3–4% annual growth through 2025, boosting potential contracts.

In downturns clients delay non-essential maintenance—industrial capex fell 8% in 2023—but emergency repairs remain steady, typically 15–25% of service revenue.

Strong telecom and power sector forecasts, with global power capex rising to ~$540 billion in 2024, generally increase demand for Badger’s services.

- Utilities T&D spend: $136B (US, 2023); 3–4% growth to 2025

- Industrial capex drop: −8% (2023) but emergency work = 15–25% revenue

- Global power capex: ~$540B (2024) → higher service demand

Inflationary pressure on parts and manufacturing

Inflation raised commodity and component costs 6.2% year-over-year in 2024, pushing prices for hydraulic systems, high-pressure pumps, and truck chassis up 7–10%, pressuring margins on Badger’s proprietary hydrovac units.

Disciplined pricing and a 3–5% productivity target in manufacturing are required to offset input-cost inflation and preserve gross margins.

Efficient supply-chain management—leveraging longer-term supplier contracts and inventory hedging—remains essential to economic viability of the internal manufacturing division.

- 2024 U.S. core PCE +4.1% YoY; parts/components +7–10%

- Target 3–5% productivity gains to offset inflation

- Long-term contracts and hedging reduce input volatility

Rising rates, diesel spikes and wages squeeze margins; T&D demand offsets weaker industrial capex

Rising borrowing costs (US 10y ~4.2% in 2024; bank loans ~7–9%) and diesel volatility (Brent ~$82/bbl, diesel +14% YTD 2024) pressure margins; wage inflation for heavy equipment operators rose ~6.5% YoY. Utilities T&D spend ($136B US, 2023; +3–4% to 2025) supports demand but industrial capex down −8% (2023). Productivity gains (3–5%) and supply contracts/hedging are required to protect margins.

| Metric | 2023–24 |

|---|---|

| US 10y yield | ~4.2% |

| Bank loan rates | 7–9% |

| Brent | $82/bbl (2024) |

| Diesel change | +14% YTD 2024 |

| Heavy operator wage | +6.5% YoY |

| US utilities T&D | $136B (2023) |

| Industrial capex | −8% (2023) |

What You See Is What You Get

Badger Infrastructure Solutions PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This Badger Infrastructure Solutions PESTLE analysis provides actionable insights on political, economic, social, technological, legal, and environmental factors relevant to strategic decision-making. The layout, content, and structure visible here are exactly what you’ll download immediately after buying. No placeholders or surprises—this is the final, professionally structured file.