Royal Bafokeng Platinum SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

Royal Bafokeng Platinum shows resilient operational strengths and unique stakeholder integration but faces commodity volatility and capital intensity that could constrain expansion; our full SWOT unpacks strategic levers, regulatory risks, and value-creation opportunities for investors and managers. Purchase the complete SWOT analysis to receive a professionally formatted Word report and editable Excel matrix—research-backed, ready for planning, pitching, and execution.

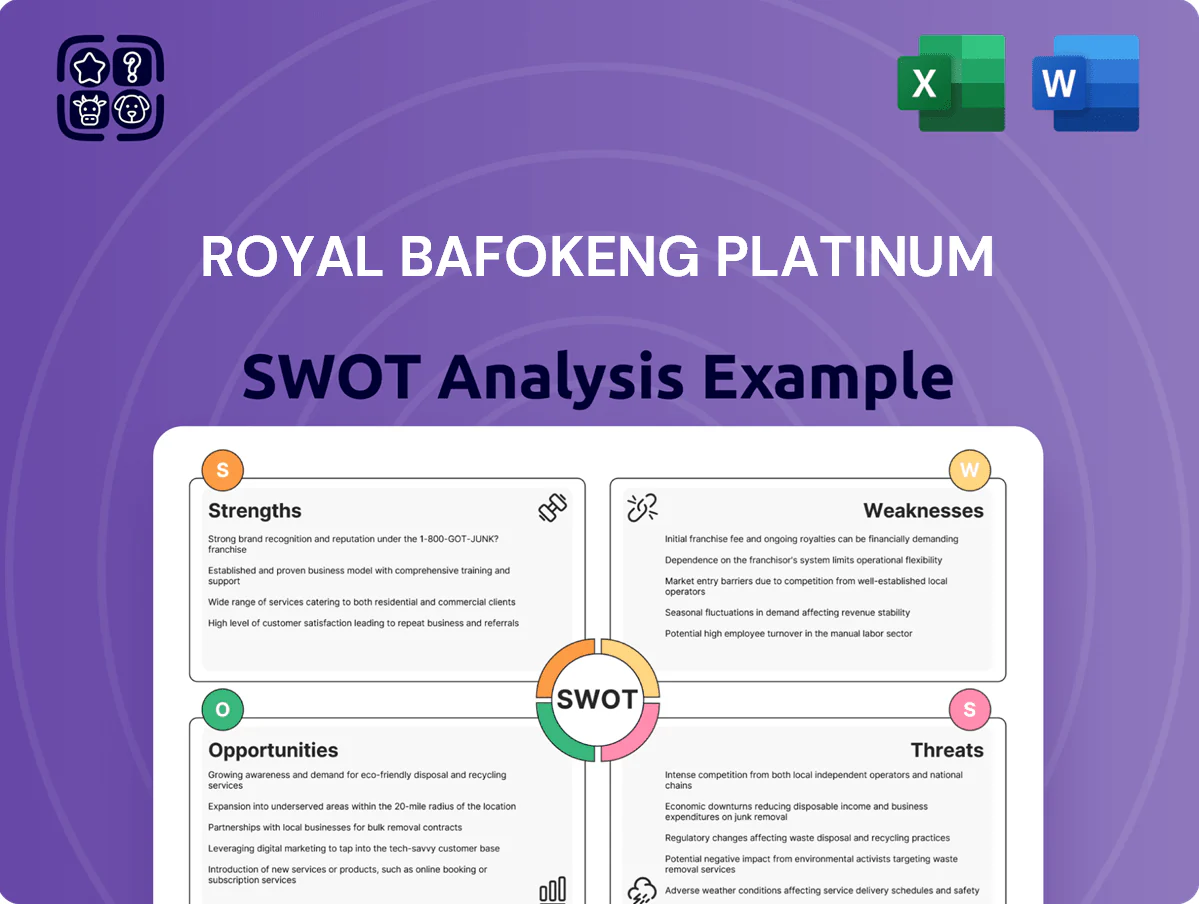

Strengths

Fully Integrated Synergy with Implats

As of late 2025, integration with Impala Platinum (Implats) gives Royal Bafokeng Platinum (RBPlat) stronger balance-sheet backing—Implats’ pro forma net debt/EBITDA fell to about 1.1x in 2025—supporting a larger R&D and capex pool for Rustenburg assets.

Shared services cut overlap: combined SG&A synergies target ~R1.2bn annual savings, while pooled technical teams lift mill throughput utilization to ~88%, improving ore flow and processing versus standalone operations.

High Grade Merensky Reef Reserves

The Royal Bafokeng Platinum (RBPlat) deposits hold a high proportion of Merensky reef, which carries average 4E (Pt+Pd+Rh+Au) grades around 4.2 g/t versus UG2’s ~3.0 g/t in the Bushveld Complex, supporting stronger head grades and cash margins. This grade mix helped RBPlat report 2024 unit cash costs of ~US$750/oz against a 4E basket price near US$1,750/oz, preserving profitability in weaker PGM cycles. Superior ore quality underpins long‑term mine life and lower strip ratios, keeping project economics resilient. What this hides: capital intensity for deepening still rises with time.

Low Cost Mechanized Operations at Styldrift

Styldrift is one of South Africa’s most modern mechanized platinum mines in 2025, with mechanisation lifting productivity to about 1.8 tonnes output per employee per shift vs 1.1 sector average and cutting unit cash costs to roughly $420/oz (2024 actuals).

Established ESG and Community Relations

Royal Bafokeng Platinum (RBPlat) holds a strong social license within the Bafokeng nation, backed by RBP investments: R1.2bn community spend 2024 and a 15% local procurement rate in 2024 that cut community-disruption risk versus peers.

The company's long-term sustainable-development focus remains central to operations under current management, with 2024 safety LTIFR 0.08 and a 12% reduction in Scope 1 emissions since 2021.

- R1.2bn community spend 2024

- 15% local procurement 2024

- LTIFR 0.08 (2024)

- Scope 1 emissions -12% since 2021

Strategic Proximity to Existing Infrastructure

Proximity to Impala Platinum smelter/refinery in Rustenburg cuts heavy logistics: Royal Bafokeng Platinum (RBPlat) likely saves millions in transport—rough estimate US$5–15/tonne in trucking, equating to ~US$10–30m annual savings given 2–2.5mtpa ore moved.

Established roads, rail links and utilities speed ore-to-metal turnaround, shortening processing lead times by weeks and trimming working-capital needs; shorter hauls also reduce Scope 3 emissions, roughly 10–25% lower per tonne versus long-haul peers.

- Lower transport cost: est US$10–30m/year

- Throughput boost: weeks faster processing

- Scope 3 emissions cut: ~10–25%/tonne

RBPlat: Low costs, high grades and Implats-backed balance sheet drive strong margins

RBPlat benefits from Implats’ stronger balance sheet (pro forma net debt/EBITDA ~1.1x in 2025), R1.2bn community spend (2024), high Merensky 4E grades ~4.2 g/t boosting margins (2024 unit cash cost ~US$750/oz vs 4E price ~US$1,750/oz), Styldrift mechanisation (1.8 t/emp/shift; unit cash cost ~US$420/oz), and logistics proximity saving est US$10–30m/yr.

| Metric | Value |

|---|---|

| Net debt/EBITDA (2025) | ~1.1x |

| Community spend (2024) | R1.2bn |

| Merensky 4E grade | ~4.2 g/t |

| Unit cash cost (2024) | US$750/oz |

| Styldrift productivity | 1.8 t/emp/shift |

| Logistics saving | US$10–30m/yr |

What is included in the product

Provides a concise SWOT overview of Royal Bafokeng Platinum, highlighting its operational strengths, financial and environmental challenges, strategic growth opportunities in PGM markets and downstream diversification, and external risks such as commodity price volatility, regulatory changes, and mining sector disruptions.

Provides a concise SWOT snapshot of Royal Bafokeng Platinum for rapid strategic alignment and stakeholder-ready summaries.

Weaknesses

Exposure to South African Power Instability

Reliance on Eskom’s national grid exposes Royal Bafokeng Platinum to frequent load curtailment that cut production; RBPlat reported 3% lower 2024 platinum-group metals output partly due to power interruptions. Ongoing self-generation projects target 200 MW but remain phased, so grid dependence still causes short-term losses. Eskom tariff increases averaged ~12% in 2024, well above South Africa’s 4.9% CPI, squeezing margins and raising operating costs.

High Capital Expenditure for Deep Level Mining

Maintaining Royal Bafokeng Platinum’s deep-level mines requires steady capital reinvestment for safety and ventilation; RBPlat reported sustaining capex of R1.2bn in H1 2025, up 18% year-on-year, reflecting this need. As shafts age, reaching deeper PGM (platinum-group metals) reefs raises extraction costs, squeezing margins—unit cash costs rose to R7,800/t in 2024. These ongoing expenditures make RBPlat’s projects sensitive to metal prices; breakeven PGM basket prices exceed $1,100/oz. Investors demand higher price tails to justify funding deep capital cycles.

Single Region Geographic Concentration

The operations are almost entirely concentrated in the Rustenburg and Phokeng areas of the North West Province, so localized shocks—like the 2023 community protests that cut regional output by an estimated 8%—directly hit 100% of production; unlike diversified global miners (Anglo Platinum had 2024 output from 3 countries), RBPlat lacks geographic hedges, raising its subsidiary risk and contributing to a higher country-concentration premium in valuation models.

Complexity of Post Acquisition Integration

The complexity of post-acquisition integration has left legacy corporate cultures and technical systems misaligned with parent processes, causing delays in IT consolidation and ERP harmonisation that raised integration costs by an estimated R120–R180 million in 2024.

Discrepancies in historical labor agreements and management structures created internal friction and administrative slowdowns, contributing to a reported 6–8% drop in operational availability in 2024 versus pre-acquisition levels.

By end-2025, these organizational hurdles still need active management to prevent ongoing efficiency leaks and preserve projected EBITDA margins; failure could shave 150–250 bps from margin forecasts.

- Legacy IT/ERP misalignments: R120–R180m extra cost (2024)

- Labor/management discrepancies: 6–8% lower availability (2024)

- Risk to EBITDA: potential 150–250 basis-point erosion by end-2025

Susceptibility to PGM Price Fluctuations

The business remains highly sensitive to volatile spot prices for platinum, palladium and rhodium; in 2024 rhodium spiked >40% y/y while platinum fell ~6% y/y, swinging revenue materially for Royal Bafokeng Platinum (RBPlat).

Limited revenue diversification means a 10% drop in automotive demand can cut cash flow sharply; RBPlat’s FY2024 revenue depended on PGMs for over 85% of sales, amplifying downturn risk.

That cyclicality makes long-term planning and dividend visibility hard—RBPlat paid a special dividend in 2023 but suspended regular increases in 2024 as net cash and price volatility tightened capital allocation.

- 85%+ revenue from PGMs (FY2024)

- Rhodium +40% y/y (2024); platinum -6% y/y (2024)

- Dividend consistency disrupted 2024

Power woes, rising costs and deep‑mine strain threaten Rustenburg PGM margins

High grid reliance: Eskom curtailments cut output (PGM production -3% in 2024); 200 MW self-gen phased. Rising power costs: Eskom tariffs ~12% (2024) vs SA CPI 4.9%. Deep-mine cost pressure: sustaining capex R1.2bn H1 2025 (+18% YoY); unit cash costs R7,800/t (2024); breakeven PGM basket > $1,100/oz. Concentration risk: 100% Rustenburg/Phokeng; 2023 protests cut regional output ~8%.

| Metric | Value |

|---|---|

| Eskom tariff (2024) | ~12% |

| SA CPI (2024) | 4.9% |

| Sustaining capex | R1.2bn H1 2025 |

| Unit cash cost (2024) | R7,800/t |

| PGM revenue share (FY2024) | 85%+ |

Preview Before You Purchase

Royal Bafokeng Platinum SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality; the preview below is taken directly from the full report you'll get, and once bought the complete, editable version becomes available for download.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Dive Deeper Into the Company’s Strategic Blueprint

Royal Bafokeng Platinum shows resilient operational strengths and unique stakeholder integration but faces commodity volatility and capital intensity that could constrain expansion; our full SWOT unpacks strategic levers, regulatory risks, and value-creation opportunities for investors and managers. Purchase the complete SWOT analysis to receive a professionally formatted Word report and editable Excel matrix—research-backed, ready for planning, pitching, and execution.

Strengths

Fully Integrated Synergy with Implats

As of late 2025, integration with Impala Platinum (Implats) gives Royal Bafokeng Platinum (RBPlat) stronger balance-sheet backing—Implats’ pro forma net debt/EBITDA fell to about 1.1x in 2025—supporting a larger R&D and capex pool for Rustenburg assets.

Shared services cut overlap: combined SG&A synergies target ~R1.2bn annual savings, while pooled technical teams lift mill throughput utilization to ~88%, improving ore flow and processing versus standalone operations.

High Grade Merensky Reef Reserves

The Royal Bafokeng Platinum (RBPlat) deposits hold a high proportion of Merensky reef, which carries average 4E (Pt+Pd+Rh+Au) grades around 4.2 g/t versus UG2’s ~3.0 g/t in the Bushveld Complex, supporting stronger head grades and cash margins. This grade mix helped RBPlat report 2024 unit cash costs of ~US$750/oz against a 4E basket price near US$1,750/oz, preserving profitability in weaker PGM cycles. Superior ore quality underpins long‑term mine life and lower strip ratios, keeping project economics resilient. What this hides: capital intensity for deepening still rises with time.

Low Cost Mechanized Operations at Styldrift

Styldrift is one of South Africa’s most modern mechanized platinum mines in 2025, with mechanisation lifting productivity to about 1.8 tonnes output per employee per shift vs 1.1 sector average and cutting unit cash costs to roughly $420/oz (2024 actuals).

Established ESG and Community Relations

Royal Bafokeng Platinum (RBPlat) holds a strong social license within the Bafokeng nation, backed by RBP investments: R1.2bn community spend 2024 and a 15% local procurement rate in 2024 that cut community-disruption risk versus peers.

The company's long-term sustainable-development focus remains central to operations under current management, with 2024 safety LTIFR 0.08 and a 12% reduction in Scope 1 emissions since 2021.

- R1.2bn community spend 2024

- 15% local procurement 2024

- LTIFR 0.08 (2024)

- Scope 1 emissions -12% since 2021

Strategic Proximity to Existing Infrastructure

Proximity to Impala Platinum smelter/refinery in Rustenburg cuts heavy logistics: Royal Bafokeng Platinum (RBPlat) likely saves millions in transport—rough estimate US$5–15/tonne in trucking, equating to ~US$10–30m annual savings given 2–2.5mtpa ore moved.

Established roads, rail links and utilities speed ore-to-metal turnaround, shortening processing lead times by weeks and trimming working-capital needs; shorter hauls also reduce Scope 3 emissions, roughly 10–25% lower per tonne versus long-haul peers.

- Lower transport cost: est US$10–30m/year

- Throughput boost: weeks faster processing

- Scope 3 emissions cut: ~10–25%/tonne

RBPlat: Low costs, high grades and Implats-backed balance sheet drive strong margins

RBPlat benefits from Implats’ stronger balance sheet (pro forma net debt/EBITDA ~1.1x in 2025), R1.2bn community spend (2024), high Merensky 4E grades ~4.2 g/t boosting margins (2024 unit cash cost ~US$750/oz vs 4E price ~US$1,750/oz), Styldrift mechanisation (1.8 t/emp/shift; unit cash cost ~US$420/oz), and logistics proximity saving est US$10–30m/yr.

| Metric | Value |

|---|---|

| Net debt/EBITDA (2025) | ~1.1x |

| Community spend (2024) | R1.2bn |

| Merensky 4E grade | ~4.2 g/t |

| Unit cash cost (2024) | US$750/oz |

| Styldrift productivity | 1.8 t/emp/shift |

| Logistics saving | US$10–30m/yr |

What is included in the product

Provides a concise SWOT overview of Royal Bafokeng Platinum, highlighting its operational strengths, financial and environmental challenges, strategic growth opportunities in PGM markets and downstream diversification, and external risks such as commodity price volatility, regulatory changes, and mining sector disruptions.

Provides a concise SWOT snapshot of Royal Bafokeng Platinum for rapid strategic alignment and stakeholder-ready summaries.

Weaknesses

Exposure to South African Power Instability

Reliance on Eskom’s national grid exposes Royal Bafokeng Platinum to frequent load curtailment that cut production; RBPlat reported 3% lower 2024 platinum-group metals output partly due to power interruptions. Ongoing self-generation projects target 200 MW but remain phased, so grid dependence still causes short-term losses. Eskom tariff increases averaged ~12% in 2024, well above South Africa’s 4.9% CPI, squeezing margins and raising operating costs.

High Capital Expenditure for Deep Level Mining

Maintaining Royal Bafokeng Platinum’s deep-level mines requires steady capital reinvestment for safety and ventilation; RBPlat reported sustaining capex of R1.2bn in H1 2025, up 18% year-on-year, reflecting this need. As shafts age, reaching deeper PGM (platinum-group metals) reefs raises extraction costs, squeezing margins—unit cash costs rose to R7,800/t in 2024. These ongoing expenditures make RBPlat’s projects sensitive to metal prices; breakeven PGM basket prices exceed $1,100/oz. Investors demand higher price tails to justify funding deep capital cycles.

Single Region Geographic Concentration

The operations are almost entirely concentrated in the Rustenburg and Phokeng areas of the North West Province, so localized shocks—like the 2023 community protests that cut regional output by an estimated 8%—directly hit 100% of production; unlike diversified global miners (Anglo Platinum had 2024 output from 3 countries), RBPlat lacks geographic hedges, raising its subsidiary risk and contributing to a higher country-concentration premium in valuation models.

Complexity of Post Acquisition Integration

The complexity of post-acquisition integration has left legacy corporate cultures and technical systems misaligned with parent processes, causing delays in IT consolidation and ERP harmonisation that raised integration costs by an estimated R120–R180 million in 2024.

Discrepancies in historical labor agreements and management structures created internal friction and administrative slowdowns, contributing to a reported 6–8% drop in operational availability in 2024 versus pre-acquisition levels.

By end-2025, these organizational hurdles still need active management to prevent ongoing efficiency leaks and preserve projected EBITDA margins; failure could shave 150–250 bps from margin forecasts.

- Legacy IT/ERP misalignments: R120–R180m extra cost (2024)

- Labor/management discrepancies: 6–8% lower availability (2024)

- Risk to EBITDA: potential 150–250 basis-point erosion by end-2025

Susceptibility to PGM Price Fluctuations

The business remains highly sensitive to volatile spot prices for platinum, palladium and rhodium; in 2024 rhodium spiked >40% y/y while platinum fell ~6% y/y, swinging revenue materially for Royal Bafokeng Platinum (RBPlat).

Limited revenue diversification means a 10% drop in automotive demand can cut cash flow sharply; RBPlat’s FY2024 revenue depended on PGMs for over 85% of sales, amplifying downturn risk.

That cyclicality makes long-term planning and dividend visibility hard—RBPlat paid a special dividend in 2023 but suspended regular increases in 2024 as net cash and price volatility tightened capital allocation.

- 85%+ revenue from PGMs (FY2024)

- Rhodium +40% y/y (2024); platinum -6% y/y (2024)

- Dividend consistency disrupted 2024

Power woes, rising costs and deep‑mine strain threaten Rustenburg PGM margins

High grid reliance: Eskom curtailments cut output (PGM production -3% in 2024); 200 MW self-gen phased. Rising power costs: Eskom tariffs ~12% (2024) vs SA CPI 4.9%. Deep-mine cost pressure: sustaining capex R1.2bn H1 2025 (+18% YoY); unit cash costs R7,800/t (2024); breakeven PGM basket > $1,100/oz. Concentration risk: 100% Rustenburg/Phokeng; 2023 protests cut regional output ~8%.

| Metric | Value |

|---|---|

| Eskom tariff (2024) | ~12% |

| SA CPI (2024) | 4.9% |

| Sustaining capex | R1.2bn H1 2025 |

| Unit cash cost (2024) | R7,800/t |

| PGM revenue share (FY2024) | 85%+ |

Preview Before You Purchase

Royal Bafokeng Platinum SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality; the preview below is taken directly from the full report you'll get, and once bought the complete, editable version becomes available for download.